The Funeral Plan: Conduct of Business Sourcebook (FPCOB) is added to the Business Standards block within the Handbook, immediately following the Claims Management: Conduct of Business Sourcebook (CMCOB). 1) (in DISP) a relevant existing complaint, relevant new complaint, a relevant transitional complaint, and (in DISP and FEES 5) a relevant claims management complaint and an appropriate transitional funeral plan complaint.

Clients and the Principles

In relation to the pursuit of activities other than designated investment business, insurance risk transformation or activities arising directly from insurance risk transformation (for example general insurance business or the acceptance of deposits) the firm may choose to comply with Principles 6, 7, 8 and 9 than if all his customers were customers. In relation to carrying out activities falling within both (1) and (3) (for example, mixed designated investment business and the acceptance of deposits), a firm's categorization of a client under the COBS client categorization chapter (COBS 3) apply for the purposes of Principles 6, 7, 8 and 9.

General

The definitions of customer in relation to those activities reflect the scope of the business opt-out under the Payment Services Regulations.

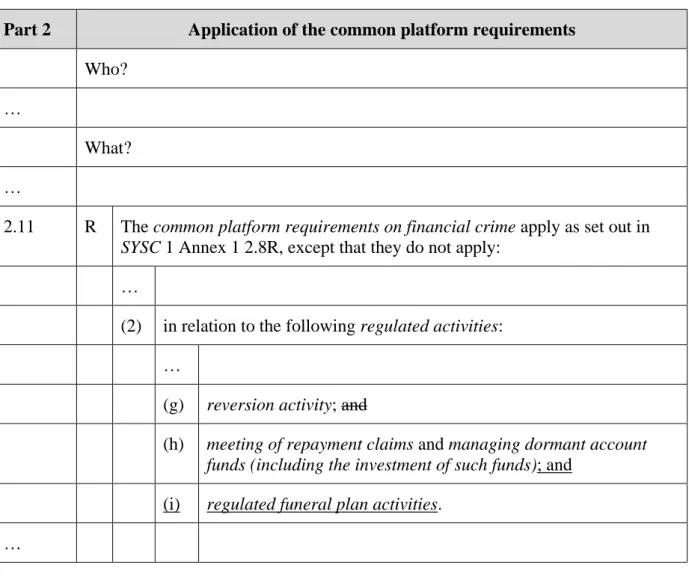

Application of the common platform requirements Who?

- Apportionment of responsibilities

- Application

- Definitions and types of firms

- Definitions of the FCA certification functions

Non-applicable guidance - but not applicable in relation to insurance distribution activities or the funeral plan. Rule regarding insurance distribution activities and funeral plan distribution. related to insurance distribution activities.

Bank of England and Financial Services Act 2016: Certification and regulatory references

Application and purpose

- G SYSC TP 7

Suitability

Assessing and maintaining competence

For this purpose, reference to retail investment adviser should be read as if it were a reference to a relevant employee (under TC 2.1.23DR). 2) With respect to SYSC 2.1.23FR, the 15 hours of appropriate continuing professional development may include structured and unstructured training and need not consist solely of formal classroom-based learning.

Appendix 1

Activities and Products/Sectors to which TC applies subject to TC Appendices 2 and 3

General saving of the Handbook for Gibraltar

Investment Intermediation Claims

Deposit acceptors’ contribution

Application of PROD 7 Application of PROD 7

For the purposes of PROD 7, a funeral broker is a manufacturer of a funeral product where an overall analysis of their business shows that they play a role in the design and development of a funeral insurance contract for the market. This chapter does not affect the application of other requirements in the FCA Handbook that apply to funeral insurance providers or companies with respect to funeral insurance benefits, including but not limited to:.

Manufacture of funeral plans

Product management arrangements: identification of the required approval process 7.2.3 R The product approval process in PROD 7.2.1R shall be proportional and. appropriate to the nature of the funeral plan product. Product monitoring and review: monitoring of distribution arrangements 7.2.42 R (1) A manufacturer shall take appropriate steps to monitor:. a) that a funeral plan product distributor acts in accordance with the objectives of the manufacturer's product approval.

