NEGOTIATING PREFERENTIAL TRADE

AGREEMENTS FOR BRAZIL:

A CGE MODELING PERSPECTIVE

Vera Thorstensen

Lucas Pedreira do Couto Ferraz

(Coordinators)

Rodolfo Arruda Cabral

Carolina Lemos Rêgo

NEGOTIATING PREFERENTIAL TRADE

AGREEMENTS FOR BRAZIL: A CGE

MODELING PERSPECTIVE

VERA HELENA THORSTENSEN

LUCAS PEDREIRA DO COUTO FERRAZ

(Coordenadores)

Carolina Lemos Rêgo

Rodolfo Arruda Cabral

(Autores)

VT

São Paulo

T522 Thorstensen, Vera Helena. Ferraz; Lucas Pedreira do Couto (coordenadores).

Cabral, Rodolfo Arruda; Rêgo, Carolina Lemos (autores).

Negotiating Preferential Trade Agreements for Brazil: A CGE Modeling

Perspective. / Vera Helena Thorstensen; Lucas Pedreira do Couto Ferraz

(coordenadores); Rodolfo Arruda Cabral; Carolina Lemos Rêgo (autores). / São

Paulo: VT Assessoria Consultoria e Treinamento Ltda., 2016.

401p.

Bibliografia

ISBN: 978-85-66977-02-8

1. Economia. 2. Acordos Preferenciais de Comércio. I. Título

CDD 330

Capa, Edição e Diagramação:

Thiago Rodrigues São Marcos Nogueira

© desta edição [2016]

VT Assessoria Consultoria e Treinamento Ltda.

Tel.: (11) 3799-7926

http://ccgi.fgv.br

[email protected]

COORDINATORS

Vera Thorstensen

Professor at São Paulo School of Economics of Fundação Getúlio Vargas (EESP-FGV),

Head of the Center for Global Trade and Investments Studies (CGTI), and Holder of the

WTO Chair in Brazil since 2014. President of the Brazil’s Governmental Committee on

Coordination of Technical Barriers to Trade (CBTC) of INMETRO since 2014. She served

as economic advisor for the Brazilian Mission to the WTO from 1995 to 2010 and

editor-in-chief of Carta de Genebra, published by the Brazilian Mission to the WTO from 2001

to 2008. She also served as Chairperson of the WTO Committee on Rules Origin from 2004

to 2010.

Lucas Pedreira do Couto Ferraz

Lucas Ferraz is Professor of Economics at the São Paulo School of Economics (EESP) from

Fundação Getulio Vargas (FGV). He holds a BD and Masters in Engineering from the

Polytechnic School (POLI) at São Paulo University (USP). He received his PhD in

Economics from Getúlio Vargas Foundation’s Graduate School of Economics

(FGV/EPGE). He participated at the EU scholarship program ALPHA and was a visiting

scholar at the University of Amsterdam, University of Antwerp e University of Brussels.

AUTHORS

Rodolfo Arruda Cabral

Rodolfo Arruda Cabral is a PhD candidate in International Economics at São Paulo School

of Economics (EESP-FGV). He holds a Master in Economics at EESP-FGV, BA in

Economics at Sao Paulo University (USP) and BA in International Relations at Pontifical

Catholic University of Sao Paulo (PUC-SP).

Carolina Lemos Rêgo

Carolina Lemos Rêgo holds a BA in Economics at São Paulo School of Economics

(EESP-FGV) (2016) with a year of studies at the University College London (2015) and the

University St. Gallen (2015). She is a member of the WTO Chair Brazil and a junior

researcher at the Center for Global Trade and Investments (CGTI) of EESP-FGV.

CONTENT

INTRODUCTION ... 7

1.

EXPLAINING THE METHODOLOGY ... 9

1.1.

MODELING

ISSUES ... 9

1.2.

DATA

BASE ... 9

1.3.

RESULTS

OF

THE

SIMULATIONS ... 10

1.4.

REFERENCES ... 10

2.

BRAZIL ... 11

2.1.

SIMULATIONS

OVERVIEW ... 12

2.1.1. Simulation 1 – Brazil x EU – US – China ... 12

2.1.2. Simulation 2 – Brazil x Japan – South Korea – Mexico ... 13

2.1.3. Simulation 3 – Brazil x EU – US – China ... 15

2.1.4. Simulation 4 – Brazil x Japan – South Korea – Mexico ... 16

2.1.5. Simulation 5 – Brazil x EU – US – China ... 18

2.1.6. Simulation 6 – Brazil x Japan – South Korea – Mexico ... 20

2.2.

SIMULATIONS ... 22

2.2.1. Simulation 1 – Brazil x EU – US – China ... 22

2.2.2. Simulation 2 – Brazil x Japan – South Korea – Mexico ... 38

2.2.3. Simulation 3 – Brazil x EU – US – China ... 54

2.2.4. Simulation 4 – Brazil x Japan – South Korea – Mexico ... 70

2.2.5. Simulation 5 – Brazil x EU – US – China ... 86

2.2.6. Simulation 6 – Brazil x Japan – South Korea - Mexico ... 102

3.

MERCOSUL ... 118

3.1.

SIMULATIONS

OVERVIEW ... 119

3.1.1. Simulation 1 – Mercosul x European Union ... 119

3.1.2. Simulation 2 – Mercosul x United States... 120

3.1.3. Simulation 3 – Mercosul x China ... 122

3.1.4. Simulation 4 – Mercosul x European Union ... 124

3.1.5. Simulation 5 – Mercosul x United States... 125

3.1.6. Simulation 6 – Mercosul x Eropean Union ... 127

3.1.7. Simulation 7 – Mercosul x United States... 129

3.1.8. Simulation 8 – Mercosul x China ... 130

3.2.

SIMULATIONS ... 133

3.2.1. Simulation 1 – Mercosul x European Union ... 133

3.2.2. Simulation 2 – Mercosul x United States... 149

3.2.3. Simulation 3 – Mercosul x China ... 165

3.2.4. Simulation 4 – Mercosul x European Union ... 181

3.2.5. Simulation 5 – Mercosul x United States... 197

3.2.6. Simulation 6 – Mercosul x European Union ... 213

3.2.7. Simulation 7 – Mercosul x United States... 229

3.2.8. Simulation 8 – Mercosul x China ... 245

4.

TPP & TTIP ... 261

4.1.

SIMULATIONS

OVERVIEW ... 262

4.1.3. Simulation 3 – Mercosul x TPP – TTIP – TPP + TTIP ... 266

4.2.

SIMULATIONS ... 269

4.2.1. Simulation 1 – Brazil x TPP – TTIP – TPP + TTIP ... 269

4.2.2. Simulation 2 – Argentina x TPP – TTIP – TPP + TTIP ... 300

4.2.3. Simulation 3 – Mercosul x TPP – TTIP – TPP + TTIP ... 331

5.

BRICS ... 362

5.1.

SIMULATIONS

OVERVIEW ... 363

5.1.1. Simulation 1 – BRICS ... 363

5.1.2. Simulation 2 – BRICS ... 364

5.2.

SIMULATIONS ... 366

5.2.1. Simulation 1 – BRICS ... 366

5.2.2. Simulation 2 – BRICS ... 382

ANNEX ... 398

INTRODUCTION

The main objective of this e-book is to present a synthesis of several studies that the Center

for Global Trade and Investment at Fundação Getulio Vargas (CGTI – FGV) has been

producing since 2013. Produced, at first, in an unrelated manner, the works presented in this

Compendium have been revisited and updated so that all simulations became part of a single

body and, therefore, comparable among each other. What is presented in the following pages

is economic information concerning the possible impacts of preferential trade agreements in

the most diverse spheres, aiming to become references to decisions on trade policies,

especially to Brazil.

The scenario for international trade has been under profound transformations. The impasses

on the Doha Round negotiations in the WTO are being solved through small steps in the

Ministerial Conferences of Bali and Nairobi and the proliferation of preferential trade

agreements (PTAs). This scenario has resulted in a transition for the focus of international

trade activities from the multilateral sphere (WTO) to the preferential sphere (PTA).

Preferential agreements, thus, have become the center for rule negotiation and instruments to

trade, expanding the regulatory frontier, with the creation of a series of rules that surpass

WTO’s charter and deepen several themes related to trade, such as services, intellectual

property, investment, environment and competition.

Preferential trade agreements have ceased to simply offer preferential access to goods and

services markets, by means of reduction or elimination of tariffs, establishing instead new

negotiating forums for the currently most important barriers to trade, non-tariff barriers

(NTBs), which comprehend custom barriers, technical barriers, sanitary and phytosanitary

measures, as well as bureaucratic obstacles to trade and, most importantly, costs risen from

regulatory divergences.

