20

A thorough analysis of political risk and its implications for EDP’s internationalization strategy

A Work Project based on the CEMS MiM Business Project “Forecast of risk-return profiles in a changing environment”, under the supervision of Goncalo Rocha

Jakob Kronbichler, #1362

1

Table of Content

1. Content of the report ... 2

A) Company ... 2

B) Market overview ... 2

C) Current client situation ... 3

D) The business project challenge ... 3

E) Summary of conclusions ... 3

2. Political risk and its implications for EDP’s internationalization strategy ... 4

A) What was the original approach to this topic and what were its main limitations? ... 4

B.1) Introduction to political risk ... 5

B.2) How to correctly assess and deal with political risk in the energy sector ... 6

3. Personal reflection on learning ... 10

A) Previous knowledge learned from your Masters program ... 10

B) New knowledge ... 10

C) Personal experience ... 11

D) What added most value? What should have been done differently? ... 11

4. Reference list... 12

2

1. Content of the report A) Company

Energias de Portugal (EDP) is Portugal’s largest business group and a European electricity provider. The Group had annual revenues of €16.1 billion in 2013 and a current market cap of €10.6 billion (May, 2014). The company is headquartered in Lisbon and mainly operates in Portugal (43% of 2013 EBITDA), Spain (26%), Brazil (18%) and the United States (9%). EDP’s business structure is divided into three main sub business units, which are EDP Iberia, EDP Renovais (Renewables) and EDP Brazil. In its core markets Iberia and Brazil, EDP operates throughout the value chain in electricity generation, electricity and gas distribution and electricity and gas supply and trading. Regarding renewable energy, EDP is the third largest wind power operator worldwide with a major presence in the United States. At the end of 2013, EDP had an installed capacity of 23GW, generating 60.9TWh, of which 67% comes from wind and hydro plants. (EDP, 2014)

In December 2011, China Three Gorges Corporation (China’s SOE in the utility sector) acquired a 21.35% Portuguese government stake in EDP for €2.69 million, making it the largest shareholder of the Group. (EDP, 2014)

B) Market overview

EDP’s home markets Portugal and Spain are currently still constituting 69% of the EBITDA of the company. These markets, as well as other Western European markets, are currently in a phase of consolidation and liberalization. There is a shift from local integrated state-owned monopolies to private multinationals. Iberia is currently undergoing an economic recession and the market is therefore saturated and characterized by rather stable electricity demand and consumption. In addition, the Portuguese generation and distribution market will be completely liberalized in 2017 (end of transition period), which will further put profitability pressure on EDP. The market was also hit by the sovereign crisis, which led to rating downgrades and increased financial costs. (EDP, 2014)

On the other hand there are new growth opportunities in emerging markets, which are characterized by rapidly increasing electricity demand and low risk in markets with power purchase agreements (PPAs) and a regulated business environment. Also, renewable energy sources are increasing at a rapid pace due to improving technology, increasing environmental consciousness and political support. (EDP, 2014)

3

C) Current client situation

The liberalization and saturation of the Iberian energy market puts considerable pressure on EDP’s future profitability. Therefore, EDP is thriving to increase its presence in growing markets in developing countries. The Group is in the phase of analyzing potential new entry opportunities. EDP is however very concerned of not increasing its risk profile and strives for a return to investment grade rating. New projects should also focus on renewable, low carbon and technologies and the aim is to increase the long-term contracts and PPAs.

D) The business project challenge

The challenge was to support EDP’s management in identifying and evaluating the best expansion opportunities, considering EDP’s goal of returning to investment grade rating and to focus on renewable energy projects.

