FUNDAÇÃO

GETUliO VARGAS

FGV

SEMINÁRIOS DE PESQUISA

ECONÔMICA DA EPGE

A general test for rule of Thumb behavior

JOÃO VICTOR ISSLER

(EPGE/FGV)

Data: 17/05/2007 (Quinta-feira)

Horário: 16h

Local:

Praia de Botafogo, 190- 11° andar Auditório n° 1

Coordenação:

A General Test for Rule-of-Thumb Behavior

Fabio A. Reis Gomes (CEPE-MG and IBMEC-MG)

João Victor lssler (EPGE- Getulio Vargas Foundation)

• Consumption is about 70% of GDP. Because of its the size, finding sub-optimal behavior in consumption decisions can cast a serious doubt on whether optimizing behavior is a framework applicable on an economy-wide scale, which, in turn, can challenge whether it is applicable at ali.

• Rule-of-Thumb behavior questions optimal behavior for consumption. Camp-bell and Mankiw(1989, 1990): 50% of ali U.S. consumers follow the rule-of-thumb behavior of consuming their current income, not their permanent

• In econometric tests, usually we have auxiliary assumptions whenever a specific hypothesis test is being conducted. In Campbell and Mankiw's case, the auxiliary assumption is the validity of the first-order log-linearized version of the Euler Equation for optimizing consumers. Rejecting the nu li that there is no rule-of-thumb behavior in this context may be due to the fact that the first-order log-linearized approximation of the Euler Equation

This Paper:

セ@ We first show that, from a theoretical point-of-view, previous tests for Rule-of-Thumb behavior were inconsistent. This is based on an expansion of the basic non-linear euler equation for consumption.

セ@ We then propose a novel framework that encampasses:

Possible Rule-of-Thumb behavior in consumption for a fixed proportion

À of the population. General test for À = O.

Possible habit formation for agents whose behavior is optimal.

This Paper (Contd.):

Motivation

e Huge discrepancy between time-series versus panel-data empirical studies in the consumption literature, suggesting the existence of aggregation bias.

e Mulligan(2002) uses a linear framework to study the effects of real return aggregation on intertemporal substitution. He comes up with new mea-sures for the after-tax return to aggregate capital, which are associated with reasonable and precise estimates of the intertemporal marginal rate of substitution in consumption.

M otivation ( Contd.)

Related Research

e Large early literature using time-series data on consumption: Ha11(1978, 1988), Flavin(1981, 1993), Mankiw(1981), Hansen and Singleton(1982, 1983, 1984), Mehra and Prescott(1985), Campbell (1987), Campbell and Deaton(1989), and Epstein and Zin(1991).

e Whole literature on Rule-of-Thumb behavior following H ali and Mishkin(1982) and subsequent work in Campbell and Mankiw (1989, 1990).

Related Research ( Contd.)

Theory

Pricing Equation:

lEt { Mt+lxi,t+l}

=

Pi,t' i=

1, 2, ... , N, or (1)IEt { Mt+lRi,t+l} = 1, i = 1, 2, ... , N, (2) where IEt( ·) denotes the conditional expectation given the information available at time t, Mt is the stochastic discount factor, Pi t denotes the price of the

'

i-th asset at time t, xi t+l denotes the payoff of the i-th asset in t

+

1,Ri,t+l

=

クセエKャ@

denotes 'the gross return of the i-th asset int

+

1, and N is the numberセヲ@

assets in the economy.Assumption 1: The Pricing Equation (2) holds.

• Assumption 1 is present, either implicitly or explicitly, in virtually ali stud-ies in macroeconomics dealing with asset pricing and intertemporal sub-stitution; see, e.g., Hansen and Singleton (1982, 1983, 1984), Mehra and

Prescott (1985), Epstein and Zin (1991), Attanasio and Browning (1995), Lettau and Ludvigson (2001) and Mulligan (2002).

• "Assumption" 2 is required because we will take logs of Mt. Ali CCAPM studies implicitly assume Mt >O, since Mt =

ヲSオセHH」エIL@

>O, where ct isCt-1

consumption, {3 E (0, 1) and U1

Taylor expansion around x, with increment h, as follows:

h2ex+À(h)·h

ex+ hex

+

,

with .\(h) :IR-+ (0,1),

or, (3) 2ex+h

e h

1+h+

h2eÀ(h)·h-

'

(4)

Let h= ln(MtRi,t) to obtain:

[ln(MtRi

t)]

2 eÀ(In(MtRi,t))·ln(MtRi,t)MtRi,t

= 1+

ln(MtRi,t)

+

'

2 . (5)

The behavior of

MtRi t

,

is governed solely by that ofln(MtRi t).