With the progressive reduction of tariff barriers through the negotiations of several rounds in

the GATT and WTO, non-tariff barriers have become relevant as the main new obstacle to

international trade, becoming an essential part to the agenda of preferential agreements. Due

to the importance of the theme and the impacts produced by such barriers in the access of

external markets, there no longer exists a single logic in promoting only the negotiation of

preferential tariffs and not also negotiating non-tariff barriers. In such a case, any potential

benefits can be limited significantly without the negotiation of NTBs. These new barriers

were considered throughout the simulations of this e-book.

Any new PTA proposed as an ambitious instrument of trade integration must address not only

the substantial elimination of tariffs, but also trade related issues as customs barriers, technical

barriers, sanitary and phytosanitary measures – including the difficult questions of standard

harmonization and mutual recognition, trade facilitation, services, investment, competition,

intellectual property, regulatory coherence, amongst other topics, which turn negotiations with

new challenges.

Considering such a scenario, Brazil’s position is questionable. The country holds only a

limited number of agreements in force, agreements which also exhibit low ambition in rule

negotiations. The integration of Brazil in international trade has necessarily to go through the

negotiation of new deals, more ambitious ones, with partners of larger importance for Brazil’s

agreements: the Transatlantic Trade and Investment Partnership (TTIP) and the Trans-Pacific

Partnership (TPP). Such agreements cover a significant share of global trade and represent

true paradigms in terms of rules negotiations, which turns the current moment into an

inflexion point concerning Brazil’s international trade policies. The country will certainly

have to rethink its entire agenda if deciding to become once again relevant to the international

scenario. Options for negotiating PTAs with the European Union or with the US, bilaterally or

within TPP or TTIP are discussed in the following chapters, as well as a closer approximation

to BRICS countries.

In synthesis, it is demonstrated that Brazil should quickly leave its isolated status in the sphere

of international trade, confining itself, in past years, in keeping intact Southern Common

Market (Mercosul) and in giving priority to South America. Further to its bonds with

Mercosul, Brazil must have clear perspectives of gains and losses in each of the negotiations

in which it could possibly engage in.

It is precisely on such perspectives that the present e-book aims to shed light.

Vera Thorstensen

1.

EXPLAINING THE METHODOLOGY

1.1.MODELING ISSUES

The GTAP computable general equilibrium model was used in the following simulations in

order to evaluate the first round effects of alternative preferential trade agreements involving

Brazil, amongst other countries. For a description of the standard GTAP model, see Hertel

(1997).

The GTAP model is a global comparative static applied general equilibrium model. The

model identifies 57 sectors in 153 regions of the world. Its system of equations is based on

microeconomic foundations providing a detailed specification of household and perfect

competitive firm behavior within individual regions and trade linkages between regions. In

addition to trade flows, the GTAP model also recognizes global transportation costs.

The GTAP model qualifies as a Johansen-type model. This model estimates the impacts of

external shocks (gains and losses of a PTA) through a comparative static modeling (before

and after the shock). The solutions are obtained by solving the system of linearized equations

of the model. A typical result shows the percentage change in the set of endogenous variables

(GDP, exports and imports, exchange rate and land value) after a policy shock is carried out,

compared to their values in the initial equilibrium, in a given environment. The schematic

presentation of Johansen solutions for such models is standard in the literature (see Dixon et

al (1992) and Dixon and Parmenter (1996)).

For the modeling of the reduction of non-tariff barriers, this project used the same

methodology presented in Ecorys, 2009.

1.2. DATA BASE

The GTAP 9 database combines detailed bilateral trade, transport and protection data

characterizing economic linkages among 140 regions, together with individual country

input-output data bases which account for inter-sectorial linkages within regions. The dataset is

harmonized and completed with additional sources to provide the most accurate description of

the world economy in 2011 (the last available data base for GTAP).

The main applied protection data used in the GTAP 9 data base originates from ITC’s

MacMap database, which contains exhaustive information at the tariff line level. The ITC

database includes the United Nations Conference on Trade and Development’s (UNCTAD’s)

Trade Analysis and Information System (TRAINS) data base, to which ITC staff added their

own data. The model transforms all specific tariffs in ad valorem tariffs.

In order to capture the first round effects from each preferential trade agreement, the

simulations were carried out using a standard GTAP hypothesis, which considers perfect

factor mobility for labor and capital and imperfect factor mobility for land and natural

resources. National aggregate supply of factors of production is exogenous and production

technology for firms is given.

The way the Brazilian economy variables are affected by horizontal reductions in bilateral

import tariffs will depend on the resulting behavior of domestic relative prices. However, in

import competition from the PTA partner will be favored, as the economy becomes more

preferentially open to trade. Overall efficiency in resource allocation tends to be improved

and, by the same token, possible gains from trade may take national welfare a step up.

Notwithstanding the aggregate benefits from improved resource allocation, regions might be

adversely affected through re-orientation of trade flows – trade diversion – as relative

accessibility changes in the system. Thus, bilateral aggregate gains from trade are not

necessarily accompanied by generalized regional gains in welfare. This issue of trade

diversion versus trade creation has been an important one in the international trade literature,

especially in the case of welfare evaluations of preferential trade agreements.

1.3.RESULTS OF THE SIMULATIONS

The results in the simulations present the impacts for exports and imports, as well as the gains

and losses for the sectorial GDP, in order to evidence the sensitiveness of each sector of the

analyzed country’s economy in relation to a possible PTA negotiation.

The choice for impacts on sectorial GDP can be explained as an attempt to explore the global

effect of each PTA in a more complete evaluation since GDP includes the impacts on

production, exports and imports.

The sectorial results are presented according to the following classification:

Variation on GDP (%) Classification 0 – 1 (+) or (-) 1 – 2 (++) or (--) 2 – 3 (+++) or (---) More than 3 (++++) or (----)

1.4. REFERENCES

DIXON, P. B., Parmenter, B. R., Powell, A. A., & Wilcoxen, P. J. (1992). Notes and problems in applied general equilibrium economics. In C. J. Bliss & M. D. Intriligator (Eds.), Advanced textbooks in economics (Vol. 32). Amsterdam: North-Holland.

DIXON, P. B.,& Parmenter, B. R. (1996). Computable general equilibrium modelling for policy analysis and forecasting. In H. M. Amman, D. A. Kendrick, & J. Rust (Eds.), Handbook of computational economics (Vol. 1, pp. 3–85). Amsterdam: Elsevier.

ECORYS, Non-Tariff Measures in the EU-US Trande and Investment – An Economic Analysis”, Report Prepared by Berden; François; Tamminem; Thelle and Wymenga for the European Commission, 2009, OJ 2007/S180-219493.

EU Commission Staff Working Document, Impact Assessment Report on the Future of EU-US trade relations, Strasbourg, March 2013 (SWD(2013) 68 final).

FRANÇOIS Joseph (coord.), Reducing Transatlantic Barriers to Trade and Investment – An economic Assesment, Centre for Economic Policy Research, London, March 2013

2.

BRAZIL

Possible PTAs of Brazil with: European Union (EU), United States (US), China, Japan, South

Korea and Mexico.

In this section the construction of different scenarios is simulated, considering the following

sectors: agriculture, industry and services.

Simulation 1 compares the impacts on Brazil of PTAs with the EU, the US and China. The

hypothesis assumed in this exercise is of a full liberalization for agriculture, industry and

services for all three countries in their agreements with Brazil, which means no tariff barriers

amongst the partners. This scenario is a good exercise to explore the gains and costs of a full

liberalization on all economic sectors.

Similarly, Simulation 2 compares the impacts on Brazil of PTAs with Japan, South Korea

and Mexico. The hypothesis assumed in this exercise is also of a full liberalization for

agriculture, industry and services for all three countries in their agreements with Brazil.

Simulation 3 compares the impacts on Brazil of PTAs with the EU, the US, and China. In

this scenario, the hypotheses assumed are, on the one hand, of a partial liberalization for

agriculture, with a 50% reduction of tariff barriers, and a full liberalization for industry and

services, for the EU and the US. On the other hand, the hypothesis assumed for China is still

of a full liberalization for agriculture, industry and services.

Simulation 4 compares the impacts on Brazil of PTAs with Japan, South Korea and Mexico.

In this scenario, the hypotheses assumed are, on the one hand, of a partial liberalization for

agriculture, with a 50% reduction of tariff barriers, and a full liberalization for industry and

services, for Japan and South Korea. On the other hand, the hypothesis assumed for Mexico is

still of a full liberalization for agriculture, industry and services.

Simulation 5 once again compares the impacts on Brazil of PTAs with the EU, the US and

China. In this scenario, the hypotheses assumed are, on the one hand, of a partial liberalization

of agriculture, with a 50% reduction of tariff barriers, a full liberalization for industry and

services and a partial liberalization on non-tariff barriers, with a 25% non-tarrif barriers

reduction, for the EU and the US. On the other hand, the hypotheses assumed for China are of

a full liberalization for agriculture, industry and services and a further partial liberalization of

non-tariff barriers for all sectors, with a 25% non-tariff barrier reduction.