E) Summary of conclusions

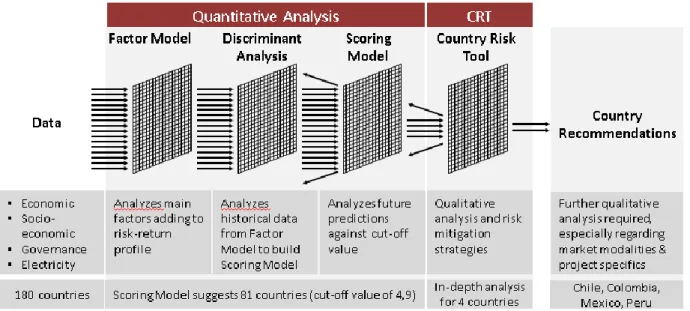

The problem was tackled by an extensive approach which included both quantitative and qualitative analysis. First, potential attractive countries were spotted with a Scoring Model based on the results of a Factor Model and a Discriminant Analysis. From an initial sample of 180 countries, the model suggested 81 countries to be very likely to be attractive. From initially 13 expansion candidates that EDP suggested us to analyze, 6 were defined as attractive by the model. Out of these 6 countries, in accordance with EDP’s risk management department, we decided to conduct an in-depth qualitative analysis for 4 candidates: Chile, Peru, Colombia and Mexico. Secondly, the Country Risk Tool, which evaluates the respective risk profiles of countries and ranked them according to their riskiness, allowed to compare and evaluate the candidates on the basis of their risk profiles. Also, it allowed for country portfolio comparison and the impact of geographic expansion on EDP’s risk profile. On the basis of the country risk profiles, mitigation strategies of the most critical risk factors were assessed via a qualitative analysis. Figure 1 and 2 of the Appendix provide a more detailed overview on the described approach and country selection process.

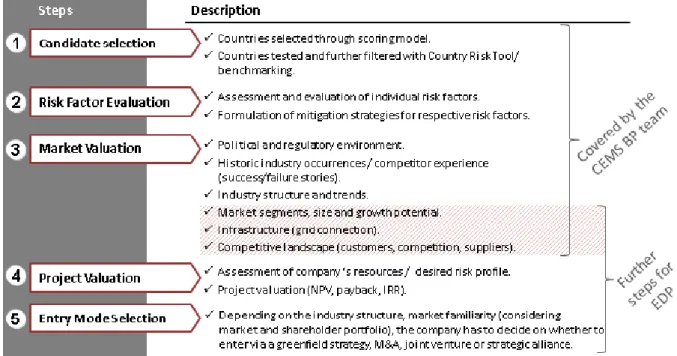

The approach identified interesting new markets and supported the viability (also from a risk profile) of entering those markets. However, the results need to be interpreted carefully, as the financial model is only based on several factors and can never include all relevant decision criteria. The approach can therefore be used to gain an initial understanding on the attractiveness and riskiness of a country. When deciding on a real investment opportunity, further analysis and due diligence (Figure 3 of Appendix) has to be carried out by EDP.

4

2. Political risk and its implications for EDP’s internationalization strategy

This section will analyze the concept of political risk and its implications for EDP’s internationalization strategy beyond the extent to which it was elaborated in the report. It will give an overview of the concept of political risk and identify suitable mitigation strategies for EDP based on a systematic risk management approach.

A) What was the original approach to this topic and what were its main limitations?

In the quantitative analysis of our business project, political risk was only included to a limited extent. The factor model assessed the overall riskiness of a country by Damodaran’s (2013) market risk premium, which is calculated as an aggregate of default risk measures, country risk scores (including economic, political and other risk) and equity risk measures. In the Country Risk Tool (CRT), political risk was individually addressed and represented a major category (together with financial risk, economic risk and other risks). The category consisted of 3 subcategories with a total of 13 variables constituting to the political risk category. These subcategories and the respective variables were: 1) risk from governance (voice and accountability, political stability, government effectiveness, regulatory quality, rule of law, corruption), 2) risk from doing business (starting a business, construction permits, getting electricity, getting credit, enforcing contracts), and 3) investment Risk (investor protection, resolving insolvency). The data used to calculate this political risk proxy came from the World Bank. Regarding the first category “Risk from Governance”, data came from the Worldwide Governance Indicators (WGI) project, which is based on a large number of enterprise citizen and expert survey respondents in industrial and developing countries. Regarding the subcategories “Risk from Doing Business” and “Investment Risk” the tool obtained the relevant data from the Doing Business Project, which gathers measures of business regulations and their enforcement among a wide set of countries. (See Table 1 and 2 of Appendix for indicator details and Figure 4 for a detailed example of the CRT model) An issue with the Worldwide Governance Indicators is that it only partially reflects the political environment for businesses, since it also largely focuses on individual citizens. A major weakness of the Doing Business Project is that it analyzes the business environment for small and medium-size companies and not, as it is the case for EDP, a major international corporation. (World Bank, 2013) Also, for all the three subcategories the analysis is kept at a macro level, not considering that political risk is especially critical in the energy industry due to the high sunk costs and potential economic damages from events such as expropriations.

