Initiatives have also been taken to build an integrated framework for the study of network industries. We owe special thanks to Bruno Hoornaert who collected most of the figures for the chapters on electricity and gas.

Executive summary

For the railways, there is a separation of accounts, as required by the EU. In the part of the market that has been opened up, there is sufficient competition.

Introduction

This framework allows for a consistent overview and benchmarking of network industries in Belgium. Each of the five chapters briefly describes the current structure of the sector and the legal framework.

I A horizontal analysis for Belgium

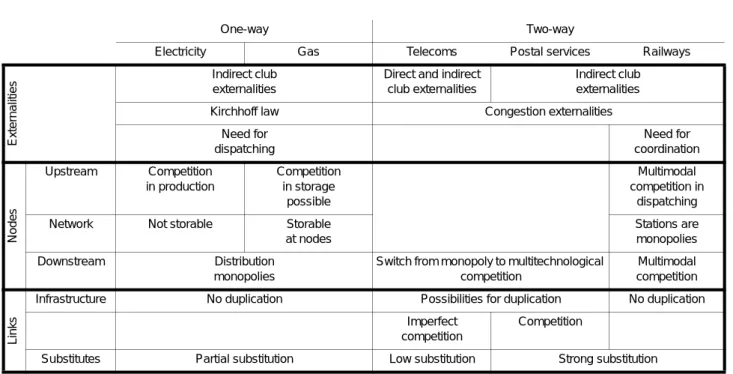

The analysis network industries

In the creation of the internal market, special attention is required for network industries. The report adopts a horizontal approach, which allows a thematic comparison of network industries.

Network industries in Belgium

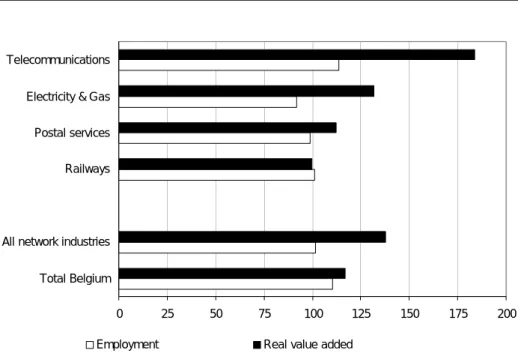

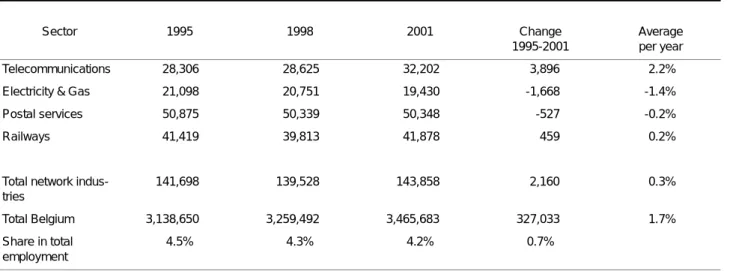

In the above, growth of the network industries has been given in terms of output and employment. For the Belgian network industries, this is shown on the right side of the white line in Figure 5.

II Telecommunications

The telecommunications sector in Belgium

A striking fact of BLEU's telecommunications services sector is the importance of foreign trade. Voice telephony is one of the most important telecommunications services and is mainly based on the analogue PSTN network. Moreover, at the end of the total number of Internet connections via DSLandTV cable.1 The spread of the Internet has also been encouraged by the liberalization of domain name registrations in December 2000 and by the sharp reduction of domain name prices (from 25 euros to 10 euros ) euro) since June 2001.

One of the most important elements for promoting competition in telecommunications is the interconnection conditions. Since December 2002, Belgacom has been assessed as having SMP in all segments of the leased line market. Market opening was closely linked to significant regulatory and institutional reorganization of communications markets.

Specific topics concerning telecommunications

However, effective competitive entry into this market segment appears to remain difficult and figures published by the European Competitive Telecommunication Association (ECTA, 2002) at the end of June 2002 showed that only 1,000 DSL lines out of a total of 363,000 were fully unbundled and operated by competing local exchange companies. The lack of competition in the DSL market is partly offset by the services provided by cable operators. BIPT publishes an annual report on the incumbent's compliance with the universal service obligations (USO).

