A Work Project, presented as part of the requirements for the Award of a Master Degree in Management from the NOVA – School of Business and Economics.

“How to grow Renova’s business out of

the tissue category in Portugal?”

Marketing Plan

Beatriz Teixeira de Figueiredo | 18497 Mafalda Guedes da Silva | 24619

Mariana Lopes | 18277 Jonas Dominique Weber | 24999

A Project carried out within the Master in Management Program, under the supervision of: Professor Jorge Velosa

Abstract

Market leader in the tissue category in Portugal, Renova is a well renowned brand in its home market. Focused on maintaining its leading position, the company has expressed interest in exploring new opportunities outside its core business, while staying within its current distribution network. Careful industry analysis of the two main categories home care and beauty and personal care identified a potential growth opportunity within the men’s grooming category. The proposed concept for ‘Renova Men’ revolves around the concept of well-being and feeling good in an approach to liberalize men from outdated stereotypes. A marketing plan for the implementation of the concept is suggested, including an Integrated Marketing Communications Plan.

Outline

1 Introduction ... 1

2 The Process of Choosing ... 2

3 Situation Analysis ... 3 3.1 Customer ... 3 3.2 Company ... 5 3.2.1 SWOT ... 6 3.3 Context ... 7 3.3.1 PESTLE ... 7 3.4 Collaborators ... 10 3.5 Competitors ... 11 4 Market Research ... 12 4.1 Salesforce Trip ... 12

4.1.1 Key takeaways from Modern Retailers ... 13

4.2 First Qualitative Research ... 14

4.2.1 Marketing Problem ... 14

4.2.2 Methodology and Sample ... 14

4.2.3 Key insights ... 15

4.3 Quantitative Research ... 16

4.3.1 Marketing Problem ... 16

4.3.2 Sample ... 16

4.3.3 Methodology and Questionnaire ... 16

4.3.4 Key Insights ... 17

4.4 Second Qualitative Research ... 19

4.4.1 Marketing Problem ... 19

4.4.3 Key Insights ... 19 5 The Concept ... 20 6 Brand ... 23 6.1 Segmentation ... 23 6.2 Target ... 24 6.3 Positioning ... 25 6.4 Positioning Statement ... 26

6.5 Renova Men Brand Identity ... 27

7 Product ... 28

7.1 Range Policy ... 28

7.2 Product Mix Breadth ... 28

7.3 Product Line Depth ... 28

7.4 Product Item Design ... 30

7.5 Intrinsic characteristics of the product ... 30

7.5.1 Design policy and packaging ... 31

8 Pricing ... 33

8.1 Pricing Strategies ... 33

8.2 Neutral Pricing Strategy ... 33

8.2.1 True Economic Value ... 34

8.2.2 Perceived Value ... 34

8.2.3 Sourcing Costs ... 34

8.3 Skimming Pricing ... 36

9 Distribution ... 36

9.1 The Channels ... 37

9.2 Channel Structure and Members ... 37

9.3 Services provided and End-User shopping behaviour ... 37

9.5 Gap Analysis ... 40

9.5.1 Environmental bounds ... 40

9.5.2 Managerial bounds ... 40

9.5.3 Demand-Side Gaps ... 40

9.5.4 Supply-Side Gaps ... 41

9.6 Closing the gaps ... 41

9.7 Power sources and potential conflicts ... 42

10 Communications Plan ... 43

10.1 Marketing objectives ... 43

10.2 Target audience selection and action objectives ... 43

10.3 Target Audience Decision Making ... 44

10.4 Communication objectives ... 44

10.5 Positioning statement for the campaign ... 45

10.6 Creative strategy ... 46

10.7 Integrated marketing communications strategy ... 46

10.8 Media strategy ... 47

10.8.1 Launch Event ... 47

10.8.2 Facebook Contest ... 48

10.8.3 Other media ... 49

10.9 Media budget allocation and campaign scheduling ... 49

10.10 Campaign tracking and evaluation ... 50

11 Promotion ... 51

11.1 Pre-Promotional Activities ... 51

11.2 Listing fees ... 52

11.3 Point of sale (POS) ... 52

11.4 Trade Advertising ... 53

12 Key Success Factors ... 54

13 Financials/ Profit & Loss ... 55

13.1 Market share projections and sales forecast ... 55

13.2 Cost of Goods sold (COGS) ... 56

13.3 P&L ... 56

14 Control Measures ... 57

14.1 KPI’s ... 57

15 Contingency Plan ... 58

1 Introduction

The proposed objective of this report is to find a solution for the challenge “How to grow Renova’s business out of the tissue category in Portugal?”. To guide the idea development there were some requirements that needed consideration: work only with non-food categories, by focusing on personal and beauty care as well as home care; use channels where Renova is already entrenched, such as hypermarkets and supermarkets, and/or other retailers where there could be an opportunity to launch new products under the Renova brand.