' which moti-vates our next assumption.Assumption 3: Let

Rt

= (R1 t, R2 t,...

RN t)'

be an N x 1 vectorstack-' ' '

Higher-order term in (5):

z·

2,t

_.

2 l x [ln(M .t 2,t

R· )] 2 e,\(ln(MtRi,t))·ln(MtRi,t).Taking the conditional expectation of both sides of (5), imposing the Pricing Equation and rearranging terms, gives:

IEt-1 {

MtRi,t}

IEt-1 (

Zi,t)

1

+

IEt-1 {ln(MtRi,t)}

+

IEt-1 (zi,t)

,

or,-IEt-1

{ln(MtRi,t)}.

(6)

(7)

Equation (7) shows that behavior of the conditional expectation of the higher order terms depends only on that of IEt-1

{ln(MtRi,t)

}.

Sinceln(MtRi,t)

is covariance stationary, IEt-1 (

Zi,t)

will be a linear function of the laggedz· 2, t 2

1

X [ln(M t 2,t R· )] 2 e,\(ln(MtRi,t))·ln(MtRi,t)>

_O

1 implies 1Et-1 ( Zi,t) 'Yi,t 2

>

O.2- ( 2 2 2 )' - ( )'

Let '"'ft

=

'Y1,t, 'Y2,t , ... , "YN,t and ct=

E1,t, c2,t, ... , EN,t stack respec-tively the conditional means 'Y'i-t and the forecast errors Ei t = ln(MtRit)-(J' ' '

Et-1 {ln(MtRi,t) }.

From the definition of E:t and (6) we have:

Denoting

rt

= In(Rt),

with elements ri,t· and mt = In (Mt) in (8), and usingIEt-1 ( zi,t) = -IEt-1 { ln(MtRi,t) }we get:

mt = -ri,t - IEt-1 ( Zi,t)

+

Ei,t, i = 1, 2, ... , N.(9)

To connect this results with optimal consumption behavior we impose Mt =

{3

r

NZセイアャ@

.

.ó.ln (

ct)

= In,B

+_!_r.+

IE!t-1 ( Zi,t) Ei,t• lEt-lJzi,t) captures the effect of the higher-order terms of the taylor

expan-sion. lt will be a function of the variables in the conditioning set used by the econometrician to compute

IEt-1 (-).

• Omission of

QeエMャセコゥLエI@

in estimating (10) will generate an omitted-variable bias. The same is true of transformations of (10), in general.• lf {

Mt+lRi,t+l}

is not log-Normal, using log-normality to solve forRule of Thumb Behavior

セ@ Campbell and Mankiw (1989), following Hall and Mishkin(1982), proposed incorporating rule of thumb behavior to the optimizing model.

セ@ Credit constrained consumers (Cushing, 1992) consume their current in-come, q t

=

Yl t=

Àyt, where Yt is aggregate income.' '

セ@ À is the fraction of the total income which belongs to restricted consumers.

When À

=

1 there are only rule of thumb consumers and when À=

O ali consumers follow optimizing behavior.セ@

Use weight À to compute llln (ct)

rv Àllln ( C!,t)+

(1 - À) llln ( C2,t) rwhere

ct

=

q t+

c2 t• and Yt=

Yl t+

Y2 t·Rule of Thumb Behavior (Contd.)

Combine now

f),. I n ( c2,

t)

T

In (3+

1 IEt-1(zi,t)

E:i,t

4

/i,t

+

c/J --;j;'

i= 1, 2, ... , N, with,I::!,. In (

ct)

r-v .\I::!,. In (C!,t)+

(1-

.\)I::!,. In (c2,t), to get,r-v .Xbs.ln

(Yt)

+

(1 -

.X) I::!,. In ( c2,t)I::!,. In (

Ct)

MM]MH

QセMNx⦅[⦅I@

In (3+

.\I::!,. In(Yt)

+ (

1 - .X)ri t

+ (

1 - .X)IEt-1(zi

t)cjJ cjJ ' cjJ . '

(1-

.X) .-

E:i

t• ali セN@Econometrics

bt..ln

(ct)

MBMMH

QセMN|MGMI@

In ,8+

.\bt..ln(Yt)

+ (

1-.\)ri t

+ (

1 - .\)lEt-1(zi t)

4Y 4Y , 4Y ,

(1- .\)

- 4Y

Ei,t•

a 11 i.• lf the term

H

QセL|IャeエMQ@

(zi,t)

is omitted, (almost?) every instrument used in the past to estimate this equation is invalid.Econometrics ( Contd.)

