1 A Work Project, presented as part of the requirements for the Award of a Master’s Degree in

Management from the NOVA – School of Business and Economics.

DESIGNING A BALANCED SCORECARD FOR A HYBRID ORGANIZATION: THE CASE OF THE CALOUSTE GULBENKIAN FOUNDATION

MARIA RITA DE HERÉDIA DA CUNHA #2613

A Project carried out on the Master in Management Program, under the supervision of: Professor Maria João Major

2 DESIGNING A BALANCED SCORECARD FOR A HYBRID ORGANIZATION: THE CASE OF THE CALOUSTE GULBENKIAN FOUNDATION

The present Working Project (WP) is an experimental case study on a Portuguese hybrid organization. In 2015 Calouste Gulbenkian Foundation embarked on a strategic reflection with the aim of reinforcing its role in society and becoming a more flexible and efficient organization. As a result, some organizational changes were made. Drawing on the idea that the Balanced Scorecard (BSC) can facilitate change processes (Kaplan & Norton, 2001) and, in contrast to the majority of BSC studies that are focused on for-profit organizations, this WP aims to contribute to help addressing the change process initiated by the foundation by designing a BSC to some of its direct activities.

Key Words: Balanced Scorecard; Foundation; Hybrid Organization; Experimental Case Study

Table of Content

I – Introduction ... 3

II – Literature review ... 5

III - Methodology ... 14

IV- The WP findings ... 16

V – The BSC designed ... 20

VI – Recommendations and main contributions of this WP ... 25

3 I – Introduction

The goal of this working project (WP) is to design a Balanced Scorecard (BSC) for some direct activities of Calouste Gulbenkian Foundation (henceforth, ‘The Foundation’). Created by a clause in the will of a Portugal-based petrol magnate of Armenian origin, Calouste Gulbenkian, The Foundation’s original purpose is focused on fostering knowledge and raising people life quality throughout the fields of the arts, charity, science and education. The achievement of this intention is obtained by providing five different services - Calouste Gulbenkian Museum, Gulbenkian Science Institute, Armenian Communities services, Music service, Art Library service and Gulbenkian Scholarship service – two branches - the French Delegation and the UK Branch - and by developing projects and initiatives in areas such as: Human Development, Education for Culture and Science, Innovation in Health and Portuguese Language and Culture, among others. All services and projects are backed by support services [see appendix I for Foundation Organization Chart].

At the start of this WP, The Foundation was in a strategic reflection period in order to strengthen its role as a driving force of modern philanthropy and social innovation. The current Foundation´s challenge is to align its actions with the changing priorities of society. So, when discussing the implementation of the BSC, which can be a useful management tool in changing environments, with Foundation´s top management team, the definition of scorecards for strategic business units (SBUs) turned the better option. In fact, when companies have a large diversity of activity areas, as in the case of The Foundation, the construction of corporate-level scorecards becomes a difficult and challenging task (Kaplan and Norton, 1993). Due to time constraints and the current Foundation’s situation, three services were chosen to be included in this WP: the Art Library Service, the Music Service and the Calouste Gulbenkian Museum, since they are the

4 priority areas of Gubenkian´s reorganization plan. These areas undertook organizational changes in the period (the Modern Art Center and the Calouste Gulbenkian Museum merged in one single department and the archives management in the Art Library business unit were aggregated), which were considered in the design of the BSCs presented in this WP. It is aimed that this WP works as a pilot project before the design of the BSC for the other activities of the Gulbenkian Foundation.

The BSC can be valuable to line up all The Foundation´s activities and consequentially reduce inequalities and contribute to a more sustainable society. A greater flexibility in foundation’s structure and a reduction on operating costs is also desirable to guarantee the sustainability of Foundation’s activities and would be considered during this project.

This WP is structured in VI Sections. Section II reviews the literature on BSC and Hybrid organizations. Section III rundown the methodology followed in the development of this WP. In Section IV the WP findings are described such as a brief description of Calouste Gulbenkian Foundation and each direct activity included in the BSC. In Section V the researcher delineates the BSC for those activities, and finally, section VI presents a list of recommendations and the main contributions of this WP.

5 II – Literature review

1) The Balanced Scorecard

Developed by Robert Kaplan and David Norton at the beginning of the 1990´s, the BSC is a strategic management system that helps managers to understand the business performance of companies (Kaplan and Norton, 1992), by emphasizing the linkages of measurements to organization’s strategy (Kaplan and Norton, 1993).

It was initially seen as a simple performance measurement system but by the end of the 20th century, strategies for creating value shifted from managing tangible assets to managing intangible assets like costumer relationships, innovative products, and information technology, as examples, which became the major source for competitive advantage. For BSC advocates, the BSC is a powerful tool that companies all over the world would be interested to adopt once understanding the benefits of using it (Kaplan and Norton, 2001).