Simulation 6 once again compares the impacts on Brazil of PTAs with Japan, South Korea

and Mexico. In this scenario, the hypotheses assumed are, on the one hand, of a partial

liberalization of agriculture, with a 50% reduction of tariff barriers, a full liberalization for

industry and services and a partial liberalization on non-tariff barriers, with a 25% non-tarrif

barriers reduction, for Japan and South Korea. On the other hand, the hypotheses assumed for

Mexico are of a full liberalization for agriculture, industry and services and a further partial

liberalization of non-tariff barriers for all sectors, with a 25% non-tariff barrier reduction.

2.1. SIMULATIONS OVERVIEW

2.1.1.

Simulation 1 – Brazil x EU – US – China

This simulation compares benefits and costs for Brazil after the negotiation of PTAs with the

EU, the US and China.

The hypothesis assumed for all possible partners is of a full liberalization for agriculture,

industry and services, with an elimination of trade barriers amongst trade partners.

Results

Comparing the three agreements, Brazilian bilateral exports increase by 57.9% for the PTA

with the EU, 7.7% for the PTA with the US and 12.2% for the PTA with China. Brazilian

bilateral imports increase by 52.7% for the PTA with the EU, 46.2% for the US and 96.1% for

China.

Considering the values for the year of 2011 (US$ F.O.B.), this would correspond to an

increase of: around US$31 billion in exports to the EU, US$2.5 billion in exports to the US

and US$6.1 billion in exports to China. Regarding imports, the increase would be of US$36.7

billion in imports from the EU, US$18.8 billion in imports from the US and US$32.5 billion

in imports from China.

Within all three PTAs it is possible to observe a significant increase in the exports of

agricultural products, which explains the gains in the land value, in much higher proportion

than the gains in the capital value.

Simulation 1 - Brazil x EU – US – China: Macro economic variables

Macroeconomic Variables EU 27 US China

Nominal GDP 1.2% -0.6% -1.2%

Real GDP 0.0% 0.0% 0.0%

Increase in total exports (US$ mi, F.O.B., 2011) 21,422 5,827 12,918

Increase in total exports % 7.8% 2.1% 4.7%

Increase in total imports (US$ mi, F.O.B., 2011) 19,502 5,496 11,807

Increase in total imports % 7.6% 2.1% 4.6%

Increase in bilateral exports (US$ mi, F.O.B., 2011) 30,996 2,537 6,100

Increase in bilateral exports % 57.9% 7.7% 12.2%

Increase in bilateral imports (US$ mi, F.O.B., 2011) 36,746 18,872 32,558

Increase in bilateral imports % 52.7% 46.2% 96.1%

Terms of trade 1.5% -0.4% -0.7%

Real wage 0.1% 0.0% 0.0%

Land gains 26.8% 2.3% 7.8%

Capital gains 0.3% 0.1% 0.2%

Real exchange rate 1.7% -0.5% -0.9%

In the sectorial analysis, the simulation presents the following results for each sectorial GDP:

For the agricultural sector, the PTA with the US appears to present positive results for the

largest number of sectors, with more expressive gains for sugar, meat and other animal

products. The PTA with the EU, nonetheless, although presenting a smaller number of

agricultural sectors with positive results, offers stronger gains for such, especially in the

sectors related to cereals, sugar, meat and other animal products.

For the industry, the PTA with the US presents the largest number of better results for Brazil,

followed by the PTA with China. The negative results for the PTA with the EU can be

explained by the increase in the agricultural exports, which have been favored in such

agreement.

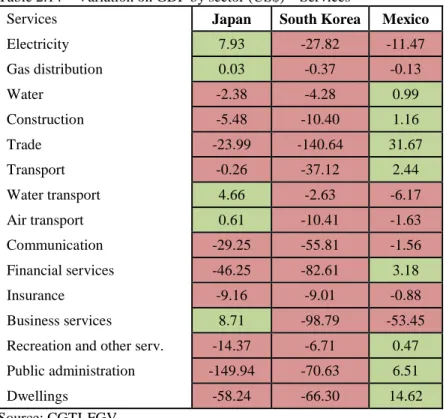

For services, only small gains and losses are verified amongst all agreements.

Simulation 1 – Brazil x EU – US – China: Sectorial AnalysisEU 27 US China Agriculture 9 17 15 Industry 1 15 12 Services 3 6 6 + 4 33 25 ++ 1 4 1 +++ 0 1 3 ++++ 8 0 4 Total 13 38 33 Source: CGTI-FGV

2.1.2.

Simulation 2 – Brazil x Japan – South Korea – Mexico

This simulation compares benefits and costs for Brazil after the negotiation of PTAs with

Japan, South Korea and Mexico.

The hypothesis assumed for all possible partners is of a full liberalization for agriculture,

industry and services, with an elimination of trade barriers amongst trade partners.

Results

Comparing the three agreements, Brazilian bilateral exports increase by 0.4% for the PTA

with Japan, decrease by 0.3% for the PTA with South Korea and decrease by 0.1% for the

PTA with Mexico. Brazilian bilateral imports decrease by 2.6% for the PTA with Japan, 3.3%

for South Korea and 0.2% for Mexico.

Considering the values for the year of 2011 (US$ F.O.B.), this would correspond to an

increase of around US$145.82 million in exports to Japan, a decrease of around US$184.5

million in exports to South Korea and a decrease of around US$63.6 million in exports to

China. Regarding imports, the decrease would be of US$1.1 billion in imports from Japan,

Within the PTAs with Japan and South Korea it is possible to observe a significant increase in

the exports of agricultural products, which explains the gains in the land value, in much

higher proportion than the gains in the capital value.

Simulation 2 - Brazil x Japan – South Korea – Mexico: Macro economic variables

Macroeconomic Variables Japan South Korea Mexico

Nominal GDP -0.1% -0.1% 0.1%

Real GDP 0.0% 0.0% 0.0%

Increase in total exports (US$ mi, F.O.B., 2011) 2,601.88 3,892.24 1,085.18

Increase in total exports % 0.9% 1.4% 0.4%

Increase in total imports (US$ mi, F.O.B., 2011) 2,396.25 3,667.39 953.68

Increase in total imports % 0.9% 1.4% 0.4%

Increase in bilateral exports (US$ mi, F.O.B., 2011) 145.82 -184.48 -63.59

Increase in bilateral exports % 0.4% -0.3% -0.1%

Increase in bilateral imports (US$ mi, F.O.B., 2011) -1,073.18 -2,293.78 -76.00

Increase in bilateral imports % -2.6% -3.3% -0.2%

Terms of trade -0.1% 0.1% 0.1%

Real wage 0.0% 0.0% 0.0%

Land gains 1.5% 6.1% 0.0%

Capital gains 0.0% 0.1% 0.0%

Real exchange rate -0.1% 0.0% 0.1%

Source: CGTI-FGV

In the sectorial analysis, the simulation presents the following results for each sectorial GDP:

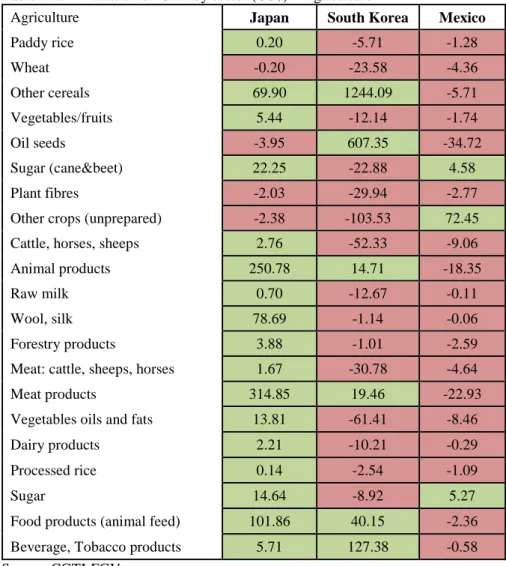

For the agricultural sector, the PTA with Japan appears to present positive results for the

largest number of sectors, with more expressive gains for wool, silk and animal and meat

products.

For the industry, the PTA with Japan once again presents the largest number of better results

for Brazil, followed by the PTA with South Korea.

For services, only small gains and losses are verified amongst all agreements.