5 Regarding the qualitative assessment of mitigation strategies for the 4 countries chosen, the assessment in the business project was conducted on a very broad level, including also financial, economic and other risk factors. Political risk mitigation strategies were identified, but as it was regarded to lie outside of the core purpose of the project, the report did not go into details and left room for interpretation on what mitigation strategies would be most feasible to be implemented by EDP.

B.1) Introduction to political risk

Political risk assessment has gained in importance throughout recent decades as transnational investments have been increasing at a fast pace and crises such as the Euro-zone negotiations or the Arab Spring took form rapidly and with little warning. (MIGA, 2013)

Foreign direct investment (FDI) flows worldwide reached an estimated $1.5 trillion in 2013, of which $617 billion to developing countries (MIGA, 2013). FDIs, in particular Greenfield investments, require a careful consideration of all possible political developments in a country. However, even though a recent World Bank study found out that half of all organizations believe that political risk is the most important constraint on investments in emerging markets (MIGA, 2013), there is still little agreement on how to best deal with it. In a PricewaterhouseCoopers and Eurasia Group study (2006), the vast majority (83%) of respondents said they would engage in ongoing monitoring of the political environment after an investment has been made, but nearly as many (73%) felt that they did not have effective political risk management processes in place. (PwC, 2006)

Adding to the complexity of political risk analysis is the fact that the specialized institutions (e.g. the World Bank Group, Eurasia Group, Business Environment Risk Intelligence) providing the information to investors in the context of the political insurance industry, do not disclose their exact methodology for risk-assessment for the obvious reason of competition. Comparisons between different political risk assessments are therefore very difficult to draw and this lack of transparency is one of the main reasons why political risk assessment is often considered a “soft science”. (Sottilotta, 2013)

The notion of political risk started in the 1960s when it was considered a phenomenon which would mostly occur in underdeveloped countries (Zink, 1973). The occurrences of political events such as the oil shock in 1973 and the Iranian revolution in 1979 with major economic consequences increased political risk awareness and led to the establishment of the political risk insurance (PRI) industry (Simon, 1984). The concept of political risk has then changed in

6 light of geopolitical terms and shifted from being a practice only conducted by Western countries on developing ones to a truly global activity. In fact, Satyanand (2011) points out that developing countries invest more in risky markets than their Western peers. Also, mainly due to the recent Eurozone crisis starting in 2008, political risk is nowadays not only associated with developing nations (Sottilotta, 2013).

Political risk can arise at a macro and micro level. Macro political risk refers to the situation when a political change is influencing all foreign companies. Micro political risk on the other hand defines the situation when changes are only affecting specific industries or companies. (Sottilotta, 2013) Macro political risk is usually assessed by institutions and consulting firms, through indices such as the Business Environment Risk Intelligence (BERI) Political Risk Index or the Economist Intelligence Unit (EIU) Political Instability Index, which rely on the judgment of country experts, and their subjective weights of assigned risk factors and indicators. Regarding the micro level, it is important to notice that political risk analysis is very much dependent on the industry that a company operates in. Companies operating in industries with a large capital asset base and raw material requirements (high sunk costs) that constrain their location choices are the most strongly affected by long-term political risk (e.g. critical change in the regime). These industries are usually highly regulated and include energy, natural resources and telecommunication. On the other hand, firms with more flexible operating platforms such as consumer product companies, care more about short-term risks such as protests or strikes that could negatively affect their reputation. (PWC, 2006)

Therefore, in the case of EDP, long-term political risk is among the most crucial aspects to consider when evaluating the attractiveness of a country. It is crucial for EDP to correctly assess political risk in the first place, and in a second step implement the necessary mitigation strategies for the respective risks.

