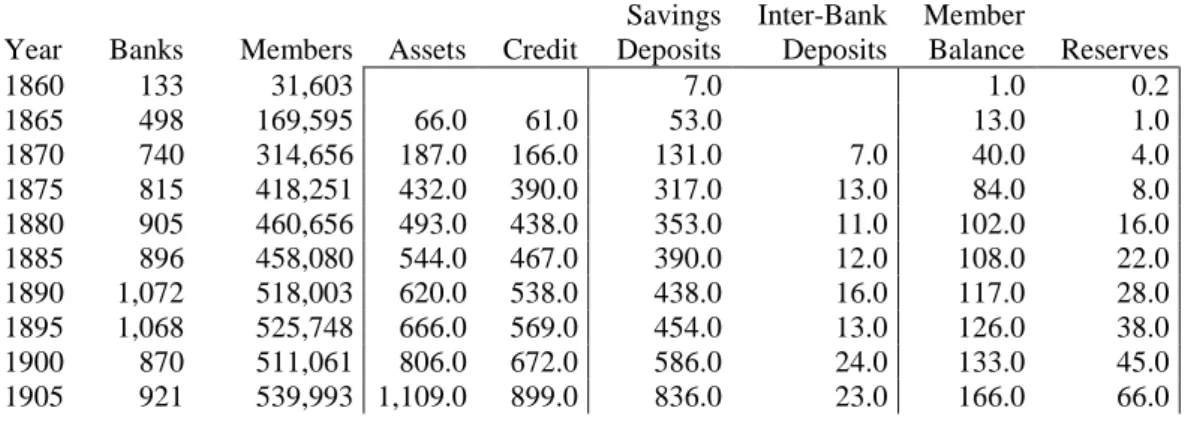

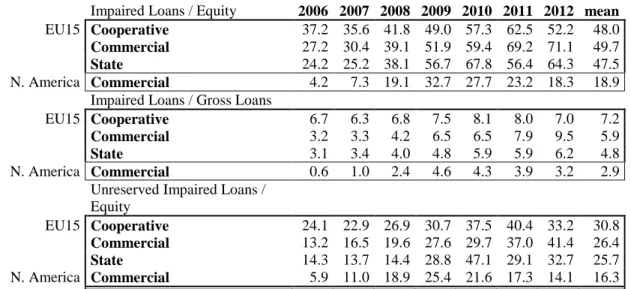

Back to the future of alternative banks and patient capital

Texto

Imagem

Documentos relacionados

Para Menegassi (2005), as estratégias de leitura não são construídas isoladamente e sem orientação. Elas precisam ser ensinadas e, para tanto, o professor precisa

Em sua pesquisa sobre a história da imprensa social no Brasil, por exemplo, apesar de deixar claro que “sua investigação está distante de ser um trabalho completo”, ele

En effet, même si le bioart n’est pas le seul type d’art contemporain faisant surgir des conflits entre esthétique et éthique, dans le cas de ce courant ces

É nesta mudança, abruptamente solicitada e muitas das vezes legislada, que nos vão impondo, neste contexto de sociedades sem emprego; a ordem para a flexibilização como

Este artigo discute o filme Voar é com os pássaros (1971) do diretor norte-americano Robert Altman fazendo uma reflexão sobre as confluências entre as inovações da geração de

This log must identify the roles of any sub-investigator and the person(s) who will be delegated other study- related tasks; such as CRF/EDC entry. Any changes to

Além disso, o Facebook também disponibiliza várias ferramentas exclusivas como a criação de eventos, de publici- dade, fornece aos seus utilizadores milhares de jogos que podem

1) During the process of diagnosis, the importance of assisting the patient to maintain both his self-identity and social identity can- not be