First of all, knowing that financial measures are known to be performance indicators that lag, that can also be easily manipulated to reach short-term results while forsaking long-term performance and that are often overly-aggregated and difficult to use when managing (Rababa’h, 2014), the BSC suggests a more ‘balanced’ view by adding nonfinancial performance measures to the traditional financial metrics. The role of nonfinancial measures is elevated by Kaplan and Norton (1996) from an operational checklist to a comprehensive system for strategy implementation. Thus, the BSC incorporates two types of performance measures: the lag measures and the drive (or lead) measures. While the former measures describe past performances, which is essential for charting progress but is useless when trying to influence the future, the latter ones are in-process measures and can be used to plan and predict future performances (Kaplan and Norton, 2001).

6 Additionally, the BSC allows a more embracing view by organizing strategic objectives into four different perspectives: Financial, Customers, Internal Business Processes and Learning & Growth. The Financial perspective includes the traditional need of financial data and establishes the strategy for growth, profitability, return-on-investments and risk from de perspective of shareholders. The Customers perspective is focused on costumers’ satisfaction, on supplying competitive and differentiable products and services and being capable to react to market changes. The Internal Business Process perspective aims to understand how well the business is running, if it is possible to reduce costs or maximize productivity, and whether the products and services satisfy customer requirements and shareholders’ interests. Finally, the Learning & Growth perspective, insures long-term improvement, innovation and growth in the organization by managing three distinct capacities1: human resources - recruiting/maintaining high qualified and motivated people; IT systems – aligning information technology with the strategy requirements; and organizational culture and values – through internal business processes, differentiated value proposition and customer relationships (Kaplan and Norton 1996, 2001, 2004, 2006).

Still, by being a strategic planning and management system, it can be useful not only to better align business activities, teams and individuals to the vision and strategy of the organization but also to establish individuals’ and teams’ objectives and remuneration, to allocate resources and to give feedback, among others. It helps to focus managers' attention on strategic issues and the implementation of strategy can be adjusted whenever needed (Kaplan and Norton, 1996).

1 Ability and capacity of an organization expressed in terms of its (1) Human resources: their number, quality, skills, and

experience, (2) Physical and material resources: machines, land, buildings, (3) Financial resources: money and credit, (4) Information resources: pool of knowledge, databases, and (5) Intellectual resources: copyrights, designs, patents, etc. (businessdictionary)

7 But there are some factors that both facilitate and motivate BSC implementation. Some examples are top management support - which is the most important factor to influence BSC implementation - and the access to high information technology - which is the mainly significant factor to facilitate the implementation (Rababa’h, 2014).

However, it is important to state that the BSC itself has no role in the formation of strategy (Lawrie, 2004). The BSC success is on the balance between short and long-term objectives, between financial and non-financial measures, between indicators that are lagging and leading and finally, between perspectives of external and internal performance. All critical variables should be incorporated on a complex set of cause-and-effect relationship among them (Kaplan and Norton, 1996).

The Development of BSC

Some organizations started to use the BSC as a broader framework to manage strategy through four processes. The first process - translation of the vision and strategy – forces managers to understand company’s strategy and translating it into the BSC by setting specific strategic objectives. The second - communicating and linking - consists of communicating the strategy at all levels of the organization and linking it with units, departments, services and individual goals. It should also link rewards to performance measures which are in turn linked to the overall strategy. The third process - Plan, set targets and align strategic initiatives – (also named: Business Planning) enables companies to integrate their business plans with their financial and budgeting plans by establishing targets for the measures that if achieved will transform the company. The fourth - feedback and learning - allows the organization to analyze if strategic

8 objectives are being achieved and to make necessary adjustments to develop the capacity for strategic learning (Kaplan and Norton, 1996).

As mentioned before, the BSC undertook changes over time. The first generation of balanced scorecard designs used a ‘4 box’ approach to identify what measures should be used to track the implementation of strategy. However, a simple ‘causality’ between the four perspectives (Financial, Customers, Internal Business Processes, Learning and Growth) was illustrated but not used for specific purpose. And, although the methods used to select measures to be included in the BSC would be critical to its subsequent success, there was also a lack of a clear definition about how measure selection activity could be done, both in terms of filtering (organizations have access to many more measures than the ones needed to the BSC) and clustering (deciding which measures should appear in which perspectives).

The 2nd Generation of Balanced Scorecard design quickly emerges with the inclusion of a 'strategy map' to fill the weaknesses of the first approach. This means that managers select a few strategic objectives within each of the four perspectives, and then define the cause-effect chain among these objectives rather than among measures, (Kaplan and Norton, 1993) by drawing links between them in order to create a strategy map (Kaplan & Norton, 1996). Once the strategic objectives are decided, managers assign “owners” to each of those objectives. Then, “owners” should define a clear outcome that would allow achieving the said objective and should define the observable parameters that will be used to measure performance against those objectives – the Key Performance Indicators (KPIs) alongside with the specific target values for each KPI. A maximum of 25 KPIs should be added in each BSC which becomes a tool for managers to measure the progress of the company towards a desirable outcome (Kaplan & Norton, 1996).

9 The BSC Criticisms

The most famous weaknesses of the traditional accounting management systems are the difficulty to explain future performance and to link those systems to the strategy of the organization; the fact that they usually provide little information on the causes or solutions to problems; and the fact that the information is too aggregated and summarized to guide management actions and capture key business changes until it is too late (Mohobbot, 2004).

