WORKING PAPER SERIES

CEEAplA WP No. 03/2008

Evaluating a Mobile Telecommunications Merger

in Portugal

Corrado Andini Ricardo Cabral

Evaluating a Mobile Telecommunications Merger

in Portugal

Corrado Andini

Universidade da Madeira (DGE)

e CEEAplA

Ricardo Cabral

Universidade da Madeira (DGE)

e CEEAplA

Working Paper n.º 03/2008

Março de 2008

CEEAplA Working Paper n.º 03/2008 Março de 2008

RESUMO/ABSTRACT

Evaluating a Mobile Telecommunications Merger in Portugal

This paper evaluates the impact of the proposed Optimus-TMN mobile telecommunications merger in Portugal. The results suggest that, if the merger would have taken place, the average market profit margin would have increased by 11.6 percentage points and the average market price would have increased by 3.8%. As a consequence, the average marginal cost would have decreased by 14.9%, and welfare would have increased by €163.3mn per year, a gain entirely captured by the producers. Moreover, the merger would have resulted in a large transfer of surplus from consumers to producers, to the tune of €99.5mn per year. The conclusion is that, while the merger could have been authorized on efficiency grounds, such authorization should have been accompanied by strict retail price-cap merger remedies.

JEL classification: L11, L13, L40, L96

Keywords: telecommunications, merger policy, duopoly

Corrado Andini

Departamento de Gestão e Economia Universidade da Madeira

Edifício da Penteada Caminho da Penteada 9000 - 390 Funchal

Ricardo Cabral

Departamento de Gestão e Economia Universidade da Madeira

Edifício da Penteada Caminho da Penteada 9000 - 390 Funchal

Evaluating a mobile telecommunications merger in Portugal

Corrado Andini Ricardo Cabral

Universidade da Madeira, CEEAplA & IZA Universidade da Madeira & CEEAplA

ABSTRACT

This paper evaluates the impact of the proposed Optimus-TMN mobile telecommunications merger in Portugal. The results suggest that, if the merger would have taken place, the average market profit margin would have increased by 11.6 percentage points and the average market price would have increased by 3.8%. As a consequence, the average marginal cost would have decreased by 14.9%, and welfare would have increased by €163.3mn per year, a gain entirely captured by the producers. Moreover, the merger would have resulted in a large transfer of surplus from consumers to producers, to the tune of €99.5mn per year. The conclusion is that, while the merger could have been authorized on efficiency grounds, such authorization should have been accompanied by strict retail price-cap merger remedies.

JEL classification: L11, L13, L40, L96

Keywords: telecommunications, merger policy, duopoly

Correspondence address

Ricardo Cabral, Universidade da Madeira, Campus Universitário da Penteada, 9000-390 Funchal, Portugal. Email: [email protected]

Acknowledgements

For valuable comments and suggestions, the authors are indebted to José Amado da Silva, Henry Chappell, Michal Grajek, Paulo Guimarães, Steffen Hoernig, the participants at the 1st ICP-ANACOM Seminar and the participants at the L1 session of the 1st Annual Meeting of the Portuguese Economic Journal. Funding from ICP-ANACOM is gratefully acknowledged. The usual disclaimer applies.

1. Introduction

Since 2001 the mobile telecommunications industry has been experiencing firm exit and growing consolidation. For example, Telefónica and Sonera exited the German market in 2002 after having invested €8.6bn in UMTS licenses. Likewise, OniWay exited the Portuguese market in 2002 after having spent €100mn in licenses. Further, in 2005, France’s Orange acquired Spain’s Amena in a cross-border merger, whereas T-Mobile acquired Tele.ring in a within-border merger in Austria. In the latter instance, the number of operators in Austria fell from 5 to 4 and the Herfindahl-Hirschman Index (HHI) rose from 2880 to 3430, based on pre-merger market shares. Moreover, in the United States, two mergers in 2004 (Verizon acquired AT&T) and 2005 (Sprint acquired Nextel) reduced the number of operators with national coverage from 6 to 4. According to Cooper (2004), the U.S. CR6 increased from 55% in 1997 to 85% in 2004, and Fox (2005) argued that the U.S. mobile telecommunications industry was more concentrated in 2005 (HHI of 6000 based on radio-spectrum licenses) than in 1998, when the industry was characterized by a duopoly.

From the outset of the mobile telecommunications, regulators promoted competition as a means to improve industry performance. The rapid industry growth experienced in the 1990s and early 2000s, in a sense, vindicated the regulatory approach and resulted in a growing preference for allowing market forces to determine outcomes and in a less prominent role for regulation in the sector, particularly regarding the retail market. On the one hand, the regulators attempted to create conditions that facilitated new entry, namely through wholesale market regulation, and, on the other hand, they accepted reductions in the number of competitors with minimal remedies.

In this context, the December 2006 decision of the Portuguese Competition Authority (Autoridade da Concorrência, 2006) to authorize a merger between two mobile operators, Optimus and TMN, which would have resulted in a market duopoly, was but an additional

step in the recent international trend towards further industry consolidation.

