This is disturbing to a lot of people […] and it is an incestuous thing what is going on with regard to the defense contractors and the Pentagon […].”2. Our article is related to five different strands of literature: The literature on the value of political connections created through (i) political appointments and (ii) corporate appointments of former government officials in the United States, (iii) of political connections in general, (iv) the literature on lobbying, and (v) the literature on the reaction of defense stocks to political decisions. 3 The Vice President of the United States is “hand-picked” by the presidential candidate, formally selected by the nominating conventions, and ultimately chosen by the Electoral College.

Thus, these two papers offer mixed evidence about the value of political connections in the United States. Similarly, only a small subset of the political affiliations studied by Fisman et al. 2006) is associated with the revolving door phenomenon. Although we look at both sides of the revolving door, we focus primarily on political appointments.

5 We focus in our discussion of Goldman et al. 2009) on the part that is closest to our empirical strategy. 2009) also take advantage of the close presidential election of 2000 and the partisanship of board members. Similarly, Johnson and Mitton (2003) find that ties with Malaysian Prime Minister Mahathir paid off in the aftermath of the Asian financial crisis.

Background

Defense of over $1 billion.17 Did we mention that he was formerly an advisory board member of Martin Marietta Corp. Winter, as Secretary of the Navy, discussed the future of naval shipbuilding with Northrop Grumman Corp. several million dollars on its way out of the gates of Northrop Grumman.22.

Former political appointees are valuable because of their connections, access and influence.23 According to Washington insiders, sleazy government officials at all stages of the procurement process are essential to obtaining contracts.24 Probably no one is better qualified for this position than former political appointees. . For example, in the confirmation process of the former corporate executives and nominees of the service secretary, Thomas E. 23 This view was expressed, for example, by the Director of of the Center for Public Integrity in Associated Press.

Data and Empirical Strategy

Winter received waivers to the rule requiring nominees to purchase pension insurance and to participate in decisions regarding his former employer.29 Thomas E. White failed to withdraw from his Enron financial positions in time and notify Congress. 30 On the same day that President Obama tightened the withdrawal requirements, William J. We require four types of daily stock market data for our analysis, for which we rely on Datastream in each case.

We therefore chose the S&P 500 as our market index for the United States stock market.33 Third, we will later supplement the market model with an industrial index. Finally, we rely on Datastream for daily stock market data on market capitalization and trading volume. We purify stock returns from market-wide stock market developments using a standard market model (MacKinlay, 1997).

We first calculate the returns of individual stocks based on the returns of the relevant market index during an estimation window prior to the announcement day. The event date is the day of the announcement if the announcement occurred on a trading day before the markets closed, otherwise on the next trading day. Since it was not possible to determine the exact time of the announcement in all cases, we also estimate the two-day cumulative returns.

In this way, we make sure to capture the stock market reactions to all announcements. We exclude observations from the analysis if other important company news identified in a full-text search such as earnings and dividend announcements, share buybacks, and M&A activity were also announced on the announcement day. If such fixed news is released the day after the release day, observations remain in the sample, but the two-day abnormal return is set equal to the (undisturbed) one-day abnormal return.

Online Appendix 1 provides detailed information on all political and corporate postings and their hard links, and Online Appendix 2 lists all DoD positions that were considered in this study.

