The current state analysis revealed that the case company's current financial reporting has deficiencies that affect the accuracy of the reports. The third segment is relatively small compared to the other two and the goods are purchased outside the company. The aim of the study is to identify the best possible costing method that can meet the real need for proper financial measurement in the case company.

After the objective determination, the process continues by analyzing the current state of the reporting status of the case company. The reason for this restriction was that the idea was to reveal the current utility status of the reports. In this strategy, the company has determined profitability as one of the areas to focus on.

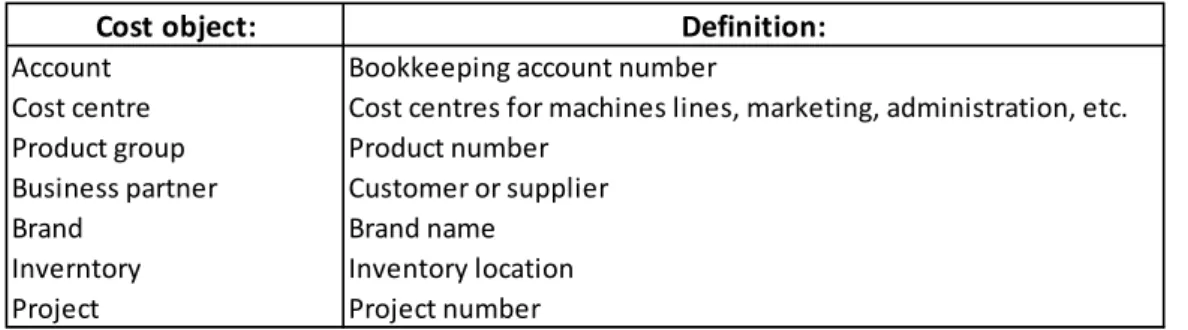

The cost price provided by the current ERP system is used to report profit per product and customer, but it has proven to be unreliable due to the slightly large variation of the own price compared to the standard own price. The owners of the company in question are also all members of the board of directors, so there is no separate owner reporting except for the annual financial report. This table is essential so that the sales department can correctly formulate prices based on the current production price level.

The executive committee of an eligible company consists of the directors of each department of the company, i.e. This is part of the literature review of the study and is intended to provide the theoretical background for developing the most appropriate method for the appropriate company. According to C.I.M.A (Chartered Institute of Management Accountants), standard costing can be defined as "the preparation of standard costs and their use to measure deviations from actual costs and to analyze the causes of changes in order to maintain maximum efficiency in production" (Arora 2010). ).