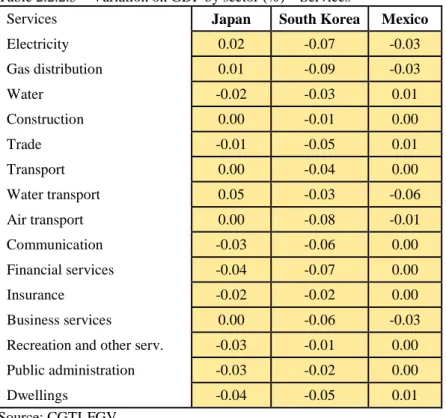

Simulation 2 – Brazil x Japan – South Korea – Mexico: Sectorial AnalysisJapan South Korea Mexico

Agriculture 17 6 3 Industry 11 8 8 Services 5 0 8 + 29 11 19 ++ 1 1 0 +++ 2 0 0 ++++ 1 2 0 Total 33 14 19 Source: CGTI-FGV

2.1.3.

Simulation 3 – Brazil x EU – US – China

This simulation compares benefits and costs for Brazil after the negotiation of PTAs with the

EU, the US and China.

The hypotheses assumed for the EU and the US are of a partial liberalization for agriculture,

with a 50% reduction of trade barriers and a full liberalization for industry and services, with

an elimination of such trade barriers amongst trade partners. The hypothesis assumed for

China is still of a full liberalization for agriculture, industry and services, with an elimination

of trade barriers amongst trade partners.

Results

Comparing the three agreements, Brazilian bilateral exports decrease by 12.3% for the PTA

with the EU, 5.6% for the PTA with the US and increase by 12.2% for the PTA with China.

Brazilian bilateral imports increase by 44.6% for the PTA with the EU, 45.5% for the US, and

96.1% for China.

Considering the values for the year of 2011 (US$ F.O.B.), this would correspond to a

decrease of around US$6.5 billion in exports to the EU, US$1.8 billion in exports to the US

and an increase of US$6.1 billion in exports to China. Regarding imports, the increase would

be of US$31.1 billion in imports from the EU, US$18.6 billion in imports from the US and

US$32.5 billion in imports from China.

Within the PTAs with the US and the EU there is a significant decrease in the exports of

agricultural products, which can be explained by the maintenance of trade barriers to

agricultural sectors by these countries. These decreases, in turn, explain the loss in land value

for Brazil in these agreements. Within the PTA with China, however, due to its full

liberalization of trade barriers, there is an increase in the exports of agricultural products,

which explains the gains in the land value.

Simulation 3 - Brazil x EU – US – China: Macro economic variables

Macroeconomic Variables EU 27 US China

Nominal GDP -2.2% -1.0% -1.2%

Real GDP 0.0% 0.0% 0.0%

Increase in total exports (US$ mi, F.O.B., 2011) 7,340 4,429 12,918

Increase in total exports % 2.7% 1.6% 4.7%

Increase in total imports (US$ mi, F.O.B., 2011) 7,181 4,271 11,807

Increase in total imports % 2.8% 1.7% 4.6%

Increase in bilateral exports (US$ mi, F.O.B., 2011) -6,582 -1,832 6,100

Increase in bilateral exports % -12.3% -5.6% 12.2%

Increase in bilateral imports (US$ mi, F.O.B., 2011) 31,133 18,590 32,558

Increase in bilateral imports % 44.6% 45.5% 96.1%

Terms of trade -1.8% -0.8% -0.7%

Real wage 0.0% 0.0% 0.0%

Land gains -6.9% -1.6% 7.8%

Capital gains 0.0% 0.0% 0.2%

Real exchange rate -1.8% -0.8% -0.9%

In the sectorial analysis, the simulation presents the following results for each sectorial GDP:

For the agricultural sector, the PTA with China presents the largest number of sectors with

positive results, with more expressive gains for the sugar, meat and wheat sectors. The PTA

with the EU, nonetheless, despite presenting a smaller number of agricultural sectors with

positive results, offers stronger gains for such, especially in the sectors related to wheat,

sugar, meat and other animal products.

For the industry, the PTA with the US presents the better results for Brazil, followed by the

PTA with the EU. Such positive results can be explained by the shift in focus from the

agricultural to the industrial sector, due to the conditions of the agreements. Within the PTA

with China, the results for the industrial sector are modest.

For services, only small gains and losses are verified amongst all agreements.

Simulation 3 – Brazil x EU – US – China: Sectorial AnalysisEU 27 US China Agriculture 12 13 15 Industry 15 17 12 Services 8 7 6 + 21 31 25 ++ 4 2 1 +++ 2 4 3 ++++ 8 0 4 Total 35 37 33 Source: CGTI-FGV

2.1.4.

Simulation 4 – Brazil x Japan – South Korea – Mexico

This simulation compares benefits and costs for Brazil after the negotiation of PTAs with

Japan, South Korea and Mexico.

The hypotheses assumed for Japan and South Korea are of a partial liberalization for

agriculture, with a 50% reduction of trade barriers and a full liberalization for industry and

services, with an elimination of such trade barriers amongst trade partners. The hypothesis

assumed for Mexico is still of a full liberalization for agriculture, industry and services, with

an elimination of trade barriers amongst trade partners.

Results

Comparing the three agreements, Brazilian bilateral exports increase by 1.8% for the PTA

with Japan, 0.6% for the PTA with South Korea and decrease by 0.1% for the PTA with

Mexico. Brazilian bilateral imports decrease by 3.1% for the PTA with Japan, 3.6% for South

Korea and 0.2% for Mexico.

Considering the values for the year of 2011 (US$ F.O.B.), this would correspond to an

increase of around US$578.7 million in exports to Japan, US$299 million in exports to South

Korea and a decrease of around US$63.6 million in exports to China. Regarding imports, the

decrease would be of around US$1.25 billion in imports from Japan, US$2.5 billion in

imports from South Korea and US$76 million in imports from Mexico.

Within the PTAs with Japan there is a significant decrease in the exports of agricultural

products, which can be explained by the maintenance of trade barriers to agricultural sectors

by this country. This decrease, in turn, explains the loss in land value for Brazil in the

agreement.

Simulation 4 - Brazil x Japan – South Korea – Mexico: Macro economic variables

Macroeconomic Variables Japan South Korea Mexico

Nominal GDP -0.5% -0.3% 0.1%

Real GDP 0.0% 0.0% 0.0%

Increase in total exports (US$ mi, F.O.B., 2011) 1,144.18 3,034.15 1,085.18

Increase in total exports % 0.4% 1.1% 0.4%

Increase in total imports (US$ mi, F.O.B., 2011) 1,119.93 2,859.96 953.68

Increase in total imports % 0.4% 1.1% 0.4%

Increase in bilateral exports (US$ mi, F.O.B., 2011) 578.68 299.00 -63.59

Increase in bilateral exports % 1.8% 0.6% -0.1%

Increase in bilateral imports (US$ mi, F.O.B., 2011) -1,249.63 -2,512.51 -76.00

Increase in bilateral imports % -3.1% -3.6% -0.2%

Terms of trade -0.4% -0.2% 0.1%

Real wage 0.0% 0.0% 0.0%

Land gains -1.1% 3.2% 0.0%

Capital gains 0.0% 0.1% 0.0%

Real exchange rate -0.4% -0.2% 0.1%

Source: CGTI-FGV

In the sectorial analysis, the simulation presents the following results for each sectorial GDP:

For the agricultural sector, the PTA with Japan appears to present positive results for the

largest number of sectors, with more expressive gains for wheat products. The PTA with

South Korea, nonetheless, although presenting a smaller number of agricultural sectors with

positive results, offers stronger gains for such, especially in the sectors related to cereals and

oil seeds.

For the industry, the PTA with Japan presents the largest number of better results for Brazil,

followed by the PTA with South Korea.

Simulation 4 – Brazil x Japan – South Korea – Mexico: Sectorial Analysis Japan South Korea Mexico

Agriculture 15 7 3 Industry 17 15 8 Services 8 4 8 + 37 24 19 ++ 2 0 0 +++ 1 1 0 ++++ 0 1 0 Total 40 26 19 Source: CGTI-FGV

2.1.5.

Simulation 5 – Brazil x EU – US – China

This simulation compares benefits and costs for Brazil after the negotiations of PTAs with the

EU, the US, China and Japan.

The hypotheses assumed for the EU and the US are of a partial liberalization for agriculture,

with a 50% reduction of trade barriers and a full liberalization for industry and services, with

an elimination of such trade barriers amongst trade partners. The hypothesis assumed for

China is still of a full liberalization for agriculture, industry and services, with an elimination

of trade barriers amongst trade partners. Furthermore, it is considered the hypothesis of a

partial liberalization of non-tariff barriers amongst all partners, with a 25% non-tariff barrier

reduction.

Results

Comparing the four agreements, Brazilian bilateral exports increase by 74.4% for the PTA

with the EU, 105.4% for the PTA with the US and 83.0% for the PTA with China. Brazilian

bilateral imports increase by 126.4% for the PTA with the EU, 156.9% for the US and

226.1% for China.

