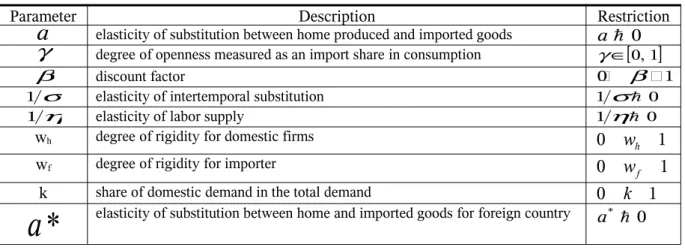

This article examines desirable monetary policy rules for a small open transition economy like Armenia, with a high degree of dollarization and huge remittances from abroad. One of the ongoing research issues in central banks is the transmission of monetary policy. In this article, we develop a small open economy model with remittances, which depicts economic developments in Armenia and can serve for implementing and analyzing monetary policy.

Impulse response and model in-sample simulation results show that the introduction of real remittance gap brings added value to the model properties. While the standard shocks in the model create responses of main macroeconomic variables similar to the standard New Keynesian models, none of them are similar to the recent economic developments in Armenia.

Introduction

To calibrate the coefficient of remittances in aggregate demand, we rely on the share of remittances in GDP. The derivation of the main equations of the model from the micro fundamentals allows us to derive the parameters of the model from the empirically probable ones. First, we estimated the structural shocks of the model (the difference between the actual variables and the variables produced in the model given the actual realization of the exogenous variables in the sample).

For our analysis, we use a simple rule that specifies the response of interest rates as a function of a few macroeconomic variables. Sensitivity analysis is used by varying the structural parameters of aggregate demand and supply to verify the robustness of the results.

Literature review

The model's structure of these works is based on the description of the transmission mechanism for small open economies proposed by Laxton and Scott (2001). These are the gap models, which are based on the premise of the monetary cycle theory and differ from each other only by calibrated parameters. They compare conventional optimal monetary policy under commitment and discretion and the variations of the simple fixed MPRs for Thailand.

Vasicek and Musil (2006) take the model of Liu (2006) and apply it to conditions in the Czech Republic. In their model, consumption contains a habit-forming factor, and the model's parameters are estimated by Bayesian method with Monte-Carlo simulation technique.

A Small Open Economy Model

- Household

- Inflation, real exchange rate and terms of trade

- Uncovered interest rate parity

- International risk sharing

- Firms

- Price setting behavior

- Equilibrium

- Demand Block

- Supply Block

- Aggregate demand and output

- Marginal cost and inflation dynamics

- Foreign variables

- Monetary policy

- Model solution

Where Pjth and Pjtf denote the prices of domestic and foreign goods j respectively, Dt+1 is the nominal payoff in period t+1 of the portfolio held at the end of period t (and which includes shares in companies), Wt. We assume that a representative household in the rest of the world faces the same optimization problem with identical preferences. In this section, we summarize linearized equilibrium aggregate supply and demand blocks of the model in terms of variables that deviate from flexible price levels.

This representation of the model will serve us for the analysis of monetary policy with different types of shocks. Therefore, in our analysis we focus on the practical aspects of rule implementation and the use of optimal simple rule, which specifies the response of the interest rate as a function of some macroeconomic variables.

Calibrating the model and model property

- Stylized facts on long-term trends

- Calibration

- Impulse Responses

- Verification of model calibration

Each temporary innovation of the model is shocked by an unexpected change of one percentage point in the first period of the simulation. The increase in the relative productivity of the domestic economy tends to narrow the output gap and put downward pressure on domestic inflation. Monetary policy increases interest rates in response to rising inflation, causing the real exchange rate to rise.

As a result of this substitution process, the demand for imported goods increases, causing the nominal exchange rate to depreciate. Monetary authorities raise interest rates as a reaction to an output gap shock that causes real and nominal exchange rate appreciation. An increased real interest gap and a reduced TOT gap reduce aggregate demand and close the output gap.

Following a domestic monetary policy shock, the domestic nominal interest rate shows an immediate increase, widening the real interest rate gap and generating exchange rate appreciation. The monetary authority responds to this situation by raising the policy interest rate, which contributes to the formation of a negative output gap and appreciation of the real exchange rate. Monetary policy responds to the higher inflation and output gap by increasing the policy rate, which reduces aggregate demand and generates exchange rate appreciation.

A positive real exchange rate shock causes the nominal exchange rate to rise, creating a positive LOP gap and TOT gap. The risk premium shock impacts the economy through the real exchange rate and the equilibrium level of real interest rates in the longer run. The model explains the nominal exchange rate through the expected exchange rate and the nominal interest rate difference between the country and abroad, supplemented with a risk premium.