But, although the BSC has been created to solve some of the issues expressed above and the success of BSC has been recognized all over the word, it also attached criticism, especially from the academic community. First, the simplistic and unidirectional relationship between the areas of measurement can lead to a lack of cause-and-effect and invalid assumptions (Norrekelit, 2003). Secondly, there is no time concept in the cause-and-effect relationship. Thirdly, the lack of integration between top-level and operational level measures can lead to misunderstandings on the implementation of BSC (Norrekelit, 2003). Then, the fact that the BSC is based on few measures makes another critical point since the advantage of checking just a few number measures becomes disadvantage when the wrong numbers are selected (Mohobbot, 2004). Also, the framework encourages the focus on internal aspects and doesn’t include questions related to competitors’ movements or changes in external conditions. Finally, stakeholders like suppliers and public authorities are not incorporate in the BSC (Norrektil, 2003). In sum and according to Mohobbot (2004) the traditional BSC concept might be not effective enough to contribute to corporate sustainability.

Additionally, many researchers have been suggesting that some other perspectives might better reflect the priorities of organizations, mainly in organizations in the public and

Non-10 Governmental sectors (Andersen & Lawrie, 2002). Aspects as social dimensions, political issues and human resources elements are important for nonprofit strategies and are not taken in consideration in the BSC (Kong, 2010).

There are alternatives to the BSC framework such as the Total Quality Management (TQM), the European Foundation for Quality Management (EFQM) Excellence Model, the Performance Pyramid, the Performance Prism, the Management by Objectives, and the Blue Ocean Strategy, which can be used by the organizations but all of these tools have strengths and weaknesses too (Norrektil, 2000).

In fact, the major barriers to BSC implementation are its high cost of installing and maintaining the system followed by the lack of information to implement BSC, resistance from employees and a lack of software packages supporting the BSC (Kasurinen, 2002; Rababa’h, 2014).

2) Hybrid organizations

A hybrid organization combines multiple identities which are the central, distinctive, and enduring features of an organization (Haveman & Rao, 2006). In the recent past, researchers start to pay closer attention to hybrids that combine aspects of the charity and business forms (Battilana & Lee, 2014) especially on social enterprises that combine both aspects at their core and thus neither can be dismissed without a fundamental change to the business model (Jay, 2013; Pache & Santos, 2012).

Hybrid organizing is present in essential areas of organizational life, as core organizational activities, workforce composition, organizational design, inter-organizational relationships, and

11 organizational culture. Hybrids vary in the amount of commercial and social goals, in the organization that allow individuals from different sectors to work together effectively, in the way by which organization leaders formally translate strategy into action, in the external relationships with other organizations and other aspects of their environment and in the way a single organizational culture integrate both social and commercial aspects and conciliate norms and values (Battilana & Lee, 2014).

Organizational theories suggest that despite the potential of social enterprises to create both social and economic value (Sabeti, 2011) they are between the business and charity sectors, and thus face the challenge of establishing their legitimacy (Haveman & Rao, 2006). The tensions between the business and charity forms manifest both externally, in managing relations with a bifurcated organizational environment or in the acquisition of financial capital, and internally, in managing organizational identity, resource allocation and decision-making (Moizer & Tracey, 2010).

But, there are hybrid organizations in which business is core and charity is peripheral, named Corporate Social Responsibility (CSR), in which social welfare activities are responsive to environmental demands and by doing so are protecting the core business of the organization (Carroll,1999; McWilliams & Siegel, 2001).

As a result, hybrid organizing can be viewed in terms of the degree to which the business and charity forms are differentiated or integrated. The forms being combined can be more or less integrated, resulting in distinct configurations of hybrid organizing (Battilana & Lee, 2014).

Calouste Gulbenkian Foundation combines both charity and business forms as core organizational features. With the main objective of fostering knowledge and raising the quality of life of persons throughout the fields of the arts, charity, science and education, the organization

12 uses its direct activities, projects, grants and scholarships to accomplish its mission. But, although Gulbenkian has annual revenues obtained through the collection of tickets at the museum and concerts they are not even enough to cover the running costs. Therefore, as the former administrator of the Calouste Gulbenkian Foundation – José Neves Adelino – observed, "Financial markets are a great source on our ability to give to society"(2015). So, the income earned with the investment portfolio and with the oil activity is what really pays the costs of the foundation making businesses as important as the charity form in this organization´s life.

3) Performance Management in Hybrid organizations

In recent years there has been a significant increase in the number of hybrid organizations derived from the rapid changes in the environment and the demands of society (Battilana & Lee, 2014). These types of organizations are playing an increasingly important role in modern economies not only as pioneers of new ideas but also as providers of goods and services and employers (Salamon & Anheier, 1996). They use products, services and consumer choice to achieve the ideas and solve the issues that they believe in (Evers & Laville, 2004). In fact, when hybrids work, they can be a fantastic creative way of solving real-world problems in totally self-sustaining ways, combining the strengths of both for-profit and nonprofit models (Forbes, 2013).