The merger proposal was considered hostile by the targeted group, Portugal Telecom (PT), owner of TMN. However, after a particularly bitter, one-year long merger process, the PT shareholders rejected a motion to change the bylaws regarding voting restrictions and, as a result, the merger failed.

Nonetheless, the Competition Authority decision raises at least three important issues from an economic perspective, which we seek to explore in this paper, by focusing on the impact the merger would have had on the Portuguese mobile-voice communications market.1 First, we try to evaluate the effects of the authorized merger on consumer’s surplus and deadweight welfare loss. Second, we attempt to quantify the effect of the merger on industry efficiency, industry surplus, and social welfare. Finally, based on the analysis of the two above issues, we elaborate on whether the Competition Authority decision was warranted.

To do so, we use a two-part methodology with some similarities to that of Stewart and Kim (1993).2 First, we estimate the effect of increasing market concentration on prices and price-cost margins, using the empirical approach of the Structure-Conduct-Performance Paradigm (SCPP) and an international dataset of mobile operators with roughly 1700 observations. The results of the estimation are used to predict the post-merger average industry price and marginal cost if the merger had indeed occurred. In the second part, we use both an isoelastic demand specification and estimates of the price elasticity of demand for mobile-voice calls in Portugal by Pereira and Ribeiro (2007), in order to infer what would have been the change in the industry output associated with the change in the average market price. Finally, using the data determined in the prior steps, and assuming no income effects and no shift of the demand curve, we calculate the Marshallian consumer’s surplus change, the deadweight welfare loss, the producer surplus change, and the overall welfare effect of the merger.

Our results suggest that the merger would have increased both industry efficiency and industry market power, i.e., growing industry consolidation would have resulted, in the long-term, in lower average marginal costs but also in higher average equilibrium price. Worryingly, the consumer-surplus loss, a consequence of the higher average price, constitutes more than one third of the estimated producer surplus change and nearly two thirds of the overall welfare improvement.

2. Merger impact on industry price and price-cost margin

The aim of the econometric analysis of this section is to obtain an estimate of the impact the merger would have had on average price and price-cost margin. In order to do so, we use two SCPP-type reduced-form models that establish the relationship between firm market share and firm price and price-cost margin:

(1) lnPicyq=α0+α1MSHAREicyq−1+α2CHURNicyq−1+α3MPPicyq+αc +αy+αq+ξicyq (2) EBITDAicyq =β0+β1MSHAREicyq−1+β2CHURNicyq−1+βc+βy+βq +ζicyq

where lnPicyq is the logarithm of the price, measured as the average revenue per minute (ARPM) of the firm i in the country c during the quarter q of the year y; MSHAREicyq−1 is the lagged market share (the ratio of the number of subscribers for the firm i to the total number of subscribers in the country c); CHURNicyq−1 is the lagged churn rate (the percentage of subscribers that cancel their contract in a given quarter), which is thought to be a significant cost factor in the mobile-voice industry; MPPicyq is a dummy variable that controls for countries where the regulatory framework is based on mobile party pays, and voice traffic is defined differently; EBITDAicyq is a proxy for the price-cost margin, defined as earnings

before interest, taxes, depreciation, and amortization divided by total operational revenues; c

α , α , y α , q β , c β and y β are vectors containing country (c), year (y) and quarter effects q

(q); and finally ξicyq and ζicyq are random disturbances.

We include market shares and churn rates with lags in our models because it is reasonable to think that, in practice, firms devise current-period pricing and mark-up plans on the basis of market data from earlier periods.3

Our dataset is extracted from the Merrill Lynch’s (hereafter ML) Global Wireless Matrix 2Q04 report and contains quarterly data on 177 firms across 45 countries, from the first quarter of 1999 to the second quarter of 2004. Summary sample statistics are reported in Appendix.

