In the result, the practical recommendations for managers of the PolySeed project were developed and the implementation of real option analysis and its benefits were illustrated. The investment analysis of young firms and especially technological enterprises is one of the most complicated questions in the literature devoted to the investment practices. In this paper, the ROA technique is implemented for investment analysis of the relevant biotechnological project to give recommendations for managers of the relevant investment fund.

LITERATURE REVIEW

Investment analysis of technological projects

- Valuation methods of technological investments

- Stages of new project development

- Risks of a technological project

Typically, three scenarios are used: the "best guess" (most likely, media attack); the "best case" (optimistic) and the "worst case" (pessimistic). At this stage, the operating history of the company can already be used in the valuation. The options of the company are to continue to the next phase or to extend the financing.

Real options for investment analysis of technological projects

- Concept of Real Options

- The Real Options Process

- Real options in technological sphere

- Common types of Real Options in the technological sphere

- Real options in biotechnological sphere

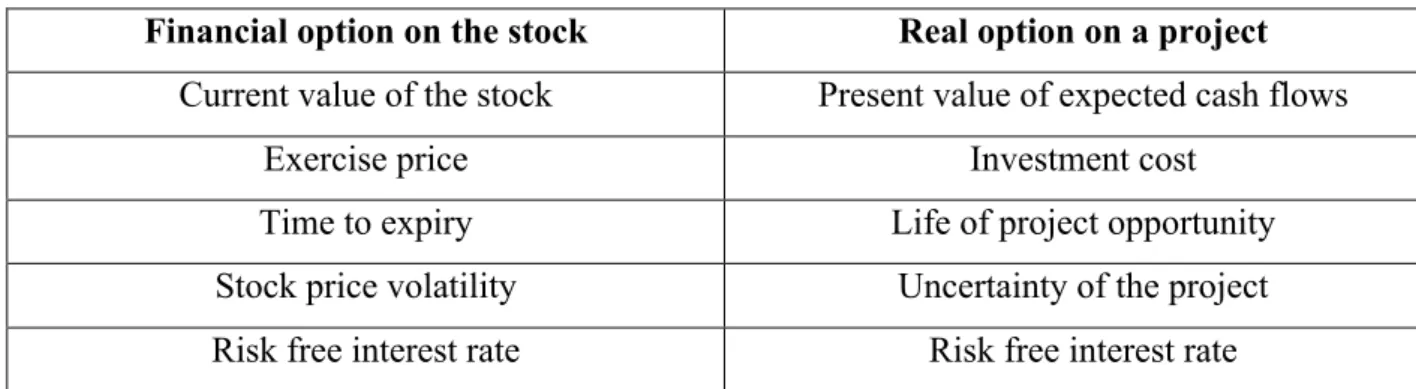

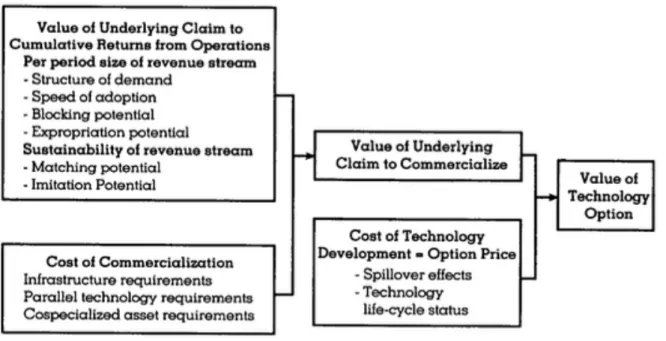

There are different approaches in the literature to illustrate the implementation of real options analysis. In ROA, the underlying asset is assumed to be the project's future profitability, which is a series of future cash flows. The implied volatility of future cash flows or other fixed assets can be calculated using the results of a Monte Carlo simulation.

This makes it possible to value all assets in the market regardless of the different individual risk preferences. All analytical methods are mostly modifications of the Black-Scholes model, which is described below. The value of an option to defer can be denoted as max(V – I, 0), where I is the initial investment and V is the present value of the project's cash flows.

The option to expand can be interpreted as an American appeal to the value of the additional production. It is also important that the method makes it possible to estimate the market value of the project, and not a subjective or private value. The idea for the growth option is that being involved in the development of the project is similar to buying a call option on the value of the next project.

In the given model, each step of the development process is described as a European call option.

METHODOLOGY

Strategic analysis

Therefore, each phase is an option that is conditional on the previous exercise of other options. If the project is a technical success, then it creates the opportunity to make a significantly larger investment in the continuing project with a relatively higher expected net return. If the project does not achieve the technical success, there is no need to allocate additional resources and therefore downside risk is limited to the initial investment costs in the R&D phase.