Distribution of funeral plans

Distribution arrangements: events indicating breach of fair value 7.3.4 G The following evidence provision provides examples of what the FCA. Distribution arrangements: change of distribution arrangements after review 7.3.13 R A distributor must change the product distribution arrangements where. appropriate given the outcome of the review of the product distribution arrangements.

Product governance requirements for subsisting funeral plans Product governance arrangements

Transitional Provisions for Funeral Plan Products

2022, been available for marketing and distribution; and (2) remain available to. a manufacturer must ensure that the requirements of PROD 7.2 are met and remain so. appropriate for the product in question to continue to be marketed and distributed from 29 July 2022. G The effect of PROD TP 2.1 and the requirements of PROD 7.2 is that where the manufacturer is unable to demonstrate that it has met these requirements , then the manufacturer must:.

Claims management and funeral plan firms) (1)

Introduction

Among other things, these Rules describe those matters for which an Appointed Representative may be exempted or to which Sections 20(1) and (1A) and 23(1A) of the Act may not apply, namely matters that include any of the following: : . a) trading in investments as an agent (Article 21 of the Regulated Activities Decree) where the transaction relates to:. i) a pure protection contract (but only if the contract is not a long-term care contract) or a general insurance contract; or.

Notification requirements

For the purposes of SUP 12.7.6AR(1)(b), an increase by a material threshold is to be understood as referring to an increase in the number of appointed representatives undertaking regulated funeral plan activity:. All categories of firms except: Entire divisions. jc) a firm with permission to do funeral plan distribution only;.

Integrated Regulatory Reporting

All company categories except: Entire sections. jc) a company licensed to operate funeral plan distribution only. and for firms involved in regulated funeral plan activity, the FPCOB sets out the FCA's detailed capital requirements. By submitting regular data, firms allow the FCA to monitor their compliance with Principle 4 and their supervisory requirements.

SUP 16.12.2

Complaints reporting rules

When a complaint is upheld in part, or when the company does not have sufficient information to make a decision, but still chooses to make a goodwill payment to the complainant, a company will submit the complaint as well-founded for reporting purposes to be considered.

A Complaints data publication rules

If you report 1,000 or more complaints, do you agree to the FCA publishing the complaint data and context information contained in that report before the firm itself publishes the data. If you report 1,000 or more complaints, do you agree to the FCA publishing the complaint data and context information contained in that report before the firm itself publishes the data.

To which activities does the Compulsory Jurisdiction apply?

To which activities does the Voluntary Jurisdiction apply?

Transitional Measure Ombudsman, Transitional Measure Complaints Mortgage and Non-Life Insurance or Claims Management Regulations. It enables the Financial Ombudsman Scheme to cover complaints about past events involving those activities before they became regulated activities.

What is the territorial scope of the relevant jurisdiction?

Is the complainant eligible?

In the compulsory jurisdiction, pursuant to the Ombudsman's Transitional Order, the Complaints Transitional Order on Mortgage Loans and General Insurance and the Claims Treatment Order and the Funeral Planning Order, where a complainant:. Activities), any of the following activities specified in Part II and Parts 3A and 3B of the Regulated Activities Order (with the addition of . administration of a benchmark):. 39) entering into a funeral plan contract as a provider (Article 59);

Determination by the Ombudsman Fair and reasonable

Awards by the Ombudsman

G Under the Funeral Plans Order, a relevant transitional funeral plan is subject to the Compulsory Jurisdiction, regardless of whether or not it concerns a firm or an unauthorized person. Unauthorized persons are not subject to DISP 1, but references to "firm" in DISP 2 and DISP 3 include unauthorized persons subject to the Mandatory Jurisdiction in relation to a relevant transitional funeral plan, where applicable.

Claimants

What is a protected claim?

Rejection of application for compensation

When must compensation be paid?

Limits on compensation payable

Payment

Quantification date

The compensation calculation

Transitional Provisions .1 Transitional Provisions Table

Application and purpose Application

General application: who? what? where?

In this sourcebook, rules may apply when referring to the customer or covered person under a funeral plan contract or both. The covered person under a funeral plan contract will not necessarily be the same person as the customer (Article 59(2)(b) of the Regulation on Regulated Activities).