However, because hybrid organizations fall outside the traditional categories they face the challenge of managing both a social and a financial mission and they raise new issues of accountability, control and legitimacy. So, the increased complexity inherent with hybrid organizations has several implications for the management team (Brandsen & Karré, 2011).

13 Even knowing that the main goal of a nonprofit organization (NPO) is not the profitability of shareholder investments but the achievement of its objective and mission, these organizations need to acquire the management capacity of commercial companies (Drucker, 1990).

When Kanter & Summers (1987) studied performance measurement in NPO concluded that the ideal performance evaluation system should acknowledge the existence of several groups and create measurements around all these groups. Another aspect to consider is a distinction between the great mission and operational goals to develop objectives in short and long terms to both groups. Balancing out the interest of all the stakeholders is also central to the system´s success.

However, one of the barriers to apply the scorecard to these sectors is the considerable difficulty that NPOs have in clearly defining their strategy. Most of the documents, once the mission and vision are articulated, consist of lists of programs and initiatives, not the outcomes the organization is trying to achieve (Kaplan and Norton, 2001). NPOs have difficulties on the original architecture of the BSC which placed the financial perspective at the top of the hierarchy although achieving financial success is not the primary objective for these organizations. Hence, nonprofit organizations can consider placing an over-arching objective at the top of their scorecard that represents their long-term objective. For instance, they can place customers or constituents at the top of the hierarchy.

Having in mind that nonprofit organizations have widely adopted the BSC as a measurement tool of effective performance (Kaplan & Norton, 1992), which involves a large range of stakeholder interests to be managed, the use of BSC in hybrid organizations seems to be a valid option (Jansson, 2005).

14 III - Methodology

Grounded on the research question “how to design a BSC in Calouste Gulbenkian Foundation?” the main objective of this WP is to design a BSC for three specific areas of the organization under study: the Art Library Service, the Music Service and the Calouste Gulbenkian Museum. Those are all The Foundation´s direct activities in the field of Art (missing only Gulbenkian Science Institute – field of Science) and are the priority areas of The Foundation´s reorganization plan. Furthermore, when companies have a large diversity of activities’ areas the definition of scorecards for SBU becomes a better option than corporate-level scorecards (Kaplan and Norton, 1993).

Therefore, the research method adopted is an experimental case study since the point is to implement new management accounting practices that are developed from existing literature and would be helpful to practitioners (Ryan et al., 2002).

In addition, an interventionist research (IVR) approach was adopted since the researcher was directly involved in the real-time flow of events (Jonsson and Lukka, 2005), working as a consultant in the BSC´s design and as a researcher when the practical involvement was combined with theoretical contribution. The goal of this WP was to produce contributions that are not only theoretically significant but also practically relevant (Suomala, 2014) for the Gulbenkian Foundation. Thus, the researcher acted as an “actor” (Ryan et al., 2002) by intervening directly in the BSC creation, being engaged, leading interviews, producing support documents and fulfilling deadlines. But, in order to promote knowledge exchange between researcher and practitioners, a balance within the emic (learn from inside the system) and etic (learn from outside the system) domains was taking in consideration by the researcher (Suomala, 2014).

15 To ensure the credibility of the case study, all steps suggested by Ryan et al. (2002) on how to create a case study were followed. After the preparation of the researcher to the study and literature reviewed (first step), the research question was formulated and gathered evidence (second step). The main sources of information were semi-structured interviews, internal archival records, participation in meetings and internal and external documentation. Semi-structured interviews took place not only to help the researcher to get a better idea of the different services´ functions but also to obtain the same type of information that allowed the comparison and understanding of the management processes similarities. The head of each direction were interviewed, some of them more than once, with each interview taking one hour on average, being tape-recorded and notes were taken [see appendix II for the list of interviews]. To assess the reliability and validity of the evidences collected (third step), data triangulation was adopted (see Ryan et al., 2002 and Yin, 2014) by interviewing different people and using multiple source of evidence. Both data triangulation and semi-structured interviews helped on the identification and explanation of patterns (fourth step), which were paramount to design the proposed BSC.

Combining Kaplan and Norton (2004) approach and The Foundation´s actual management system - which already includes periodic measurement of KPIs for some departments - the researcher opted to start by the definition of the departments’ strategic objectives, than the definition of measures, of targets that measure the fulfillment of those objectives, of which initiatives should be undertaken and of how often measurement should take place.

The BSC design plan was elaborated and proposed by the researcher to The Foundation’s top management but the heads of each direct activity were key in this process.