.ô.ln (

ct)

⦅H

QセM⦅I@

In,6

+

À.Õ.in(Yt)

+ (

1-À)

rit

+ (

1 - À)lEt-1(zi

t)

cp

cp

'

cp

'

(1-

À)

- - é ' t

-

cp

'/,)

I i = 1, 2, ... ,N.

Econometrics ( Contd.)

• Since, in principie, the number of assets can go to infinity, i.e., N --+ oo,

unless T --+ oo at rate N 2 , estimating the whole system is unfeasible.

Most of the literature did not take this issue seriously and opted to let

N = 2: a risky and a "riskless" asset.

• This procedure is suboptimal compared to estimating the system as a whole.

• An alternative to estimating the system as a whole is cross-sectional ag-gregation: Mulligan(2002), where in principie we do not throw away useful

information contained in ri t• i = 1, 2, ... , N.

Stylized Version of Mulligan(2002): Cross-sectionally aggregate

Llln

(ct)

MGMH

QセM⦅I@

In/3

+

Àilln(yt)

+ (

1-À)

Ti t

+ (

1 - À)IEt-1(zi t)

セ@ セ@ ' セ@ '

(1-

À)

.

.

- si t. ali セN@ to obtam,

セ@ '

Llln

(ct)

(1-À)

In/3

+

Àilln(yt)

+ (

1-À)

Tt

+ (

1 - À)IEt-1(zt)

セ@ セ@ セ@

(1 -

À)

セ@ ct,

N

where

Tt

= N1 2:::::Ti t

is the logarithmic return to aggregate capital,zt

. 1 '

2=

1 N 1 N

N . 1 ' 2::::: Zi t. ct = N . 1 ' 2::::: éi t·

• Despite having a properly aggregated model, we have to take into account the term

HャセIャeエMャ@

(zt)-• lgnoring

HャセIャeエMQ@

(zt)

will also generate an omitted regressar problem under IV estimation, just as before. This happens whether or not À=

O.• Mulligan (2002) estimates the above regression imposing À = O.

Habit Formation

Consider now the extended CRRA utility, with habit formation,

U

(C[,

Cf-1)

=(C[

-

f'Ct1) 1-cp

1-cp

(11)

We let (o) stand for an optimizing consumer, and

(r)

stand for a credit-constrained consumer whose consumption isct;

= À.Yt· As before,o+

rct=Ct Ct·

lnstead of considering the response of consumption to ali i = 1, 2, ... , N,

As in Weber(2002), solve for consumption of the optimizing consumer:

o- \

Ct - ct - AYt·

Habit Formation and General Rule-of-Thumb

Use the nonlinear euler equation as in Weber(2002). Use here the return to

aggregate capital. Then we encompass habit formation and rule-of-thumb in a

very general framework, with proper cross-sectional aggregation:

Et-1

( cf-1- 'fCf-2)

-<P-f3

(

cf- 'Ycf-1)

-<Ph+

Rt]+'Jf3

(

cf+1- 'Ycf)

-<P RtSubstituting in

cf

= Ct- ÀYt we obtain:[( ct-1 -

ÀYt-Ü -'Y (

Ct-2 - ÀYt-2)]-<P=

o,

(12)

Et-1

<

-{3 [(ct-

Àyt) -'Y ( ct-1 -

ÀYt-1)]-<Ph+

Rt]t

= O. (13)Obtaining (12) and (13): cross-sectional aggregation of:

E J ( cf-1 - --ycf-2)

-r/J

-

f3

(

cf - --ycf-1)-r/J

[

'"Y+

Ri,t]t-1\ (

)-c/J

+--r/3

cf+1 - --ycf Ri,to

1, 2, ... , N. and,

.

'l

[(ct-1- ÀYt-1)- '"Y (ct-2- ÀYt-2)]-cP

O = Et-1

<

-j3 [(ct- Àyt)- '"Y (ct-1- ÀYt-Ü]-cP[--r+

Ri,t]+--r/3

[(

Ct+1 - ÀYt+1) - '"Y ( ct - Àyt)]-cP Ri,tz = 1,2, ... ,N.