In order to answer this challenge, a marketing business plan was developed. Several steps of analysing industry data were undertaken at the beginning to evaluate the risk and potential of the various opportunities in the different sub-categories within the two main categories, home care and beauty and personal care, which led to the determination to explore opportunities in the men’s grooming category. In the consecutive steps a situation analysis (5C’s analysis) was first outlined. As a second step, qualitative and quantitative market research was conducted to gather insights about consumer behaviour in the men’s grooming category. Thereafter, a suitable concept for the launch of a men’s grooming line was established, that is afterwards translated into a marketing strategy starting with segmentation, targeting and positioning as well as establishing a brand identity. Proceeding in the marketing plan the marketing mix with product definition, pricing strategy, distribution and promotional activities for above and below the line activities is developed. In the following key success factors were determined, which lead over to financial aspects of the marketing plan that cover the sales forecast and cost of goods sold and culminate in a profit and loss statement. Lastly, control measures and a contingency plan for the project are proposed.

2 The Process of Choosing

The process began through market analysis, more specifically through the development of a market attractiveness matrix to assess both the potential and risk of new possible product categories. For that, market data for the Portuguese market was collected from Euromonitor International for two industries that were already in tune with Renova’s current business: home care and beauty and personal care, each one comprising several business categories (Exhibit 1). The data was grouped into potential and risk variables using a point scale of 0-100 and a scoring to compare them. The variables included market size in retail value RSP €, the Herfindahl index, historic and predicted growth rates (CAGR), penetration of private label (expressed through market share) and the dominance of the biggest player (expressed through market share). The individual weights within the scoring for each variable are depicted in exhibit 2, and the resulting matrix from the scoring is shown in exhibit 3.

In the first matrix, the categories skin care, laundry care and men’s grooming were considered perfect matches (high potential and low risk quadrant), and along with the category fragrances (considered a low hanging fruit due to its low risk and low potential), were selected for further analysis. Next, market trends and insights were researched for each perfect match. This research led to the exclusion of laundry care from further consideration, due to its very high competition and market concentration on a few very large MNC’s that dominate the category (Exhibits 4 and 5). Another category attractiveness matrix was built, this time only including the sub-categories of skin care, men’s grooming and fragrances (Exhibit 6), using market size and predicted growth in the form of the CAGR as variables (Exhibit 7). The matrix can be found in exhibit 8.

Once again, at this stage market trends and insights were researched. At this point, the category fragrances was excluded from further consideration due to only the premium men’s fragrance being a relevant match, with all fragrance sub-categories not being a good fit in the matrix.

Consecutively, trends and other relevant information were collected for both skin care and men’s grooming (Exhibits 9 and 10). Skin care has a very large market size of €325M, being an extremely developed category, especially for female products. It has a very intense competition, and it is predicted to further intensify in the future. Also, facial care products are more often purchased at pharmacies and beauty specialist retailers (Exhibit 11). On the other hand, the current market size for men’s grooming is €233M and, according to data retrieved from Euromonitor (Euromonitor, 2016 A), the category is not very developed yet, apart from the shaving category, and is less segmented when compared to the female market. Thus, there is strong potential for development. The predicted CAGR for 2015-2020 is 1,73% and the expected market size for 2020 is €254M. Contrary to skin care, there is an observable inclination to buy men’s grooming products in supermarkets, beauty specialist retailers and also hypermarkets and discounters (Exhibit 12).

Thereby, considering the market size and category growth potential in combination with the aforementioned analysis, a final choice in favour of selecting the men’s grooming category was agreed upon. In order to further explore the opportunity within the men’s grooming category in Portugal, a situation analysis is conducted in the following part of this report.