It is also important to mention that if a stage of the R&D process was not successful, managers have the option to postpone the project to improve the original product so that it can pass through that stage. At the beginning of the strategic analysis, it is useful to build the project's decision tree that will contain the most important milestones. The weighted average value of the project that will be obtained after decision tree analysis is a good proxy for investment analysis.

However, one should not forget that the decision tree does not evaluate the entire range of possibilities for the project.

Risk analysis

- Technological uncertainties

- Commercialization uncertainties

The first phase of clinical trials are the first studies in humans, which aim to find the optimal dose for the components of the drug. The given studies are intended to indicate tolerance, safety and presence of the therapeutic effect on the healthy body. These studies aim to determine the difference between the product and other drugs on the market in a particular niche and hidden risk factors not covered during the previous studies.

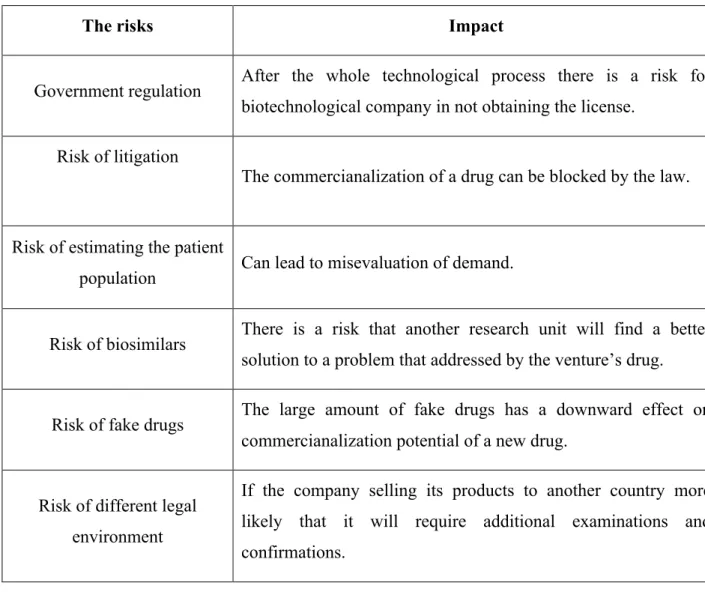

The probability of failure can be obtained using the Delphi method, an anonymous survey among the experts working on the project and on the projects with similar characteristics. The data can be obtained from the website of the Association of Clinical Trials Organizations (ACTO) which publishes figures annually for the duration of the clinical trial. These uncertainties depend not only on the company's stage of development and experience, but also on the types of drugs being developed.

Risk of biosimilars There is a risk that another research unit will find a better solution to a problem addressed by the company's drug. There is always the uncertainty that another research unit will find a better solution to a problem addressed by the company's drug. Ernst & Young noted that counterfeit drugs accounted for approximately 10 percent of the world's pharmaceutical product supply as of 2008.

Hanse, there is an additional risk of not obtaining the license and that the procedure of passing the clinical trials will be temporary.

