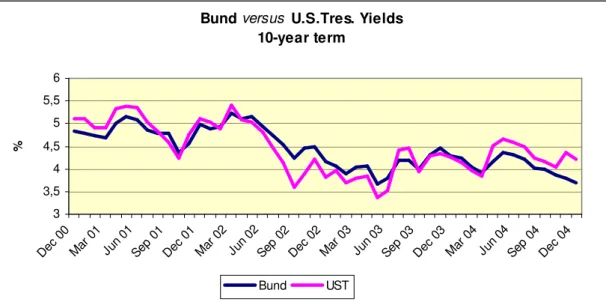

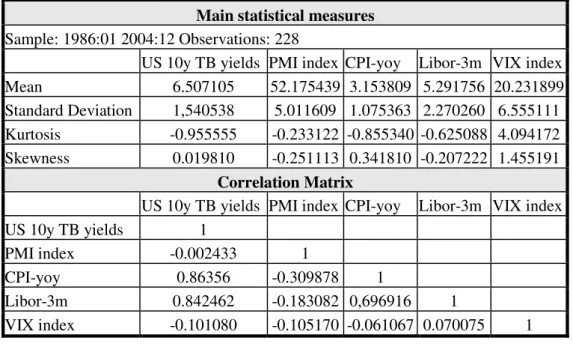

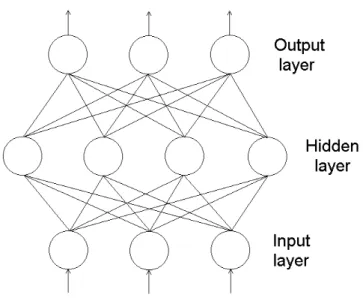

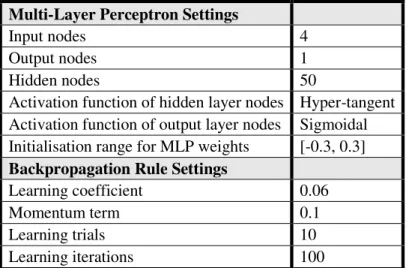

FORECASTING LONG-TERM GOVERNMENT BOND YIELDS: AN APPLICATION OF STATISTICAL AND AI MODELS

Texto

Imagem

Documentos relacionados

Results based on the Common Correlated Effect estimator of Pesaran (2006) and on Panel Error Correction Models to sort out short- and long-run fiscal developments show that

I use a panel of semi-annual vintages of growth and fiscal forecasts of the European Commission, covering the period 1998:II-2008:II, to assess its effects on 10-year

Study Year Report 13, University of Warwick. Linear Bayesian methods. Royal Statistical Soe. The Econometric Analysis of Time Series. unified view of statistical

Na prática, um dos cônjuges não poderá pedir a certidão de divórcio em um cartório, caso a decisão não seja consensual., pois diante do entendimento do CNJ,

A aquisição originária da nacionalidade, e o consequente gozo e exercício de direitos que delineiam a cidadania são regulados na Consti- tuição Imperial e na

A metodologia proposta inova nos seguintes aspectos: (i) integra uma ferramenta clássica da área de produção, CA, a uma técnica consolidada para a identificação

A par com este estudo foram delineados alguns objetivos primordiais expectando-se o seu cumprimento, tais como demonstrar que as revistas temáticas cons- tituem uma fonte

Statistical regression models allow us to model predictor variables of treatment stability and offer the next patient a more individualized. Johnston