N N

where Rt

=

L

wi t ·Ri t• whereL

wi t=

1, for alit.

. 1 ' ' . 1 '

H a bit Formation and Rule-of-Thumb ( contd.)

e lf there is no habit formation for the optimizing agent, "f = O, we obtain:

f3Et-1

I (

ct

-

ÀYt )-c/J

Ct-1 - ÀYt-1 Rt

I

= 1(14)

e lf there is no rule-of-thumb behavior, but there is habit formation, we obtain:

[ct-1 - "fCt-2]-c/J

Et-1 { -{3

[ct-

"fCt-1]-cP[I+

Rt]

+"tf3 [ct+1 -

"tct]-cP

Rt• lf there is neither rule-of-thumb nor habit formation, we obtain:

(

ct )

-c/J

f3Et-1

I

RtI

= 1.Our Contribution:

e Regarding Weber(2002): we deal with cross-sectional aggregation of asset returns. No information is thrown away by limiting the number of as-sets. lndeed, we use Mulligan's(2002) capital rental rate after income and

property taxes as a measure of Rt.

e Regarding Mulligan(2002): We deal with non-linearity, Rule-of-Thumb, and Habit Formation.

セ@ Cross sectional aggregation is properly taken care of by using the return to

aggregate capital and not a system of euler equations. This can be done beca use the euler equations are LINEAR on

Ri

t, i= 1, 2, ... ,N,

despite'

being non-linear on other variables and parameters.

セ@ The nonlinear equation is key to our study. Estimating it directly allows

us to encompass ali high-order terms: General Rule-of-Thumb test and a General test for Habit Formation.

セ@ The general model is ali in terms of observables. lt encampasses habit for-mation for the optimizing agent, ry

#-

O, as well as rule-of-thumb behavior for the credit-constrained consumer, À#-

O.セ@ Estimation of (3, cjJ and À is performed using GMM. Habit formation and

Data

• Annual frequency form 1947 to 1997.

• US Nationallncome and Product Account (NIPA) and from the US Census Bureau: real disposable personal income, real consumption of nondurable and services and real consumption of non-durables, and population.

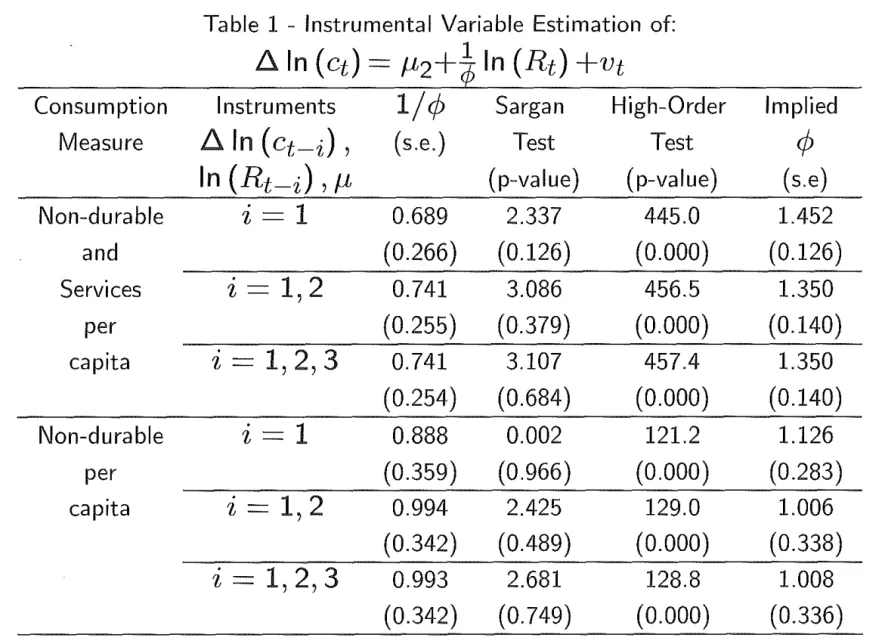

Table 1 - Instrumental Variable Estimation of:

f:::. In (

ct)

=JL2+

à

In (Rt) +vt

Consumption I nstru ments 1/c/J Sargan High-Order lmplied Measure L::::. In (

Ct-i)