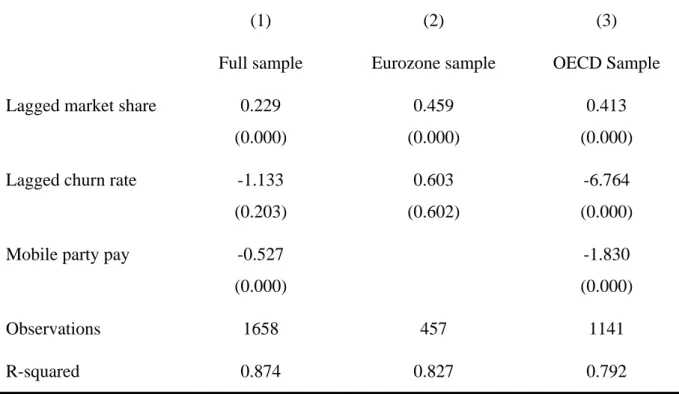

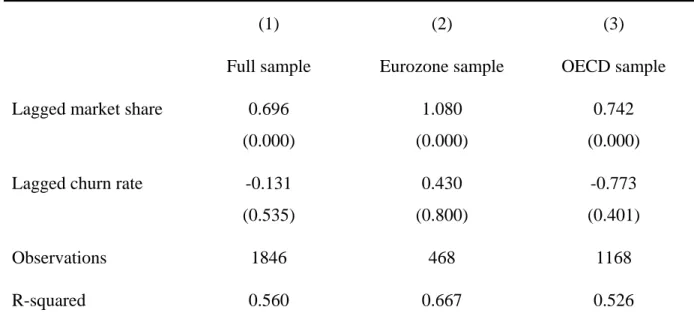

The estimation results, based on ordinary least squares, are presented in Table 1 and 2. To summarize, we find that a one percentage-point increase in the average market share results in a 0.7 percentage-points increase in the average market margin and in a 0.2% increase in the average market price per minute of call (measured as the average of the average revenue per minute of each firm in the market). If we consider the Eurozone sub-sample (or an OECD sub-sub-sample), the effects are even larger. Specifically, a one percentage-point increase in the average market share results in a 1.1 (0.7) percentage-percentage-points increase in the average margin and a 0.5% (0.4%) increase in the average price.4

Our approach is as follows. If the number of firms in the Portuguese market falls from 3 to 2 because of a merger, then the average market share increases by 16.7 percentage points. Multiplying this change by our market-share coefficient estimates obtained from (1) and (2), we obtain an estimate of the expected change in both average price and average margin, respectively, when the average market share increases. In practice, the approach, like prior literature (Salant et al., 1983), compares two static long-run equilibria: the basis scenario of the pre-merger three-firm oligopoly with the duopoly structure that would have resulted, had

the merger been successful. The empirical results suggest that, if the average market share were to increase from 33% to 50%, the average price would have increased by 3.8% and the average margin would have increased by 11.6 percentage points. Moreover, since regression (1) and (2) results suggest that margins and prices increase with market share, it is likely that the firm with a market share larger (smaller) than the average would have higher (lower) prices and margins than the average firm. For comparison, Grzybowski and Pereira (2008), using Portuguese mobile telecommunications data, estimate that the proposed Optimus-TMN merger would have increased the average price by 6 to 7%.

The use of the average in the appraisal of the merger effects is novel, to the best of our knowledge, and is a way of dealing with at least three issues. First, as pointed out by Salant et

al. (1983), Perry and Porter (1985), as well as Farrell and Shapiro (1990), following a merger, the merged parties reduce the output, while the parties that are external to the merger increase the output, even when the resulting oligopoly is strongly asymmetric. Thus, the combined pre-merger market share is not a good predictor for the post-merger market share of the merging firms. Likewise, the post-merger market share of the non-merging firms is likely to increase. Hence, estimating the impact of the merger on prices, margins, and welfare using pre-merger market shares is inappropriate.

Second, data on output by operator are neither public nor available to us. Nevertheless, by using total industry output in combination with average prices and margins, it is possible to obtain estimates of the merger impact on welfare, consumer, and producer surplus (see Section 3 below). Specifically, the industry’s output and average price can be derived from the average firm’s output and price.

Finally, since the proposed merger would have resulted in a duopoly with an above-average and a below-above-average firm, it is still possible to make general inferences on the performance (prices and margins) of these firms relative to a hypothetical average firm.

On the other hand, we are aware that the average conveys little information about the performance of each firm, nor does it indicate how the estimated producer surplus is going to be split in the resulting duopoly.

3. Merger impact on industry output

To infer the output variation consistent with the change in the average price, we use an isoelastic demand curve and estimates of the price elasticity of demand for minutes of mobile telephony calls in Portugal due to Pereira and Ribeiro (2007).

Specifically, we assume that the demand curve is given by:

(3) Q= AP−ε

where A is a demand shifter, Q is the industry output measured as minutes of voice traffic, P is the average price per minute of voice call, and ε is the price elasticity of demand.

Pereira and Ribeiro (2007) estimate the own-price elasticity of demand for TMN, Vodafone, and Optimus, at 1.3, 2.2, and 3.3, respectively. Thus, we use the non-weighted average of Pereira and Ribeiro’s own-price elasticities of demand, 2.3, as our measure of the Portuguese market’s price elasticity of demand ε. Section 5 discusses the sensitivity of our welfare analysis (Section 4) to changes in the price elasticity of demand.

We solve equation (3) to determine the parameter A for Portugal, using 2004 pre-merger industry data on output and price. Note that we resort to 2004 data as they are the latest data available in our dataset. Particularly, first half of 2004 price data from the ML dataset indicate that the average (non-weighted) nominal average price per minute (P) in Portugal is €0.197 per minute. The total industry output (Q) in 2004 is 14487 million minutes, according to the Portuguese Telecommunications Regulator, ICP-ANACOM (2005a).5

Therefore, we evaluate the pre-merger parameter A at 345.3=11487

(

0.197)

2.3.In order to estimate the change in the industry output associated with the change in average price, we assume, like prior theoretical and empirical literature (Salant et al., 1983; Farrell and Shapiro, 1990; Levin, 1990; Stewart and Kim, 1993), that the demand curve does not shift as a result of the merger, i.e., the parameter A does not change because of the merger.

As argued in the previous Section, the average market price would have risen by 3.8% to €0.205 per minute. Therefore, equation (3) suggests that the total industry output would have diminished by 8.2% (or 1191 million minutes) to 13296 million minutes. This is roughly 119 fewer minutes per subscriber per year.