16 IV- The WP findings

a) Calouste Gulbenkian Fundation

The Foundation´s main activities in the field of Art are the permanent collections of the Calouste Gulbenkian Museums exhibitions– The Founder’s Collection and the Modern Collection – and the performances featuring in the Gulbenkian Music season in which the Gulbenkian Orchestra and Choir always play a central role. Furthermore, there are temporary exhibitions, and The Foundation publishes books, speeches and conferences. By awarding study grants and subsidies,

The Foundation renders support to projects and activities to enable the acquisition of new skills, competences and knowledge, in accordance to the aim of the Education Field. The Foundation provides also incentives to facilitate the inclusion of vulnerable groups in the population through the empowerment of people and organizations and by promoting and experimenting innovative solutions. Fostering health as a global public good, stimulating creativity and quality in scientific practices and promoting biomedical research and training new scientific leaders represent some of the core objectives of Foundation actions in the field of Science.

b) Brief profile of the direct activities under study

Art Library and Gulbenkian Archive

As a result of the organization restructured process, the unification of the Art Library (AL) and Gulbenkian Archive (GA) will begin to take effect in the following year [see appendix III for the new service organization chart].

17 With a new mission of “promoting, through the sharing and development of documentary collections and archives, the study and understanding of the Portuguese Visual Arts and Architecture and also the Foundation’s and Founder’s historical/cultural legacies” the main activities of this remodeled service are: the acquisition of books, magazines and other documentary sources for updating and enrichment of AL and GA funds; the acceptance, preservation/conservation and restoration of documents; the digitization/scanning and preservation of photographic and bibliographic materials in the collection of the GA and AL; and the description, digitization and conservation of architect Siza Viera's legacy.

Music Service

The Music service ensures the programming and production of concerts and performances of the Gulbenkian Music Season, structured in several cycles - Gulbenkian Choir and Orchestra, Sunday Concerts, Participatory Concerts, Piano, Major Performers, Old Music, Chamber Music, Soloists of the Gulbenkian Orchestra, Rising Stars, World Music, Jazz in August and Met Opera Live in HD [see appendix IV for the music service organization chart].

Mainly focused in the production of classical music concerts, it is natural that, a significant part of the public is middle to upper class, belonging to older groups and culturally informed. Although particular attention is paid to the fact that this same public is the main source of ticket revenue, in the recent years a new strategy for public diversification have been followed. With the aim of attracting less informed and younger public this service developed new programming lines with more accessible repertoires and prices (Sunday concerts) and brief explanatory comments (Concerts for Schools). More musical genres were also included such as opera, world music, musician-theatrical shows and jazz, among others.

18 Simultaneously, and in collaboration with the Gulbenkian Human Development Program, the Music service wants to extend its intervention in the social area by providing small instrumental trainings to socially vulnerable groups given by Gulbenkian Orchestra members.

Museum Service

The Calouste Gulbenkian Museum was the service who suffered the major restructure until this moment. The unification of both museums – Calouste Gulbenkian Museum and Modern Art Museum – as one direction, led to the creation of a new management team integrated in the various sectors: Curatorship, Programming, Collection Management, Dissemination and Education [see appendix V for the new museum service organization chart].

The main responsibility of the Musuem service is the support and promotion of modern and contemporary art, the study of the Calouste Sarkis Gulbenkian Collection and the contribution to the cultural enrichment of the public through temporary exhibitions, publication of catalogs and the granting of scholarships for contemporary artistic creation and for the internationalization of Portuguese art. The conservation and restoration of pieces, the cataloging, conservation, treatment and digitalization of Archive of the Calouste Gulbenkian collection, the acquisition of consumables (films, photographs, digital media, paper, etc.) and the renewal of stocks of various articles representing the collection for the museum shop are some of the activities executed by this service.

19 c) Description of performance management system in use at the foundation

Calouste Gulbenkian Foundation is developing an accreditation system, the Quality Management System (QMS) that covers aspects as Quality, Environment, Social Responsibility, Hygiene, Heath and Safety at Work. Currently, only the museum exhibitions, the collection peaces loan process and the shops and library activities are under the QMS certification.

This system with the purpose of facilitating the development, implementation and management of each direction’s activities, is made up of two distinct parts: The Transversal Part - which includes processes applicable to the whole institution - and The Specific Part – which includes specific processes of each activity area.

A set of processes and sub-processes were defined for both transversal and specific parts. For example, the transversal process of Human Resources Management is divided in four sub-processes: profiles functions management, recruitment, professional training and performance evaluation. Then, each process/sub-process has a normative documentation with operational procedures that should be followed in order to get the certification of quality.

In fact, the internal documentation supporting the QMS includes: normative documents that define guidelines or methodologies, rules and responsibilities; documents for communicating internal information related to operational subjects; contract documents that link The Foundation to an external certification entity; and documents for recording activities or results of activities. Consequently, there is no process where the result cannot be verified by measurement or monitoring.

20 The responsibility for the QMS implementation belongs to the heads of each unit. Nevertheless, the central services play an important role in the correct functioning of QMS. Firstly because they designed all processes and procedures in closer contact with all business units involved. Secondly, they help on the monitoring and evaluation processes mostly composed of an extensive list of KPIs such as the Satisfaction rate on QMS survey, number of digitalizations or number of foreigns visitors that must be permanently evaluated and reviewed. Finally the central services conducts an internal audit at the end of the first semester to assess the current situation and reviews all the procedures with the respective areas. However, it is only in the last quarter of the year that the QMS is audited by the external certification body, the SGS.