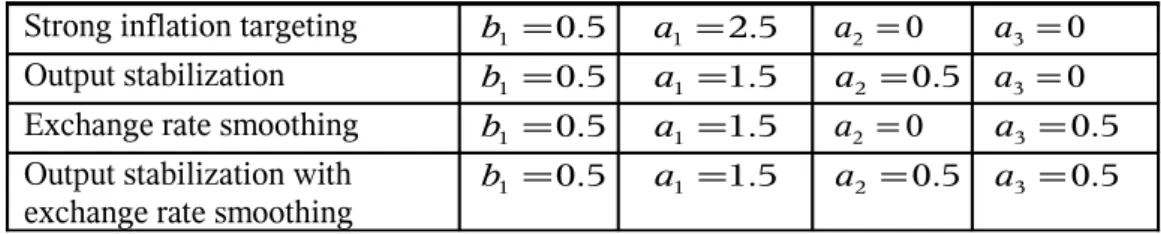

Optimal simple monetary policy rule

Given the relatively small data set available, we choose to run VAR with only three variables: output gap, inflation and real exchange gap. Considering that the exchange rate channel is much stronger than the interest rate channel in Armenia, we finally choose to use the real exchange rate. For all types of rules, we set the interest rate smoothing parameter to 0.5 to reflect the CBA's willingness to keep the policy rate smoother due to a less developed financial system.

For each simulation, we compare the performance of alternative policy rules using variability for key macroeconomic variables and the value of the loss function. These shocks are; the financial shock to the unhedged interest rate, the real shock to domestic productivity, the real shock to foreign output, the real shock to domestic demand and the real shock to remittances. The results of the simulations with all shocks show that the lowest value of the loss function was achieved with the strong inflation targeting (SIT) rule.

Indeed, as the tables show, the stronger inflation targeting rule leads to lower standard deviations of both the inflation rate and output gap, but generates the highest variation for exchange rate and LOP gap. Considering this fact, we believe that the rule for the Armenian economy is more desirable. ERS rule has relatively low value of loss function and less variability in exchange rate and LOP gap compared to SIT rule.

We should mention that the results also depend on the weights of the loss function. In this paper, we do not analyze the impact of different weights on the performance of interest rules, which could be an interesting topic for further research. From the table, we can see that for a certain level of interest rate equalization, the minimum value of the loss function is achieved with the following numerical parameters of the ERS rule:

Sensitivity Analysis

Changes in degree of rigidity

According to the theoretical constraint, the degree of rigidity can be between zero and one. According to our calibration result, it is equal to 0.66, assuming that companies keep prices unchanged for three quarters. We analyze the performance of difference MPRs both with higher and lower degrees of rigidity compared to the calibrated value.

We choose 0.85 as a higher degree of rigidity, which assumes that prices adjust after one and a half years. For a lower value of degree of rigidity, we choose 0.35, which means that firms change their prices every quarter and a half. The performance of MPRs with a higher degree of rigidity did not change significantly compared to the baseline scenario.

The SIT rule guarantees the lowest value of the loss function, but generates greater variability in exchange rate and LOP gap behavior. The exchange rate smoothing rule has a relatively low loss function value and less variability in the exchange rate and LOP gap compared to the SIT rule. Since Armenia is a small open economy and assuming that prices are more flexible, the effect of shocks, especially external shocks, on the exchange rate will be greater.

Changes in private sector behavior

The performance results of the lower MPRs show the same picture as in the case with the baseline calibration.

Conclusion and Policy recommendations

Source: National Statistical Service of Armenia, Central Bank of Armenia, authors' estimates Relative share of expenditure in GDP. A quasi-rational model of the business cycle with wage and price inertia, Quarterly Journal of Economics. Linde (2005), Firm-specific capital, nominal rigidities and the business cycle, Federal Reserve Bank of Chicago Working Paper, 1.

Benigno (2002), Implementing Monetary Cooperation Though Inflation Targeting, CEPR Discussion Paper The Federal Funds Rate and the Channels of Monetary Transmission, American Economic Review, 82:4, pp. 1997), Systematic Monetary Policy and the Effects of Oil Price Shocks, Brookings Pap. September 1987), Monopolistic Competition and the Effect of Aggregate Demand, American Economic Review Price Asynchrony and Price Level Inertia, MIT Press. Evans (1998), Monetary Policy Shocks: What Have We Learned and to What Purpose?, NBER Working Paper 6400.

Evans (2001), Nominal Rigidities and the Dynamic Effects of a Monetary Policy Shock, NBER Working Paper Monetary Policy in a Small Emerging Economy: Exploring Desirable Interest Rate Rules. Gertler (2001), Optimal Monetary Policy in Open Versus Closed Economies: An Integrated Approach, American Economic Review. Stiglitz (1977), Monopolistic Competition and Optimal Product Diversity, American Economic Review. 2000), Habit Formation in Consumption and Its Implications for Monetary Policy Models, American Economic Review.

2001), Sticky-Price Models of the Business Cycle: Specification and Stability, Journal of Monetary Economics The Exchange Rate in a Dynamic-Optimizing Business Cycle Model with Nominal Rigidities, Journal of International Economics. Zha (1996), What Does Monetary Policy Do?, Brookings Papers on Economic Activity, 2, pp. 2006), A Small New Keynesian Model of the New Zealand Economy, Reserve Bank of New Zealand. Mei 1985), kleine menukosten en grote bedrijfscycli: een macro-economisch model van monopolie, Quarterly Journal of Economics.

Nelson (1999), An Optimizing IS-LM Specification for Monetary Policy and Business Cycle Analysis, Journal of Money, Credit and Banking. Nelson (2000), Monetary policy for an open economy: an alternative framework with optimizing agents and sticky prices, Oxford Review of Economic Policy, 16, 74-91.