The following patterns determine the importance of the research: .. volumes of M&A deals in the oil and gas industry are expected to increase in the near future due to: 1) economic changes making it tighter to keep profit margins at levels previous; . The first chapter will provide a literature review with a focus on the M&A performance relationship, the value chain and trends of the oil and gas industry, and the drivers of M&A within the industry. Further, in the fourth chapter, the results of the empirical study will be presented and discussed.

At the end, conclusions will be given and the practical contribution of the study will be explained. The findings showed that mergers and acquisitions increased shareholder value and corporate profitability. The study aimed to determine the effects of mergers and acquisitions on the performance of the acquiring and controlled companies.

Oil and gas companies operating in all the mentioned sectors are called integrated. The financial performance of the companies in this industry depends to a large extent on the spot oil prices and thus reflects its fluctuations in the market. Taxation is traditionally one of the most critical considerations mentioned in the literature (eg World Bank, 2010, Mitchell, 2012).

THEORETICAL FRAMEWORK AND HYPOTHESES

For example, Homberg et al. 2009) investigated a number of mergers and acquisitions and concluded that in order to realize the planned synergies, it is necessary for the acquirer to be larger than the target company, but the latter must be closer to the acquirer in terms of absolute and relative size . Moreover, one of the assumptions of the q-theory states that as the target size increases, so do the potential synergy gains. The effect is so because the higher value the target company represents, the easier and faster the acquirer can achieve financial advantages compared to other competitors in the market (Lucas, 1978).

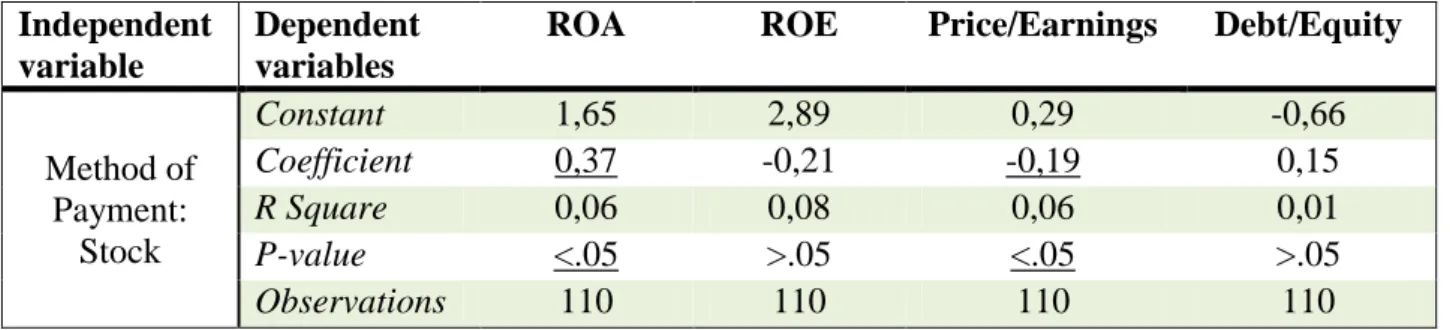

Moreover, since the size of the target company is mainly associated with effects on outputs and variable costs of the company, we exclude the solvency measures from this analysis. Shleier's and Vishny's argue that in the long run the market makes corrections to the acquirers' stock which leads to negative long-term returns for the acquirers. Hypothesis 2a: Transactions where inventory is used as a method of payment are positively associated with the acquirer's ROA ratio.

Hypothesis 2b: Transactions where inventory is used as a method of payment are positively associated with the acquirer's ROE ratio. Hypothesis 2c: Transactions where inventory is used as a method of payment are positively associated with the acquirer's P/E ratio. Hypothesis 2d: Transactions where inventory is used as a method of payment are negatively associated with the acquirer's D/E ratio.

Control by the parent company means better applicability of new management rules and processes. These processes can directly affect the performance of the combined company and therefore the parent company may be interested in establishing a higher level of control in the company it has acquired. Such control is achieved when the acquirer's management has the majority of voting rights in making strategic decisions.

