This thesis focuses on the intersecting dynamics of the digital work platforms and digital payments, as manifested in these ride-hailing apps. I argue that the mobilization of drivers and their digital wallets is at the service of the app's customers.

L IST OF A BBREVIATIONS

G LOSSARY

Used in conjunction with 'account therapy', a concept that loosely describes a range of practices to improve the 'quality' of an account from being a gag to being a gag. Used by executives to describe reaching their daily incentive point targets to receive the daily bonus.

A CKNOWLEDGEMENTS

A special thanks to my PhD colleague there Agus Indiyanto, and his students Annisa, Rahmad and Ami, for sparring and guidance during fieldwork. To Eka, thank you for first inspiring me to come to Jogja, and to both Ibu Tanti and Ibu Puji for extending your friendship to me.

I NTRODUCTION

As the head of Gojek's data engineering team writes on the company blog, “The biggest moat GOJEK has built is payments. This refers to situations where algorithmic governance inadvertently causes pain to the users of the digital system.

M ETHODOLOGY

These interviews primarily helped me expand my technical understanding of the system and the broader context of digital money in Indonesia. This upbringing shaped my understanding of the world, my intuition and my sensitivity.

C ONFIGURING P EERHOOD 1

Introduction

In the second part, I turn to the concept of digital transaction and how such digital payment applications can be conceptualized as forms of accounting technology, drawing on literature from economic anthropology to show how money can be understood as tokenized debt. For example, how the increasing re-centralization of the Internet, our payment infrastructures and their respective transaction communities centralizes control of our transactions in the applications of a few private actors.

The Meaning of Peerhood

The term peer-to-peer, as understood in payments, generally describes the direction of money flow. The concept of P2P arose before contemporary digital payments, namely in the early development of the Internet's underlying infrastructures.

Technologies for Keeping Account

Thus, for intermediaries, “the dream is of a system in which value enters the network and circulates endlessly, never leaving as physical cash” (Maurer, 2016, p. 214), providing them with a constant source of income. The idea of using P2P networks as a way to manage a decentralized process dates back to the origins of the Internet and is a visible ideal in the open source community. A longtime proponent and developer of P2P technology (cf. Robinson et al., 2018), McKelvey expressed that "in P2P, token is a bad word." The phrase stuck with me because many of the people in the room from the blockchain community she spoke to were supposedly part of the P2P community themselves.

Where cash allows users to transact with limited barriers and transactional metadata—the original peer-to-peer payment system, as Brett Scott (2017) argues—digital payment platforms increasingly control the circulation of value much like Internet platforms control the circulation of information.

Conclusion

This raises questions about what happens when money exists as tokens within the transactional ecosystems of platforms like Gojek, and how they introduce peers into their transactional communities, which I explore in the following chapters. In the case of P2P payments, presumably the person on the other end of the exchange. However, in the case of P2P payments, as implemented by fintech, the peers do not contribute to the network, they are the exchange parties.

In the rest of this thesis, I examine the case of payment apps in Indonesia, and the terms of exchange they impose on their users, how they affect exchange dynamics and either reinforce or introduce new digital hierarchies of transaction.

