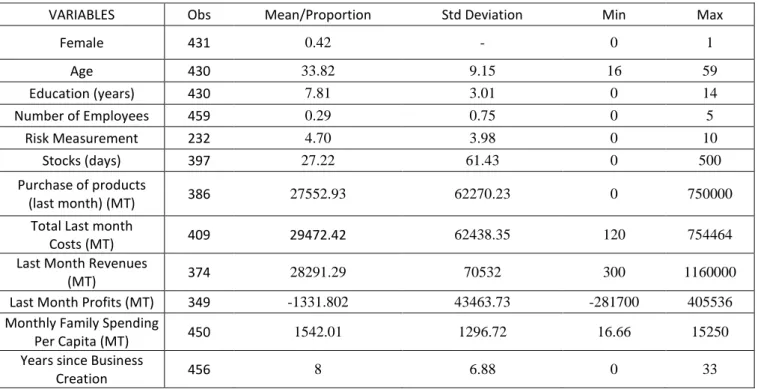

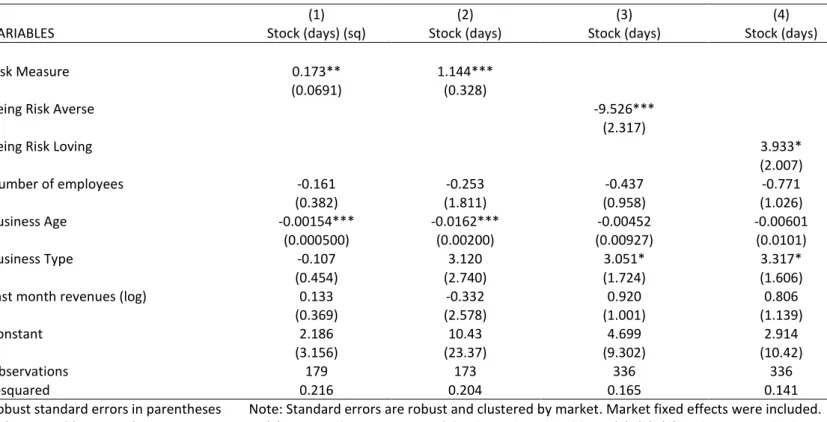

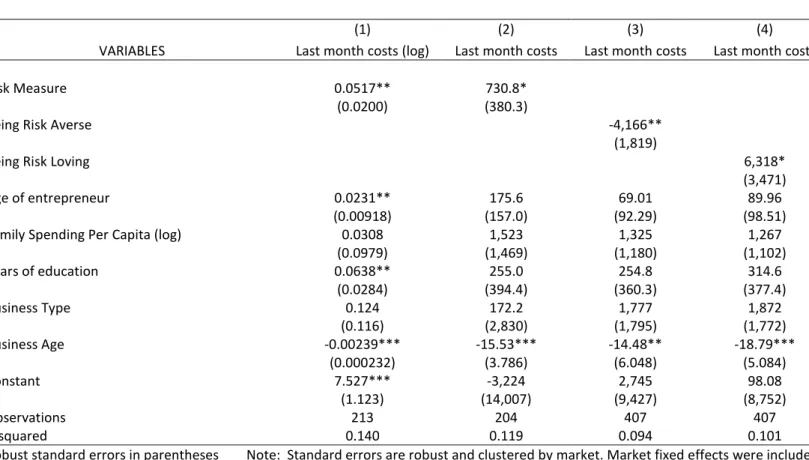

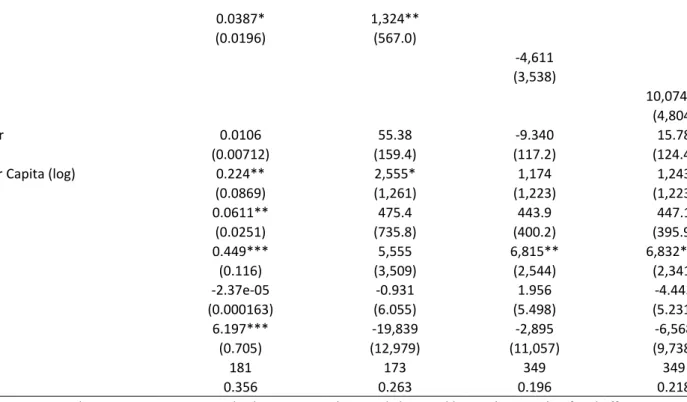

The impact of risk attitudes on micro-enterprise performance

Texto

Imagem

Documentos relacionados

segundo o tipo de cirurgia, a sobrevida global em cinco anos foi de 87,5% para os pacientes submetidos à cPtr e à nefrectomia parcial.. esses índices são semelhantes aos estudos

The probability of attending school four our group of interest in this region increased by 6.5 percentage points after the expansion of the Bolsa Família program in 2007 and

More and more, the RIHL research becomes critical to the knowledge about the auditory health of neonates and infants with risk indicators, once they are more susceptible to develop

Manuel Couret Branco, Nuno Ornelas Martins and Ana Cordeiro Santos, « The Economy as Substantive Reality: The First Meeting of the Portuguese Association of Political Economy...

Conclusion: The risk of death due to cerebrovascular and ischemic heart diseases declined in the Southwest and South, whi- ch are the more developed regions of Brazil, whereas the

Não é suficiente afirmar que as imagens de Cláudio Assis em Amarelo Manga e Baixio das Bestas querem o desconforto, porque o desconforto ali está sempre associado a uma

Após a última delimitação, verificou-se que os municípios que compõem o Semiárido Nordestino totalizam 1.171, estando espacializados na Figura 2. Esses municípios

Durante agosto de 2018, foi divulgado, aleatoriamente, em grupos de Whatsapp, uma chamada com a seguinte expressão “Formulário de inscrição para recebimento de