I declare that all information contained in this study has been collected and presented in accordance with academic norms and ethical principles, and that all information and documents that are not original to the study have been referenced in accordance with citation standards, within the framework required by the rules and principles. AN EXAMINATION OF THE EFFECT OF MONETARY EXPANSION POLICIES IMPLEMENTED BY FOUR MAJOR CENTRAL BANKS AFTER ALBANIA. GLOBAL FINANCIAL CRISIS 2008 AND THE COVID-19 CRISIS IN DEVELOPING COUNTRIES AS AN EXAMPLE OF TURKEY.

In the literature, there are many studies which show us that the financial crisis and the financial globalizations began to appear more often than before. The market's mood is reflected in the data when risks and uncertainty increase in the financial markets. The negative effects of the Covid-19 crisis, which had not arisen for economic reasons at the same time, creating a supply and demand shock, were seen quickly.

The link between the 2008 global financial crisis and the Covid-19 crisis is the need to increase declining aggregate demand. By putting money into improved market economies, it helps developing countries meet the need for financing that will deliver economic growth and development, while reducing production and increasing dependence on external financing. In 2008, the financial crisis and the COVID-19 crisis were brought about by a number of top leaders in the fight against the disease.

I express my eternal appreciation to my good friends who did not spare me their spirituality while preparing this study, and to my dear sister Tülay Öztürk, who has supported me at every stage of my life, and finally to my entire family.

INTRODUCTION

MONETARY POLICIES APPLIED AFTER THE GLOBAL CRISIS

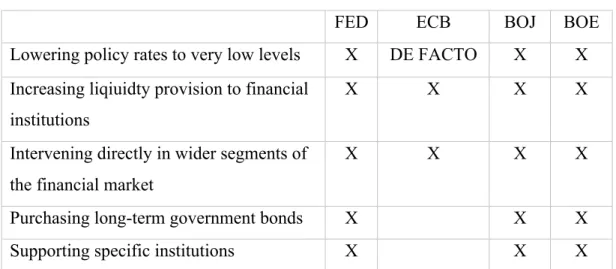

Monetary Easıng Policies Implemented By The Four Major Central

- Monetary Expansion Policies Implemented By The Federal

- Monetary Expansion Policies Implemented By The Bank Of

- Monetary Expansion Policies Implemented By The Bank Of

- Monetary Expansıon Polıcıes Implemented By The European

Reflections Of The Monetary Expansion Policies Implemented By

EFFECTS OF THE GLOBAL CRISIS AND MONETARY EXPANSION

As a natural result, the budget deficit has increased, foreign trade volumes have narrowed, unemployment tends to increase, and social problems have become severe, aggravating (Bedirhanoğlu Balaban, 2009: 1). Net portfolio investment, which followed a more volatile course, tended to increase again after the crisis of 2002. The table below shows the components of net foreign direct investment and portfolio investment directed to Turkey between 1989-2012.

MONETARY POLICIES APPLIED AFTER THE COVID CRISIS

- Monetary Expansion Policies Implemented By The Bank Of

- Monetary Expansion Policies Implemented By The European

- Monetary Expansion Policies Implemented By The Bank Of

- Reflections Of The Monetary Expansion Policies Implemented By

Since the Covid-19 pandemic has caused heavy economic costs to the economy, the Federal Reserve (FED) implemented various policies to counter the effects of the crisis in order to promote economic and financial stability. This is much more than the scope of the quantitative easing program envisaged in 2009 by the Bank (House of Lords, 2021: 3). On the other hand, these days, due to economic uncertainty after the pandemic, central banks are trying to balance the financial market and prevent possible large-scale corporate bankruptcies.