Introduction

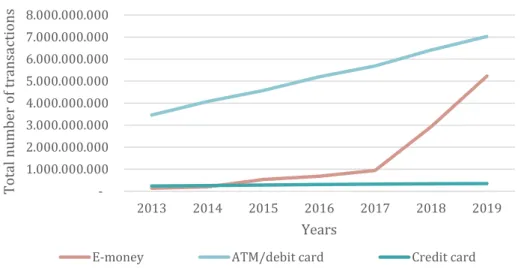

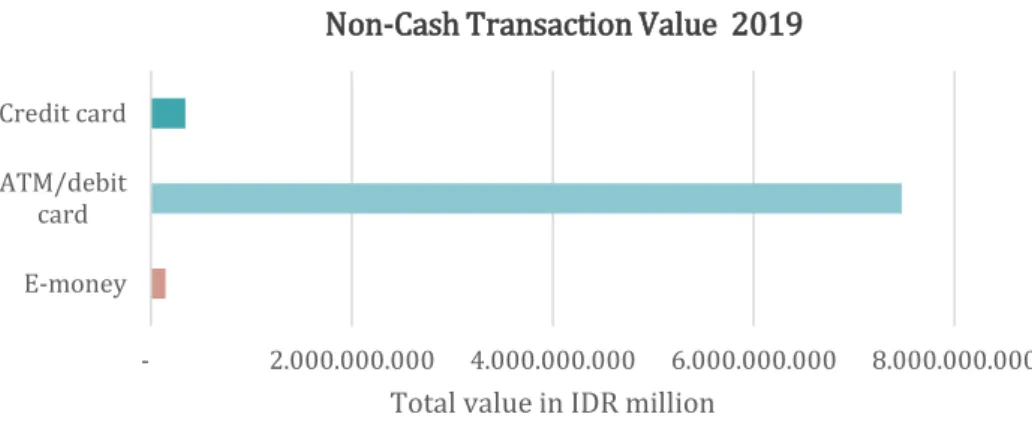

In this chapter, I present some of these socio-economic and infrastructural developments and the more recent political and regulatory transformations that form the context for the digital economy that exists in Indonesia today. In the first section, I examine how infrastructures of connectivity, such as mobile phones and the Internet, converge with infrastructures of digital money to form 'e-money', which increasingly dominates the Indonesian digital economy. In the next section, I focus on two of the Indonesian unicorns that Jokowi referred to, now decacorns,15 which were the focus of my data collection.

My purpose here is to show how these fintech players have positioned themselves centrally in the digital economy.

Converging Infrastructures of Connectivity and Money

Exploring how the "Internet" looks and feels in Indonesia is an important analytical starting point for understanding its use. Media expert Merlyna Lim has written extensively on the emergence and use of the Internet in Indonesia since it became commercially available in the mid-1990s (cf. Lim, 2018a. The importance of the ATM was also made clear when I asked the women in the focus group if they had owned or used a bank account.

One of the first forms of e-money to gain huge popularity in Indonesia was called BBM Money.

Towards a Cashless Future

- Indonesian Unicorns and their Driver-Partners

- Conclusion

This was before the release of the Gojek app itself in 2015, which shows the prospect of incorporating an integrated payment into the transport app. This redesign also marked a change in the core services of the app from ride-hailing to a multi-service platform with an integrated payment system. Although the use of mobile phones far exceeds the members of the population with access to a bank account in Indonesia, smartphones are less common.

In the next chapter, I explore these arguments about financial inclusion and cashless payments, and the way in which driver-partners are mobilized in the service of the digital economy through the application infrastructure.

S ERVICING C ONSUMER -C YBORGS 3

Introduction

I show how recent economic growth has led to increased wealth and income inequality, as well as what some scholars call an emerging middle class. I explore how middle-class identity is tied to both moral and intellectual social standing, as well as “practices of making” (Simone and Fauzan, 2013), which include social markers such as consumption that correspond to a perceived middle-class lifestyle. . I also draw on the concept of “slavery culture” (Ray and Qayum, 2009) to explore how the middle class is constituted through the employment of domestic workers.

First, I use the concept of 'social infrastructure' (Elyachar, 2010; Simone, 2004) to argue that driver-partners are mobilized as an extension of the payment infrastructure itself.

Fintech and the Pursuit of Cashlessness

The example was made in a report from the development sector and was cited as an example of the inefficiency of the network. These visions of the middle class are reproduced in many ways through the digital payment apps and reflect certain ideas about its users. The conceptualization of the Indonesian middle class as being tied to consumerism is a dominant narrative in the literature.

In her analysis of the 'emergence of the market' in Indonesia, Lisa Tilley (2016) makes the astute argument that this dispossession of the urban poor has been enabled in part because of perceptions held by the middle class.

