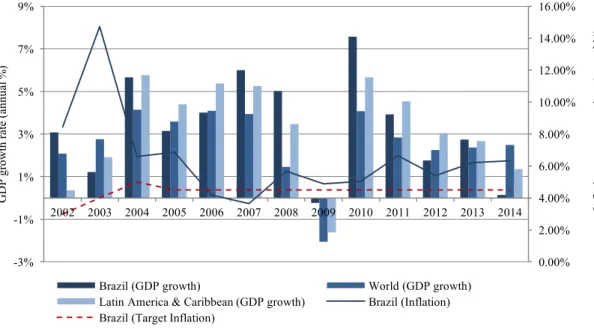

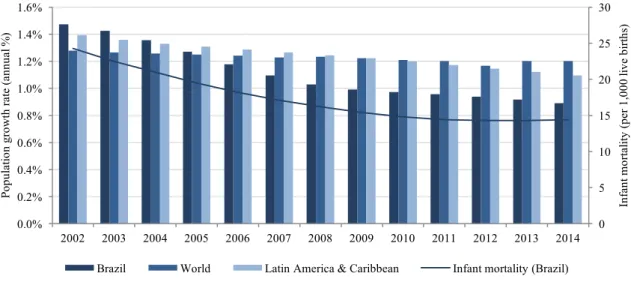

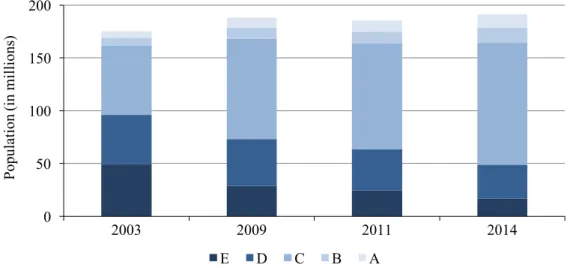

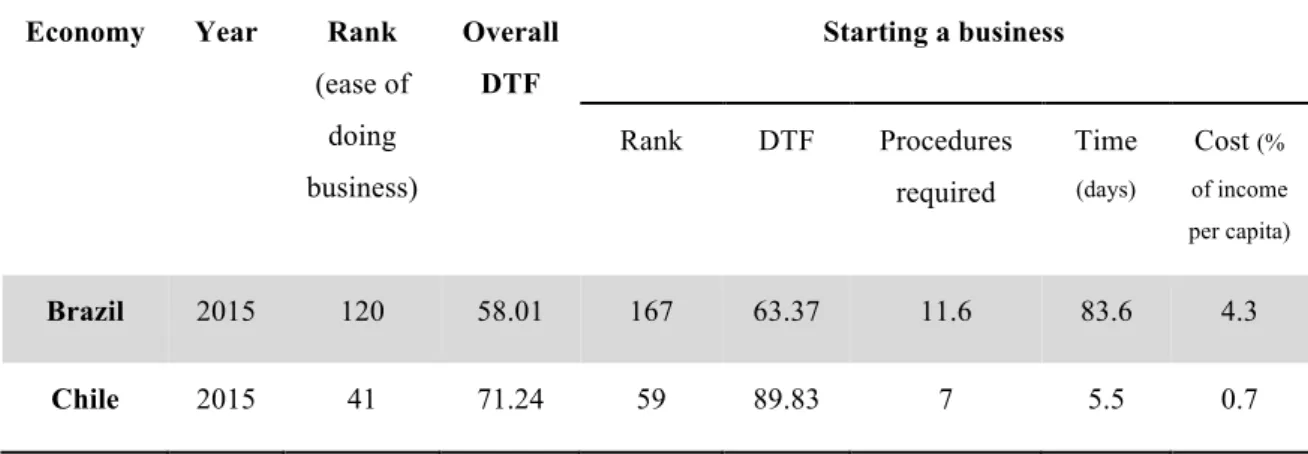

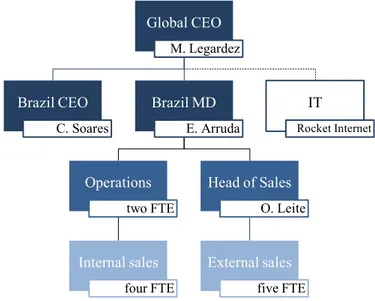

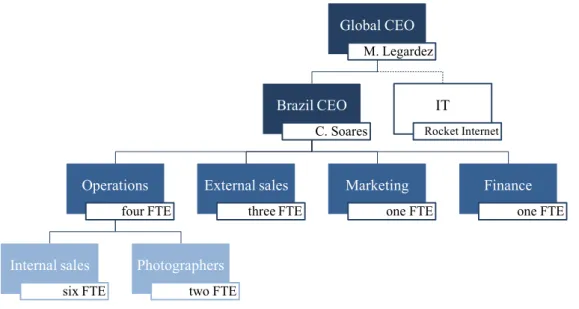

Structuring a startup's operations in an emerging market

Texto

Imagem

Documentos relacionados

This study was performed to introduce the allele Bush of commercial cultivars with a bush growth habit into Cucurbita moschata accessions and select the best crossings for production

This log must identify the roles of any sub-investigator and the person(s) who will be delegated other study- related tasks; such as CRF/EDC entry. Any changes to

Quer isto dizer que também recentemente, apesar da relação terapêutica (terapeuta-paciente) ser considerada um bom preditor de sucesso e eficácia para o resultado das

Material e Método Foram entrevistadas 413 pessoas do Município de Santa Maria, Estado do Rio Grande do Sul, Brasil, sobre o consumo de medicamentos no último mês.. Resultados

Foi elaborado e validado um questionário denominado QURMA, específico para esta pesquisa, em que constam: a) dados de identificação (sexo, idade, profissão, renda familiar,

A situação não deixa de ter certa justiça poética, uma vez que para aqueles que queriam controlar a movimentação de pessoas – emigração, imigração e colocação de

Você terá os seguintes benefícios ao participar da pesquisa: a realização de práticas de manejo ambiental para controlar o vetor da Leishmaniose Visceral no seu domicílio e

Em Pedro Páramo, por exemplo, tem-se uma escritura (des)organizada em 70 fragmentos narrativos, que se desenvolvem em diferentes planos, nos quais a evoca- ção, a fantasia, o mito e