3 Situation Analysis 3.1 Customer

In the case of Renova the customer market in which it operates is the consumer market that “consists of individuals and households that buy goods and services for personal consumption” (Kotler et al., 2008). In terms of overall market size Portugal has about 10,4 Mio. inhabitants in 2015 as depicted in exhibit 13. As males are the relevant demographic group for the project at hand, the male population in Portugal is 4,9 Mio. individuals (exhibit 14). However, the population is predicted to decrease due to an aging population. Regarding the level of income,

the “Portuguese average monthly wage was €984 in 2013 – nearly half the European average (€1,972). Portugal was in 18th position in a list of 28 topped by Denmark (€3,739), with Bulgaria in last place (€316)” (Euromonitor, 2014).

Furthermore, it is also fundamental to look at the trends in the Portuguese society. Recent trends indicate that men show an increasing interest in their appearance, which leads to a bigger investment in personal hygiene and beauty care products. However, it is important to bear in mind that this trend is clearer on younger generations with a more open mind; since most Portuguese men are still unaware of the products offering in this category or simply do not feel the need to use them (Euromonitor, 2016 A).

In order to understand which benefits customers are seeking, it’s important to state that these will vary among the different products in the men’s grooming category. The same will happen in the following topics that will be discussed below. While the main benefit that should be present on a men’s post-shave is the ability of smoothing men’s skin after shaving, the main benefit that consumers look for in a deodorant is to avoid any inconvenient smell caused by sweating. Regarding skin care, the main benefit goes along with the recent trend described above, to improve appearance. An increasing amount of men has now concerns in keeping a clean and hydrated skin, looking also for anti-ageing products to address wrinkles and fatigue (Euromonitor, 2016 A).

According to the findings of the primary research, the purchase motivation for the various products is driven by a mixture between necessity of usage and sensorial gratification, as well as the desire to improve their appearance. However, depending on the specific products the major motivational factor can vary, e.g. the purchase of products such as shaving foam/gel or shower gel/soaps is more motivated by the necessity of using these products, while the purchase of moisturizing creams and body lotions is more motivated by the desire of improving

appearance and the positive feeling of using them. The importance of smelling good is the driver behind the purchase of fragrances and deodorants.

Furthermore, according to the qualitative and quantitative researches, the most relevant factors influencing men’s decision while buying personal hygiene and beauty care products are the quality, brand reputation and fragrance. As an example there is the skin care sub-category, in which men prefer to buy premium products. Facial skin care are the products men perceive as more worthy to invest more money in order to have additional care (Euromonitor, 2016 A). In terms of shopping behaviour, men tend to look for convenient choices such as multifunctional products, and do not usually engage in complex in-store browsing. This suggests that promotion, advertising and the packaging will have important roles helping the men’s decision process (Warc, 2015).

3.2 Company

Renova is a Portuguese producer of paper consumption goods and hygiene products. Founded in 1939, the company has its headquarters and two factories in Torres Novas, Portugal.

Renova is a household name in the retail tissue and hygiene category in Portugal, with total value sales of €140 million in 2015, according to Nuno Matos (R&D and Innovation manager), only surpassed by Procter and Gamble and Sonae. However, if only retail tissue is considered, Renova is the second largest player with 20% value share in 2015, just after Sonae. By offering a wide range of tissue products at different price points, Renova is able to perform better than private labels, having recently proven its strength in the Portuguese market by taking away market share from its two largest competitors (Euromonitor, 2016 B).

Besides Portugal, the company is present in over 50 international markets that correspond to approximately 60% of Renova’s current sales. The company plans on maintaining its strong position in the domestic market, while further fostering its international presence, mainly in countries like Spain, France, Belgium and Luxembourg, where it has commercial units.

However, the aim is not to grow exclusively in volume, but for Renova to remain relevant in the industry through innovation and product differentiation (Euromonitor, 2016 C).

Also, Renova became increasingly known worldwide with the launch of its black toilet paper, which the company calls ‘the sexiest toilet paper on earth’. Coloured toilet paper helped underline Renova’s position as an innovative company and has changed the way consumers perceive toilet paper. Over the years, the brand has partnered with several prominent photographers to produce artistic advertising campaigns, that rely heavily on symbolic features and the concept of well-being, although the company has also showcased more sensual concepts (‘the pleasure of being clean’), featuring nude models in its advertising (Sousa, 2012).

3.2.1 SWOT

For the purpose of this project, a SWOT analysis was conducted in order to assess both the internal and external environment the company faces by entering the men’s grooming category.