So, although the QMS allows period-on-period comparisons, the major limitation of the QMS is the lack of alignment of the services’ objectives with The Foundation’s strategy. This system is monitored by an extent list of KPIs but do not contemplate the setting of strategic objectives. Therefore, the BSC is intended to complement the current QMS system by integrating a set of objectives and quantifiable measurements, which should be aligned with the Foundation’s strategy and periodically tracked.

V – The BSCs designed

Ideally, the design of The Foundation’s BSC should start at the Board of Trustees and cascade down to all services, projects and initiatives. However, when organizations have a diverse range of Strategic Business Units (SBU), managers in departments and functional units can develop their own scorecard. According to Kaplan and Norton (1996), a department or functional unit should have a BSC when that organizational unit has a mission, a strategy, customers (internal or

21 external), and internal processes that enable it to accomplish its mission and strategy, which is the case of Art Library, Music Service and Caslouste Gulbenkian Museum.

Therefore, based on The Foundation’s vision of promoting knowledge and raising life quality throughout the fields of the arts, charity, education and science the ‘Translating the vision’ process took place by understanding each service mission and how to adapt it to each BSC. The definition of strategic objectives had in considerations several aspects. First of all, the Customer perspective reaches a special importance on The Foundation’s activity and since Gulbenkian Foundation is a non-profit organization the financial perspective loses priority. Consequently, these differences are translated on the reverse order of BSCs perspectives: firstly, the strategic objectives were defined focused on the Customer perspective followed by the Internal Business Processes, Learning and Growth and finally the Financial Perspective.

Then, given three different BSCs are being developed it urged to find the similarities between services to make the best possible alignment between all services and The Foundation´s propose. Thereby, the researcher suggested some common strategy objectives to the tree SBU as: the collaboration with external entities and with other foundations services (under the Customer Perspective); the development of employees’ competences and the implementation of a personal evaluation system (under the Learning and Growth Perspective); or the building of a multi-year financial plan and reach financial contributions (under the Financial Perspective). This line of thought also contributes to a greater flexibility in The Foundation´s structures and to reduce operation costs in the medium-to-long term. Lastly, the researcher used some of the strategic objective already established by each SBU for next year, mostly on Internal Business Perspective.

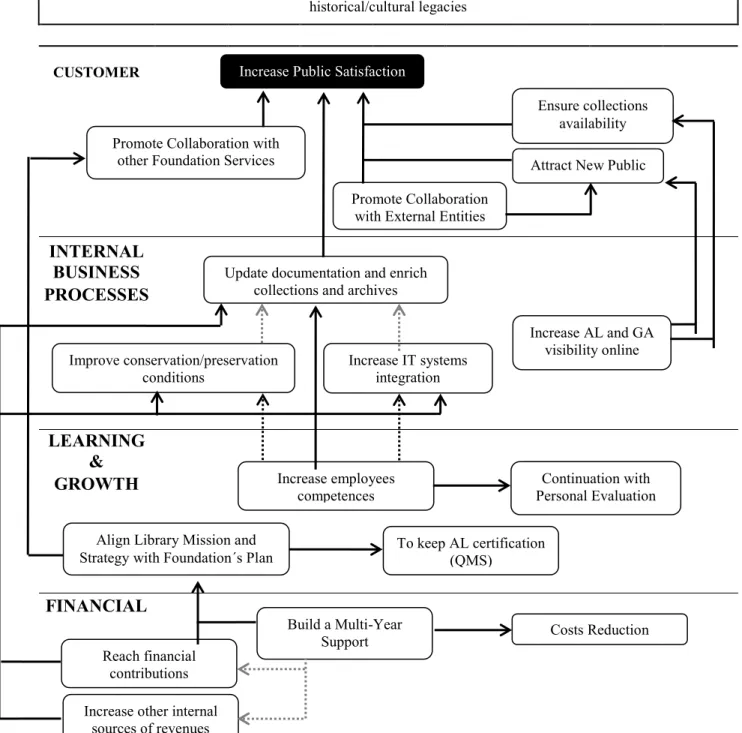

22 These strategic objectives were integrated in strategy maps developed by the researcher, discussed and approved by each service direction, which are shown in the following figures:

Figure I – Art Library Strategy Map

MISSION

Promoting, through the sharing and development of documentary collections and archives, the study and understanding of the Portuguese Visual Arts and Architecture and also the Foundation’s and Founder’s

historical/cultural legacies CUSTOMER INTERNAL BUSINESS PROCESSES LEARNING & GROWTH FINANCIAL

Increase Public Satisfaction

Increase AL and GA visibility online Promote Collaboration with

other Foundation Services

projects Attract New Public

Promote Collaboration with External Entities Update documentation and enrich

collections and archives

Ensure collections availability

Improve conservation/preservation conditions

Align Library Mission and Strategywith Foundation´s Plan

Increase IT systems integration Continuation with Personal Evaluation System Increase employees competences To keep AL certification (QMS) Costs Reduction

