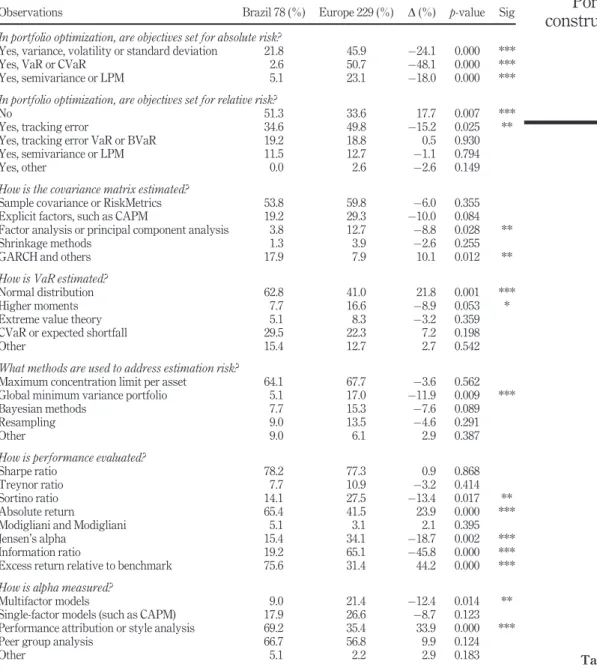

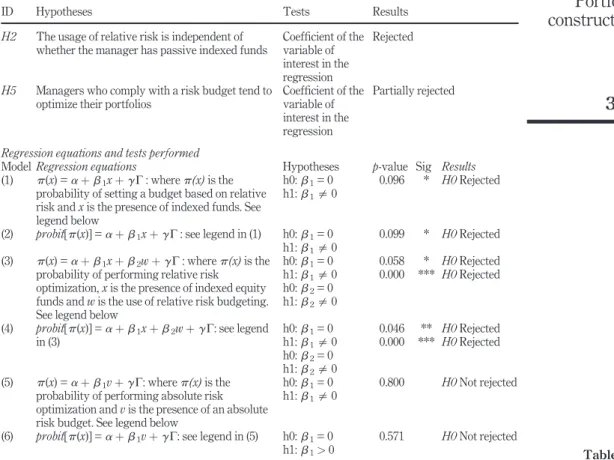

Portfolio construction and risk management: theory versus practice

Texto

Imagem

Documentos relacionados

Endoscopic Surgery of the Lateral Nasal Wall, Paranasal Sinuses and Anterior Skull Base. Endoscopic Surgery of the Lateral Nasal Wall, Paranasal Sinuses and Anterior

Ao utilizar-se um teste destinado a amostras de medicina humana, e devido à ausência de reacções cruzadas entre a proteína C reactiva humana e canina, os valores

The six families with the greatest numbers of species constitute 75 per cent of the species we model, and for them we predict increases from 20 per cent (Euphorbiaceae; range 16 –

Entre as décadas de 1980 e 2010 os programas de monitoria restringem-se apenas as universidades e elas os regulamentam baseadas em parâmetros baseados em seus

20 This pilot study of macroalgae as a substrate for invertebrates, present within IMTA’s earthen pond, where 7678 individuals were sampled, with an average density of

For the liquid oral medicines, by the presence of reducing sugars, the per cent of glucose was determined in the sample solution before acid inversion, and the per cent su- crose

- Capítulo 4: Diagnóstico Ambiental – Descrição do diagnóstico por domínio ambiental, considerando os aspectos relevantes da actividade associada a

Homero, o poeta: filho de Meles, o rio de Esmirna, e da ninfa Creteida, segundo Castrício de Niceia ou, segundo outros, de Apolo e da Musa Calíope, ou como diz o historiador Cárax,