,

(s.e.) Test Test cPIn

(Rt-i), JL

(p-value) (p-value) (s.e)Non-durable i= 1 0.689 2.337 445.0 1.452

and (0.266) (0.126) (0.000) (0.126)

Services i -- 1 2 ' 0.741 3.086 456.5 1.350

per (0.255) (0.379) (0.000) (0.140)

capita i = 1, 2, 3 0.741 3.107 457.4 1.350 (0.254) (0.684) (0.000) (0.140)

Non-durable i= 1 0.888 0.002 121.2 1.126

per (0.359) (0.966) (0.000) (0.283)

capita i -- 1 2

'

0.994 2.425 129.0 1.006 (0.342) (0.489) (0.000) (0.338)Table 2 - Instrumental Variable Estimation of:

.ó.ln (

ct)

= À.Ó.In(yt)

+

(1- À)HセQ@

+

à

In(Rt)

+

Vt)

Cons. lnst. (1- À)

/c/J

À Sargan Hi.-Order lmpl.Meas. .ó.ln (ct-i) (s.e.) (s.e.) Test Test cjJ

In

(Rt-i)

(p-val.) (p-val.) (s.e).ó. In

(yt_i) ,

cNon-dur. i=1 0.496 0.199 2.680 104.2 1.616

and (0.322) (0.238) (0.102) (0.000)

Serv. i= 1, 2 0.389 0.300 3.570 151.0 1.799

per (0.264) (0.149) (0.467) (0.000)

capita i = 1, 2, 3 0.322 0.341 7.183 163.3 2.044

(0.255) (0.141) (0.410) (0.000)

Non-dur. i=1 0.667 0.238 0.001 14.90 1.125

per (0.691) (0.635) (0.980) (0.002)

capita i - 1 2 -

'

0.361 0.559 0.955 102.3 1.223(0.374) (0.225) (0.917) (0.000)

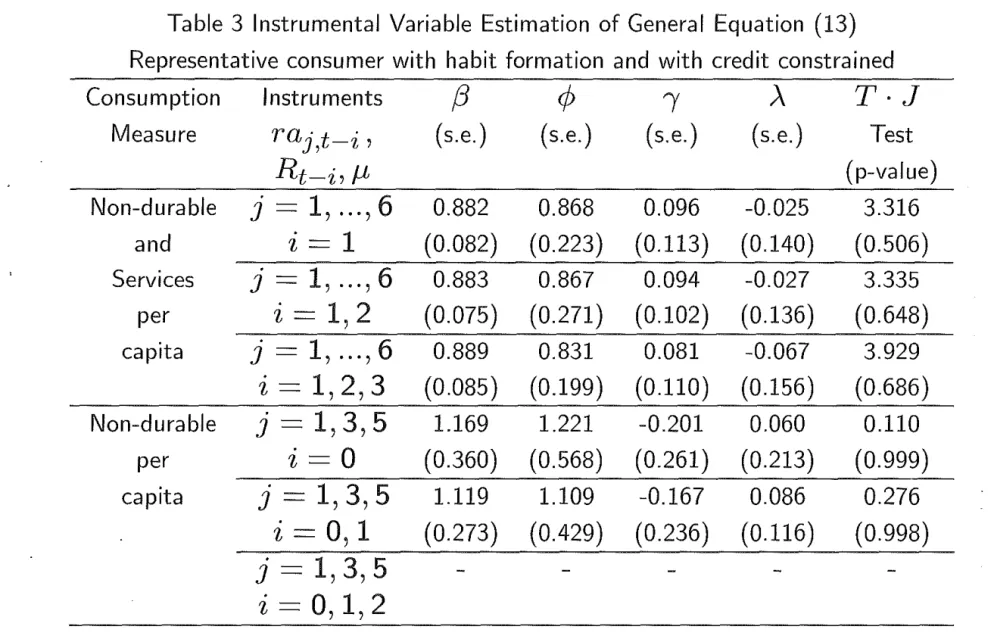

Table 3 Instrumental Variable Estimation of General Equation (13) Representative consumer with habit formation and with credit constrained

Consumption lnstruments j3

q;

"( À T·JMeasure raj,t-i' (s.e.) ( s.e.) (s.e.) (s.e.) Test

Rt-i, f.L (p-value)

Non-durable j=1, ... ,6 0.882 0.868 0.096 -0.025 3.316

and i= 1 (0.082) (0.223) (0.113) (0.140) (0.506)