Empirical Results for Political Appointments 1. Baseline Results and Robustness

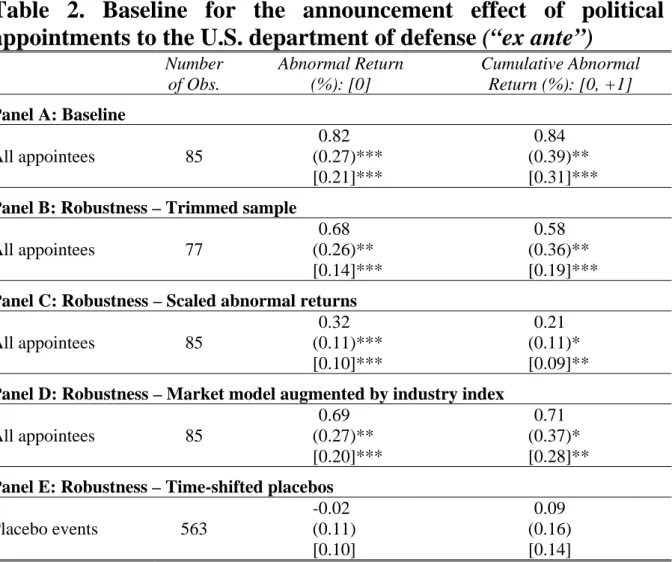

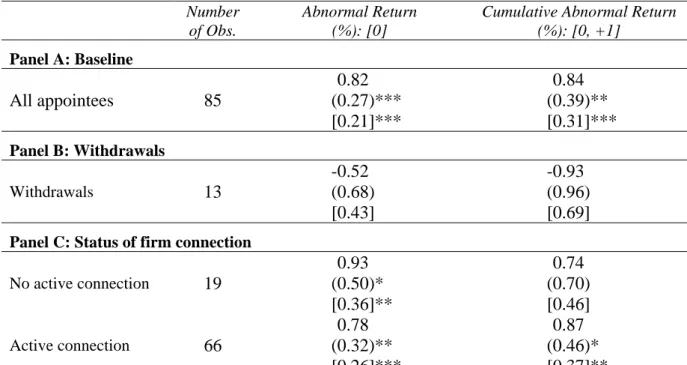

Strong ties to these political appointees are well established, with an average tenure at firms of around seven and a half years.36 We find positive abnormal returns of 0.82% for the announcement day and of 0.84% for a two -day window including the announcement day and the next trading day. First, Panel B of Table 2 displays the mean abnormal returns for a truncated sample, excluding the top and bottom 5% of the abnormal return distribution during the event windows. Second, Panel C of Table 2 presents mean scaled abnormal returns, that is, abnormal returns divided by the standard deviation of estimation period residuals.

This robustness check confirms our main finding that political appointments—and not unobserved firm characteristics that may be correlated with political announcements—lead to positive abnormal returns. One might hypothesize that the positive abnormal returns are related to the (outgoing) appointee's departure from the firm rather than to her political appointment. Below we provide two additional pieces of evidence that are inconsistent with this alternative interpretation of the abnormal returns.

Second, we assess whether political appointments also lead to positive abnormal returns in cases where the appointee is no longer officially associated with the firm. For the later group, we find – based on 19 observations with an average maturity of nine and a half years – positive and significant abnormal returns of 0.93% for the announcement day. Although abnormal returns are not significant for a two-day window, the announcement effects for both groups are similar in magnitude.

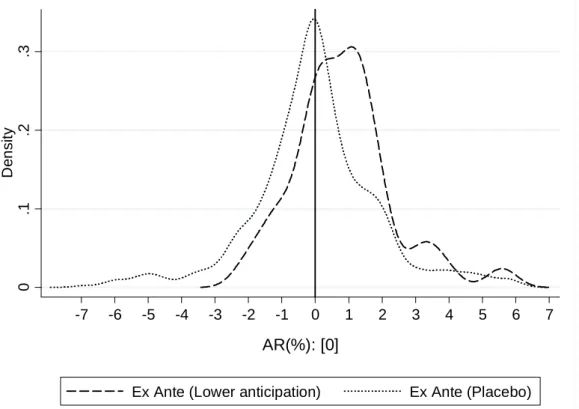

All our results so far refer to one- and two-day average cumulative abnormal returns. Nevertheless, in Figure 3 we examine the temporal pattern of the average cumulative abnormal returns for the four trading weeks preceding and following the announcement day, with the shaded area representing the two-day event window. First, cumulative abnormal returns are, on average, about one and two percentage points higher in the post-event period compared to the pre-event period for the baseline sample and the less expected event sample, respectively.

Second, our one- and two-day average cumulative abnormal returns are comparable to long-term effects.

Empirical Results for Corporate Appointments

There remains some uncertainty about the exact timing of other major company news and therefore some of these events could still confound estimates. On the one hand, rumors about pending nominations may be reflected in the price movements of the base sample before the event date. For example, on day -18, sources close to the transition team were quoted as saying that the appointment of Paul D. Wolfowitz as Deputy Secretary of Defense was likely.46.

On the other hand, post-event price movements may reflect uncertainties in the confirmation process. Lynn's nomination met with resistance in the Senate on Day +10 and was suspended. which fall below conventional levels of statistical significance for one method of calculating standard errors. This suggests that the results for company appointments are to some extent based on outlier observations.

The return distribution for corporate appointments is flatter and the right place of the distribution is shifted outwards. The Kolmogorov-Smirnoff test rejects the equality of these two distributions at the 5 percent significance level. According to Panel B of Table 7, we find larger positive abnormal returns for corporate board appointments than for other corporate appointments.

The two-day event window of abnormal returns for board members can be directly compared to the results of Goldman et al. Consistent with our results for political appointments and those of Goldman et al. 2009), we find stronger effects in people who served in democratic administrations.48.