The management contract also contains the budget allocated by the state to Belgacom to carry out these tasks. As these consumer prices continue to be measured on the basis of prevailing prices, they do not reflect the most attractive conditions offered by the market. For 2002, however, there has been a general decrease in the tariffs used by the main providers of Internet access via DSL connections, which increased the number of these connections.

Annex

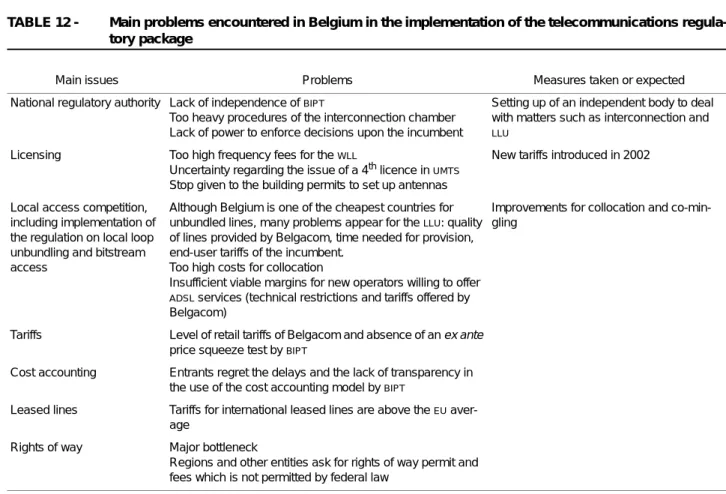

In the last few years, the original operator Belgacom has invested a lot of effort in digitizing an important part of the network. Directive 2002/58/EC on the processing of personal data and the protection of privacy in the electronic communications sector. Too difficult procedures of the connecting chamber. Lack of authority to enforce decisions over the holder.

Competition for local access, including implementation of the regulation on unbundling of subscriber circuits and bitstream access. Although Belgium is one of the cheapest countries for unbundled lines, many problems arise for LLU: the quality of lines provided by Belgacom, time needed for delivery, end-user tariffs for the incumbent. Cost Accounting Participants regret the delays and lack of transparency in the use of the cost accounting model by BIPT.

III Electricity

The electricity sector in Belgium

For example, Belgium has adopted major implementing decrees, especially regarding the appointment of the TSO, the general structure of transmission tariffs and the technical rules for the management of the electricity transmission network (network code). The role of the federal government is mainly related to the procedures for investments in the transmission and generation of electricity and the setting of tariffs. Belgium has five bodies responsible for the regulation and control of the electricity market: four regulators for open market segments (one at federal level and three at regional level), and the Control Committee for Electricity and Gas (CCEG). for captured market segments.