Quantitative analysis

- DCF valuation

- Decision tree analysis

- Real options analysis

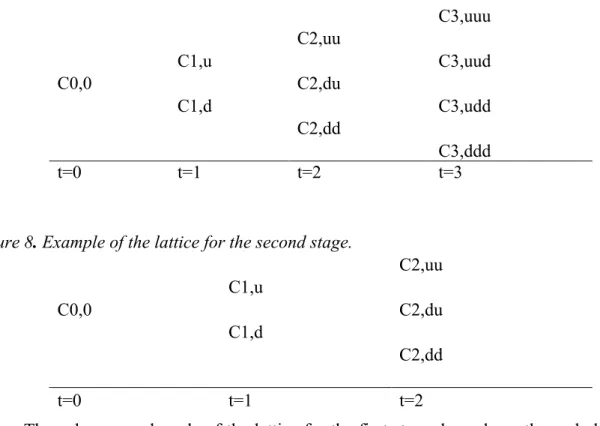

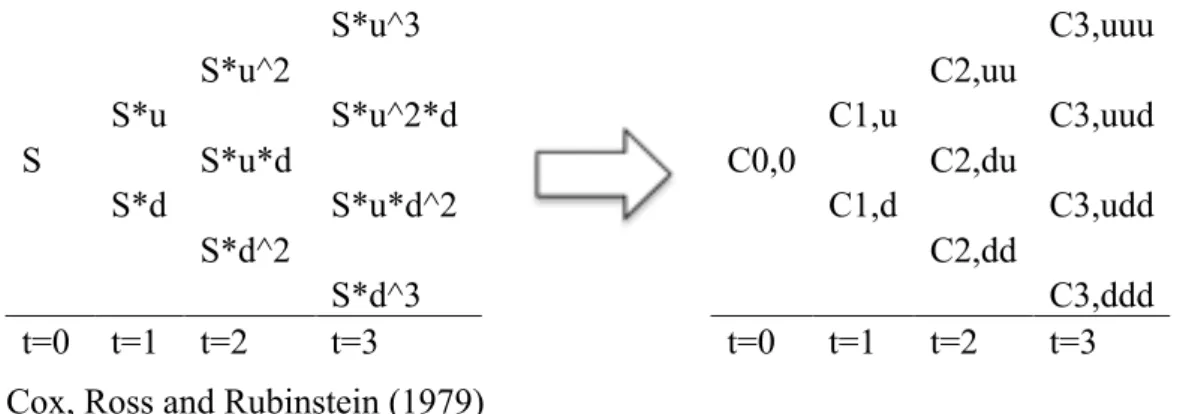

Normally, a constant discount rate is applied to find value of the project using the decision tree method (Steffens, 2007). The first step of the binomial model is to form evolution grid of the underlying asset. At the end of the first phase, the result is the value of the underlying asset at any period.

Following Kellog et al. 2000, this study estimates volatility using formula 8. 8) Where l is the time period, h is the maximum value for the project cash flows, A is the value of the underlying asset. The idea is that we want the value of the project to grow from A to the maximum value of h after l time intervals. For example, after the first month, the value of the project may increase or decrease by 10%, and so on.

To determine the value of the project, the value of several successive European options must be found. The value at each grid node for the first level depends on the underlying asset, and the values of the second grid depend on the value from the previous level. The decision tree approach is an alternative method for determining the value of a technology project.

For example, in the case of biotechnology development, the value of the first phase depends on the success of the next phase.

CASE STUDY

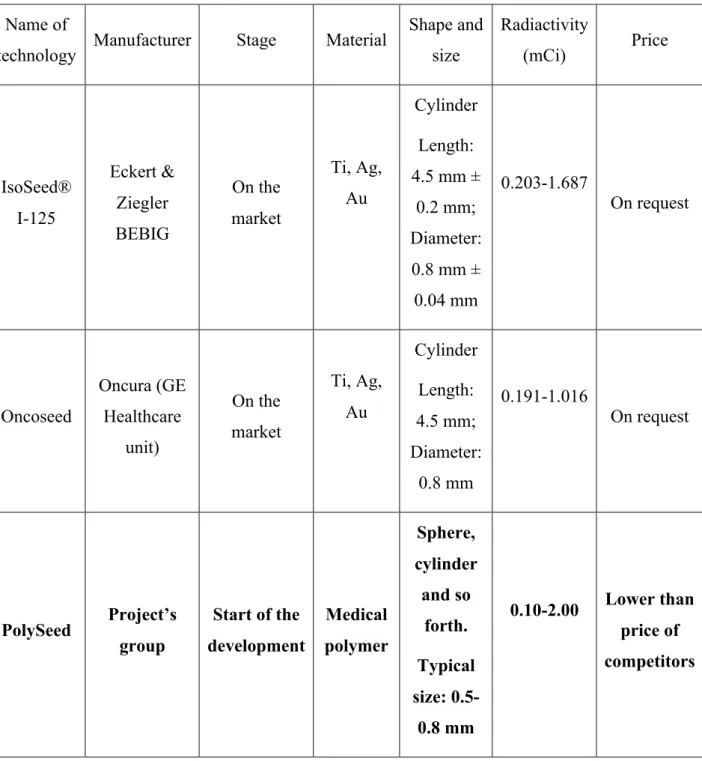

Description of the project

- Market of brachytherapy

World medical statistics testify to the annual increase in the number of new cancer cases worldwide - about 13 million. Over the past decade, the number of men diagnosed each year with prostate cancer has increased by an average of 7.6%. The absolute number of newly diagnosed prostate cancer has increased since 2001, more than 2 times: from 12.8 thousand to 28.6 thousand cases of the time.