4. Merger welfare analysis

The estimation of consumer’s surplus and welfare changes has been an important tool in guiding merger analysis in the last decades (Harberger, 1971; Willig, 1976; Motta, 2004; Brito and Catalão-Lopes, 2006), despite criticisms about the concept of consumer’s surplus (Harberger, 1971; Hausman, 1981).

Generally, mergers are regarded as detrimental to society if they result in large deadweight welfare losses or alternatively in large transfers of consumer’s surplus to producers. They are regarded as beneficial, if they result in large producer efficiency gains with limited impact on prices, and thus on consumer’s surplus. In this section, we use the results of the prior two sections to infer the impact of the merger on consumer’s surplus, producer’s surplus, and welfare.

We use Marshallian rather than Hicksian measures of consumer’s welfare change. In using the former approach, we also follow the theoretical merger literature assumption of no income effects (Salant et al., 1983; Farrell and Shapiro, 1990; Levin, 1990), consistent with

Marshallian applied welfare analysis. While Hicks’ compensating and equivalent variations are the correct theoretical measures of the impact on consumer’s welfare from a change in a single good’s price, most analyses have estimated consumer’s welfare change using the Marshallian demand function and consumer’s surplus concept.6 Moreover, prior literature (Willig, 1976) has shown that, if the income effects are small relative to overall income, then the Marshallian consumer’s surplus approach provides a sufficiently accurate estimate of the correct compensating and equivalent variations. Hausman (1981), however, points out that the Marshallian approach, despite providing an accurate estimate of the change in consumer’s welfare, may result in significant differences in the estimate of the deadweight welfare loss.

Since the total consumer’s surplus change, as we will see, represents less than 0.1% of Portugal’s GDP, income effects can be considered as being very small relative to overall consumer’s income. Thus, the income effects associated with a rise in the average price can be neglected. Moreover, as we shall show below, the deadweight welfare losses are quite small relative to the overall merger impact and to the consumer’s surplus change. Thus, the Marshallian consumer’s surplus approach used in this paper provides a sufficiently accurate estimate of the impact the merger would have had on consumer welfare.

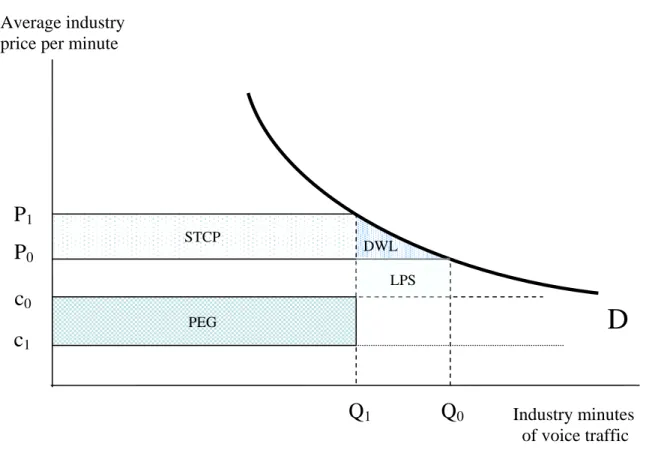

- Figure 1 about here -

Figure 1 represents the welfare impact of the merger, where D is the Marshallian market demand curve, Q is the industry output, total industry voice traffic in minutes, P is the average market price of a minute of voice traffic, c is the industry average marginal cost per minute of voice traffic, and the subscript 0 (1) is for the industry output, price, and marginal cost before (after) the merger.

welfare ∆W is defined and estimated below.

Change in consumers’ surplus

The change in consumers’ surplus would have been brought about by the increase in the post-merger average price. The impact of the merger on Marshallian consumer’s surplus is given by: (4) 1 0 1 0 1 0 P P 1 P P P P 1 AP dP AP dP ) P ( Q CS ⎥ ⎦ ⎤ ⎢ ⎣ ⎡ ε − = = = ∆

∫

∫

−ε −εand corresponds to the area to the left of the demand curve when the average industry price rises from P0 to P1 (see also Figure 1).

Substituting in equation (4) the values of parameter A, price elasticity of demand ε, and pre- and post-merger average prices estimated in Sections 2 and 3, the total change in consumer’s surplus is €103.9mn per year, which, using a 5% discount rate and an infinite time horizon, has a present value of €2.1bn. Thus, the merger would have had a large detrimental effect on consumer’s surplus.

Most of the loss in consumer’s surplus, €99.5mn, would have resulted from the transfer of surplus from consumers to producers (STCP in Figure 1), since consumers would have paid higher prices at the final, lower level of industry output. The remainder, €4.4mn, is a loss of consumer’s surplus related to the output that is no longer consumed at the higher price, the deadweight welfare loss (DWL in Figure 1). This means the deadweight welfare loss would have been relatively small compared to the transfer of surplus from consumers to producers or when compared to the overall industry size.

Change in producers’ surplus

Due to increased market concentration and economies of scale, it is reasonable to expect that the merger would have resulted in an increase in the producer’s surplus. The issue is the extent to which the change in the producer’s surplus is obtained through increased market power (improved ability to set higher prices) vs. improvements in producer efficiency (reductions in marginal costs).