B.2) How to correctly assess and deal with political risk in the energy sector

Political risks can appear in different forms and can have several causes. They can stem from governments, but also non-governmental organizations, trade unions or other groups pursuing political objectives. Political risks can mainly occur in the following ways: bribery, capital controls, contract default, expropriation/nationalization, license cancellation, protests/strikes, regulatory change, taxation, and war/terrorism. (Accenture, 2012) A further description of these political risk types together with some examples can be found in Table 3 of the Appendix.

7 Political risks also differ between developed and developing countries. Regarding regulation, advanced economies are characterized by stiffer regulations and protection of national companies. In developing countries on the other hand, regional or bilateral agreements as well as safe haven regulations, can make it difficult for an international company to operate. Cash flow expropriation can appear in various forms of taxation (e.g. windfall taxes in Australia) in advanced economies, whereas in developing economies it often takes the form of real asset expropriation or compulsory partnerships with local companies. Social or environmental oppositions to projects arise in both developed and undeveloped countries. A recent example is the HidroAysén project in Chile, a joint venture between Endesa and Colbún, which was decided upon in 2011 and involved the creation of five hydro plants with a total capacity of 2,750 MW (representing 20% of Chile’s generation base). However, heavy protests from Chile’s population put the project on stand-bye in 2012 (Dettoni et al., 2012). EDP has to follow a systematic political risk management approach in order to improve on its overall business performance. The following proposed approach has been developed by Accenture (2013) and involves a three-stage process.

Stage 1 identifies the main political risk by geographic location. The critical question is how political actions directly affect the objectives of the company. It is crucial to distinguish between perceived and real political risk. In some situations there might be substantial political instability in a country, but with relatively little influence on the company’s operations. EDP’s risk management has to develop an evidence based set of risk scenarios, based on detailed data directly relevant to the company’s objectives. Once a broad set of political risk scenarios is constructed, the risk management can prioritize on the ones that are most relevant to the business. Risks can be ranked according to relevance on the basis of a matrix combining probability and impact. Additional criteria might include recent losses, board-level concerns or high vulnerability to extreme events.

In stage 2, the impact of each political risk scenario has to be assessed. For this purpose, a discounted cash flow (DCF) analysis can be used in order to estimate the financial impact of major changes caused by political nature, such as changes in regulations or taxes. Other possible tools would be an organizational network analysis, which could estimate the operational impact of specific risk by creating a model of the company as a network of several inter-dependent business units. Finally, companies can use an Enterprise Risk Management (ERM) diagnostic tool, which measures risk management maturity along several dimensions. The most important aspect of measurement is to translate identified risks

8 into comprehensible metrics, such as dollar figures. Considering the characteristics of the energy industry (large potential impacts of long-term political risk) and EDP’s intention to expand to developing countries (mostly countries in South America), the company should pay special attention to the following types of political risks: bribery, contract default, expropriation/nationalization, regulatory changes, licensee cancellation, war and terrorism. Stage 3 involves managing risk, i.e. setting up the appropriate mitigation strategies. The following table gives an overview of EDP’s possible mitigation strategies when dealing with different political risk scenarios. The following mitigation strategies were identified as most relevant and should be implemented: joint venture, lobbying, community initiatives and PRI.

EDP could therefore mitigate its political risk exposure by partnering with a local player in a developing market, or alternatively enter a joint venture with a multinational company that is already established in the market and has good connections with the local government. EDP should also focus on developing a sustainable and long-term position in the host country. Lobbying should be considered, but it is important to comply with anti-corruption and anti-bribery laws. Bribery is a very common problem in the energy industry and often

Mitigation Strategy What is it? Relevance for EDP

Joint Business Venture

Partner with local company that

understands political risk environment and has good connections with government

Very relevant, as energy sector requires close collaboration with government and knowledge about business environment.

Political Risk Insurance (PRI)

Covers a number of political risk types and can considerably reduce risk exposure

Very relevant, as energy sector is

characterized by high sunk costs and long-term perspective

Lobbying

Legitimate influencing of governments through industry associations, or strategic advice from former cabinet members etc.