Inducements

Customers with a payment shortfall Application

Trusts: solvency assessment, remediation and other requirements Application

Communications and financial promotions: the obligations Fair, clear and not misleading rule

A company is required to comply with the financial promotion rules in relation to a financial promotion announced by its designated representative, even where the financial promotion does not require approval due to the exemption in Article 16 of the Financial Promotion (Exempt Persons) Ordinance. A company must ensure that the information on contractual obligations to be communicated to a consumer in the pre-stage phase is consistent with the contractual obligations that would result from the law that is supposed to apply to the distance selling agreement if that agreement is concluded.

E-Commerce Application

A consumer will provide all information necessary for a funeral provider to decide whether to offer an arrangement and to calculate the price of the arrangement. The response of a funeral insurance provider, who gives the consumer a quote containing the price of the provision and the terms and conditions, is likely to amount to an offer of the terms on which the funeral provider will offer the arrangement.

Means of communication to customers Application

Fee disclosure Application

Charging for funeral plan distribution Application

However, this rule only limits the receipt of payments or benefits in connection with the business of participating in the distribution of funeral arrangements. For these purposes, it is immaterial whether the payment for the funeral is received at the time the customer enters into the relevant funeral plan contract or at some other time thereafter.

Payments to funeral plan intermediaries Application

Prohibition Prohibition

This may include a funeral plan contract that requires the customer to pay until the insured individual reaches a certain age or regularly until the insured individual dies.

Demands and needs

A funeral plan provider may agree to a moratorium period with a client of less than 24 months provided it remains in compliance with FPCOB 3.1.6R. 8 Identification of client needs and counseling 8.1 Application. In determining whether a funeral plan contract is consistent with the client's requirements and needs, a firm should consider, among other things:

Ensuring customers can make an informed decision Disclosing the limits of the service provided

Advised sales Application

When taking reasonable care to ensure the appropriateness of advice on a funeral plan contract, a company should:. a) determine the client's requirements and needs by using information readily available to the Company and obtaining further relevant information from the client, including details of existing alternative arrangements by which the client can reasonably cover the cost of the funeral in question finance. This could be, for example, insurance products, investments or cash savings, or where the customer has already made provisions for the customer or the insured person.

Producing and providing product information Application

Providing product information to customers: general

Responsibility for producing and delivering the funeral plan summary between funeral plan providers and funeral plan intermediaries. This must be done orally if a company provides information orally about one of the main characteristics of a funeral plan, but otherwise in writing.

Post-contract information: funeral plan contracts Application

In the case of a distance contract concluded by telephone, it may be secured in writing or by another durable means no later than immediately after completion.

Means of communication Means of communication

This section should clearly define items that are not included in the cost of the plan and that must be paid for separately. A firm must provide a clear explanation of the funeral plan contract's coverage if the covered individual dies before payments end, including any associated fees.

Application and purpose Application

This rule applies to a funeral plan provider who has taken over the undertaking under a funeral plan contract to provide or provide insurance for a funeral as a result of the transfer of the contract. Such firm may not receive or process payments for a funeral plan contract except in the form of cash and may receive or process a cash payment only if such contract will be effective from the time of receipt. .

Obligations on intermediaries

Obligations on providers

Appointed representatives

The right to cancel

Effects of cancellation Termination of contract

Accordingly, the rules in this chapter establish requirements regarding the financial resources of a firm to which this chapter applies.

General solvency requirement

Where the FCA decides to issue guidance, it will usually explain how the FCA will approach the supervision of the general solvency requirement in relation to a firm. The FCA expects that a firm will normally confirm to the FCA that it will hold in future the amounts set out in this guidance (and will therefore have adequate capital and/or liquidity resources to meet the general solvency requirement), unless the firm subsequently determines that they are necessary higher amounts.

Core capital resources requirement

Capital resources: relevant accounting principles

Core capital resources requirement for a firm that only undertakes funeral plan distribution activity

Core capital resources requirement for a firm carrying on other regulated activity

Calculation of annual income Annual income

Calculation of core capital resources

For the purposes of calculating capital resources in relation to the occupational defined benefit pension scheme:. For the purposes of calculating capital resources, a company must make the following adjustments to its reserves where.