Increase other internal sources of revenues

Build a Multi-Year Support Reach financial

23 Figure II – Music Service Strategy Map

MISSION

Promote and qualify the artistic panorama in the field of music, having as reference the highest international standards. This project is realized through musical productions, focused on the activity of the resident artistic groupings: Gulbenkian Orchestra and Choir. In addition, it contributes to audience’s education, with particular attention to communities that have more difficulties on accessing cultural and musical experiences. It also supports vocational music education, the encouragement of musical creation and the dissemination of Portuguese historical-musical heritage. CUSTOMER INTERNAL BUSINESS PROCESSES LEARNING & GROWTH FINANCIAL

Reach more people: Attract disadvantage and young public

Retain Loyal Contributors / Public

Launch Unique and Diverse Repertory Collaboration with

Prestigious Partners

Collaboration with other Foundation Service

Ensure the offering of Musical Services

Accessibility to

new music work Contract/Retain Musical Talent (Launch promotion campaign) Develop Web-based Services

Develop a strategic communication plan Develop employees’

competences

Align Library Mission and Strategywith Foundation’s Plan Implementation of a Personal Evaluation System Reach Financial Contributions Build a Multi-year Support Increase revenues Costs Reduction

24 Figure III – Calouste Gulbenkian Museum Strategy Map

MISSION

Support the study, preservation and promotion of Calouste Sarkis Gulbenkian´s collection and Contemporary and Modern Art while contributing to the cultural enrichment of the public through the presentation of collections, temporary projects and exhibitions, educational activities and editions.

CUSTOMER INTERNAL BUSINESS PROCESSES LEARNING & GROWTH FINANCIAL Internationalization of Portuguese Art Increase visitors satisfaction

Build Reputation for High Standards Present a diverse collection Increase collection quality To educate people

Expose pieces of the collection that are in reserve

Develop a divulgation strategy Develop management systems Develop employees’ competences

Align Museum Mission and Strategywith Foundation’s Plan Implementation of a Personal

Evaluation System

Increase other internal sources of revenues Reach Financial Contributions Costs reduction Increase tickets revenues Collaboration with other

Foundation Service

25 Then, the researcher filtered and clustered the KPIs used on The Foundation´s QMS and on previous years Business Plans. Some of those KPIs were integrated in the BSCs designed, which also enabled the ‘Linking process’ mentioned above. But another concern was the integration of lag and lead indicators that help the measurement of short and long term objectives. The selected KPIs were distributed to everyone in each service, enabling the ‘Communicating and Linking’ process to take place.

Moreover, the three BSCs intended to improve Costumers satisfaction as evidenced by the strategic theme chosen. To measure the execution of the strategic objectives, 25 KPIs were selected for Art Library BSC, Music Service BSC and Museum BSC. The BSCs designed during this WP includes objectives grouped into four perspectives and mapped in chains of cause-and-effect relationships, associated KPIs and targets as well as some other initiatives planed to help achieving some objectives [see appendix VI, VII and VII for Art Library, Music service and Museum BSCs details]. These BSCs enables The Foundation to analyze if strategic objectives are being achieved and making necessary adjustments whenever fells the necessity - feedback and learning process (Kaplan and Norton, 1996; 2008).

VI – Recommendations and main contributions of this WP

Kaplan and Norton (1996) said that even in corporations with several independent SBUs is advantageous to start by developing a BSC at the corporate level because it establishes a common framework, a corporate template, about themes and common visions that must be implemented in the scorecards developed at the individual SBUs. Since the Foundation is currently under reorganization, it was not possible to develop a BSC at a corporate level and it was set that the purpose of this WP would be to design a BSC for three different services.

26 In order to overcome the drawbacks of not being able to design a BSC at a corporate level, the researcher tried to identify the strengths of each SBU and to extend them to the remaining services. For instance, after identifying that the Library Service has a employees’ personal evaluation implemented, it was suggested to extend it to the Museum’s and the Music Service’s BSC. Additionally, as already in place at the Music Service webpage, it was recommended to the Museum management team the development of online selling tickets.

Despite having been able to establish some common visions and strategic objectives, the researcher points out that the Top Management Team should be involved on BSC implementation process at a corporate level. A corporate scorecard establishes how a corporation adds value beyond the value created by the individual SBUs operating as independent units (Kaplan and Norton, 1996). Therefore and as already mentioned, this assignment should be used as a pilot project and extended to all Foundation’s services.

Concluding, this WP drew attention to the fact that up to the present, the Foundation’s services strategic objectives were purely operational. And although the costumer mindedness was present, it wasn’t expressed in concrete objectives. So, this WP allowed the creation of a more ‘balanced’ view to the services under study and enriched the Foundation’s strategic management systems.

VII – List of references

Andersen, H. V. and Lawrie, G. J. G. 2002. "Examining Opportunities for Improving Public Sector Governance Through Better Strategic Management". Proceedings of Performance Measurement Association Conference, Boston

Battilana, J., M. Lee, J. Walker and C. Dorsey. 2012, In Search of the Hybrid Ideal. Stanford Social Innovation Review, 51-55.