Very relevant, as projects are often assigned by government. However, full compliance with anticorruption laws has to be in place

Community Initiatives

Social Responsibility activities (e.g. partnerships with NGOs, education initiatives, etc.)

Very relevant, especially in countries which have high degree of social inequality (most LATAM countries)

Asset/Personnel Security Management

Management of risks to personnel or assets due to political violence, terrorism, etc.

Relevant, as top managers of multinationals are often target for kidnapping etc.

Financial Hedging Financial instruments (forwards, futures) to limit financial exposure to political risk

Relevant, but mainly addressed under financial risk management

Portfolio Diversification Diversify investment portfolio using political risk as a key factor

Not relevant, as EDP is seeking for FDI and not portfolio investments

Agile and Resilient Supply Chain

Flexible supply chain to respond to significant disruptions

Not relevant, as EDP is bound to location due to high sunk costs

9 companies argue that such under-the-table payments are normal and necessary business practices. However, bribe payments can have severe negative consequences. It can seriously damage a company’s international reputation or - in the case of a change in the political leadership of a developing country – undermine a company’s position locally. (Gale, 2008) Many international companies try to avoid this problem by using an intermediary, in many cases the firm’s local partner. However, this does not guarantee immunitiy from political and criminal prosecution. A good strategy is to invest in development projects in local communities. By doing so a company ensures to have the local support. Also, it makes it more difficult for corrupt officials to undermine a company’s position in other ways. (Gale, 2008) Companies operating in a market in which there are clear signs of corruption may also review their code of conduct and organize local training activities in order to ensure that all rules are thoroughly understood. (Accenture, 2012)

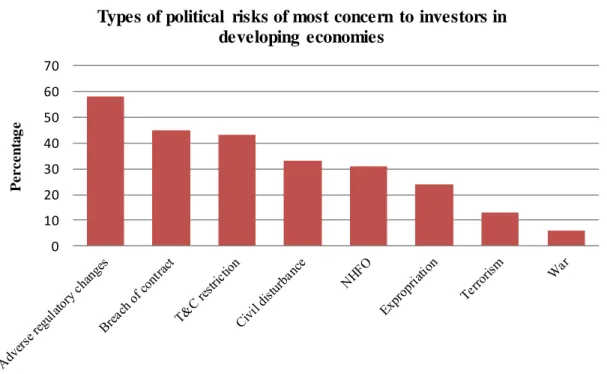

Besides these preventive measures, PRI can be used to reduce the risk of investing in developing countries. The PRI industry is increasing rapidly, with new issuance by members of the Berne Union (the leading association of public, private and multilateral insurance providers) increasing by 33% in 2012 to approximately $100 billion (even though worldwide FDI fell during the same time period). The ratio of FDI to PRI in 2012 has been 14.2% for developing markets. PRI is available for convertibility insurance, expropriation insurance, war and civil unrest insurance and breach of contract insurance. Figures 5 and 6 in the Appendix provide an overview of which political risks are the most severe ones in terms of investor concerns and losses incurred. (MIGA, 2013)

PRI is highly relevant for EDP, as the MIGA report (2013) points out that the electricity and power sector is accounting for 19% of all contract breaches (the only industry scoring higher is the oil & gas industry with 24%). PRI can effectively ensure against project delays, damage and cancellation caused by unforeseen political incident or regulatory complications. (Parnell, 2014)

However, there are limitations in the scope of PRI since it does not cover against all political risks. Legitimate government actions and laws, such as revised tax rates or regulations that are non-discriminatory and apply to all companies in general, are not covered. (Tchajkov, 2013) Also, in energy infrastructure projects a government party is often a stakeholder. PRI does not protect foreign investors from a government party being an unreliable partner. (Howell, 2012) Finally, PRI is expensive, typically measured in percentage terms rather than per mill, as are standard property and casualty policies. (Gould, 2013)

10

3. Personal reflection on learning

A) Previous knowledge learned from your M asters program

Throughout the project, I could benefit from a solid knowledge base obtained during my master program.