Considering the values given for the year of 2011 (US$ F.O.B.), this would correspond to an

increase of: around US$39.8 billion in exports to the EU, US$26.4 billion in exports to the US

and US$33.1 billion in exports to China. Regarding imports, the increase would be of

US$88.1 billion in imports from the EU, US$64.1 billion in imports from the US and

US$76.6 billion in imports from China.

In comparison with the results presented in the previous simulation, the significant increases

in exports within all three PTAs can be explained by the partial liberalization of non-trade

barriers, which appear to have great influence in the determination of trade amongst countries.

Within the PTAs with the EU and China the gains in the land value can be explained by

increase in exports of agricultural products.

Simulation 5 - Brazil x EU – US – China: Macro economic variables

Macroeconomic Variables EU 27 US China

Nominal GDP 0.1% 0.7% -0.2%

Real GDP 0.7% 0.5% 0.5%

Increase in total exports (US$ mi, F.O.B., 2011) 40,335 29,827 37,883

Increase in total exports % 14.7% 10.9% 13.8%

Increase in total imports (US$ mi, F.O.B., 2011) 36,145 26,423 33,122

Increase in total imports % 14.0% 10.2% 12.8%

Increase in bilateral exports (US$ mi, F.O.B., 2011) 39,816 34,599 41,537

Increase in bilateral exports % 74.4% 105.4% 83.0%

Increase in bilateral imports (US$ mi, F.O.B., 2011) 88,158 64,170 76,592

Increase in bilateral imports % 126.4% 156.9% 226.1%

Terms of trade -0.2% 0.5% 0.7%

Real wage 0.9% 0.7% 0.2%

Land gains 7.6% -4.2% 29.4%

Capital gains 0.9% 0.6% 0.7%

Real exchange rate 0.7% 1.0% 0.4%

Source: CGTI-FGV

In the sectorial analysis, the simulation presents the following results for each sectorial GDP:

For the agricultural sector, the PTA with the EU presents the largest number of sectors with

positive results, with more expressive gains for the wool and meat sectors. The PTA with

China, nonetheless, despite presenting a smaller number of agricultural sectors with positive

results, offers stronger gains for such, especially in the sectors related to sugar, oil seeds, meat

and other animal products.

For the industry, the PTA with Japan is the one that presents the better results for Brazil,

followed by the PTA with the US. The negative results for the PTA with China can be

explained by the increase in the agricultural exports, which have been favored in such

agreement.

For services, small gains for all agreements are verified.

Simulation 5 – Brazil x EU – US – China: Sectorial AnalysisSource: CGTI-FGV EU 27 US China Agriculture 9 3 7 Industry 9 10 7 Services 11 13 11 + 17 20 14 ++ 2 1 2 +++ 2 1 1 ++++ 8 4 8 Total 29 26 25

2.1.6.

Simulation 6 – Brazil x Japan – South Korea – Mexico

This simulation compares benefits and costs for Brazil after the negotiation of PTAs with

Japan, South Korea and Mexico.

The hypotheses assumed for Japan and South Korea are of a partial liberalization for

agriculture, with a 50% reduction of trade barriers and a full liberalization for industry and

services, with an elimination of such trade barriers amongst trade partners. The hypothesis

assumed for Mexico is still of a full liberalization for agriculture, industry and services, with

an elimination of trade barriers amongst trade partners. Furthermore, it is considered the

hypothesis of a partial liberalization of non-tariff barriers amongst all partners, with a 25%

non-tariff barrier reduction.

Results

Comparing the three agreements, Brazilian bilateral exports increase by 1.8% for the PTA

with Japan, 1.1% for the PTA with South Korea and decrease by 0.1% for the PTA with

Mexico. Brazilian bilateral imports decrease by 9.2% for the PTA with Japan, 9.4% for South

Korea and 1.5% for Mexico.

Considering the values for the year of 2011 (US$ F.O.B.), this would correspond to an

increase of around US$606.8 million in exports to Japan, US$599.3 million in exports to the

US and a decrease of around US$343.3 million in exports to Mexico. Regarding imports, the

decrease would be of around US$3.7 billion in imports from Japan, US$6.5 billion in imports

from South Korea and US$521.7 million in imports from Mexico.

Within the PTAs with Japan and South Korea it is possible to observe a significant increase in

the exports of agricultural products, which explains the gains in the land value, in much

higher proportion than the gains in the capital value.

Simulation 6 - Brazil x Japan – South Korea – Mexico: Macro economic variables

Macroeconomic Variables Japan South Korea Mexico

Nominal GDP -0.5% -0.4% 0.6%

Real GDP 0.1% 0.1% 0.1%

Increase in total exports (US$ mi, F.O.B., 2011) 6,866.81 8,095.86 5,781.65

Increase in total exports % 2.5% 3.0% 2.1%

Increase in total imports (US$ mi, F.O.B., 2011) 6,043.63 7,267.33 5,040.98

Increase in total imports % 2.3% 2.8% 2.0%

Increase in bilateral exports (US$ mi, F.O.B., 2011) 606.81 599.32 -343.30

Increase in bilateral exports % 1.8% 1.1% -0.7%

Increase in bilateral imports (US$ mi, F.O.B., 2011) -3,768.33 -6,587.08 -521.68

Increase in bilateral imports % -9.2% -9.4% -1.5%

Terms of trade -0.4% -0.4% 0.4%

Real wage 0.1% 0.1% 0.2%

Land gains 1.0% 4.7% -0.2%

Capital gains 0.1% 0.2% 0.1%

Real exchange rate -0.3% -0.3% 0.6%

In the sectorial analysis, the simulation presents the following results for each sectorial GDP:

For the agricultural sector, the PTA with Japan appears to present positive results for the

largest number of sectors, with more expressive gains for wool, silk and meat products. The

PTA with South Korea, nonetheless, although presenting a smaller number of agricultural

sectors with positive results, offers stronger gains for such, especially in the sectors related to

cereals and oil seeds.

For the industry, the PTA with Japan presents the largest number of better results for Brazil,

followed by the PTA with South Korea.

For services, only small gains and losses are verified amongst all agreements.

Simulation 6 – Brazil x Japan – South Korea – Mexico: Sectorial AnalysisJapan South Korea Mexico

Agriculture 19 12 4 Industry 13 14 8 Services 10 10 10 + 38 32 19 ++ 2 1 2 +++ 0 1 1 ++++ 2 2 0 Total 42 36 22 Source: CGTI-FGV

2.2. SIMULATIONS

2.2.1.

Simulation 1 – Brazil x EU – US – China

Hypothesis: EU, US, China – Full liberalization on Agriculture + Agribusiness + Industry + Services Table 2.2.1.1 – Variation on GDP by sector (%) – Agriculture

Agriculture EU 27 US China Paddy rice -0.74 0.19 0.23 Wheat -8.32 0.90 0.72 Other cereals 4.30 0.31 0.28 Vegetables/fruits 1.17 0.28 -0.06 Oil seeds -5.06 0.60 3.63 Sugar (cane&beet) 6.14 0.69 4.81 Plant fibres -6.00 -0.47 -1.77

Other crops (unprepared) -2.94 0.85 0.83

Cattle, horses, sheeps 28.51 0.22 0.04

Animal products 14.02 0.63 1.33

Raw milk -0.59 -0.12 -0.19

Wool, silk -0.17 0.00 -0.17

Forestry products -0.73 0.13 0.20

Meat: cattle, sheeps, horses 37.91 0.26 0.03

Meat products 25.56 1.16 2.65

Vegetables oils and fats -1.28 0.55 2.29

Dairy products -0.85 -0.11 -0.13

Processed rice -0.43 0.10 0.17

Sugar 10.05 1.16 6.71

Food products (animal feed) 4.23 0.28 0.21

Beverage, Tobacco products -0.42 -0.34 0.00

Simulation 1 – Brazil x EU – US – China

Hypothesis: EU, US, China – Full liberalization on Agriculture + Agribusiness + Industry + Services Table 2.2.1.2 –– GDP: Gains and losses by sector – Agriculture

Agriculture EU 27 US China Paddy rice - + + Wheat ---- + + Other cereals ++++ + + Vegetables/fruits ++ + - Oil seeds ---- + ++++ Sugar (cane&beet) ++++ + ++++ Plant fibres ---- - --

Other crops (unprepared) --- + +

Cattle, horses, sheeps ++++ + +

Animal products ++++ + ++

Raw milk - - -

Wool, silk - + -

Forestry products - + +

Meat: cattle, sheeps, horses ++++ + +

Meat products ++++ ++ +++

Vegetables oils and fats -- + +++

Dairy products - - -

Processed rice - + +

Sugar ++++ ++ ++++

Food products (animal feed) ++++ + +

Beverage, Tobacco products - - -

Total (positive results) 9 17 15

Source: CGTI-FGV Variation on GDP (%) Classification 0 – 1 (+) or (-) 1 – 2 (++) or (--) 2 – 3 (+++) or (---) More than 3 (++++) or (----)