Battilana, J. and M. Lee. 2014. Advancing research on hybrid organizing – insights from the study of social enterprises. Academy of Management Annals, 8: 397-441

27 Bourguignon, A., V. Malleret and H. Nørreklit. 2004. The american Balanced Scorecard versus the french Tableau de Bord: the ideological dimension, Management Accounting Research 15: 107-134.

Bradsen, T. and Karré, P.M. 2011, Hybrid Organizations: No Cause for Concern?, International Journal of Public Administration, 34 (13): 827-836

Carroll, A. 1979. A three dimensional model of corporate per-formance. Academy of Management Review, 4: 497-505.

Drucker, P. 1990. “Non-Profits: The Second Career”. In Managing the Non-Profit Organization: Practices and Principles, 204-217. HarperCollins

Evers, A. and Laville, JL. 2004. “Social services by social enterprises: On the possible contributions of hybrid organizations and a civil society.” In The Third Sector in Europe, Edward 237-256. Elgar Publishing,

Haveman, H.A., and Rao H. 2006.”Hybrid forms and the evolution of thrifts”. In American Behavioral Scientist, 49(7): 974-986.

Jansson, E. 2005. “The Stakeholder Model: The influence of the Ownership and Governance Structure”, Journal of Business Ethics, 56(1): 1-13

Jay, J. 2013. “Navigating paradox as a mechanism of change and innovation in hybrid organizations.” Academy of Management Journal, 56(1): 137–159

Jönsson, S. and Lukka K. 2005. “Doing Interventionist Research”. Management Accounting. 6, Gothenburg Research Institute.

Kanter, R.M. and Summers, D.V.1987. “Doing Well, While Doing Good: Dilemmas of Performance Measurement in Non-Profit Organizations and the Need for a Multi-Constituency Approach.” The Non-Profit Sector: A Research Handbook. W. W. Powell. Yale, Yale University Press

Kaplan, R. S. and D. P. Norton.1992. The Balanced Scorecard: measures that drive performance, Harvard Business Review 70(1), 71-79.

Kaplan, R. S. and D.P. Norton. 1996. The Balanced Scorecard: Translating Strategy into action. Boston: Harvard Business School Press.

Kaplan, R. S. and D. P. Norton. 2001. The Strategy-Focused Organization: how balanced scorecard companies thrive in the new business environment. Boston, MA: Harvard Business School Press.

Kaplan, R. S. and D. P. Norton. 2001. “Transforming the Balanced Scorecard from performance measurement to strategic management: Part I”, Accounting Horizons 15(1): 87-104.

28 Kaplan, R. S. and D. P. Norton. 2004. Strategy maps: converting intangible assets into tangible outcomes. Boston, MA: Harvard Business School Press.

Kaplan, R. S. and D. P. Norton. 2006. Alignment: Using the Balanced Scorecard to Create Corporate Synergies. Boston, MA: Harvard Business School Press.

Kasurinen, T. 2002. “Exploring management accounting change: the case of Balanced Scorecard implementation”. Management Accounting Research 13: 323-343.

Kong, E. 2010. “Analysing BSC and IC's usefulness in non-profit organisations.” Journal of Intellectual Capital, 11(3): 284-304

McWilliams, A., and Siegel, D. 2000. “Corporate social responsibil- ity and financial performance: Correlation or misspecification?” Strategic Management Journal, 21: 603-609. Mohobbot, A. 2004. The Balanced Scorecard (BSC) – A critical analysis. Journal of humanities and social. Volume 18. November 2004. Pp 219 -232.

Moizer, J. and Tracey, P. 2010. “Strategy making in social enterprise: The role of resource allocation and its effects on organizational sustainability.” Systems Research and Behavioural Science, 27 (3): 252-266.

Nørreklit, H. 2000. “The balance on the Balanced Scorecard – a critical analysis of some of its assumptions” Management Accounting Research 11(1): 65-88.

Nørreklit, H. 2003. The Balanced Scorecard: what is the score? A hetorical analysis of the Balanced Scorecard, Accounting, Organizations and Society 28(6): 591-619.

Pache, A.-C., and Santos, F. 2012. “Inside the hybrid organization: Selective coupling as a response to conflicting institutional logics.” Academy of Management Journal, 56(4): 972–100 Rababa’h A. 2014. “The case of Balanced Scorecard Implementation within Jordanian Manufacturing Companies.” International Review of Management and business Research 3(1): 174-181

Ryan, B., Scapens, R. W. and Theobald, M. 2002. Research Method & Methodology in Finance and Accounting, 2nd edition, Thomson.

Sabeti, Heerad. 2011. “The For-Benefit Enterprise.” Harvard Business Review

Salamon, Lester and Helmut K. Anheier. 1996. Defining The Nonprofit Sector: A Cross-National Analysis Manchester: Manchester University Press

Sales, X. 2013. “Entrepreneurs And The 'Hybrid' Organization”, Forbes

Suomala, Petri, Jouni Lyly-Yrjänäinen and Kari Lukka. 2014. "Battlefield around interventions: A reflective analysis of conducting interventionist research in management accounting." Management Accounting Research, 25 (4): 304-314.