The cost of the wafer is a substantial part of the total cost of solar cells. In the course of the analysis, a number of research and development points have been identified.

TARGETS AND MILESTONES FOR EPIA ROADMAP

Promote the export of European technology, especially to the rural electrification market in developing countries. Fostering partnerships between European industry and companies in developing countries to develop products for this particular market is essential.

1 EXECUTIVE SUMMARY

CONCLUSIONS

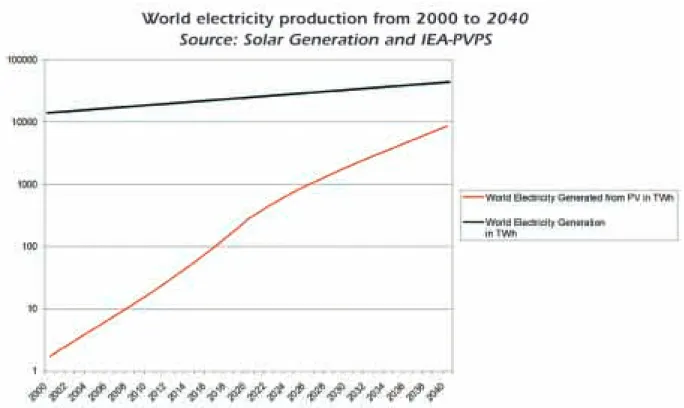

A considerable part of the future energy supply will be provided by renewable energy sources, and an important role in this field will be assumed by photovoltaic electricity production. Keeping this technology in Europe and creating jobs and opportunities will require strong efforts in technological development, investment in production facilities and market expansion with political support.

PHOTOVOLTAICS – THE BEST CHOICE

2 INTRODUCTION

A BRIEF HISTORY OF PV MANUFACTURING AND MARKET DEVELOPMENT

According to the findings of the International Energy Agency's PV Power Systems programme, the proportion of new grid-connected PV installed in the countries participating in the program - most of the main OECD countries1 - has increased since 1997 from 58% to up over 86% in 2002 The EU (especially Germany) and Japan have also been the main players in promoting more positive legal frameworks to enable grid connection of PV systems.

PHOTOVOLTAICS – POWERING OUR FUTURE

It is also important to realize that the development of the PV market does not only depend on how the EU chooses to tackle the various technological challenges or its response to market needs and opportunities. This roadmap recognizes that if the EU is to take full advantage of the opportunities associated with the deployment of PV markets, all parties – government, industry, financiers and user groups (utilities, building developers, architects, local authorities) – must work towards common goals. .

GENERAL OBJECTIVES

3 ROADMAP OBJECTIVES AND METHODOLOGY

METHODOLOGY

Extrapolating the market development after 2010 is certainly difficult as it depends so heavily on the political scene.

INTRODUCTION

ANALYSIS OF THE SITUATION

4 TECHNOLOGY DEVELOPMENT

- DETAILED DESCRIPTION OF TECHNOLOGIES

- GENERAL REMARKS

- CRYSTALLINE SILICON Feedstock requirement and pricing

- THIN-FILMS

- OTHER INNOVATIVE TECHNOLOGIES

- ACTION PLAN

- GENERAL EFFORTS AND EXPECTED RESULTS

- LIST OF TARGETS AND ACTIONS

- INTRODUCTION

- PV FOR GLOBAL POWER SYSTEMS

- THE CONCEPT

Since the cost of materials is a significant part of the total cost, reducing the consumption of materials is essential, especially in the case of crystalline silicon. The biggest challenge in the production of PV modules is to reduce the cost, at the same time maintaining or even improving the quality of the product. EPIA's Crystalline Silicon Technology Working Group has undertaken an assessment of the availability of suitable low-cost feedstocks from the polysilicon electronics industry in the time frame up to 2010.

The main visual difference between thin-film modules is the homogeneous appearance that opens up new market segments based on customer needs regarding the design of the modules. Of the various thin film technologies, amorphous silicon is the best understood and currently accounts for virtually all commercial thin film production. However, Japan's thin-film panel market share is growing due to the long experience of Japanese industry in this field and huge investments.

The long-term reliability of PV modules and especially thin-film devices is highly dependent on protecting the sensitive semiconductor material from the environment, especially from water ingress.

