The aim of the study is the development of the coordinating model of WCM in collaborative SCs. The theoretical relevance of the master's thesis is justified with the fulfillment of the research gap identified as a result of theoretical review of WC in SCs – the absence of works devoted to the coordinating model of WCM in collaborative SCs.

Theoretical review of financial supply chain

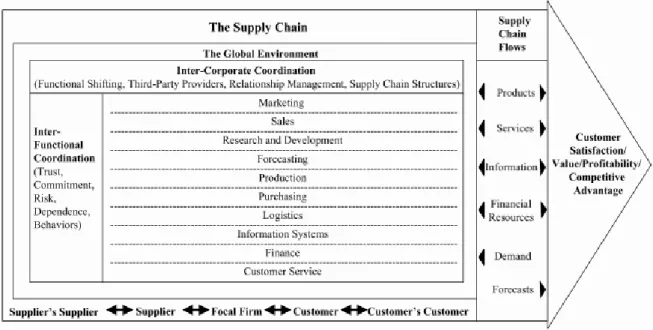

Collaboration in supply chains

Spekman et al., (1998) emphasize the fact that the initiation of SC management is at the stage of cooperation. Integration means that all SC participants are involved in the business processes of other participants.

Financial supply chain management (FSCM)

Commercial credit is one of the most frequently used tactics for short-term SC financing. Recently, reverse factoring has started to develop and is now one of the most common SC finance practices.

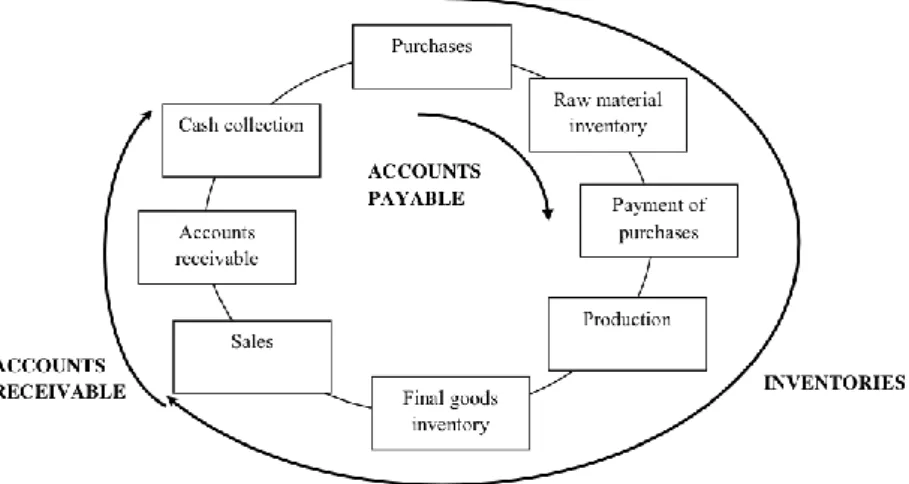

Working capital management as a FSCM perspective

This field includes the studies in empirical archival research – the case studies from different industries and countries, qualitative conceptual research – mainly focuses on CCC at all stages of collaboration in the field of SC and mathematical modeling. The operational approach to measure WC is the WC cycle time – the CCC approach is one of the main topics of this master thesis and its adaptation and optimization in collaborative SCs will be discussed in the following chapters.