Infrastructures for Consumer-Cyborgs

To explore how these drivers form a critical social infrastructure in the context of digital payments, I will first introduce two fundamental examinations of the concept through the work of Julia Elyachar and AbdouMaliq Simone. Brian Larkin (2013) describes this feature of the relationality of infrastructure and outlines what he calls the 'peculiar ontology of infrastructure'. The consumer is a cyborg and the app is the operating system of the 'real' world.

Gray and Suri draw attention to the point that by making them invisible, the work of workers in the "ghost economy" is easily devalued, both monetarily, socially, and in terms of labor rights and protections.

Conclusion

Thus, the app companies can easily extract some of the wealth generated by the investment the drivers themselves have made in their trade. The company provides you with an interpretation and configures its users through the interface of the app. By this I mean the way in which the driver-partner figure becomes an integral part of the process of introducing money into the digital system and then contributing to its further circulation.

Meanwhile, the language of automation surrounding the use of the app from a consumer's perspective makes the work of these drivers invisible.

H ASSLE -F REE P AYMENTS 4

Introduction

I examine a specific example of an exchange that illustrates how, in prioritizing the needs of cyborg consumers, the app's design exposes drivers to infrastructure vulnerabilities by reducing their performance over their own digital money. Any stabilization on the exchange parameters they offer is temporary as the infrastructure continues to change with each app update. During my fieldwork, I also realized that app experiences cannot be relied upon as consistent across users, for example due to A/B testing by companies, asynchronous updates, etc.

Therefore, I do not strive to give one "true" and "accurate" representation of the app, but accept the experiences of my interlocutors, whether communicated as stories or through screenshots, as valid experiences.

Enabling Cashless Transactions

In the case of the barista, it was the driver who enabled my transaction to go cashless with his own cash to pay. Again, OVO credit can be seen immediately in the upper right corner of the wallet menu. In this thesis, I focus on the role of the driver as an exchange broker.

Importantly, it is not about creating trust between the customer and the application technology, but between the two parties involved in the transaction.

Introduction

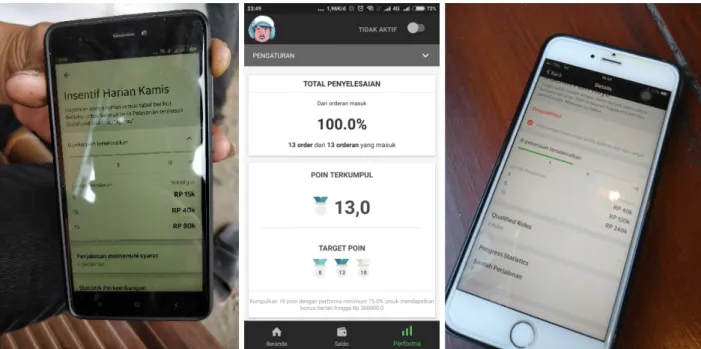

I show how salespeople play an ambiguous role in relation to managers, as they contribute to the configuration of the manager-partner through their communicative practices. In the final section, I examine events surrounding the introduction of a new incentive points system in March 2019 that dramatically changed the working conditions of drivers. I show how managers tried to challenge this system through protest and by making themselves temporarily unavailable to the consumer cyborgs.

I show how drivers collaborate to make sense of these algorithmic changes in the face of a lack of transparency from the companies, communicating strategies to counter the new conditions, but also internalizing the moral doctrines of work that implies of the new system to justify the exploitation of the "lazy" and rewarding of "diligent" drivers.

Driver-Partners

Once your registration is approved, you can activate your account through the driver version of the Gojek or Grab app. By increasing the value of the endpoints, these apps create a strong incentive for drivers to work as long as possible and thus remain available to the consumer cyborgs. By linking the bonus payment to the order completion rate, it discourages drivers from cancelling.

Customers also cancel orders and this will not affect the driver's 'performance rating'.