The estimation of the efficiency gains is made by comparing the price-cost margins before and after the merger, considering that, after the merger, prices would have been 3.8% higher. Specifically, we have a measure of the initial non-weighted average price-cost margin for the Portuguese mobile telecommunications market in 2004 (the average EBITDA of the operators), which is 35.6%. Using the results of regression (2), we estimate that the expected long-run average margin in the Portuguese market would have increased to approximately 47.2% (see Section 2).7

Since we know initial and final average prices (P and 0 P1) and average margins (EBITDA and 0 EBITDA1), it is possible to estimate the reduction in the average marginal cost (c1− ) using the following approximations: c0

(5) 1 1 1 1 0 0 0 0 EBITDA P c P EBITDA P c P ≈ − ≈ −

where the subscript 0 (1) is for the price and marginal cost before (after) the merger (see also Figure 1).

Substituting the prior results in (5), we estimate that the merger would have resulted in an average marginal-cost reduction equal to €0.019 per minute or 14.9% of the pre-merger marginal cost. Thus, the potential efficiency gains might have been large.

Given the large reduction in the average marginal cost, the average market margin would have increased by 32.5%, nearly ten times more than the average price increase. In fact, not only would the merger have significantly enhanced industry efficiency, but it would also have resulted in an increase in the average price, relative to the steady-state with three firms. Thus, the increase in average market price is directly attributable to increased market power.

The change in producer surplus ∆PS is given by (see also Figure 1):

(6) ∆PS=STCP+PEG−LPS

where STCP=(P1−P0)Q1, PEG=(c0−c1)Q1 and LPS=(P0 −c0)(Q0−Q1). The areas STCP, PEG and LPS are, respectively, the surplus transferred from consumers to producers, the total producer efficiency gain at the final level of industry output, Q1, and the loss of producers’ surplus from the reduction in the level of industry output from Q0 to Q1.

Equation (6) indicates that the producers’ surplus would have increased by a total of €267.2mn per year, of which 37.2% would have been the result of a surplus transfer from consumers to producers. Producers would have captured the entire efficiency gain and some surplus from consumers by raising prices. Using the 5% discount rate, the present value of the total producers’ surplus increase is €5.3bn.8

Change in welfare

Finally, the change in welfare is given by:

In sum, the merger would have been welfare-improving by €163.3mn per year, with a present value of €3.3bn. This result seems consistent with the recent anecdotal evidence of growing industry consolidation. The market is driving further industry consolidation not only because firms have an incentive to increase their market power, but foremost because there are substantial efficiency gains to be had.

Analysis of the Competition Authority’s decision

The above results suggest that Portugal’s Competition Authority decision to authorize the merger might have been warranted on efficiency and welfare maximization grounds. However, the results also suggest that such a decision should have been accompanied by strict retail price-cap merger remedies. These would have been necessary to ameliorate the large detrimental merger impact on both consumer’s surplus and industry output. In fact, ICP-ANACOM (the national telecommunications sector regulator), in its October 19th, 2006 expert opinion on the merger, did recommend the implementation of relatively strict retail price caps (Autoridade da Concorrência, 2006, pp. 540-549). However, most of these recommendations were not adopted by the Competition Authority in its final decision.

The Competition Authority decision imposed some retail price-caps remedies, which constrained the merged firm to change the prices for three consumer baskets at the lowest of either the rate of change of the consumer price index for services or the average rate of change of the price of the same consumption baskets for a (confidential) group of reference European mobile telecommunications operators (Autoridade da Concorrência, 2006, pp. 734-737). The strength of the price caps would have depended on the duration, the type of consumption baskets, and the choice of reference European mobile operators, information which were all confidential. As such, it is not possible to ascertain how strict the decision’s price cap remedies would have been.

Alas, long term price-cap regulation based on the evolution of prices in other markets would have gone a long way in addressing the detrimental consumer’s surplus effects identified in this paper. However, the monitoring of the decision’s price-caps would have likely been difficult to achieve and offered the possibility for regulatory arbitrage. Thus, given the large potential costs to consumer’s welfare, reduction of consumer’s choice, and the uncertainties associated with the merger, the Competition Authority decision’s retail price remedies should have been designed to err on the side of consumer, and probably should have been much simpler to calculate, as recommended in the October 19th expert opinion of the ICP-ANACOM (Autoridade da Concorrência, 2006, pp. 547-549). This might have been accomplished, for example, by means of a one-off retail price reduction, followed by annual retail price-cap regulation of the average price per minute by the telecommunications sector regulator (ICP-ANACOM).