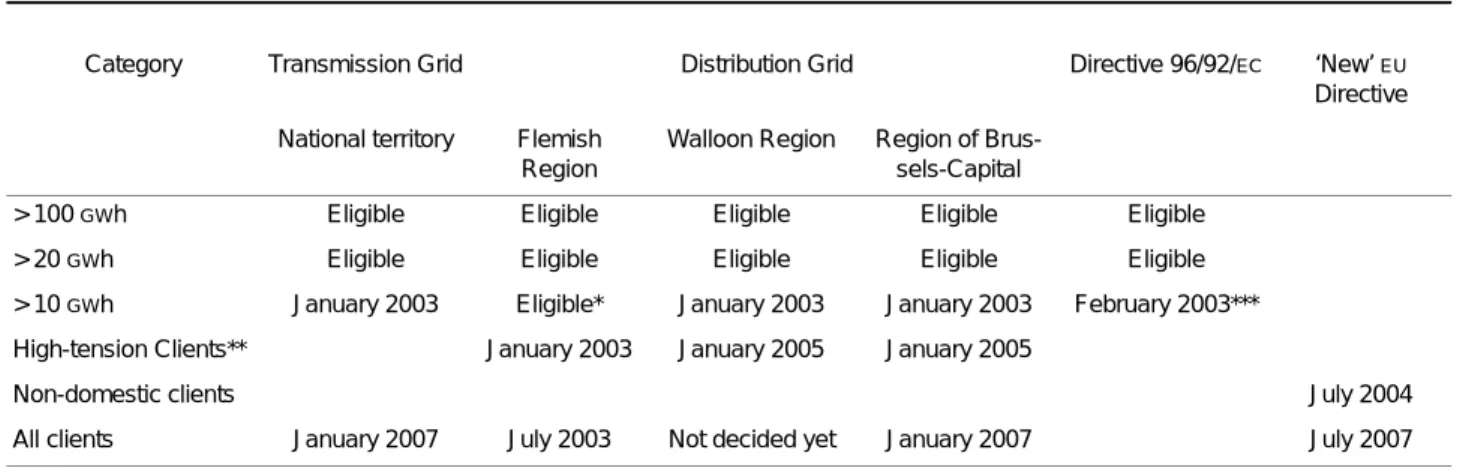

The board members must not have any direct or indirect interest in the electricity industry. According to the current legal provisions, the timetable for the opening of the electricity market is summarized in Table 13. As can be seen from Table 13, the opening of the electricity market is progressing faster in Flanders than elsewhere in Belgium.

Specific topics concerning electricity

Those of the electricity producers and suppliers are part of the permit criteria for power generation and supply. The third category of PSO concerns the protection of the environment through the promotion of renewable energy sources and the rational use of energy. Legal provisions regarding the promotion of rational energy use include, among other things, the establishment of a system of combined heat and power certificates in Flanders.

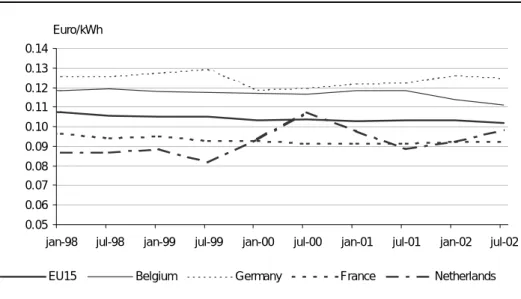

Changes in the prices of consumer goods arose mainly as a result of the application of rules on price restrictions on the own electricity market. In addition to price reductions and the implementation of PSO (see Chapter 2 above), the reform of the electricity sector has brought benefits in terms of energy services offered to different categories of customers. There are also initiatives to improve the quality of service for customers of distribution companies.

IV Gas

The gas sector in Belgium 1

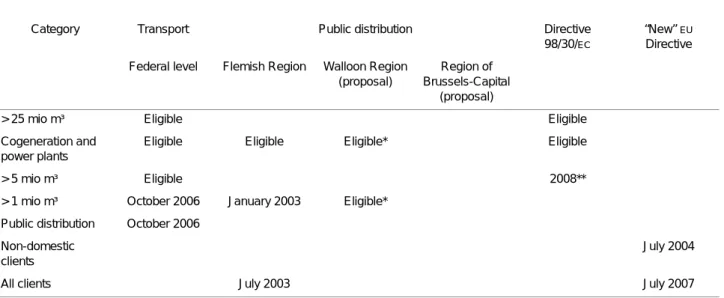

At present, five companies have a license to supply gas to the eligible customers in the 'transport' category. Similar to the electricity sector, the implementation of the European Gas Directive into Belgian law involves the adoption of both federal and regional legislation. The regional legislative and administrative regulations deal with gas distribution, gas supply to 'distribution customers' and rational use of energy (mainly cogeneration).

The role of the federal government is mainly related to the security of gas supply, major infrastructure for transportation and the setting of tariffs. Nevertheless, there have been very limited changes to the gas supply market so far. In particular, large pieces of law regarding access to the transport network are missing (regulated tariffs, transport licences).