3.3 Context

3.3.1 PESTLE

To get a better understanding of the environment in which Renova operates, the next pages highlight the relevant findings of the PESTLE analysis (the components that influence the business environment) conducted for the Portuguese market.

3.3.1.1 Political factors

The Portuguese political scene can be described as volatile; Portugal is considered a relatively unstable country, when comparing to other developed nations within the European Union. The country still has a low Political Stability Index (Valev, 2015).

Secondly, the Portuguese government has been vocal about reducing the unemployment rate, that reached 13,4% in 2014 and is down to 10,5% in the third trimester of 2016 (Crisóstomo, 2016 A). Also, young-population unemployment is a recent and concerning phenomenon (34,5% in 2014) (Silva, 2015). Regarding taxation, there was a decrease in the fiscal burden for Portuguese consumers, and the forecast is for the burden to further decrease in 2017, with no increase on direct taxes, which can be positive for private consumption. The normal VAT has been constant at 23% since 2011, although it has increased from 20% before the economic crisis (Crisóstomo, 2016 B).

3.3.1.2 Economic factors

Portugal is ranked 50th in GDP (PPP) worldwide in 2014 by The World Bank (2016). Moreover, it is ranked 41st worldwide in the Human Development Index (United Nations Development Programme, 2014) and 64th worldwide in Index of Economic Freedom (The Heritage Foundation, 2016).

In general, the Portuguese economy has been recovering slowly from the 2008 financial crisis, yet the latest economic indicators, such as GDP growth or consumer confidence, show a

positive development. However, several uncertainties, such as government debt, remain that could dampen the economic outlook for Portugal (Euromonitor, 2016 D).

In addition, the cost of living in Portugal is lower compared to most of the rest of Europe, yet the low average income leads to shrinking purchasing power and a preference for low cost products or cutting unessential expenditures (Euromonitor, 2016 E).

With regards to consumer expenditure, as illustrated in exhibit 15 and 16, it can be noted that the figures for Portugal are much lower compared to other European neighbours, yet the prediction is that the expenditure in Portugal will increase stronger than in other European countries in the years leading up to 2020. These findings also apply to consumer spending on personal care.

3.3.1.3 Social factors

Demographics: Portugal has a shrinking population with the second lowest birth rate in the European Union due to struggles of young families to find a stable financial situation to raise children. This leads also to a higher percentage of older people in the population. A trend that is enhanced by the strong emigration of many young people to neighbouring European countries (Euromonitor, 2014). The size of the various age groups and their predicted development till 2020 is depicted in exhibit 13 for the total population and in exhibit 14 for the male population as already in the customer part of this report. The two figures illustrate how the younger age groups are shrinking whilst the age groups above 45 a predicted to become bigger till 2020. Leisure: For the Portuguese watching TV is popular and the use of the internet and social media is increasing. However, cultural events are less visited with the exception of live music events (Euromonitor, 2014).

Appearance: Portuguese men are making more extensive use of beauty and personal care products and the usage of these products has become more accepted within the society. However, there are increasingly advertising campaigns that focus on portraying the “real

people” instead of highly perfected artificial beauty standards, thus promoting a wider diversity of beauty standards. Furthermore, wearing a beard in various shapes and sizes is popular among Portuguese men (Euromonitor, 2014).

3.3.1.4 Technological factors

Rate of technological change: the FMCG industry is highly competitive with product differentiation and innovation being crucial to survive for manufacturers (Cosmetics Europe, 2016). However, the success rate of product innovation is low, with 30% yielding positive outcomes, and with 20% being super hits; and 94% of innovations are me-too imitations, thus being early followers of the market and only 1,8% of new SKU are truly innovations. Innovation is mostly driven by large MNC players in FMCG (Marketeer, 2013). Regarding men’s grooming specifically, the underdevelopment of the category leaves great space for innovation and product differentiation, which can be a determinant factor for new entrants. Big brands such as Gillette invest highly in new product formats and models as a way of remaining relevant. Facial care products, namely anti-aging, are also under high levels of research and innovation by manufacturers (Euromonitor, 2016 F).