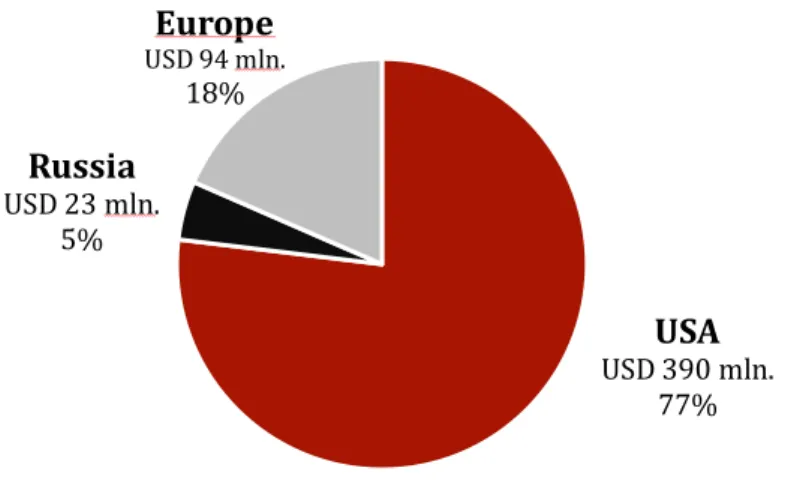

The HDR brachytherapy method has become a primary therapy to be used for the treatment of localized malignant tumors in distant organs such as the prostate, esophagus, stomach, pancreas, kidney, bladder, uterus, trachea, bronchi and lungs. In the total amount of newly diagnosed cancers, there are more than 40% that can be cured by low-dose brachytherapy. Today, the capacity of the Russian market for HDR brachytherapy is estimated at about 3 thousand microsources per year, in Europe 12 thousand in the USA -50 thousand.

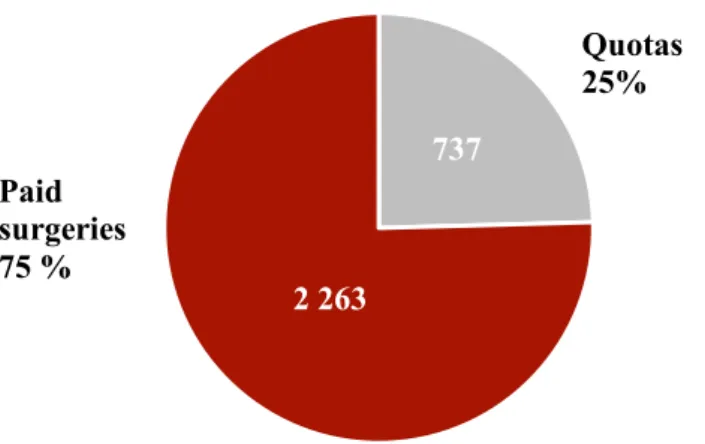

At the selling price of micro resources in USD 130, the entire market is estimated at USD 507 million. In Russia, the state allocates quotas for operations: in 2013, the number of quotas for low-dose brachytherapy was 737, which is 100 quotas more than in 2012. According to the Association of Russian Brachytherapists, there are 17 medical centers in our country that have brachytherapy services with leading clinics.

Investment analysis of the project

- Strategic analysis of the PolySeed project

- Risk analysis of the PolySeed project

- DCF valuation of the PolySeed project

- Decision tree analysis of the PolySeed project

- Real options analysis of the PolySeed project

Phases of the PolySeed project Phase Duration (month) Cost (in thousand rubles) Probabilities Research of. Nevertheless, the main objective of the project is the sale of patent rights to international companies. The discounted cash flow analysis shows that the present value of the project is slightly above zero.

The decision tree method was used to estimate the expected net present value of the project. It estimates the value of the option to abandon the project in case of technology. The volatility of the project's cash flow was estimated using the formula presented in the second chapter where h is 60 million rubles - the maximum amount of money that the project can receive, l is.

The option price for the first option reflects the flexibility value of the entire project. The extended value of the project according to the ROA approach is the value of the sequential compound option, i.e. the real options approach allows obtaining the value of the enterprise at each stage of R&D development.

The value of the option shows the maximum amount that investors can spend at the beginning of the phase.

Discussion

In this research, the real options model was implemented for valuation of the project in biotechnology industry. The decision tree approach allows building a consistent framework for the project and should be used as the first stage of real options. At that point, it is important to say about the limitations of the sequential compound model for valuing real options.

The aim of given research was to make recommendations on improving the investment analysis process of biotechnological projects by applying the methodology of real options. The second part of the first chapter is devoted to the literature review of the real options concept and its applicability in the technological and biotechnological sphere. The second chapter is devoted to the formulation of the methodology for the investment analysis of the biotech startups.

To conduct the real option analysis of the biotechnology enterprise, the sequential composite rainbow option model was implemented. It also provides the strategic framework of the project's value, which is a useful tool in decision-making. The implementation of the real options tool and its benefits were illustrated by the example.

Methods of risk assessment and management: Using the concept of real options to evaluate real estate investment projects.

DCF valuation

Decision tree of the PolySeed project

Evolution of the underlying asset of the PolySeed project

The binomial lattices of the forth and the fifth stages

The binomial lattices of the first and the second stages

Strategic lattice for the PolySeed project