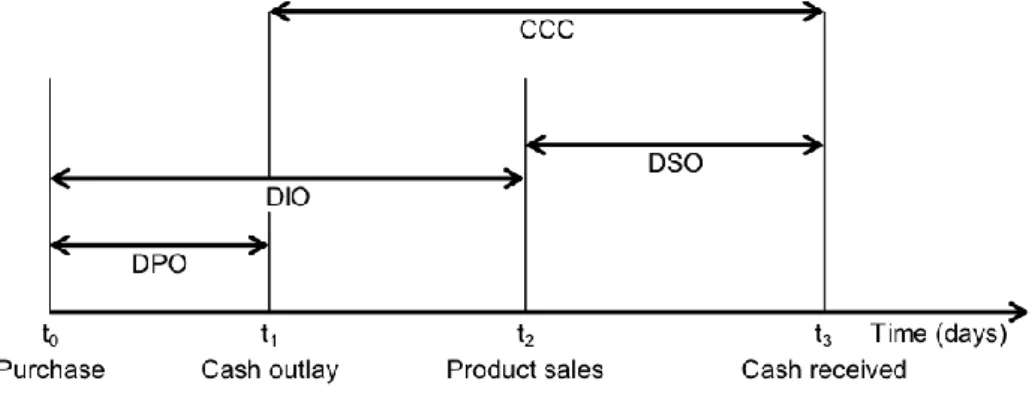

Cash conversion cycle (CCC) as a WC measure

Shin and Soenen (1998) developed the Net Trade Cycle (NTC) framework – in their equation all components of CCC should be sales percentages – but as long as all denominators are different – the change is not useful. Monto (2013) also notes that WCM has an interorganizational context due to the fact that the cycle times are the result of the decisions and not only of one central company. On the contrary, Hofmann and Kotzab (2010) argue that “the synchronization of the goods/material and financial (payment) flows within the SC is the key to reducing the net WC and increasing the value for the connected SC businesses".

1.4) Limitations of the cooperative approach of KKK include difficulties in sharing accounting information and the competition factor also occurs if the company operates with several suppliers and customers. The financial cycle time model allows estimating the costs of each stage of collaborative SC and Viskari et al. 2013) introduced the formula of financial costs. The new component of unpaid A/E days is added to the CCC calculation and is analogous to the other components.

The logic of the equation is that the other components of the CCC remain the same and the DAO is subtracted.

Coordinating modified collaborative cash conversion cycle model (mCCCC) methodology

The first – the modified scenario analysis proposed by Randall and Farris (2009) allows validation of the efficiency of using the DAO component in SC as Talonpoika et al. Each scenario describes the impact of each component on the overall changes of the mCCCC (2.1) and the total FC, which is the sum of the total financial costs of each member of a collaborating SC (2.31). The basic concept of GP is explained by Orumie and Ebong (2014) in their study: GP is “one of the oldest multi-criteria decision making techniques used in optimizing multiple objective goals by calculating the deviation for each of the objectives from the objective minimalize. desired goal”.

Feasible region - Figueira, Greco and Ehrgott (2005) it remains as "the set of solutions in the decision space that satisfy all constraints and sign restrictions in a goal programming from the feasible region. The problem formulation for this framework is the following – DM (in this case either or financial intermediary or consulting company) decided to minimize the objective function for the total financial cost – the total financial cost of the SC, which is the sum of the financial costs associated with each mCCC cycle of each participant in the 3-stage collaborative SC based on the cost criterion of using the DVs for collaborative mCCCC. 42 DM set constraints on operating cycle costs that no costs after f(z) optimization should exceed their pre-optimization values to meet the requirement to provide the centralized decision for decentralized supply chain. 2.6) The DM indicates the objectives to be achieved through cooperative actions – the value after specific percentage reduction of total inventory (TI) and total A/R (TAR) and the value after specific percentage increase of total A/P (TAP) ) and total accrued expenses ( TAE) for each member of a collaborative SC.

According to Taha (1971) "the variable is the component of deviating variables or representing the purpose of".

Data collection and industries studied

In addition, the mCCCC optimization model can be calculated using other programs such as MATLAB, TORA and others. The data collection process and the industries studied are discussed in the following sections of Chapter 2. 48 The author made adjustments to the data to ensure the applicability of the model – the data obtained from the financial reports of the members of the cooperative 3-stage SCs. each industry is assumed to be dedicated to each specific cooperative SC without involving other operations. This value is mostly due to the nature of the industry and the continuous dependence of customers on ICT services.

The main purpose of A/E in the ICT industry is the amount of money sufficient to finance the projects. The paper and publishing industry is closer to the end industry than the previous two industries, which are mainly focused on B2B business. Due to the fact that A/E in the form of annual subscriptions are very popular among customers, publishing collaborative SCs can achieve negative mCCCC.

However, the industry is interested in the fact that it was particularly hit by the economic crisis – the drop in oil resulted in lower real incomes and lower demand (McKinsey, 2011).

Research design

The author made adjustments to the data to ensure the applicability of the model - data obtained from the financial reports of members of 3-stage cooperative SCs of each industry are assumed to be dedicated to each specific cooperative SC without including other operations. In the first stage of problem and objective identification the author makes a theoretical review of WC in FSCM. In the second phase, the author introduces the concept of mCCCC using archival and design science approaches.

In addition, examination of models described in the literature to estimate the cycle time of collaborative SCs revealed flaws in existing measures. In the third and fourth phases, the developed mCCCC concept is tested in four collaborating SCs from different industries - projects, ICT, publishing and automotive. Two approaches are used - scenario analysis for the justification of the DAO component in collaborative SCs and optimization of the mCCCC model for minimizing total financial costs based on mCCCC components such as variables, target levels of total inventory, total A/R, A/P total and A total. /E as goals and current cost levels as constraints.