Simulation 1 – Brazil x EU – US – China

Hypothesis: EU, US, China – Full liberalization on Agriculture + Agribusiness + Industry + Services Table 2.2.1.3 – Variation on GDP by sector (%) – Industry

Industry EU 27 US China Extractive Fishing 0.47 0.02 0.01 Coal -0.85 0.28 0.58 Oil -0.54 0.23 0.42 Gas -0.64 0.21 0.46 Minerals -1.16 0.36 0.80 Manufacturing Textiles -3.10 -0.13 -9.42 Apparel -1.47 0.11 -4.86 Leather products -1.78 2.31 -3.86 Wood products -2.28 0.17 -0.27 Paper products -1.53 0.21 0.67 Petroleum products -0.27 0.08 0.18

Chemical, rubber, plastics -2.77 -0.38 0.63

Mineral (non-metallic) -1.18 0.33 -0.46

Iron, steel -4.71 0.09 0.04

Metals (non-ferrous) -5.71 1.11 2.17

Metal products -3.80 -0.70 -1.09

Motor vehicles and parts -3.34 0.18 0.20

Transport equipament -2.77 1.25 3.38

Electronic equipment -1.59 -0.20 -1.82

Machinery and equipment -8.33 -1.78 -1.91

Others Manufactures -0.86 -0.06 -1.47

Simulation 1 – Brazil x EU – US – China

Hypothesis: EU, US, China – Full liberalization on Agriculture + Agribusiness + Industry + Services Table 2.2.1.4 –– GDP: Gains and losses by sector – Industry

Industry EU 27 US China Extractive Fishing + + + Coal - + + Oil - + + Gas - + + Minerals -- + + Manufacturing Textiles ---- - ---- Apparel -- + ---- Leather products -- +++ ---- Wood products --- + - Paper products -- + + Petroleum products - + +

Chemical, rubber, plastics --- - +

Mineral (non-metallic) -- + -

Iron, steel ---- + +

Metals (non-ferrous) ---- ++ +++

Metal products ---- - --

Motor vehicles and parts ---- + +

Transport equipament --- ++ ++++

Electronic equipment -- - --

Machinery and equipment ---- -- --

Others Manufactures - - --

Total (positive results) 1 15 12

Source: CGTI-FGV Variation on GDP (%) Classification 0 – 1 (+) or (-) 1 – 2 (++) or (--) 2 – 3 (+++) or (---) More than 3 (++++) or (----)

Simulation 1 – Brazil x EU – US – China

Hypothesis: EU, US, China – Full liberalization on Agriculture + Agribusiness + Industry + Services Table 2.2.1.5 – Variation on GDP by sector (%) – Services

Services EU 27 US China Electricity -0.65 0.13 0.22 Gas distribution -0.94 0.16 0.17 Water 0.01 -0.05 -0.06 Construction -0.03 0.00 0.00 Trade -0.02 -0.03 -0.09 Transport -0.07 0.01 0.07 Water transport -1.13 0.37 0.81 Air transport -0.57 0.09 0.16 Communication -0.33 -0.04 -0.03 Financial services -0.36 -0.05 -0.04 Insurance -0.14 -0.04 -0.02 Business services -0.57 0.12 0.28

Recreation and other serv. -0.03 -0.06 -0.02

Public administration 0.03 -0.08 -0.10

Dwellings 0.00 -0.12 -0.21

Simulation 1 – Brazil x EU – US – China

Hypothesis: EU, US, China – Full liberalization on Agriculture + Agribusiness + Industry + Services Table 2.2.1.6 –– GDP: Gains and losses by sector – Services

Services EU 27 US China Electricity - + + Gas distribution - + + Water + - - Construction - - - Trade - - - Transport - + + Water transport -- + + Air transport - + + Communication - - - Financial services - - - Insurance - - - Business services - + +

Recreation and other serv. - - -

Public administration + - -

Dwellings + - -

Total (No. of positive results) 3 6 6

Source: CGTI-FGV Variation on GDP (%) Classification 0 – 1 (+) or (-) 1 – 2 (++) or (--) 2 – 3 (+++) or (---) More than 3 (++++) or (----)

Simulation 1 – Brazil x EU – US – China

Hypothesis: EU, US, China – Full liberalization on Agriculture + Agribusiness + Industry + Services Table 2.2.1.7 – Summary of gains - GDP by sector

EU 27 US China Agriculture 9 17 15 Industry 1 15 12 Services 3 6 6 + 4 33 25 ++ 1 4 1 +++ 0 1 3 ++++ 8 0 4 Total 13 38 33 Source: CGTI-FGV

Table 2.2.1.8 – Macroeconomic outlook

Macroeconomic Variables EU 27 US China

Nominal GDP 1.2% -0.6% -1.2%

Real GDP 0.0% 0.0% 0.0%

Increase in total exports (US$ mi, F.O.B., 2011) 21,422 5,827 12,918

Increase in total exports % 7.8% 2.1% 4.7%

Increase in total imports (US$ mi, F.O.B., 2011) 19,502 5,496 11,807

Increase in total imports % 7.6% 2.1% 4.6%

Increase in bilateral exports (US$ mi, F.O.B., 2011) 30,996 2,537 6,100

Increase in bilateral exports % 57.9% 7.7% 12.2%

Increase in bilateral imports (US$ mi, F.O.B., 2011) 36,746 18,872 32,558

Increase in bilateral imports % 52.7% 46.2% 96.1%

Terms of trade 1.5% -0.4% -0.7%

Real wage 0.1% 0.0% 0.0%

Land gains 26.8% 2.3% 7.8%

Capital gains 0.3% 0.1% 0.2%

Real exchange rate 1.7% -0.5% -0.9%

Simulation 1 – Brazil x EU – US – China Table 2.2.1.9 – Trade Balance: Agriculture

Agriculture EU 27 US China

∆ Trade balance % % ∆ Trade balance % % ∆ Trade balance % %

(US$ Million) Exports Imports (US$ Million) Exports Imports (US$ Million) Exports Imports Paddy rice -27.70 3.81 221.53 2.90 17.14 96.61 1.81 3.13 -3.51 Wheat -299.91 282.93 13.55 11.43 2.22 51.28 10.66 11.79 -3.07 Other cereals -163.75 -10.42 12.58 7.64 0.74 0.55 3.71 3.31 9.98 Vegetables/fruits -10.91 8.79 41.71 3.47 1.64 39.63 -22.35 44.99 46.02 Oil seeds -892.18 -9.93 32.39 64.72 21.99 20.72 795.90 7.02 27.14 Sugar (cane&beet) -0.10 -30.61 27.75 0.00 0.67 0.32 -0.02 -6.39 19.58 Plant fibres -163.32 -12.30 29.43 -28.32 16.29 17.09 190.26 27.76 -4.89 Other crops (unprepared) -1144.72 -8.55 44.01 321.22 11.28 19.04 321.92 58.83 17.18 Cattle, horses, sheeps -120.57 -18.65 48.16 3.69 3.79 0.73 3.80 1.51 -1.62 Animal products -48.68 -4.08 25.14 1.05 2.06 8.54 -0.51 53.66 16.54 Raw milk -1.06 -25.13 28.96 0.06 2.44 -1.54 0.05 2.48 -1.43 Wool, silk -6.49 -32.38 24.73 0.66 4.33 -2.82 0.01 7.07 -7.10 Forestry products -2.55 -3.52 15.93 0.65 2.51 20.29 1.86 6.15 29.47 Meat: cattle, sheeps, horses 15314.88 2802.44 52.33 73.93 3.37 53.51 139.07 150.17 59.49 Meat products 7006.25 487.02 72.81 265.06 15.80 139.08 630.56 57.05 -4.92 Vegetables oils and fats -729.26 -9.32 78.07 114.50 4.13 87.03 620.79 78.58 89.81 Dairy products -138.47 59.83 175.35 -2.02 165.50 170.93 18.96 111.55 155.20 Processed rice -40.95 136.07 75.61 11.16 4.85 68.40 19.50 4.52 -3.19 Sugar 4063.15 559.62 102.22 379.89 73.44 125.82 2242.76 174.18 170.72 Food products (animal feed) 1493.67 125.28 52.46 192.86 23.02 58.40 131.06 57.77 39.15 Beverage, Tobacco products -111.77 47.85 43.09 -141.31 4.47 36.60 36.27 35.85 50.65