Services j=1, ... ,6 0.883 0.867 0.094 -0.027 3.335

per i= 1 2

'

(0.075) (0.271) (0.102) (0.136) (0.648)capita j=l, ... ,6 0.889 0.831 0.081 -0.067 3.929

i=1,2,3 (0.085) (0.199) (0.110) (0.156) (0.686)

Non-durable j=1,3,5 1.169 1.221 -0.201 0.060 0.110 per i=O (0.360) (0.568) (0.261) (0.213) (0.999) capita j = 1, 3, 5 1.119 1.109 -0.167 0.086 0.276

i=

o,

1 (0.273) (0.429) (0.236) (0.116) (0.998)j = 1,3,5

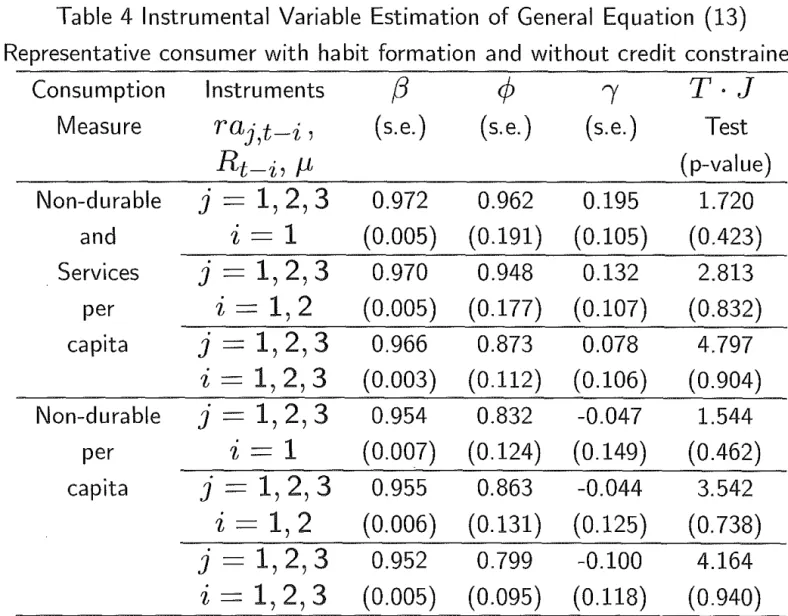

Table 4 Instrumental Variable Estimation of General Equation (13)

Representative consumer with habit formation and without credit constrained

Consumption lnstruments (3

cp

ry T·JMeasure raj,t-i' (s.e.) (s.e.) (s.e.) Test

Rt-i, p, (p-value)

Non-durable j

= 1,2,3

0.972 0.962 0.195 1.720 andi= 1

(0.005) (0.191) (0.105) (0.423) Services j= 1, 2, 3

0.970 0.948 0.132 2.813per

i- 1 2

-'

(0.005) (0.177) (0.107) (0.832) capita j= 1,2,3

0.966 0.873 0.078 4.797i= 1,2,3

(0.003) (0.112) (0.106) (0.904) Non-durable j= 1,2,3

0.954 0.832 -0.047 1.544per

i=1

(0.007) (0.124) (0.149) (0.462) capita j= 1, 2, 3

0.955 0.863 -0.044 3.542i- 1 2

-'

(0.006) (0.131) (0.125) (0.738)j

= 1,2,3

0.952 0.799 -0.100 4.164Table 5 Instrumental Variable Estimation of General Equation (13)