3.3.1.5 Legal factors

Portugal is among the European countries with the highest level of tax aversion, and it is estimated that 37% of Portugal’s wealth is in offshore accounts (Zucman, 2014). Nevertheless, the country was able to diminish VAT evasion in 2016 (Crisóstomo, 2016 C). With regards to consumer protection laws, Portugal has strong consumer protection laws in accordance to the standards of the European Union (Official Journal of the European Union, 2009) guided through e.g. the European chemicals agency (ECHA), scientific committee on consumers’ safety (SCCS). Also, there are several Portuguese Consumer Protection organisations, like Direção-Geral do Consumidor (public institution) and DECO, that help consumers exercise their rights

3.3.1.6 Environmental factors

Concerns regarding the natural environment are increasing and becoming an important issue in Portugal (European Environment Agency EEA, 2015). In addition, Portugal has a well-developed infrastructure with good availability of electricity, water, mobile network coverage and transport infrastructure such as roads, airports and ports (European Commission, 2016). 3.4 Collaborators

The general value chain for the cosmetics and personal care industry is characterised by five steps. The first step is characterised by the companies that provide the inputs to production, such as the raw materials of the ingredients. Within Europe there are more than 100 companies that manufacture cosmetic ingredients. Secondly, there are the product manufacturing companies, as well as all adjacent industries such as IT and research and development, required for the manufacturing process. In Europe alone there over 4,600 companies that manufacture cosmetics in Europe. Within the manufacturing process it can further be divided in in-house production and outsourced production. Once the product is completed, the next step in the value chain is the distribution and wholesale, which is followed by retailers and beauty services that are selling to the consumers. Lastly, there are the consumers that purchase and use the products (Cosmetics Europe, 2016). Besides the aforementioned steps of the supply chain there are also adjacent services, such as marketing agencies and advertising collaborators.

Since Renova’s core business is the production of paper products, it will outsource the production of the planned men’s grooming products to a different manufacturer. Therefore, in the downstream direction of the supply chain, they will collaborate with raw material suppliers that supply the inputs for the production, as well as with suppliers that manufacture the product. However, at the current stage of the project the choice for a certain supplier to manufacture the product is still to be made. Nonetheless, there are some considerations already in place that can help to determine the choice for a certain supplier. In this sense, the development of the product

can be split in the parts of developing and supplying a fragrance, the liquid, a bottle design and a packaging box. The choice is between a single one-stop-shop supplier that takes care of all these aspects, or to use several different suppliers. For both of these options there are several suppliers within the European Union that could collaborate with Renova. The preferred choice of Renova would be to have a one-stop-shop supplier, as it would make the project implementation easier, allow for smaller order volumes and would require less coordination efforts, thus likely leading overall to cost savings. However, the drawbacks are that perhaps one supplier cannot fulfil all desired product characteristics, which would make the product more mainstream and less exclusive with possible implications for the differentiation of the product. Consequently, the sourcing decision for certain suppliers is a constant discussion of trade-offs at Renova and the chosen supplier will be an important collaborator for Renova.

Once the product is manufactured, it will be delivered in Renova’s warehouse, from where it will be dispatched to the retailers through Renova’s existing logistics system. Thereby, the retailers are one of the most important collaborators, as they will have to accept the new products on their shelves to give them valuable retail space on them. With regards to the retailers, the most important collaborators are a few, yet very big, retail chains in Portugal, such as Sonae, Auchan and Jerónimo Martins. In addition to these big retail chains there are numerous smaller retail stores that also sell the brand Renova.

3.5 Competitors

By offering products such as men’s post-shaves, oil for beards, men’s facial moisturizers, men’s deodorants etc., Renova Men competes directly within the men’s grooming category in Portugal. Besides direct competitors from the men’s grooming category there is also indirect competitors from other categories such as skin care, bath and shower and deodorants that are not specifically for men. Furthermore, the competitors in the men’s grooming category in Portugal can be divided, to a certain degree, by the predominantly used distribution channels

for specific brands. Thereby, the biggest distribution channel for men’s grooming products are supermarkets, beauty specialist retailers and hypermarkets as outlined in exhibit 12, thus making modern grocery retailers the most important distribution channel. However, certain more premium positioned brands are usually not sold through the channel of modern grocery retailers, such as supermarkets.

The top 20 men’s grooming brands are depicted in exhibit 17, and the ones that are directly competing with Renova in the grocery retail channel are highlighted in red. The market shares demonstrate that the biggest players in the category are large MNC’s such as Procter & Gamble, Beiersdorf, Unilever, L’Oréal, and private label brands.