5 PRODUCTS AND APPLICATIONS

PV in utility grids

- GRID-CONNECTED SYSTEMS

- STAND-ALONE - AND ISLAND GRID SYSTEMS

- PV POWER SYSTEMS – THE NEXT STEPS

- MANUFACTURER OF SYSTEM COMPONENTS

- BUILDING-INTEGRATED PHOTOVOLTAICS (BIPV)

- ACTION PLAN

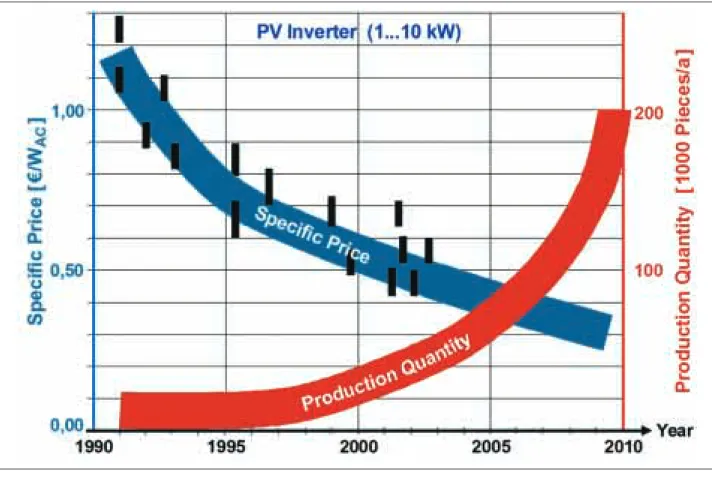

For example, the power conditioning units (for example, inverters and inverters that represent the heart of PV system technology) must have high efficiency and low cost. A broad extension of decentralized electrification would automatically lead to the interconnection of local grids. The energy produced by the PV module depends on the incident solar radiation, the module temperature and the operating point of the module.

In addition to the PV modules, it includes a charge controller to ensure long life for the lead battery. This can be attributed to the high life cycle cost of the diesel generator set. Implementation of the modularization concept with standardized components to be connected on the AC side that are compatible with the existing supply network.

The quality of the inverter must meet the highest industry standard, on the other hand, the price of the device must be reasonable.

- EUROPEAN PV INDUSTRY

- STRUCTURE OF EUROPEAN INDUSTRY

- MARKET SHARE OF REGIONAL INDUSTRIES

In a narrow sense, the PV industry includes companies engaged in silicon crystallization and coating, solar cell manufacturing, module manufacturing, and thin film module manufacturing. In Europe, the entire value chain is covered by a number of companies, and most of them are represented by EPIA. Some are affiliated with major oil companies and utilities, but most are independent companies from major industrial players.

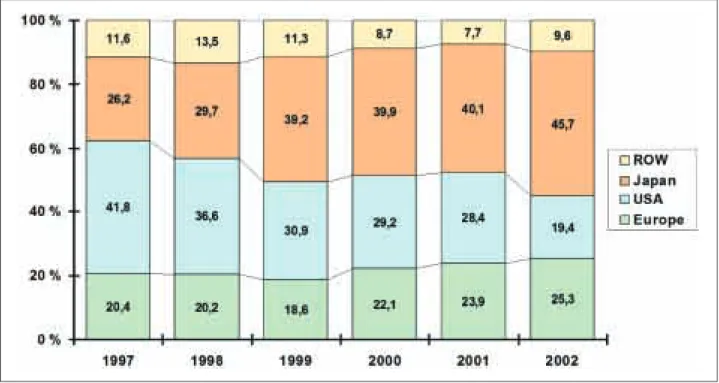

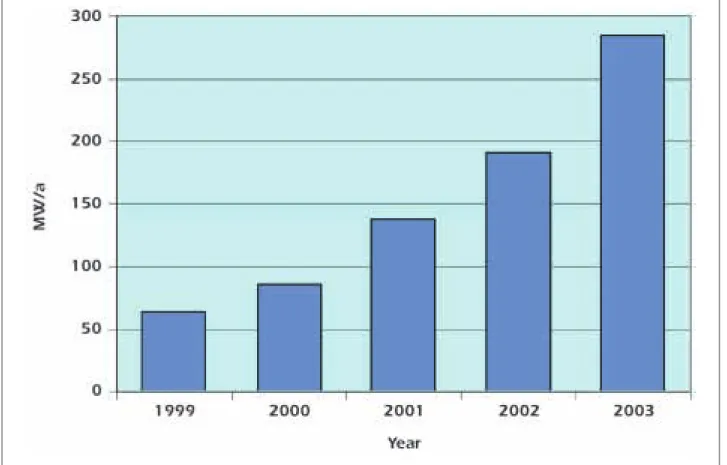

Some of the companies have been in the field for more than twenty years, but especially in recent years a number of new companies have started business, financed by independent investors. 7 shows the market shares of the industries in Europe, USA, Japan and Rest of the World (ROW) for the last six years. The strong position of the Japanese industry is evident, but the European industry also shows steady growth.