In particular the finance courses, such as Financial Management, M&A, Corporate Interaction with Markets and Financial Statement Analysis, helped me to get a good understanding of basic required financial theory such as portfolio theory, valuation, capital budgeting, and profitability analysis. Also, these courses sharpened my analytical thinking skills and improved my Excel capabilities.

From Project Management I learned how to approach a project of such length and complexity, by planning it in advance and setting up important KPIs and milestones.

The course Corporate Strategy helped me to obtain a good understanding of the complex operations of major international corporations such as EDP. Also, it enabled me to develop a good understanding of the energy industry.

Finally, Macro for Managers and Sustainable International Business provided me with the relevant macroeconomic background to understand current developments in the energy industry.

B) New knowledge

Since I am a management student and the business project was mainly about financial modelling, I gained a lot of new knowledge while working on the project.

Understanding all the reasoning and implications behind the factor model was a big challenge for me, as I had no previous experience with financial modelling.

I also gained a lot of knowledge in the field of risk management. Besides considerably improving my Excel skills, building the Country Risk Tool (Excel based risk model) taught me how to identify and quantify different risk variables that you have to consider when operating internationally.

Finally, I obtained a good insight into the energy industry, which was originally the main reason why I listed this business project among my preferences.

11

C) Personal experience

Overall, the experience of working as a group on such a challenging project in the energy industry was very positive. Within the group we got along very and even though we did not have an outspoken leader we managed to coordinate and divide up tasks nicely and fairly. I proved myself that I can handle challenging situations and content which lies outside my area of expertise. I also prioritized my efforts according to the different tasks the project required. I realized that when it comes to econometrics there were group members with a more advanced skill set. Therefore, I tried to create most value possible for the group by focusing on my main strengths, which are in strategy and management. As a consequence I assumed major responsibility for the Country Risk Tool and the detection of mitigation strategies. Also, I functioned well within our very diverse group (4 different nationalities and various academic backgrounds) as well as in the corporate environment during the meetings and presentations at EDP.

Regarding weaknesses, the project clearly demonstrated that even though I have a solid finance base, I still lack knowledge and expertise to work on complex financial models. Also, the project made me realize that I still have to improve on my personal planning and organization skills. Even though we finished everything in time, we always faced substantial time pressure before the meetings and the final deadline.

D) What added most value? What should have been done differently?

In hindsight I believe that the main strength of our project was the integration of a quantitative and a qualitative model, which resulted from the diversity of our group. However, while everyone focused on its major strengths, we continuously made sure that everyone was always on track regarding all the different areas of the project.

Doing the project again, I would try to improve in the communication with our corporate advisors. Especially at the beginning we were left in the dark and nobody of the group really knew what to do and where we were heading. Instead of seeking the dialogue with our corporate advisors, we continued working on what we believed could be right. This resulted in a very inefficient first phase of the project and a misalignment of EDP’s and our own project perception. Furthermore, we wasted considerable time and effort in doing things that were out of the project’s purpose. It was very unnecessary, since our academic and corporate advisors were very helpful and always available if we had any questions or concerns.

12

4. Reference list

Damodaran A. (2013). Rediscovering risk in emerging markets: A Country Risk Premium

update. Retrieved on May 13, 2014, from:

http://aswathdamodaran.blogspot.pt/2013/07/rediscovering-risk- in-emerging- markets.html

Dettoni J. & Stankova Y. (2012). Chile’s Power Challenge: Reliable Energy Supplies.

PowerMag.com. Retrieved on May 13, 2014, from: http://www.powermag.com/chiles-power-challenge-reliable-energy-supplies/

Energias de Portugal - EDP (2014). 2013 Annual Report. Retrieved on May 18, 2014, from:

http://www.edp.pt/en/Investidores/publicacoes/relatorioecontas/2013/Annual%20Report%20 2013/RC_EDP_2013_ING.pdf

Energias de Portugal - EDP (2014). 2013 Investor Presentation. Retrieved on May 18,

2014, from:

http://www.edp.pt/en/Investidores/publicacoes/tematicas/Apresentaes%20Temticas/Investor %20Presentation%20-%20March%202014.pdf

Gale B. (2008). Identifying, assessing and mitigating political risk. INSEAD Knowledge.