Simulation 1 – Brazil x EU – US – China Table 2.2.1.10 – Trade Balance: Industry

Industry EU 27 US China

∆ Trade balance % % ∆ Trade balance % % ∆ Trade balance % %

Extractive (US$ Million) Exports Imports (US$ Million) Exports Imports (US$ Million) Exports Imports Fishing -8.81 7.52 8.17 1.71 0.96 19.76 3.89 53.79 13.21 Coal 39.31 2.90 -1.56 -3.99 -0.09 -0.10 -8.48 0.01 -0.65 Oil -140.16 -1.05 0.09 80.93 1.48 -0.39 129.04 1.06 -0.61 Gas 16.26 1.12 -1.85 1.77 1.26 -0.78 -0.40 0.92 -0.08 Minerals -32.69 -0.66 1.23 51.83 0.58 1.21 160.33 1.11 5.95 Manufacturing Textiles -678.17 32.87 263.40 -102.98 48.10 271.44 -2051.29 178.32 148.14 Apparel -647.17 49.08 567.65 24.15 100.36 701.38 -1891.84 250.79 215.94 Leather products -269.92 14.64 401.70 355.71 69.49 440.79 -739.34 67.74 185.65 Wood products -224.98 3.92 138.81 12.21 8.37 128.36 -14.04 11.07 110.01 Paper products -809.49 -4.98 63.97 97.69 3.54 47.91 368.27 7.81 72.69 Petroleum products 214.53 -0.74 0.36 66.84 3.40 1.76 3.49 24.49 1.34 Chemical, rubber, plastics -4215.85 1.37 48.93 -958.14 14.14 50.56 994.08 56.21 58.73 Mineral (non-metallic) -312.23 -0.86 52.35 118.52 19.09 61.48 -169.88 89.88 62.44 Iron, steel -737.01 -3.20 64.49 244.46 5.39 79.57 274.34 14.68 68.66 Metals (non-ferrous) -284.13 6.85 55.93 277.48 5.58 70.20 510.08 11.53 92.83 Metal products -1426.66 -6.13 119.03 -355.38 6.27 143.91 -592.35 101.82 125.35 Motor vehicles and parts -2882.44 12.44 113.89 57.47 6.91 131.36 -20.92 53.05 204.03 Transport equipament -420.85 -3.80 32.14 143.69 5.55 7.57 473.07 45.49 189.62 Electronic equipment -848.65 -5.38 87.59 -122.31 6.18 87.77 -1327.23 18.31 50.64 Machinery and equipment -6836.64 -3.37 86.59 -1891.15 7.01 97.24 -2027.94 97.95 114.67 Manufactures -371.64 -6.91 139.50 -27.93 4.85 161.15 -570.76 170.54 103.90

Simulation 1 – Brazil x EU – US – China Table 1.11 – Trade Balance: Services

Services EU 27 US China

∆ Trade balance % % ∆ Trade balance % % ∆ Trade balance % %

(US$ Million) Exports Imports (US$ Million) Exports Imports (US$ Million) Exports Imports Electricity -57.62 -6.93 1.59 21.90 2.97 -1.55 43.33 5.87 -2.71 Gas distribution -3.60 -4.74 4.43 0.44 2.78 -1.48 0.90 4.68 -1.79 Water -3.88 -6.58 2.80 1.53 2.98 -2.07 3.08 6.15 -4.00 Construction -8.91 -4.19 1.99 4.24 2.37 -1.63 8.81 4.85 -2.98 Trade -166.21 -5.07 2.64 62.39 2.22 -1.68 133.17 4.57 -3.10 Transport -136.59 -3.96 2.14 57.56 1.85 -1.40 118.00 4.04 -2.84 Water transport -90.97 -3.59 0.47 43.47 1.67 -0.81 93.95 3.60 -1.46 Air transport -96.04 -3.75 1.63 40.79 1.67 -1.05 80.72 3.58 -2.17 Communication -33.61 -4.95 1.92 13.66 2.15 -1.60 27.85 4.56 -3.03 Financial services -94.10 -5.23 1.77 41.33 2.15 -1.53 81.42 4.55 -3.25 Insurance -67.71 -5.16 2.12 25.48 2.13 -1.43 52.03 4.44 -2.82 Business services -810.54 -5.01 1.86 315.76 2.15 -1.43 641.88 4.56 -2.69 Recreation and other serv. -94.63 -5.01 2.55 36.96 2.18 -1.58 77.10 4.83 -3.18 Public administration -205.91 -4.90 2.12 88.68 2.09 -1.49 174.69 4.77 -3.12 Dwellings 0.00 -0.02 5.93 0.00 0.67 -1.92 0.00 1.36 -3.66

Simulation 1 – Brazil x EU – US – China

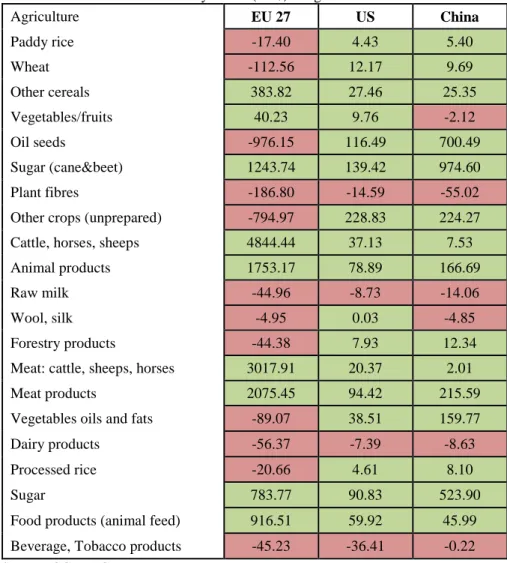

Hypothesis: EU, US, China – Full liberalization on Agriculture + Agribusiness + Industry + Services Table 1.12 – Variation on GDP by sector (US$) – Agriculture

Agriculture EU 27 US China Paddy rice -17.40 4.43 5.40 Wheat -112.56 12.17 9.69 Other cereals 383.82 27.46 25.35 Vegetables/fruits 40.23 9.76 -2.12 Oil seeds -976.15 116.49 700.49 Sugar (cane&beet) 1243.74 139.42 974.60 Plant fibres -186.80 -14.59 -55.02

Other crops (unprepared) -794.97 228.83 224.27

Cattle, horses, sheeps 4844.44 37.13 7.53

Animal products 1753.17 78.89 166.69

Raw milk -44.96 -8.73 -14.06

Wool, silk -4.95 0.03 -4.85

Forestry products -44.38 7.93 12.34

Meat: cattle, sheeps, horses 3017.91 20.37 2.01

Meat products 2075.45 94.42 215.59

Vegetables oils and fats -89.07 38.51 159.77

Dairy products -56.37 -7.39 -8.63

Processed rice -20.66 4.61 8.10

Sugar 783.77 90.83 523.90

Food products (animal feed) 916.51 59.92 45.99

Beverage, Tobacco products -45.23 -36.41 -0.22

Simulation 1 – Brazil x EU – US – China

Hypothesis: EU, US, China – Full liberalization on Agriculture + Agribusiness + Industry + Services Table 1.13 – Variation on GDP by sector (US$) – Industry

Industry EU 27 US China Extractive Fishing 10.61 0.37 0.21 Coal -1.12 0.37 0.77 Oil -147.42 62.07 116.66 Gas -3.80 1.27 2.74 Minerals -429.68 134.54 295.91 Manufacturing Textiles -497.37 -20.34 -1512.56 Apparel -217.39 15.90 -719.48 Leather products -119.17 154.99 -259.05 Wood products -181.07 13.84 -21.24 Paper products -477.58 64.31 207.77 Petroleum products -10.80 3.04 7.11

Chemical, rubber, plastics -2198.86 -300.64 497.81

Mineral (non-metallic) -185.75 52.27 -72.88

Iron, steel -1019.37 19.76 8.41

Metals (non-ferrous) -289.84 56.36 110.38

Metal products -1108.46 -203.23 -318.19

Motor vehicles and parts -802.14 44.21 46.94

Transport equipament -160.66 72.68 196.00

Electronic equipment -416.60 -52.40 -476.86

Machinery and equipment -2615.37 -559.81 -599.92

Others Manufactures -146.86 -9.54 -250.60

Simulation 1 – Brazil x EU – US – China

Hypothesis: EU, US, China – Full liberalization on Agriculture + Agribusiness + Industry + Services Table 1.14 – Variation on GDP by sector (US$) – Services

Services EU 27 US China Electricity -270.64 55.76 89.73 Gas distribution -3.81 0.66 0.68 Water 2.12 -7.46 -9.37 Construction -36.12 -4.07 -1.97 Trade -59.92 -105.22 -266.87 Transport -61.52 8.92 58.78 Water transport -107.28 35.12 77.61 Air transport -71.05 11.58 19.73 Communication -290.94 -34.56 -23.26 Financial services -453.16 -65.21 -53.74 Insurance -53.43 -14.51 -6.78 Business services -1003.97 214.84 489.49

