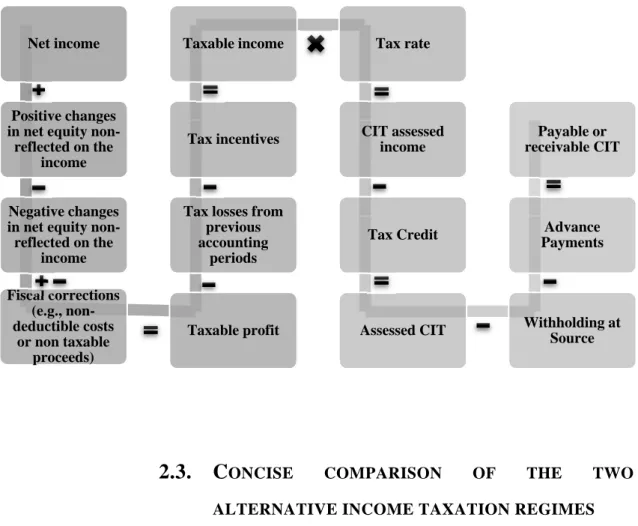

Earnings management as a determinant of choice between alternative income taxation regimes of small Portuguese companies

Texto

Imagem

Documentos relacionados

Além desta introdução, o artigo apresenta-se em quatro partes: a revisão da literatura sobre policy transfer; as transferências de políticas públicas brasileiras no campo da

Acrescentem-se as contribuições de Isla e Pesa (2003): a ausência dessa discussão pode levar à não discriminação entre o modelo e a realidade por ele representada, ao

Aumenta a expressão de genes supressores tumorais (galectina-1, metalotioneína- 1X e proibitina-2), de proteínas que ativam a apoptose (complexos de transporte da cadeia

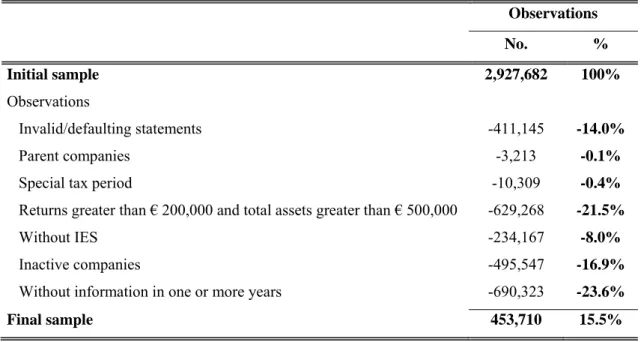

[r]

Negative impact of total expenditure on growth. Positive impact of direct taxation, indirect taxation and public investment. Negative effect of government consumption, transfers,

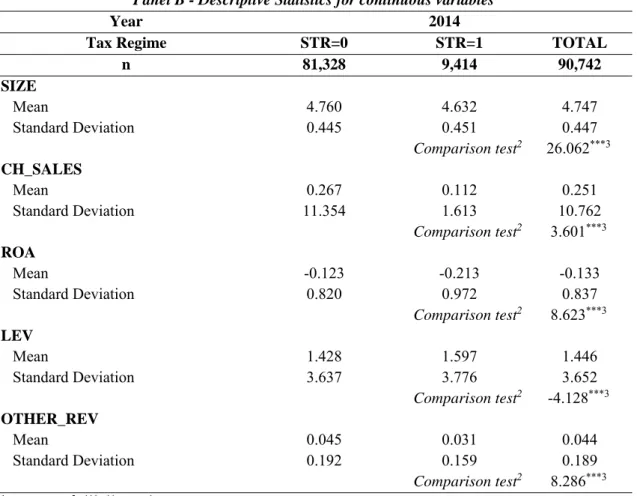

assets, size of companies, loss ratio (risk), premium growth, age of companies, and the.. management

It intends to perceive the reality of the Cape Verdeans’ organizations regarding the employees ‘perceptions about their leaders’ authenticity and how these perceptions influence