First, the exchange rate moves in a way that determines the impact of the tariff (a tariff on imports appreciates the home currency and a tariff on exports lowers it). This section presents a model of the oset exchange rate and examines its quantitative implications for the US dollar and Chinese renminbi. The exchange rate is defined as the price of foreign currency in terms of home currency, so that an increase in the exchange rate means a depreciation of the home currency.

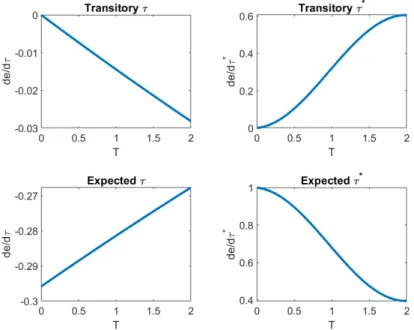

The country of origin applies a rate τt to imports, which means that the price of the foreign good is in its own currency. The domestic terms of trade is equal to the price of the domestic good in terms of the foreign good. Equation (24) implies that the size of the exchange rate oset increases with the import elasticity and decreases with the export elasticity.

Greater import elasticity increases the impact of the tariff on domestic demand for household goods and requires greater interest appreciation. Since the tari reduces foreign demand for a domestic good, it results in a depreciation (rather than an appreciation) of the domestic currency. 6The influence of the exchange rate on domestic demand for domestic goods is captured by the term in ωH(1−m) in equation (20).

The impact of the exchange rate on the supply of household goods is represented by the term in (i−1) in equation (21).

Alternative assumptions

In contrast, the exchange rate effect of a tariff on exports is reduced by a factor of less than two. We observe that the impact of an expected tari on imports does not decline very rapidly with the lag. During our benchmark calibration, the exchange rate for a tari on imports increases to 0.35 (instead of 0.30 under the PCP).

The exchange rate for a permanent export tariff is also higher under DCP than under PCP and for similar reasons. During our benchmark calibration, the exchange rate is 1.22 for a tari on exports (instead of 1.0 under the PCP). The result is that the exchange rates are also greater than under the PCP and about the same as when the home economy is not the United States (0.35 for a tari on imports and 1.19 for a tari on exports).

To summarize the analysis so far, imposing an import tariff leads to an appreciation of the home currency and imposing an export tariff has the opposite effect. Under PCP, the exchange rate oset is 30 percent for a permanent import rate and 100 percent for a permanent import rate for our benchmark calibration.

Application to the dollar and the renminbi

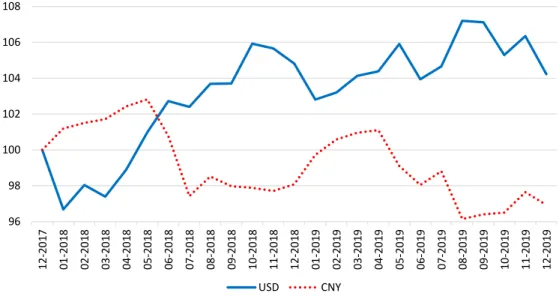

Based on this approach, we found that tariffs imposed by the US in 2018-19 averaged 3.7 percent of the value of imports of goods into the US. The third column reports the multilateral appreciation of the dollar caused by the import tariff as predicted by the model in the calibration of Table 1. The third row of Table 2 reports the results of the same exercise performed for the renminbi.12 The average tariffs on Chinese imports and exports were calculated in the same way as for the US (see Appendix B for details).

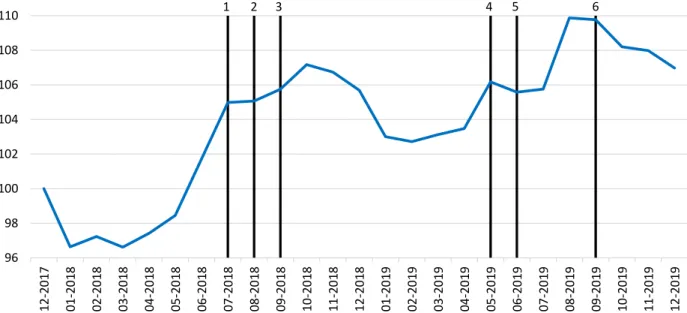

The Chinese average tari rates are the mirror image of the US taris, in the sense that the taris on Chinese exports are more than three times the taris on Chinese imports. To answer this question, we look separately at the nominal eective exchange rates (NEERs) for the dollar and the renminbi. Cumulatively, the US tari news resulted in a 0.9 percent appreciation of the USD NEER and a 2.0 percent depreciation of the CNH.

16Our currency basket is composed of the top 10 currencies used in the BIS baskets. According to this calculation, the US taris explain 65 percent of the renminbi depreciation and 22 percent of the dollar appreciation observed in 2018-19. The model predicts a somewhat larger effective depreciation of the renminbi than measured by the event analysis.

About thirty percent of the news in the BK sample is not in the Bloomberg sample. However, this is not the case - the magnitude of the exchange rate impact of tari news is comparable between the two samples. This article began by observing that the taris introduced by the US in 2018-19 was caused in part by a simultaneous depreciation of the renminbi against the dollar.

Furthermore, our model suggests that taris can explain a significant portion of the changes in the dollar and renminbi exchange rates observed over that period. It must be resolved for the dynamics of the transition both in the US and in the rest of the world. The rest of the world is supposed to have the same type of Taylor rules as the US.

The demand for output of the representative non-US country is the sum of domestic demand and foreign demand. The appreciation of the dollar can be seen in the initial decline in S∗ and E (using the fact that Pt∗ and PF t are sticky in equation (C4)). Note that exporters in the RoW adjust their dollar prices downward (πF goes below target) as dollar appreciation increases their values.

The ten major currencies account for approximately 85 percent of the BIS basket for the dollar and 80 percent for the renminbi.