6 INDUSTRY DEVELOPMENT

- SUPPLY INDUSTRY

- EQUIPMENT MANUFACTURERS

- SYSTEMS INTEGRATORS

- MARKET DEVELOPMENT – THE FUTURE

The importance of silicon raw material supplied by semiconductor silicon manufacturers has already been highlighted. But this is just one example of the PV industry's dependence on outside materials. As in the semiconductor industry, the PV industry also requires the supply of many materials from outside.

Investors in large PV and module manufacturing facilities are no longer interested in developing their own equipment, and it is true that over the past few years the equipment industry has adapted to the high growth rate of the PV industry and now offers entire production lines with a high degree of automation. The involvement of the equipment industry in the development of mass production from medium-scale manufacturing is indispensable. It must be pointed out that the strong growth in Europe over the past four years is primarily due to the implementation of the German feed-in law (EEG).

EPIA strongly supports this program and favors similar policy measures for solar electricity in all states of the Union.

7 MARKET DEVELOPMENT

MARKET DEVELOPMENT IN EUROPE

- POLICY INITIATIVES

- MARKETING, EDUCATION AND STANDARDS

- ACTION PLAN

One of the most important aspects of the German Renewable Energy Act is that it has provided a secure medium-term planning basis for investments to help the PV industry move from niche markets to mass production. However, EPIA firmly believes that a coordinated incentive scheme based on pan-European rates similar to the REL would be an important boost for European industry and a dynamically expanding market would serve to accelerate the cost reduction process . If REL had been implemented across the EU, for example, the generation capacity installed since 2000 alone could be almost 900 MWp - roughly 50% more than has been installed in Japan and four times more than in USA.

Building regulations that recognize and support the role of solar in the sustainable supply of electricity in the urban environment would stimulate a large potential for solar, based on capturing part of the newbuild market and rooftops. A relatively modest requirement for PV of 5% of new buildings would stimulate a market in the order of 200 MW. Governments can and must continue to play a crucial role in technology promotion through general sector marketing (e.g. via support to European and national industry associations and via public information campaigns – similar to the support offered to promote energy efficiency measures).

Guidelines for best practices regarding PV in the credit and construction sectors should also be developed.

DEVELOPMENT OF EXPORT MARKETS

- GENERAL REMARKS

- ACTION PLAN

During the life of the scheme, the guaranteed feed-in tariff may drop each year for new contracts in order to encourage PV producers to strive for continuous cost reductions. This model should take into account the solar radiation in each member state in such a way that the owner of PV systems can operate it economically. Continued focused RTD program with improved funding arrangements: Extensive research and technological development is essential for the European PV industry to remain competitive and open new markets.

Improving cooperation between the research sector and industry will help the research sector to better understand the needs of the PV industry and its customers, as well as to develop more appropriate technologies. In the medium term, 70% of research funding should be allocated to industry, half to internal research and half reallocated to research institutes. As the experiences of Germany and Japan have so clearly shown, a stable and supportive policy framework, supported by a coherent program of research and technological development is essential for securing investment in industry and maximizing market development potential and market share. .

In addition, the EPIA plan will greatly increase the competitiveness of the European PV industry and provide solar electricity at economic prices in the long term.

8 STRATEGIC ACTIONS FOR ESTABLISHING A VITAL AND

EPIA has devised a program of specific actions that European industry, in collaboration with other key stakeholders from politics, finance, the electricity industry, academia, construction and other sectors, should adopt in order for Europe to exploit the global PV market potential. Central to the program are the following three branches of political support, which provide the long-term framework for the industry to base its investments on. Using the German model to support grid-connected PV, there should be a guaranteed price paid through utilities for PV-produced electricity of x Euro/kWh, guaranteed for y subsequent years.

There should also be dedicated grants for product development for this market and a revolving fund specifically for rural PV systems. The EPIA Secretariat thanks EPIA members for their valuable contributions and their voluntary work in the preparation of this document. Aulich, PV Silicon AG, for initiating and helping to organize the work and to Dr. Winfried Hoffman, RWE Schott Solar GmbH, and Mr.

We would also like to thank the following companies and institutions that provided us with photos and allowed their use.

ACKNOWLEDGEMENTS