The fifth part summarizes all components and provides an explanation of the achieved objectives of the master's thesis.

Coordination modeling case study analysis

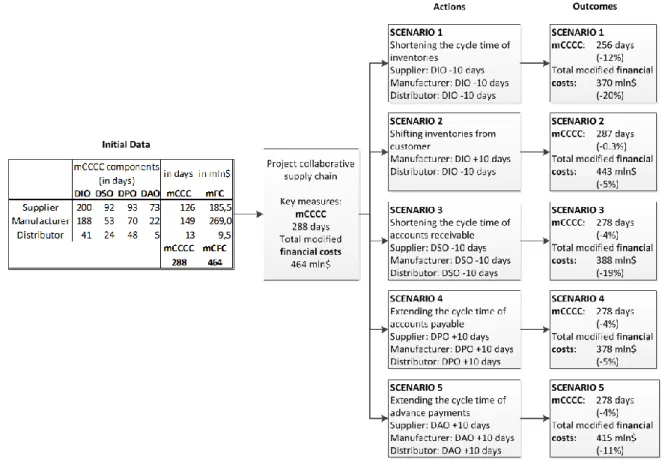

Case study of mCCCC scenario analysis

51 The data set is characterized by the high level of the DIO component for all stages of the cooperative SC. 52 Another possible scenario when inventory reduction is not possible – expansion of DPO and DAO components in cooperating SCs – internal payment terms. This cooperative SC is characterized by the high inventory level of the manufacturing company and pays its supplier late, but receives cash quickly from operations.

This increase may be due to high inventory holding costs and the fact that inventory levels for the manufacturer are already high – the high level of the DIO component proves that. In this case, in terms of collaborative SC – information sharing and trust, the members can agree to increase the cycle time of A/E to reduce the cycle time of WC and the total financial cost for an entire SC. The DAO component plays an important role in reducing the costs associated with the collaborative SC and the increase of this component brings a significant reduction in the mCCCC value.

In this case, the use DAO component in terms of collaborative SC can bring its benefits.

Case study of mCCCC coordination modelling

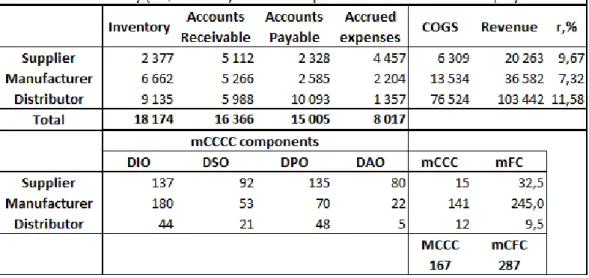

The optimized model has managed to achieve all criteria specified by the DM – reduction of total inventory and total A/R by 5% and an increase of total A/P and total accrued costs by 5%. For example, the amount of inventory for supplier is reduced and inventory for manufacturer and retailer is increased, but decisions based on trust and information exchange in cooperating SC give better results if all companies operate separately – the example of this decision was reviewed in chapter 3.1. The optimized model has managed to achieve all the criteria stated by the DM – the reduction of total inventory and total A/R by 5% and an increase of total A/P and total accrued costs by 5%.

The results of the minimization of the objective function using the mCCCC components as variables are listed in Table 3.6. The optimized model was able to achieve all of the criteria specified by DM - a 5% decrease in total inventory and total A/R to $9,709 million and $32,841 million in back and an increase in total A/P and total prepaid expenses of 5 %. to $8,057 million and $16,454 million in retrospect. The improvement of the concept mainly refers to a more accurate estimate of the WC cycle time in the SC – the DAO component is added to the traditional CCC calculation.

The scenario analysis which was adapted for mCCCC evaluation purposes by Randall and Farris (2009) does not take into account some critical characteristics of collaborative SC – the absence of overlapping intermediate payments as recommended by Viskari (2012), using the 10- daily is robust and do not reflect everyone's measures. The developed methodology of the mCCCC optimization model assumes the possibility of the absence of a feasible solution and offers two methods for prioritizing goals - weighted goals or preemptive programming. Coordination modeling – optimization of the mCCCC modeling fixed all the flaws identified in the WC cycle time collaborative estimation scenario analysis – goals which are stated by the DM and reflect the goals of the mCCCC and the minimization of the total cost function.

The feasible solution for Case 1

The feasible solution for Case 2

The feasible solution for Case 3

The feasible solution for Case 4