Therefore, the purchase of a larger share can be considered as a way of improving the influence of the parent company and thus the resulting performance. In the next chapter, we continue with the research methodology and the selection of variables for our model.

RESEARCH METHODOLOGY

31 on the country, to avoid biased interpretations of the results, countries with narrow economic positions were selected. The choice of the statistical model for the given research is based on the analysis of previous studies and refers to the methods applied by the authors in papers on similar problems. The given equation is further adjusted according to specific parameters selected for each of the financial indicators.

For the purposes of the research, the testing of the independent variables will be carried out by both including all the variables in a multiple regression model (except for dummy variables that divide the sample into two groups each) and, in the case where the combination of specific variables would be incompatible and lead to insignificance of the overall model (leaving only one or more variables significant), the effects of the independent variables on the financial indicators will be tested in separate regression models. The identification of appropriate financial measures for dependent variables is essential for the correct testing of the proposed hypotheses. In the case of full acquisitions and mergers, companies start to prepare consolidated financial reports where the results of the acquired company are already included.

For example, if we test our hypothesis that the size of the target firm can affect the acquirer's post-deal profitability indicators, we would get the most likely result that it did only because the total size increased. Return on assets is one of the important profitability indicators and measures in terms of the ratio between assets and net profit. Another interpretation of the P/E ratio is a reflection of the market's optimism about the company's growth potential (Kaplan, 2012).

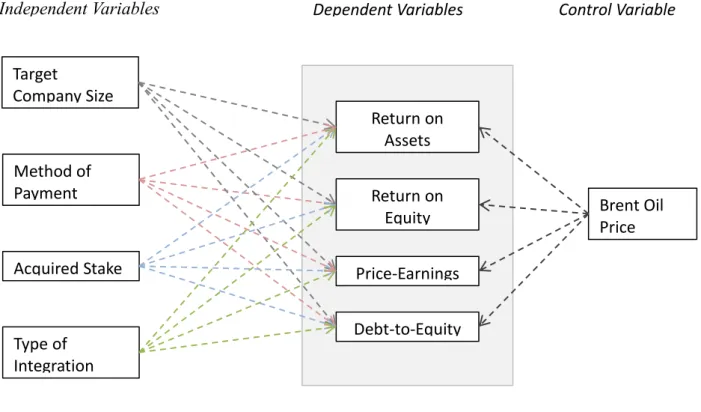

The variables were selected according to the purpose of the research, that is, with a focus on characteristics related to the agreement and within the limitations of the data available for the research. The size of the target company will be measured not in absolute terms but in relative terms. As a measure for the size of the companies, their capitalization figures before the agreement will be used.

For the variable representing the size of the stake purchased, we will use the percentage values obtained from the Zephyr database. Therefore, if the operating subtype of a buying company is the same as that of the target company, the transaction will be considered a horizontal transaction.