Activity Analysis

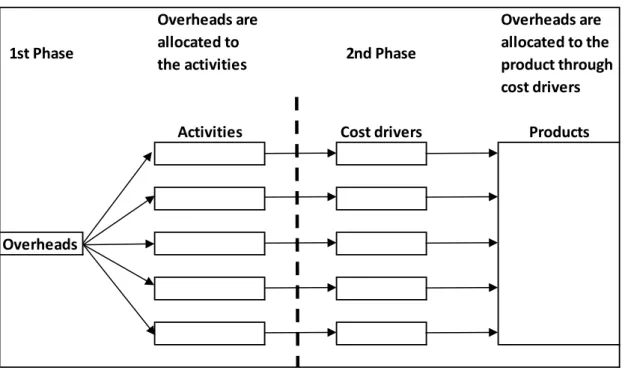

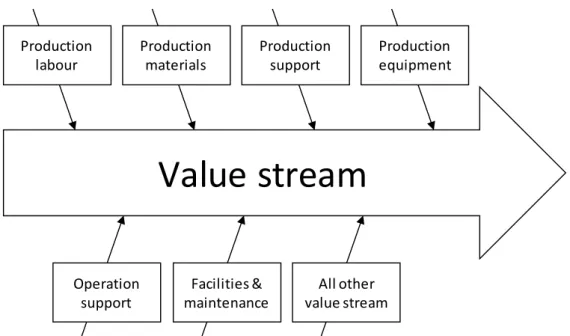

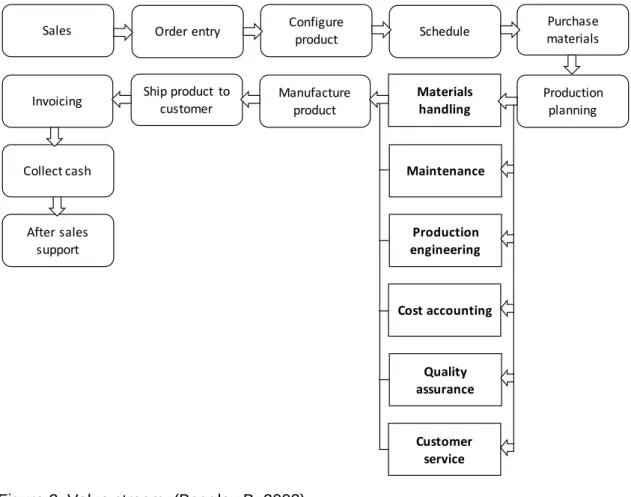

To implement the activity-based costing system in a company, a great deal of cooperation is needed between different departments of the company. Cost drivers must be chosen carefully and no one person can have the type of information from all departments.

Use of resources

Specification of cost drivers

Costing of the cost to object

Lean accounting is more of a term that brings together the changes needed in the accounting department of a company that has adopted the lean idea. Often when a company implements the lean concept, they ran into a situation where accounting holds back lean development. The reason is that traditional accounting is designed for mass production, while lean is about creating value for the customer.

According to Maskell and Baggley, lean accounting principles can be divided into five distinct areas:.

Lean and simple business accounting

Accounting process that supports the lean transformation

Clear and timely communication of information

Planning and budgeting from a lean perspective

Strengthen internal accounting controls

As mentioned before, the case company has strategy that focuses on growth, profitability and digitization. Although the case company does not have that many customers, it is vital to know the real profit they generate. With this background, the new model should be transparent, explainable, and since the case company does not have any specific resources reserved for this task, it should be easily maintained.

When considering the possible advantages and disadvantages of the different methods, it is important to recognize the case company's business. The case company basically purchases raw materials daily and this causes fluctuation in the price of the used raw materials. Private label manufacturing on the other hand is not at the core of the case company's business as it aims to increase sales of its own brands.

The pricing does not rely on the cost of the product, but the value that the product would give to the customer. When considering the case company, it would be far too big a risk to turn the entire organization into a lean model. The case company is starting a project aimed at modernizing the current ERP system.

The project will start in the coming months and would give the company handling the case the opportunity to rearrange all the basic settings so that they can start using the new reporting model. The example company is relatively aware of what the price is for a single product. The proposed model would serve the company well and is widely recognized as very suitable for a manufacturing environment.

In addition, it is recommended that the company handling the case uses some kind of light reporting program. In addition to the findings within the case company, the literature search provided a valuable perspective on the methods used to analyze manufacturing companies. The chosen Activity Based Accounting method seems to fit quite well with the requirements or profile of the case company, so to speak.

For the case company, that is probably not the best because raw materials are purchased in different units such as kilograms, meters or square meters. It describes in a simple way how the different units can be made equal, so that the end result is correct. The result of this stage is the total cost that one product bears for the total amount of overheads that the case company has.

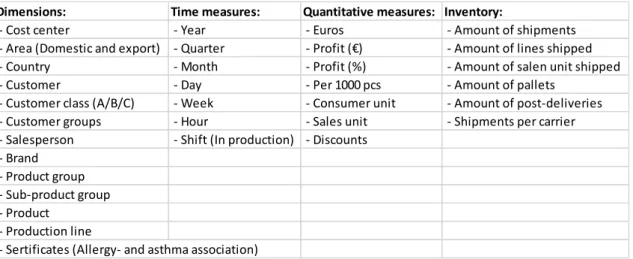

Mistä osa-aluiesta haluaisit saada raportointia? (Asiakkaat, tuotteet jne.)

Missä muodossa haluaisit vastaanottaa tai tulkita raportteja?

Haluaisitko mielummin saada aina saman raporttipaketin vai tuottaa raportteja itse?