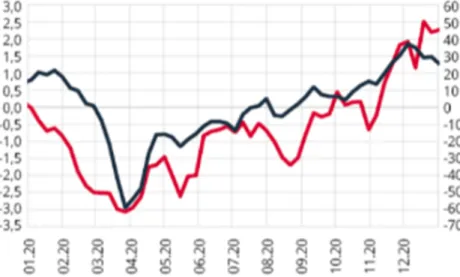

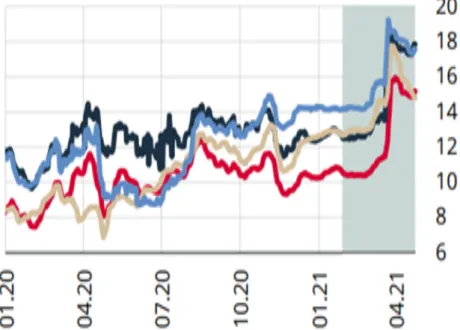

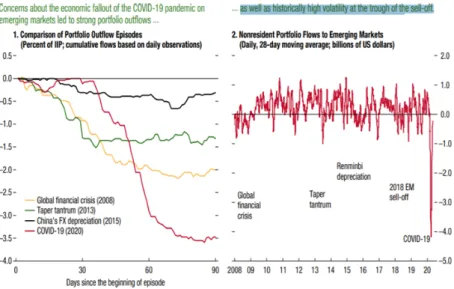

Looking at capital movements, portfolio flows to developing countries rose sharply in November 2020, according to IMF data. Reflections on monetary expansion policies implemented by post-Covid developed countries Post-Covid countries. This figure is more than three times the amount realized during the same period of the global crisis of 2008 (Şenol, 2020: 87).

To improve the area of capital flows, some measures were taken, such as a relaxation of the rules on entry. In portfolio flows to developing countries, the high output observed in the first quarter after the outbreak continued to increase in the second quarter of the year. As of the first week of July, outflows from developing country portfolios reached US$109.2 billion over the year.

As shown in the figure below, emerging market outflows in the second quarter accounted for almost all of the total outflows (CBRT. 24 During the period, there was one of the highest ever portfolio outflows from developing countries. The highest production occurred in Asian countries, especially China, as in the previous period, while a very large part of the production was from the stock markets in contrast to the previous period.

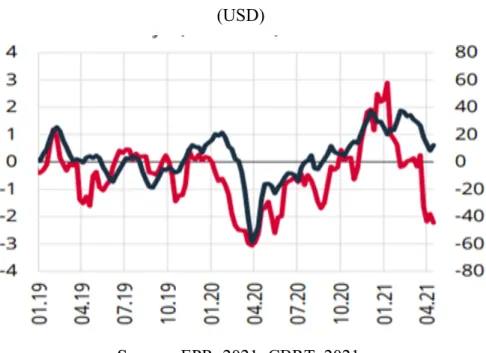

According to the graph below, in the first half of July, it can be seen that the outflows from regions other than Latin American countries have slowed down in the stock markets, while the outflows from the debt exchanges have decreased in all regions. According to IIF data, debt securities are the determinant of relative growth observed in the first quarter of 2021. Portfolio flows are expected to be negatively impacted by rising long-term inflation expectations in the United States, regardless of risk profiles of the country. (SBB, 2021).

REFLECTIONS OF THE COVID CRISIS AND THE MONETARY

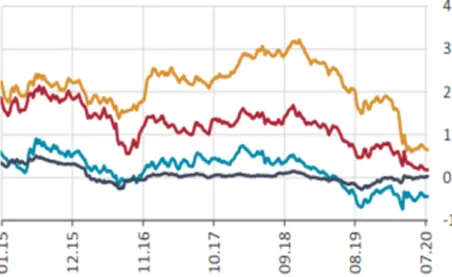

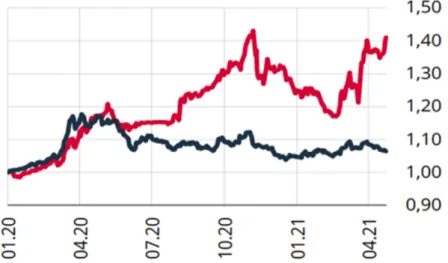

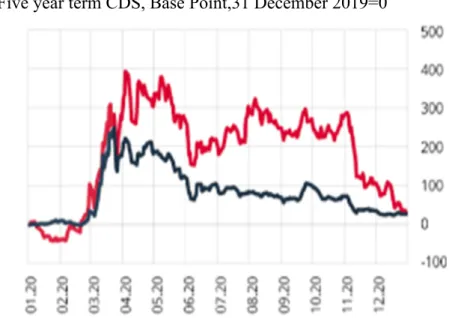

As a result, both portfolio inflows to Turkey recovered and the Turkish lira imbalance narrowed. Change in risk premium in Turkey and developing countries Five-year CDS basis point, 31 December 2019=0. The increase in long-term bond yields in developed countries also had a negative impact on portfolio inflows to developing countries: since February, portfolio movements have returned to the exit direction.