Retrieved on May 13, 2014, from:http://knowledge.insead.edu/economics-politics/identifying-assessing-and-

mitigating-political-risk-2013?nopaging=1#QSv7GqBbL6e6lpi4.99

Gould J. (2013). RPT – As political risks proliferate, insurers step up to cover. Reuters.

Retrieved on May 12, 2014, from: http://uk.reuters.com/article/2013/07/10/insurers-politicalrisk-cover- idUKL5N0EU3US20130710

Howell N.M. (2012). An Overview of Political Risk Mitigation for Energy Projects in

Emerging Markets. King & Spalding, Retrieved on May 12, 2014, from:

http://www.kslaw.com/library/newsletters/EnergyNewsletter/2012/June/article5.html

MIGA (2013). World Investment and Political Risk Report. Multilateral Investment

Guarantee Agency – World Bank. Retrieved on May 15, 2014, from: http://www.miga.org/documents/WIPR13.pdf

Parnell J. (2014). Renewables insurance firm offers political risk policy. PV Tech. Retrieved

on May 13, 2014, from:

13

PwC Advisory and Eurasia Group (2006). How managing political risk improves global

business performance. Retrieved on May 13, 2014, from: http://www.pwc.com/us/en/risk-compliance/assets/PwC_PoliticalRisk_052006.pdf

Satyanand, P.N. (2011) How BRIC MNEs deal with International Political Risk. The Vale

Columbia Center on Sustainable International Investment.

Simon, J. D. (1984). A Theoretical Perspective on Political Risk. Journal of International

Business Studies, Vol. 15, No. 3 (Winter), pp. 123-143.

Sottilotta C.E. (2013). Political Risk: Concepts, Definitions, Challenges. LUISS Guido

Carlli School of Government.

Tchajkov A. (2013). Politically Speaking. Canadian Underwriter Ca. Retrieved on May 12,

2014, from: http://www.canadianunderwriter.ca/news/politically-speaking/1002811838/?&er=NA

The World Bank (2014). Doing Business – Measuring Business Regulations. Retrieved on

May 12, 2014, from: http://www.doingbusiness.org/

The World Bank (2014). Worldwide Governance Indicators project (2014). Retrieved on

May 12, 2014, from: http://info.worldbank.org/governance/wgi/index.aspx#home

Zink, D.W. (1973). The Political Risks for Multinational Enterprise in Developing Countries

14

5. Appendix

Figure 1: Overview of the country selection approach developed in the BP.

Figure 2: Left: graphical illustration of the results of the factor model. Right: countries filtered according to EDP’s preference list.

15

Figure 3: Overview of steps covered by the CEM S BP team and further steps for EDP.

World Bank Ease of Doing Business (entrepreneurial environment)

Starting a Business Procedures, time, cost and minimum capital to open a new

business Dealing with Construction

Permits

Procedures, time and cost to build a warehouse

Getting Electricity Procedures, time and cost required for a business to obtain a

permanent electricity connection for a newly constructed warehouse

Registering Property Procedures, time and cost to register commercial real estate

Getting Credit Strength of legal rights index, depth of credit information index

Protecting Investors Indices on the extent of disclosure, extent of director liability

and ease of shareholder suits

Paying Taxes Number of taxes paid, hours per year spent preparing tax

returns and total tax payable as share of gross profit

Enforcing Contracts Procedures, time and cost to enforce a debt contract

Resolving Insolvency The time, cost and recovery rate (%) under bankruptcy

proceeding

16 World Bank World Wide Governance Indicators

Voice and Accountability (VA) Capturing perceptions of the extent to which a country's citizens are able to participate in selecting their government, as well as freedom of expression, freedom of association, and a free media.

Political Stability and Absence of Violence (PV)

Capturing perceptions of the likelihood that the government will be destabilized or overthrown by unconstitutional or violent means, including politically-motivated violence and terrorism.

Government Effectiveness (GE)

Capturing perceptions of the quality of public services, the quality of the civil service and the degree of its independence from political pressures, the quality of policy formulation and implementation, and the credibility of the government's commitment to such policies.