RESULTS AND DISCUSSION

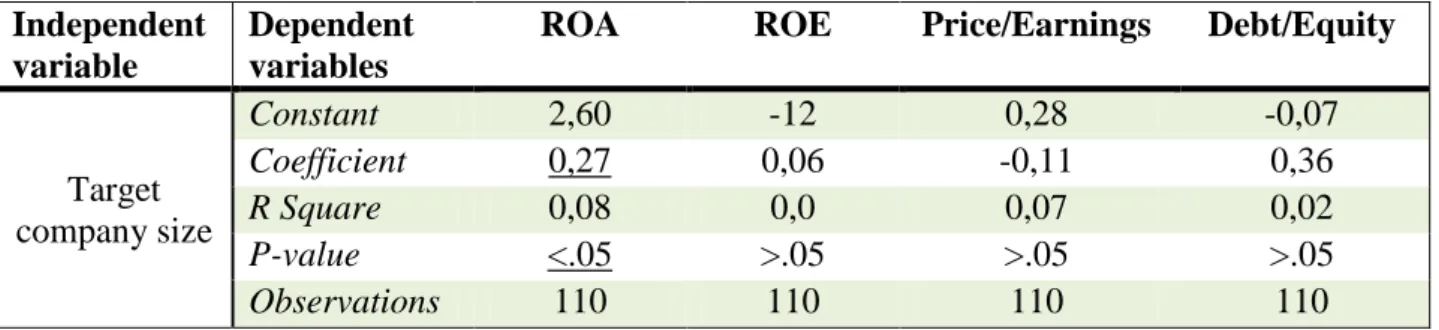

The primary focus in discussing the results below will be on the statistically significant associations, but the hypotheses that were not significant will also be considered. With regard to the predictive relationship between the size of the companies that acquirers buy or invest in and the performance of the following companies, the positive result was identified for the changes in the ROA ratio. There are several possible explanations as to why the relative size of the target may, albeit to a limited extent, cause the increase in the return on assets ratio of the acquiring company.

Therefore, one of the reasons for the increase in the efficiency achieved may be economies of scale. Regarding the effect of the company size on the ROE ratio, contrary to the theoretical expectations (Bruner, 2004; Ismail et al., 2011), the outcome effect showed insignificant. The size of the target company as an explanatory variable also did not hold within the 95%.

Since the P/E ratio is a market ratio, it represents the reaction of investors to the news of the M&A deal. So, one of the explanations of the negative result could be that in the case of M&A deals the prices in the P/E ratio have already reacted. When this happens, the value of the company's assets, especially its shares, decreases proportionally.

As a result, the decrease in the asset part of the ROA ratio raises it to a higher value. Contrary to theoretical expectations, the effects of financing method on ROE and D/E ratios were not found to be significant at the 95% confidence level. The degree of corporate control, reflected in the size of the stake acquired, is hypothesized to be positively related to and influence subsequent financial performance (e.g. Rani et al., 2015).

To support this idea, the selected control variable representing global economic changes was significantly and positively related to the changes in most of the models. Returns to scale may be greater depending on the size of the company as well as the ability of the target company to manage its costs.

CONCLUSION

34;Integrating Relative Position and Market Discipline: A Complexity Theory Perspective of Post-Merger Executive Initiation." performance toward mergers and acquisitions." Review of Financial and Accounting Studies. 34; METHODOLOGIES USED FOR DETERMINING THE PERFORMANCE OF WRITINGS AND PURCHASES." Academy of Accounting and Financial Studies Magazine 16, no.

34;Financial synergies and optimal firm size: Implications for mergers, spinoffs and structured finance." The Journal of Finance 62, no. 34;An Examination of Success of Mergers and Acquisitions in Manufacturing Sector in India Using Index Score. 34; Vertical integration and profitability in the oil industry." Journal of Economic Behavior & Organization 2, no.

34;The Impact of Mergers and Acquisitions on the Performance of the Greek Banking Sector: An Event Study Approach." International Journal of Economics and Finance 3, no. 34;Chief Strategy Officers: Contingency Analysis of Their Presence in Top Management Teams." Strategic Management Journal 35, no. 34;The Impact of Mergers and Acquisitions on the Financial Performance of West African Banks: A Case Study of Some Selected Commercial Banks." International Journal of Education and Research 2, no.

34;Mergers And Acquisition and Firm Performance: Evidence from the Ghana Stock Exchange." Research Journal of Finance and Accounting 4, no. 34;Financial Performance Analysis of Mergers and Acquisitions: Evidence from India." International Journal of Business and Management 25, no. The Trade-offs for Buyers and Sellers in Mergers and Acquisitions." Harvard Business Review 77, no.

34;Acquisition performance unbundling: how are they performing and how can it be measured?" Handbook of Mergers and Acquisitions, Oxford University Press, Oxford UK (2012a). 34;The Effect of Mergers on Bank Performance: Evidence From Bank Consolidation Policy In Indonesia." In International Business Research Conference.

APPENDICES

Financial performance indicators

Academic research on M&A-Performance relationship (Extract)

Statistical model results Target company size and ROA ratio Target company size and ROA ratio.

Statistical model outputs Size of the target company and ROA ratio Size of the target company and ROA ratio