5. Caveats

There are a number of issues with the analysis, which we briefly discuss in this section. First, there is the issue of extending the results of our 45-country sample to the Portugal case. Our estimates are based on approximately 1700 observations which are used to draw inferences relative to the Portuguese market. We follow this approach since the sample comprehends diverse observations with a variety of market structures. This, in our view, is better than the alternative of using the few available Portuguese market observations to draw inferences about prices and margins under an entirely different post-merger market structure. The margin and price regression coefficient estimates for the Eurozone sub-sample and for the OECD sub-sample, both of which include Portugal, are larger than those of the international sample, and the price equation coefficient estimate is approximately twice as large. Moreover, price data for Portugal indicate that, from 1999 to 2004, prices in Portugal

fell by less than in other Eurozone countries, suggesting that the level of competition in Portugal was less intense than in other Eurozone countries. Thus, it may be the case that the Portuguese sub-sample distribution bears more close resemblance to the Eurozone and OECD distributions than to the international one. Therefore, the inferences we make on the rise in prices in Portugal and, consequently, on the surplus redistribution effects from consumers to producers may be, if anything, under-estimated. Indeed, the previously cited result of Grzybowski and Pereira (2008), who estimate an average price increase of 6 to 7%, points in the same direction.

Second, our SCPP-type comparative statics model departs from the hypothesis that the market is in a long-run equilibrium. The inferences one can draw are also about the long-run equilibrium, after a transitional period, ceteris paribus. While there are a number of issues with such models, the fact is that they provide a useful benchmark and have been widely used for merger analysis in the past (Salant et al., 1983; Farrell and Shapiro, 1990; Levin, 1990).

Third, as usual in applied work, the analysis faces data contraints. We based the analysis on non-weighted 2004 averages from our original data sample, and 2004 industry output data from ICP-ANACOM (2005a), but the merger would have only been carried out in 2007. In addition, it would have taken some time to actually merge the operations of the two firms. Thus, not only would prices, margins, and output data have changed somewhat in this period, but the industry as a whole might have also evolved.9 Further, it may be that our proxy for the margin, the EBITDA, captures not only price-cost margins but also efficiencies that reduce fixed costs, such as consolidation of duplicated network installations. If this were the case, our inference about the reduction in the average industry marginal cost might be over-estimated.

Forth, changes in the price elasticity of demand do not affect our policy conclusions. For example, if the average price elasticity of demand were similar to that estimated by

Hausman (1997) for the U.S. mobile telecommunications market (0.4), consumer’s surplus would have decreased by €107.7mn annually, rather than by €103.9mn (3.7% higher impact), the deadweight welfare loss would have been 81.7% smaller, at €0.8mn annually, and the producer’s surplus change would have been 35.2% larger, at €361.4mn annually. Therefore, a decision to authorize the TMN-Optimus merger would still be warranted on the grounds that there is an increase in total welfare, as long as accompanied by strict retail price-cap remedies.

Furthermore, we define output as minutes of outgoing calls plus off-net incoming calls, consistent with the way the output is defined in our dataset. However, while the operator revenues derived from outgoing calls are based on retail tariffs, operator revenues for off-net incoming calls (e.g., from fixed networks) are typically based on wholesale tariffs between operators. End consumers pay a higher retail tariff for off-net incoming calls, for which we lack data. Thus, our measure of consumer’s average price is not perfect. Nonetheless, we do not expect this issue to result in an incorrect estimate of the effect of the merger on the average retail price nor to affect the order of greatness of the results we derive and their implications for policy making. The reason is as follows. While retail prices for outgoing calls are not regulated, off-net incoming call wholesale prices between operators are regulated by ICP-ANACOM (2005b). ICP-ANACOM indicates that operators set off-net incoming-call prices at the maximum wholesale price level, which, in 2004, was of €0.185 per minute for fixed-mobile incoming calls and €0.187 per minute for mobile-mobile off-net incoming calls, slightly lower than our estimate of average price.10 Correcting for this effect, the estimated price of outgoing calls would be €0.201 per minute, which is fairly similar to the average price used in our analysis (€0.197). On the other hand, outgoing traffic was approximately 73.5% of total traffic (10653 million minutes).11 Thus, roughly 73.5% of the estimated change in consumer’s surplus results from the expected change in retail prices.

Moreover, earlier literature has found evidence of collusion in duopoly markets, which may not be well captured by our empirical analysis as our sample contains few duopoly markets. For example, Parker and Röller (1997) find evidence of collusion under a duopoly for U.S. metropolitan areas, with estimated price-cost margins of 35% implying that prices are 23% higher due to collusion. Busse (2000), using the same dataset, estimates that, under duopoly, multimarket contact results in 7% higher prices through collusion. Valetti (1998) as well as Stoetzer and Tewes (1996) argue that the price evolution, before and after the introduction of additional competition in the United Kingdom and in Germany, suggests there was collusion under duopoly. Hence, this literature suggests that the negative effects of the TMN-Optimus merger on consumer’s surplus might have been even larger than argued so far, due to collusive behavior.

Finally, we are not able to control for the effect of the merger remedies imposed by the Competition Authority to authorize the merger. Of course, these might have reduced the negative impact of the merger on consumers. We also do not consider tax policy effects. In fact, since the merger structure was based on a large level of debt financing, it would have resulted in a reduction of taxable income for the acquired firm, and therefore it would have resulted in a large surplus transfer from taxpayers to producers.

