Thesis title The relationship between the level of debt and earnings management of Russian companies. The main research objective is to determine the relationship between the level of debt and earnings management in the Russian companies. These different conclusions about the relationship between debt levels and earnings management can be explained.

The main objective of the research is to determine the relationship between debt level and profit management in Russian companies.

Concept of Earnings Management

Neutral profits are the result of neutral business operations, and finally, aggressive methods, such as understating provisions and inventories and deferring research and development or advertising expenses, are used in aggressive accounting. Accrual earnings management and real earnings management are two techniques that can be used to manipulate earnings. Discretionary accruals are non-mandatory in nature and are based only on the manager's choice, while non-discretionary accruals are mandatory in nature because they are derived from ordinary business transactions or previous accounting transactions.

As a result, discretionary accruals are used as an earnings management tool and are used as a benchmark for earnings management (Mangala, 2017).

Motives for earnings management

Political costs are high because of the profitability of the firm that can attract media and consumer attention (Moses, 1997). The bonus plan hypothesis suggests that in order to get the bonus, managers will choose accounting procedures that allow future earnings to be transferred to the current period (Wiratama, 2020). Another motive for companies to use earnings management is to meet the expectations of stock market analysts.

They can also carry over income in the current period to the next, as no further bonuses are paid after this (Holthausen, 1995).

Background of the research

In the article by Safa Lazzem and Faouzi Jilani (2018), they examined the role of increasing leverage at the level of accrual earnings management in France. After empirically analyzing the impact of leverage on earnings management, they found that leverage has a positive effect on earnings management. There are also a number of previous studies that have found no relationship between capital structure and the earnings management phenomenon.

The table below summarizes the results of the most relevant previous research on the relationship between the level of debt and the phenomenon of earnings management.

Hypothesis development

Using a sample of data from 33 countries over a 10-year period, they found that short-term debt spurs greater earnings management. This impact of short-term debt is particularly strong in countries with weak legal regimes (Gupta, 2008). The researchers found that this relationship is strongest when new financing occurs in the presence of greater refinancing pressure (i.e., positive changes in short-term debt).

On the other hand, the role of short-term debt monitoring has been highlighted by Datta et al.

Earning management measure

These models are discussed in the article to compare the results of the main model based on the results obtained. The most common and one of the basic models now used to identify discretionary accruals is the Jones model. The Jones model reflects the relationship between the company's accruals and the main indicators of its business performance.

𝑅𝐸𝑉t = Income in year 𝑡 minus income in year 𝑡 − 1, 𝑃𝑃𝐸t = Gross property plant and equipment in year 𝑡, 𝛼1, 𝛼2, and 𝛼2, and alpha 3 = Resuël estimated in year, viz. 𝑡. In the empirical part of the paper, I use a modified version of the Jones model as my main model, as it is considered one of the most reliable and widely used. The amendment is supposed to eliminate the assumed tendency of the Jones model to measure discretionary accruals with errors in the exercise of discretionary power over income.

The only adjustment to the original Jones model is that the change in income is adjusted for the change in receivables in the event period. The modified version of the Jones model implicitly assumes that all changes in loan sales in the event period are the result of revenue management. 𝐷𝐶𝐿t = Change in short-term debt included in current liabilities in year 𝑡, 𝐷𝐸𝑃t = Depreciation and amortization expense in year 𝑡.

𝑅𝐸𝐶t = Net receivables in year 𝑡 minus net receivables in year 𝑡 − 1, 𝑃𝑃𝐸t = Gross tangible fixed assets in year 𝑡,. In general, this model is considered additional, the most important calculations will be performed by the modified Jones model.

Summary

EMPIRICAL STUDY OF THE RALATIONSHIP BETWEEN THE

Research Methodology

- Data collection

- Data description

- Empirical model and variables

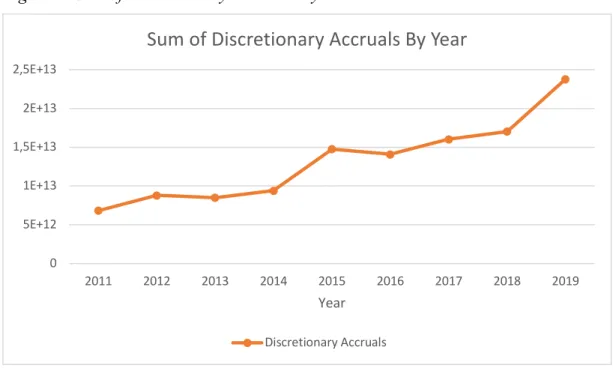

Empirical investigation of the relationship between debt level and earnings management of Russian companies. There are 39 companies from the Production of industrial goods and services, which is 23% of the sample, and 35 companies from the Production and distribution of electricity, gas and water (20%). The third sector is the extraction and production of basic resources. This includes 25 companies and represents 14% of the sample.