Recreation and other serv. -16.74 -29.96 -9.51

Public administration 119.97 -369.48 -430.24

Dwellings 0.20 -174.82 -300.50

Simulation 1 – Brazil x EU – US – China Table 1.15 – Trade Balance – Agriculture

Agriculture EU 27 US China

∆ Trade balance Exports Imports ∆ Trade balance Exports Imports ∆ Trade balance Exports Imports (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) Paddy rice -27.70 1.46 0.49 -27.70 1.46 0.49 1.81 0.00 0.00 Wheat -299.91 10.44 0.12 -299.91 10.44 0.12 10.66 0.61 0.00 Other cereals -163.75 -33.46 0.02 -163.75 -33.46 0.02 3.71 0.21 0.12 Vegetables/fruits -10.91 54.01 61.90 -10.91 54.01 61.90 -22.35 0.51 67.59 Oil seeds -892.18 -257.04 0.59 -892.18 -257.04 0.59 795.90 827.50 0.17 Sugar (cane&beet) -0.10 -0.01 0.01 -0.10 -0.01 0.01 -0.02 0.00 0.00 Plant fibres -163.32 -3.35 0.17 -163.32 -3.35 0.17 190.26 167.23 0.00 Other crops (unprepared) -1144.72 -472.58 20.10 -1144.72 -472.58 20.10 321.92 261.96 2.11 Cattle, horses, sheeps -120.57 -0.05 7.69 -120.57 -0.05 7.69 3.80 0.00 0.00 Animal products -48.68 -3.26 16.43 -48.68 -3.26 16.43 -0.51 2.87 7.75 Raw milk -1.06 -0.16 0.09 -1.06 -0.16 0.09 0.05 0.01 0.00 Wool, silk -6.49 -0.13 0.01 -6.49 -0.13 0.01 0.01 0.01 0.00 Forestry products -2.55 -0.84 1.50 -2.55 -0.84 1.50 1.86 0.14 0.06 Meat: cattle, sheeps, horses 15314.88 15460.78 3.99 15314.88 15460.78 3.99 139.07 15.73 0.54 Meat products 7006.25 8118.95 19.64 7006.25 8118.95 19.64 630.56 241.79 -0.06 Vegetables oils and fats -729.26 -263.77 220.73 -729.26 -263.77 220.73 620.79 487.61 0.84 Dairy products -138.47 2.50 127.84 -138.47 2.50 127.84 18.96 1.48 3.86 Processed rice -40.95 6.75 3.33 -40.95 6.75 3.33 19.50 0.03 -0.01 Sugar 4063.15 4737.08 1.47 4063.15 4737.08 1.47 2242.76 2208.73 0.31 Food products (animal feed) 1493.67 1944.87 320.38 1493.67 1944.87 320.38 131.06 98.21 164.74 Beverage, Tobacco products -111.77 103.94 250.31 -111.77 103.94 250.31 36.27 0.95 1.11

Simulation 1 – Brazil x EU – US – China Table 1.16 – Trade Balance – Industry

Industry EU 27 US China

∆ Trade balance Exports Imports ∆ Trade balance Exports Imports ∆ Trade balance Exports Imports Extractive (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) Fishing -8.81 0.63 0.24 1.71 0.11 0.34 3.89 0.11 0.10 Coal 39.31 0.00 0.00 -3.99 0.00 -0.91 -8.48 0.00 0.00 Oil -140.16 -9.53 0.00 80.93 54.07 -0.35 129.04 19.60 0.00 Gas 16.26 0.00 -0.54 1.77 0.00 -0.41 -0.40 0.00 0.00 Minerals -32.69 -72.42 2.03 51.83 1.76 2.20 160.33 292.20 1.46 Manufacturing -2051.29 0.00 0.00 Textiles -678.17 29.31 1051.28 -102.98 58.59 577.54 -2051.29 48.12 3519.77 Apparel -647.17 29.37 978.03 24.15 52.02 127.30 -1891.84 29.59 2293.75 Leather products -269.92 171.58 353.92 355.71 260.47 50.76 -739.34 276.98 1524.34 Wood products -224.98 37.60 244.73 12.21 57.45 174.46 -14.04 6.83 282.43 Paper products -809.49 -100.47 650.40 97.69 47.76 212.87 368.27 156.43 138.53 Petroleum products 214.53 -2.35 3.07 66.84 94.92 129.32 3.49 6.37 16.34 Chemical, rubber, plastics -4215.85 46.78 6328.42 -958.14 357.93 4914.25 994.08 348.78 2462.31 Mineral (non-metallic) -312.23 -1.69 321.18 118.52 161.02 149.30 -169.88 10.58 449.89 Iron, steel -737.01 -43.33 670.07 244.46 187.27 255.91 274.34 95.95 569.35 Metals (non-ferrous) -284.13 88.14 420.93 277.48 55.68 139.81 510.08 23.12 324.44 Metal products -1426.66 -18.10 1838.26 -355.38 20.07 892.03 -592.35 24.08 1408.80 Motor vehicles and parts -2882.44 164.18 7029.41 57.47 75.54 1245.64 -20.92 40.94 2647.30 Transport equipament -420.85 -44.20 607.59 143.69 52.02 253.43 473.07 293.00 1058.14 Electronic equipment -848.65 -12.69 1108.08 -122.31 6.96 1073.01 -1327.23 14.24 3378.15 Machinery and equipment -6836.64 -65.92 13196.62 -1891.15 186.83 7944.33 -2027.94 265.60 11188.58 Manufactures -371.64 -8.22 481.39 -27.93 10.38 160.02 -570.76 70.04 922.61

Simulation 1 – Brazil x EU – US – China Table 1.17 – Trade Balance – Services

Services EU 27 US China

∆ Trade balance Exports Imports ∆ Trade balance Exports Imports ∆ Trade balance Exports Imports (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) (US$ Million) Electricity -57.62 -3.70 23.05 21.90 0.55 -0.81 43.33 0.59 -1.67 Gas distribution -3.60 0.00 0.33 0.44 0.00 -0.04 0.90 0.00 -0.01 Water -3.88 -0.81 0.59 1.53 0.32 -0.07 3.08 0.24 -0.06 Construction -8.91 -1.39 1.54 4.24 0.00 0.00 8.81 0.00 -0.06 Trade -166.21 -24.13 46.25 62.39 3.81 -1.91 133.17 10.82 -11.53 Transport -136.59 -23.88 33.52 57.56 9.55 -1.44 118.00 7.59 -2.17 Water transport -90.97 -49.07 11.65 43.47 0.49 -0.48 93.95 0.51 -0.17 Air transport -96.04 -13.64 41.32 40.79 1.77 -5.55 80.72 1.44 -0.32 Communication -33.61 -11.73 5.06 13.66 2.11 -0.38 27.85 1.20 -0.25 Financial services -94.10 -20.12 18.53 41.33 8.15 -9.81 81.42 0.94 -0.27 Insurance -67.71 -6.59 10.80 25.48 5.25 -4.18 52.03 9.61 -1.22 Business services -810.54 -216.00 158.38 315.76 60.96 -16.42 641.88 16.85 -5.48 Recreation and other serv. -94.63 -13.30 38.02 36.96 3.63 -3.22 77.10 2.96 -1.34 Public administration -205.91 -28.37 30.98 88.68 19.58 -27.25 174.69 4.62 -1.76 Dwellings 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2.2.2.

Simulation 2 – Brazil x Japan – South Korea – Mexico

Hypothesis: Japan, South Korea, Mexico – Full liberalization on Agriculture + Agribusiness + Industry + Services

Table 2.2.2.1 – Variation on GDP by sector (%) – Agriculture

Agriculture Japan South Korea Mexico

Paddy rice 0.01 -0.24 -0.05 Wheat -0.02 -1.74 -0.32 Other cereals 0.78 13.93 -0.06 Vegetables/fruits 0.16 -0.35 -0.05 Oil seeds -0.02 3.15 -0.18 Sugar (cane&beet) 0.11 -0.11 0.02 Plant fibres -0.07 -0.96 -0.09

Other crops (unprepared) -0.01 -0.38 0.27

Cattle, horses, sheeps 0.02 -0.31 -0.05

Animal products 2.01 0.12 -0.15

Raw milk 0.01 -0.17 0.00

Wool, silk 2.70 -0.04 0.00

Forestry products 0.06 -0.02 -0.04

Meat: cattle, sheeps, horses 0.02 -0.39 -0.06

Meat products 3.88 0.24 -0.28

Vegetables oils and fats 0.20 -0.88 -0.12

Dairy products 0.03 -0.15 0.00

Processed rice 0.00 -0.05 -0.02

Sugar 0.19 -0.11 0.07

Food products (animal feed) 0.47 0.19 -0.01

Beverage, Tobacco products 0.05 1.19 -0.01