6. Conclusion

The authorized merger between Optimus and TMN in Portugal would have given the combined operator a 65% market share, based on pre-merger market shares. We propose a methodology for evaluating the welfare impact of the merger based on the analysis of its effects on the price and the margin of a hypothetical industry firm with average market share. The results we obtain are robust to changes in a number of assumptions. More important than the estimated absolute values of the merger impact is the order of greatness and the relation

between the different types of impacts. We find that, given the size of the mobile-voice telecommunications market, the merger would have resulted in large consumer-surplus losses as well as large producer-surplus gains. As a result of these surplus changes, overall welfare would have increased.

These findings raise important issues for a social decision-maker on the trade-off between consumer-welfare and welfare maximization. Moreover, the balance of evidence available suggests that the Portuguese Competition Authority, even if warranted in approving the merger due to the large potential efficiency gains, should have given more emphasis to retail price-cap remedies, in order to address the merger’s large detrimental consumer’s surplus effects.

References

Autoridade da Concorrência (2006) Decisão: Processo AC – I – 08/2006 – Sonaecom / PT, available at: <http://www.autoridadedaconcorrencia.pt> (accessed: August, 2007).

Brito, D., and Catalão-Lopes, M. (2006) Mergers ad Acquisitions: The Industrial Organization Perspective, Kluwer Law International BV, The Netherlands.

Busse, M. (2000) Multimarket Contact and Price Coordination in the Cellular Telephone Industry, Journal of Economics & Management Strategy, 9: 287-320.

Cooper, M. (2004) Remonopolizing Local Telephone Markets: Is Wireless Next?, White Paper, Consumer Federation of America, July.

Farrell, J., and Shapiro, C. (1990) Horizontal Mergers: An Equilibrium Analysis, American Economic Review, 80: 107-126.

Fox, J. (2005) Consolidation in the Wireless Phone Industry, NET Institute Working Papers, nº 05-13, October.

Grzybowski, L., and Pereira, P. (2008) Merger Simulation in Mobile Telephony in Portugal, Review of Industrial Organization, forthcoming.

Harberger, A. (1971) Three Basic Postulates for Applied Welfare Economics: An Interpretive Essay, Journal of Economic Literature, 9: 785-797.

Hausman, J. (1981) Exact Consumer’s Surplus and Deadweight Loss, American Economic Review, 71: 662-676.

Hausman, J. (1997) Valuing the Effect of Regulation on New Services in

Telecommunications, Brookings Papers on Economic Activity: Microeconomics, 1: 1-54. ICP-ANACOM (2005a) Anuário Estatístico 2004, available at: <http://www.icp.pt> (accessed: November, 2006).

ICP-ANACOM (2005b) Decisão: Mercados Grossistas de Terminação de Chamadas Vocais em Redes Móveis Individuais, available at: <http://www.icp.pt> (accessed: November, 2006). Levin, D. (1990) Horizontal Mergers: The 50-Percent Benchmark, American Economic Review, 80: 1238-1245.

Motta, M. (2004) Competition Policy: Theory and Practice, Cambridge University Press, Cambridge.

Parker, P., and Röller, L.H. (1997) Collusive Conduct in Duopolies: Multimarket Contact and Cross-Ownership in the Mobile Telephone Industry, RAND Journal of Economics, 28: 304-322.

available at <http://www.ios.neu.edu> (accessed: March, 2008).

Perry, M. and Porter, R., (1985) Oligopoly and the Incentive for Horizontal Merger American Economic Review, 75: 219-227.

Salant, S., Switzer, S., and Reynolds, R. (1983) Losses from Horizontal Merger: The Effects of an Exogenous Change in Industry Structure on Cournot-Nash Equilibrium, Quarterly Journal of Economics, 98: 185-199.

Stewart, J., and Kim, S.K. (1993) Mergers and Social Welfare in U. S. Manufacturing 1985-86, Southern Economic Journal, 59: 701-720.

Stoetzer, M.W., and Tewes, D. (1996) Competition in the German Cellular Market? Lessons of Duopoly, Telecommunications Policy, 20: 303-310.

Valetti, T., and Cave, M. (1998) Competition in UK Mobile Communications Telecommunications Policy, 22: 109-131.

Willig, R. (1976) Consumer’s Surplus Without Apology, American Economic Review, 66: 589-597.

Table 1. Price equation

Dependent variable: logarithm of average revenue per minute calculated using (1) 2004 nominal exchange rates to the Euro; (2) data in Euros; (3) annual PPPs to the US Dollar.

(1) (2) (3) Full sample Eurozone sample OECD Sample

Lagged market share 0.229 0.459 0.413

(0.000) (0.000) (0.000)

Lagged churn rate -1.133 0.603 -6.764

(0.203) (0.602) (0.000)

Mobile party pay -0.527 -1.830

(0.000) (0.000) Observations 1658 457 1141

R-squared 0.874 0.827 0.792

P-values based on robust standard errors are in parentheses. Regression controls include country, year and quarter effects. Country and year effects are jointly significant at the 1% level. Quarter effects are jointly significant at 1% level in (1) and at 10% level in (2). They are not jointly significant in (3).