Chemical industry represents 11% of the data and includes 19 companies, while Extraction of oil and gas occupies 8% and consists of 14 companies. Property and production of personal and household goods are only represented in one company and take up less than 1% of the data set. The following graph shows the distribution of the amount of short-term debt, long-term debt and total debt by sum.

Regression will be used to identify the relationship between the independent variables of the base model and earnings management. To test the hypothesis on the nature of the relationship between the level of debt and the absolute value of discretionary accruals as a proxy for earnings management, it is necessary to estimate panel regression models, where total debt, short-term debt and long-term debt are exchanged. to see the difference between earnings management dependence on them. STD is a measure of short-term debt utilization and is calculated as debt to current liabilities divided by total assets.

According to Dechow (1994), discretionary accruals often provide managers with the ability to manipulate earnings because of the flexibility they have. They are calculated by identifying the non-discretionary accruals as part of the total accrual.

Results

- Descriptive statistics

- Regression results

- Additional tests

The multiple R-squared of the model is 0.3581 and the adjusted R-squared is equal to 0.3311, which means that about 33% of the variability in earnings management is explained by the selected independent variables. The results obtained after testing the first hypothesis show that total debt has a significant positive impact on accrual earnings management activities, meaning that as debt increases, managers are more involved in AEM. The multiple R-squared of the model is 0.3232 and the adjusted R-squared is equal to 0.3204, which means that about 32% of the variability in earnings management is explained by the independent variables in the model.

Results obtained after testing the second hypothesis show that short-term debt also has a significant impact on accrual earnings management activities, which means we can accept the second hypothesis. Multiple R-square of the model is 0.3212 and adjusted R-square is equal to 0.3183, which means that approx. 32% of the Earnings Management variability is explained by the independent variables in the model. Results obtained after testing hypothesis number three show that the level of long-term debt has no significant positive impact on accrual earnings management activities.

And as expected, the value is negative, meaning that larger companies have less incentive to engage in earnings management. Regarding the variable value of interest expense (INTEXP), the results show that the cost of debt has no significant effect on earnings management. These results show that interest expense has no effect on the earnings management practices of the companies studied.

Research on the earnings management behavior of failed firms has evolved greatly over the past decade. Knowledge about the behavior of earnings management in periods leading to bankruptcy is important for all stakeholders. They also discuss the utility of knowledge of earnings management behavior for bankruptcy prediction models.

In other studies, however, earnings management is estimated downward prior to the bankruptcy event (Dutzi, 2016).

Summary

The personal use and consumption sub-model is largely consistent with our baseline model. One unit increase in total debt would result in a 0.21 increase in earnings management, so we can conclude that industries in this subsample are more prone to manipulate their earnings with respect to debt than other industries. This model also has a large growth in sales and interest, which is not consistent with the basic models.

So, for this subset, growing firms manipulate their earnings in order to obtain even greater financing and further fuel their growth.

Managerial implications

Limitations of the study

The main objective of this study was to determine the relationship between level of debt and earnings management in the Russian market. The concept of earnings management was described, and the main motives on the basis of which managers resort to manipulation of earnings were dissected. Most studies have found a positive significant relationship between the level of debt and the level of earnings management.

Further in line with some research, this article separates total debt, short-term debt, long-term debt and their relationship with Earnings Management. According to the results, a significant correlation exists between the earnings management manipulation and the level of total debt and the level of short-term debt. While no significant correlation was found between the level of long-term debt and earnings management.

Furthermore, short-term debt creates an incentive for borrowers to delay recognizing bad news through earnings management. It is also the first report on Russian companies to address the relationship between debt levels and earnings management. Furthermore, the evidence presented in this study contributes to a relatively new area in the financial literature related to the impact of debt maturity structure on earnings management.

The impact of leverage on accrual earnings management: The case of French listed companies. The impact of corporate governance on the relationship between firm size and financial leverage on earnings management. Impact of Earnings Management on Capital Structure of Non-Financial Companies Listed on (KSE) Pakistan.

ASSESSMENT OF THE EFFECTS OF FIRM CHARACTERISTICS ON THE EARNINGS MANAGEMENT OF LISTED FIRMS IN NIGERIA.