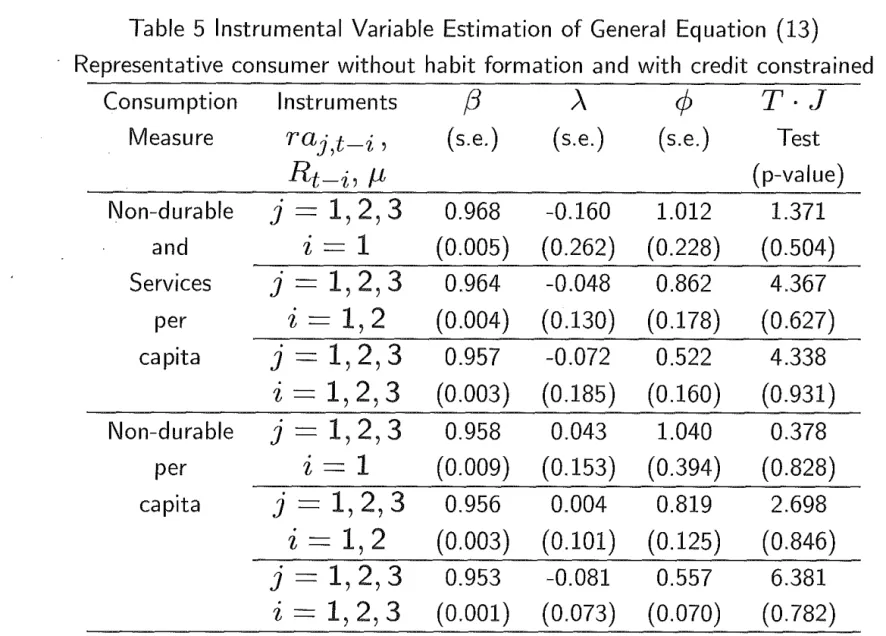

· Representative consumer without habit formation and with credit constrained

Consumption lnstruments fJ À

cp

T·JMeasure raj,t-í' (s.e.) ( s.e.) (s.e.) Test

Rt-í, fL (p-value)

Non-durable j = 1,2,3 0.968 -0.160 1.012 1.371

and i= 1 (0.005) (0.262) (0.228) (0.504)

Services j = 1,2,3 0.964 -0.048 0.862 4.367

per i - 1 2 -

'

(0.004) (0.130) (0.178) (0.627)capita j=1,2,3 0.957 -0.072 0.522 4.338

i=1,2,3 (0.003) (0.185) (0.160) (0.931)

Non-durable

j

= 1,2,3 0.958 0.043 1.040 0.378 per i=1 (0.009) (0.153) (0.394) (0.828) capitaj

= 1,2,3 0.956 0.004 0.819 2.698i -- 1 2

'

(0.003) (0.101) (0.125) (0.846)j

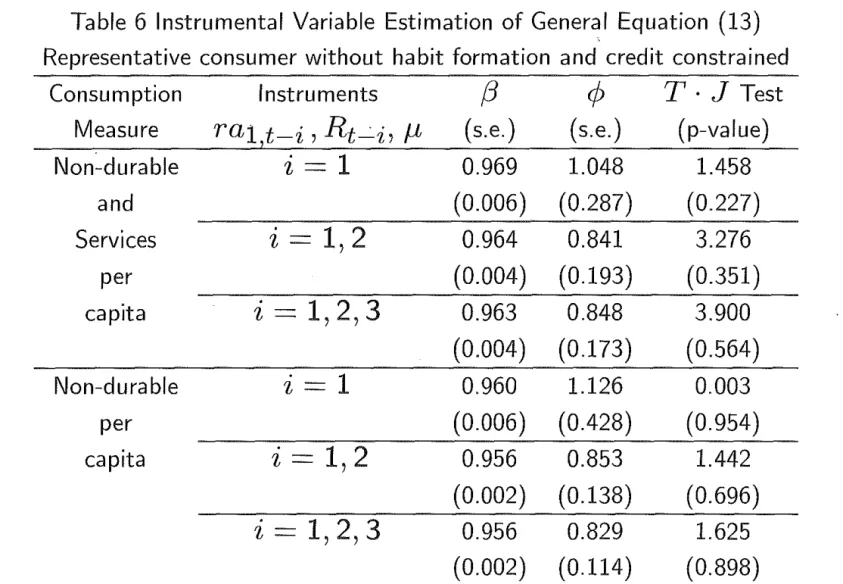

= 1,2,3 0.953 -0.081 0.557 6.381Table 6 Instrumental Variable Estimation of General Equation (13) Representative consumer without habit formation and credit constrained

Consumption lnstruments (3

cP

T · J Test Measure ra1 t-i , Rt__:_i, /L (s.e.) (s.e.) (p-value)Non-durable i= 1 0.969 1.048 1.458

and (0.006) (0.287) (0.227)

Services i= 1, 2 0.964 0.841 3.276

per (0.004) (0.193) (0.351)

capita i=1,2,3 0.963 0.848 3.900

(0.004) (0.173) (0.564)

Non-durable i= 1 0.960 1.126 0.003

per (0.006) (0.428) (0.954)

capita i= 1, 2 0.956 0.853 1.442

(0.002) (0.138) (0.696)

i=1,2,3 0.956 0.829 1.625

llllllllllllllllllll/1 11111

(BIBLIODATA)BB002936753

f I