Regulatory Quality (RQ) Capturing perceptions of the ability of the government to

formulate and implement sound policies and regulations that permit and promote private sector development.

Rule of Law (RL) Capturing perceptions of the extent to which agents have

confidence in and abide by the rules of society, and in particular the quality of contract enforcement, property rights, the police, and the courts, as well as the likelihood of crime and violence.

Control of Corruption (CC) Capturing perceptions of the extent to which public power is

exercised for private gain, including both petty and grand forms of corruption, as well as "capture" of the state by elites and private interests.

17

Figure 4: Example of CRT output. Comparison of Chile with Brazil. Green bars suggest that Chile is performing better (lower risk) than Brazil in the respective risk factors.

0,00 0,10 0,20 0,30 0,40 0,50 0,60 0,70 0,80 0,90 C red it R is k R ati n g S& P 5 Y C D S 10 Y Bo nd S p rea d Tr an sa cti o n Ri sk : F X vo la ti lity Tr an sl ati on R is k: S p ot ra te tr en d G D P p er c ap ita G D P p er c ap ita g ro w th r ate 5 Y El ec tr ic al C o n su m p ti o n p er C ap ita En er gy P o ver ty In fl at io n 5 Y A ver ag e El ec tr ic ity T ra n sm is si o n L o ss es R oa d D en si ty Se co nd ar y Ed uc ati on Ter ci ar y Ed uc ati on C u ltu ra l D is ta n ce G in i-C o e ff ic ie n t U n em p lo ym en t R ate V o ic e an d A cc o u n ta b ili ty P o liti ca l S ta b ili ty G o ver n m en t Ef fec ti ven es s R eg u la to ry Q u a lity R ul e o f L aw C o rr u p ti o n S ta rti n g B u si n e ss C o ns tr u cti o n P er m its G etti n g El ec tr ic ity G etti n g C red it En fo rc in g C o n tr ac ts In ves to r P ro tec ti o n R es o lv in g In so lv en cy N at ur al C ata str op he Li ke lih o o d o f D is e a se s

Sovereign Risk FX Risk Demand CPI

Infra-structure HR Risk Social Inequality Risk from Governance Risk from Doing Business Investment Risk Natural

FINANCIAL RISK ECONOMIC RISK POLITICAL RISK OTHER

RISK G lo b al P e rc e n ti le S co re Lo w R is k H ig h R is k

Worse than Brazil Better than Brazil World Average Brazil

18

Risk Type Examples

Bribery Necessity to pay government officials in order to receive contract

Unforeseen border “taxes”

Capital Controls Limits of profit repatriation

Administrative delays in approving capital transfers

Contract Default Politically-driven debt default

Politically-driven failure to deliver on a contract

Expropriation/ Nationalization

Confiscation of a plant

Forced sale of assets to government at below-market price

Politically driven increase in state ownership of joint ventures

Licensee Cancellation Change to organization’s License to Operate ahead of an election

Loss of Social Licens e to Operate from lack or loss of local community support

Protests/Strikes Anti-government or anti-company protests; work stoppages

Costly project delays due to demonstrations and lawsuits

Regulatory Change Complex new environmental or labor standards

Regulatory enforcement authority handed to a state-owned company

Taxation Windfall taxes levied over “excessively high” profits

Duplicate tax claims by/between central and local governments

War and Terrorism Border and road closures due to interstate fighting

Politically motivated terrorist attacks against foreign investors

19

Figure 5: Types of political risks of most concern to investors in developing countries. T&C=Transfer and convertibility restrictions; NHFO=Non-honoring of financial obligations. Source: M IGA-EIU Political Risk Survey .

Figure 6: Financial losses incurred over the past three years on account of political risks. T&C=Transfer and convertibility restrictions; NHFO=Non-honoring of financial obligations. Source: M IGA-EIU Political Risk Survey .

0 10 20 30 40 50 60 70 Pe r c e n ta g e

Types of political risks of most concern to investors in developing economies 0 5 10 15 20 25 30 35 40 45 P e r c e n ta g e

Financial losses incurred over the past three years on account of political risks