The main reason for the increase in long-term bond yields is the improvement in growth prospects and, accordingly, increased inflation. This trend is clearly visible in the US economy, which has the most positive growth prospects. So, with the outbreak of the epidemic, all portfolio investments coming from developing countries have returned, and the markets of these countries have started seeing outflows and fluctuations again.

Due to the global excess of liquidity and the high uncertainty associated with the epidemic, developments in the economies of developed countries in the future may cause fluctuations in the financial markets of developing countries. In the three weeks following the CBRT's January 2021 inflation report, the improvement in financial indicators continued. In the process, the Turkish lira gained value, while the country risk premium fell below 300 basis points.

Global risk appetite, which was on a positive trajectory after the US elections, started to deteriorate in February due to the uncertainty caused by inflation expectations. As details of the new fiscal stimulus package expected after the election became clear, US bond yields rose rapidly and global risk appetite reversed. The movement in bond markets has also led to a rapid deterioration in the perception of developing countries.

The ongoing times Fed policymakers highlight the downside risks to members' inflation and growth outlook for the year to the end of 2022 and the Fed policy stance that they do not expect us to because of a change in bond markets due to the perception of risk has improved. Bond yields, which moved horizontally at the beginning of the reporting period, rose due to a weakening in global risk appetite. After the calm of the global panic, risks caused by local developments emerged and severe losses in nominal bond prices were experienced.

CONCLUSION

Capital flows to emerging markets have begun to recover and many economies regained the market (IMF, 2020). Due to the abundance of liquidity caused by monetary expansion, developing countries have received their share according to their economic performance. Turkey is a country struggling with structural problems such as current account deficit from an economic point of view and struggling to achieve political stability due to its geographical location.

But it is becoming an attractive country thanks to its high growth potential and relatively high interest rates. In reviews, portfolio outflows from developing countries were experienced following the Covid crisis, while outflows from Turkey were significantly reduced in foreign reserves and losses were more severe due to country-specific developments such as the excessive devaluation of the Turkish Lira. Although there is no significant increase reflecting policy-infused liquidity as capital flows to developing countries due to the ongoing uncertainty created by the Covid crisis, there will be a sharper recovery towards the end of 2021 as a result of developments and decisions made. from developing countries.

Turkey's share in increasing the risk appetite of international capital and turning to developing countries will be proportional to economic growth and stability. The Effect of Quantitative Easing Policies on the Composition of Portfolio Flows to Emerging Markets (in Turkish). Global Financial Stability Report: Chapter 1 Overview of Global Financial Stability Markets in the Time of Covid-19, https://www.courthousenews.com/wp-content/uploads/2020/04/imf-global-financial-stability-report. pdf, Access: 07/08/2021.

Assessing the economy-wide effects of quantitative easing (Working Paper No. 443) https://www.bankofengland.co.uk/working-paper/2012/assessing-the-economy-wide-effects-of-quantitative-easing, Consulted data: 6.07.2021. Stratejik Düşünce Enstitüsü, https://www.sde.org.tr/merve-karacaer-ulusoy/genel/fed-koronavirus-parasal-genisleme-ve-politikalar-kose-yazisi-16668, Data accessed: 8.07.2021. An Event Study of Central Bank Quantitative Easing in Advanced and Emerging Economies Due to Covid-19 (NBER Working Papers 27339), National Bureau of Economic Research, Inc.

Dünya ekonomisindeki son gelişmeler bülteni, https://www.sbb.gov.tr/wp-content/uploads/2021/06/Dunya-Ekonomisinin-Son-Gelismeler-2021-Yili-1-Ceyrek.pdf, erişilen veriler: 7.07.2021. Türkiye'de Makroekonomik Görünüm ve Para Politikası, https://www.tcmb.gov.tr/wps/wcm/connect/acc32e90-1220-4ce7-8d31-.