Conclusions

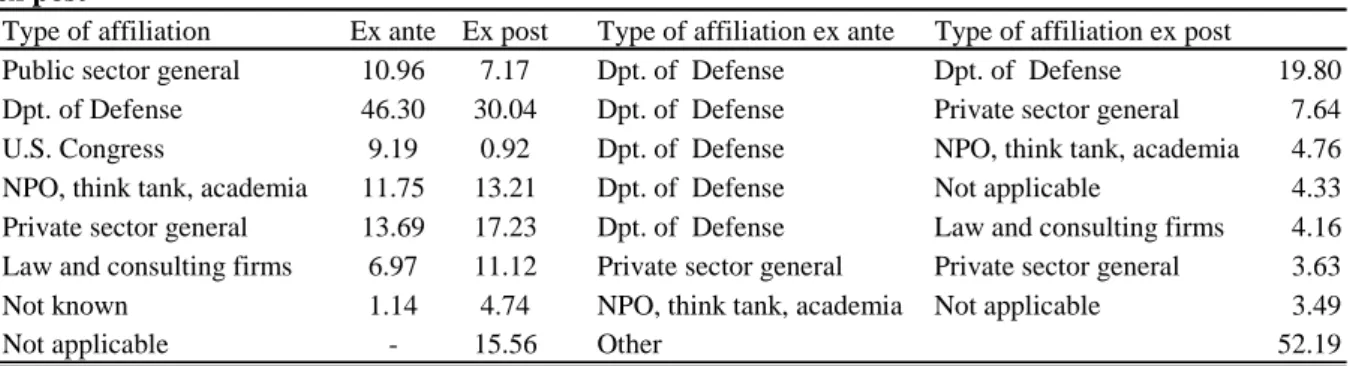

Affiliation refers to all positions held two years before the announcement (ex ante) and two years after leaving the position (ex post). The sample is based on political appointments in the US Department of Defense in the years 1988-2009. Abnormal returns are associated with nomination announcements of political appointees who served within the past two years as members of the board of directors or advisory board. an executive officer or an employee for a listed firm.

Panel A reports the baseline (“prior”) results, and the remaining panels provide different robustness checks to the baseline. Abnormal returns refer to announcements of nominations, withdrawals from the confirmation process, or deaths of political appointees who have served on a board or advisory board, executive officer, or employee of a publicly traded company within the past two years. Abnormal returns refer to announcements of nominations of political appointees who have been board or advisory board members, CEO or employee of a listed company in the past two years.

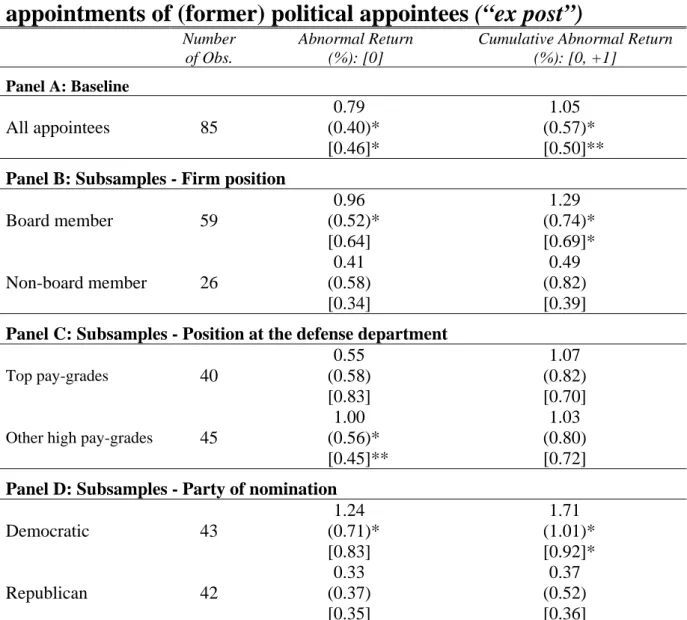

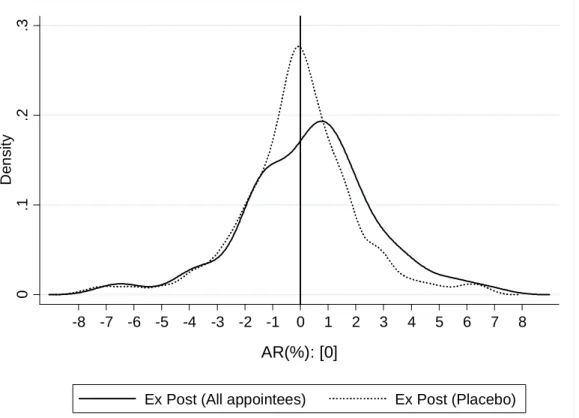

Abnormal returns relate to announcements of political appointees who have served within the past two years as members of the board of directors or advisory board, executive officer or employee for a listed firm. Basis for the effect of announcing appointments in the private sector of (former) political appointees ("ex post"). Notes: Sample is based on private sector appointments of (former) US political appointees.

Abnormal returns are related to the announcements of (former) political appointees who worked (at least for some time) for the US Department of Defense during the last two years before their move to the private sector. Panel A reports the baseline results (“ex post”) and the remaining panels provide various robustness checks to the baseline. Subsamples of the announcement effect of appointments in the private sector from (former) political appointments (“ex post”).

Abnormal returns are related to the announcements of (former) political appointees who worked (at least for some time) for the US Department of Defense during the last two years before their move to the private sector (for further details see Table 6) . Notes: Figure 3 presents the average cumulative abnormal returns for day -20 up to and including the specified day for the 85 events in the baseline and the 39 less expected events.