Specific topics concerning gas

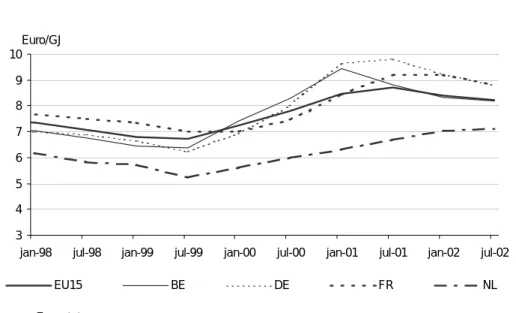

In terms of the geographical coverage of the pipeline system, Belgium has a well-developed gas network. The process of liberalization of the gas industry is not expected to significantly affect the border price of gas, at least in the coming years. The increase in prices has been stronger in relative terms for industry than for individuals due to the more important role of marginal prices in the price structure of this last category of consumers.

The development of Zeebrugge's short-term or wholesale gas market may provide some scope to lower the average gas supply price. This happened in the context of the accelerated market opening and in the context of the then sharply rising oil prices. The plan identifies the necessary investments to guarantee the operation of the gas market and security of supply.

V Postal services

The postal sector in Belgium

As part of the upcoming opening of the market, a strategic plan was drawn up in 2001, which was revised in 2002. The gradual opening of the European postal market was initiated by the Council with Directive 97/67/EC. Finally, the contract defines the basic principles of pricing and density of the postal network.

As an owner, it can influence the appointments of the board and management of the company. In the current year, 92% of the items should be delivered the next day, as measured by an internationally standardized method. As parts of the market have already been opened up, a number of competitors are active on the Belgian market.

Specific topics concerning the postal services

This will make it easier for the institute to adapt to the constant dynamics of the postal and telecommunications industry. They must ensure compliance with the directive and can also act as an antitrust authority. For Belgium, the fulfillment of the criteria of quality, universality and financial accessibility is ensured by the third management contract.

Please note that separate agreements on the terms of the service are entered into with the state and the publishers. Reserved area: The maximum criteria in the respective EU directives are used (100 grams or three times the price of a standard letter); According to De Post's own measurement, only 85% of post was delivered the next day in 2001, but this rose to 92% in the first half of 2002.

VI Railways

The railway sector in Belgium

The law only imposes PSOs, which are the performance of internal passenger traffic and the maintenance of the railway network. The gradual liberalization of the European railway market was initiated by the Council with three directives (91/440/EEC, 95/18/EC and 95/19/EC). Directive 95/19 regulates the allocation of capacity (slots on the railway network) to users and the introduction of infrastructure use charges.

More important, however, is the timetable for opening up the market for international rail freight. The 1997-2001 contract lays down the basic principles for the management of the company, such as the pursuit of efficiency and the fulfillment of statutory duties. However, it must also take into account the independence required by the 1991 EU directive.

Specific topics concerning the railways

Once network management and train operation are separated, it is relatively easy to make further separations of the latter. Note that the issue of network operator access and tasks is not limited to international freight traffic. Duties for the needs of the nation: Among the duties are transport ordered by the administration, military duties and services for De Post;.

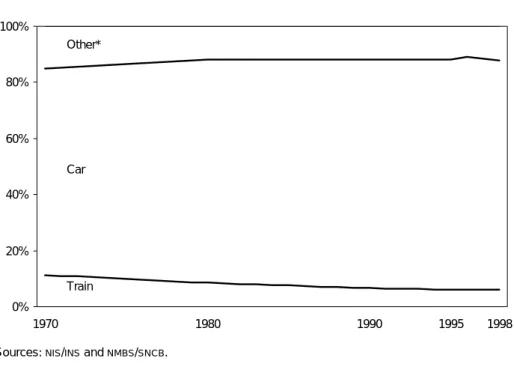

Furthermore, compensation is provided for the state's needs, pensions, damages and other financial obligations for the state. However, since the conclusion of the previous contract, the state contribution has grown from 2.1 to 2.3 billion per year. Due to the ever-increasing amount of goods being transported, stable traffic implies a declining market share.

VII References

European Commission (EC), 2001a, Market Performance of Network Industries Providing Services of General Interest: A First Horizontal Assessment. European Commission (EC), 2002c, Second Comparison Report on the Implementation of the Internal Market for Electricity and Gas.