Table 2. Price-cost margin equation

Dependent variable: EBITDA margin

(1) (2) (3)

Full sample Eurozone sample OECD sample

Lagged market share 0.696 1.080 0.742

(0.000) (0.000) (0.000)

Lagged churn rate -0.131 0.430 -0.773

(0.535) (0.800) (0.401)

Observations 1846 468 1168

R-squared 0.560 0.667 0.526

P-values based on robust standard errors are in parentheses. Regression controls include country, year and quarter effects. Country and year effects are jointly significant at the 1% level. Quarter effects are not jointly significant.

Figure 1. Welfare effects

c

0Q

1D

Q

0 STCPP

1P

0c

1 PEG LPS DWL Industry minutes of voice traffic Average industryAppendix. Selected sample statistics

Table A1. Variables

Variable Obs Mean Std Dev Min Max

EBITDA 2482 0.269 0.375 –9.170 0.770

MSHARE 3390 0.284 0.176 0.010 0.950

MPP 3760 0.163 0.369 0.000 1.000

CHURN 2074 0.022 0.017 0.001 0.400

ARPM 2107 0.184 0.093 0.026 1.065

Table A2. Year effects

Year Freq Perc Cum

1999 656 18.37 18.37 2000 634 17.75 36.11 2001 630 17.64 53.75 2002 653 18.28 72.03 2003 663 18.56 90.59 2004 336 9.41 100.00

Table A3. Quarter effects

Quarter Freq Perc Cum

1 976 27.32 27.32

2 979 27.41 54.73

3 810 22.68 77.41

4 807 22.59 100.00

Table A4. Country effects

Argentina, Australia, Austria, Brazil, Belgium, Canada, Check Republic, Chile, China, Colombia, Denmark, Egypt, Finland, France, Germany, Greece, Hong Kong, Hungary, India, Indonesia, Ireland, Israel, Italy, Japan, Korea, Malaysia, Mexico, Netherlands, New Zealand, Norway, Philippines, Poland, Portugal, Russia, Singapore, South Africa, Spain, Sweden, Switzerland, Taiwan, Thailand, Turkey, United Kingdom, United States, Venezuela.

Endnotes

1

Mobile-voice communications represented approximately 80% of the €3bn mobile telecommunications industry in Portugal in 2004.

2

Stewart and Kim (1993) estimate the effect of exogenous factors and observed merger activity level on price indices levels and price-cost margins, for a sample of 117 U.S. three digit manufacturing industries. They use these estimates to calculate the impact of the merger activity level on consumer’s surplus, producer’s surplus, and welfare for industries grouped according to concentration levels.

3

The use of lagged explanatory variables also has the benefit of addressing the endogeneity issue in the econometric estimation.

4

We obtain similar results if we drop the MPP regressor to obtain symmetric equations.

5

The average revenue per minute in 2004, based on ICP-ANACOM (2005a), is €0.169 or 14.2% lower than Merrill Lynch’s first half of 2004 data. The difference may be explained by falling prices in the second half of 2004, the use of weighted vs. non-weighted estimates, and measurement discrepancies. To maintain consistency in the use of the econometric results, we use Merrill Lynch estimates. Nonetheless, the use of the ICP-ANACOM measure of price does not significantly affect the results of the welfare analysis presented in Section 4 (results based on ICP-ANACOM data are available from the authors upon request).

6

The Hicksian measure of surplus considers both substitution and income effects when the good’s price changes. The Marshallian consumer’s surplus is equivalent to only considering the substitution effect.

7

Interestingly, the Financial Times Lex column of October 3rd, 2006 suggested that the merged firm (Optimus-TMN) could have increased its EBITDA margin to 48%, fairly similar to our own estimate.

8

Private sector firms calculate the present value of the synergies of a merger based on a shorter time horizon (7 years), and often with no discount rate. Using this methodology, we estimate the private value of the merger at €1.9bn. This compares with an estimate of €2bn provided by the Financial Times Lex column of October 21st, 2006 and with the acquirer’s (Sonaecom) estimate of €1.5-2bn for the full Sonaecom-PT merger.

9

A seminar participant pointed out that new technologies (e.g. VoIP and Wi-fi) may affect the competitive dynamics in this industry. Nonetheless, the effect of new technologies is likely to remain marginal in the near term. In fact, in mature markets, mobile operators’ revenues and output are still growing, even if at lower rates than in the past. Thus, the merger would still have had a large economic impact.

10

Optimus was allowed to set a higher fixed-mobile termination rate.

11

The merger effect on consumer’s surplus could have been lessened if the mobile-to-mobile off-net traffic between TMN and Optimus became on-net traffic as a result of the merger. Since off-net tariffs are higher than on-net tariffs, this might have resulted in a smaller increase of the average price than that predicted by our model. Total mobile-to-mobile off-net traffic between the three pre-merger operators was 2147 million minutes or 14.8% of total traffic. However, it is not clear whether, in a post-merger context, on-net prices would have applied to the part of this traffic between TMN and Optimus. The reason is that the Competition Authority (Autoridade da Concorrência, 2006) did not impose lower on-net call prices in its decision to allow the merger. Thus, apparently, the merged operator would have had the choice to maintain off-net prices for communications between TMN and Optimus subscribers.