4 Market Research

Three separate primary researches were conducted. The first one was a qualitative research conducting 12 in depth interviews to explore the consumer behaviour in the men’s grooming category. Secondly, a quantitative research was conducted to test the insights from the qualitative interviews. Afterwards, another qualitative research was conducted to get insights for the price determination of the products. Additionally, to understand how Renova’s distribution and sales department works a field trip to several distribution partners of Renova was undertaken.

4.1 Salesforce Trip

To better understand the relationship between retailers and manufacturers (in this case Renova), a trip around Renova’s main distributors in the Lisbon area was guided by Mr. Paulo Faria, from the Department of Merchandising.

Renova is present in both traditional and modern retail. Nevertheless, despite managing the negotiation process with its modern retail partners, Renova has little control over small traditional brick-and-mortar stores, as they buy through cash-and-carries such Makro and

Recheio. The main focus of Renova’s commercial team is therefore on its modern distribution partners.

4.1.1 Key takeaways from Modern Retailers

Cardex: The negotiation of the products sold in each retailer (the list of products is called ‘cardex’) depends both on the retailer itself and the size of the stores – a hypermarket will have a larger ‘cardex’ than a supermarket. It can be renegotiated and altered, according to the success/failure of products, discontinuation or introduction of new products.

Negotiation power: Retailers have an increasingly high power over manufacturers, which can influence trade conditions and constrain manufacturers in the negotiation process. The payment of listing fees is often required for the introduction of new products.

Product placement: The placement of products in the shelves can be made using different criteria, being the format of the product, brand, or type of product. Most commonly, products are organised by product category, e.g. all deodorants placed together, and all after-shaves placed together. Ultimately, it is the retailer who plans the placement, although manufacturers can try and influence the process.

Promotions: These days, promotional activities are very intense. A common promotional endeavour undertaken by Renova is the negotiation of ‘topos’ (the shelves on the extremity of a corridor that face the main aisles of a store) and ‘islands’ (displays that lie in the centre of the store). Both formats can be accompanied by a price reduction on the items they display, and the amount paid to the retailer varies a lot depending on the retailer itself, the type and size of the store, and the promoted products. A new trend of permanent ‘topos’ could be observed in several retailers. These are more sophisticated displays that usually comprise several products of a specific brand, and they are negotiated to be present for a longer time than a regular temporary ‘topo’.

4.2 First Qualitative Research

4.2.1 Marketing Problem

The marketing research “is the systematic design, collection, analysis and reporting of data relevant to a specific marketing situation facing and organization” (Kotler et al., 2008). For Renova the purpose of doing this research is to understand the purchase behaviour in the men’s grooming category, and to assess market potential for the new products and the new concept that Renova will offer.

4.2.2 Methodology and Sample

Following the analysis of secondary data in the previous parts of this report, primary data from in depth interviews was collected.

For the first qualitative research an initial sample of 12 male respondents were selected. The sample was divided into two age segments: between 25 and 34 years old, and above 34 years old. For further details regarding the characteristics of the sample please refer to exhibit 18.1. The research questionnaire has five main steps outlined in the following (Kotler et al., 2008): ● Problem definition - Launch of a men’s grooming line.

● Research objectives - The goal was to understand the present consumption of men’s grooming products asking for their habits and valued characteristics, their perception about the products of the category and the brands used the most; also, after building the concept, get in front of customers and obtain their reactions, get feedback on what needs to be changed and then revise our concept.

Research Plan - In a first stage, 12 in-depth individual semi-structured interviews and a projective technique to understand the brand personality. Before proceeding with the interviews, a pre-recruiting questionnaire was conducted, in order to assess if individuals were applicable candidates for the interview. The interview guide for the qualitative research can be found in exhibit 18.2.

● Collecting and analysing the data - For the qualitative research we recorded the interviews, making sure all topics are covered and after that we did an analysis of the registered content. ● Interpreting and reporting the findings - see below.

4.2.3 Key insights

Regarding the present consumption of men’s grooming products, there are differences between the 2 age segments regarding the shaving routines: men between 25 and 34 years old usually do not shave every day; men above 34 years old usually shave every day. The products consumed on a frequent basis are deodorant, perfume, pre-shave, after-shave and facial moisturiser. For most of the mentioned products the respondents indicated that they use these products because they perceive it as a necessity. Furthermore, they indicated that price is not a very important criteria to purchase the products. Finally, the most valued characteristics in men’s grooming products are the quality, comfort provided and the fragrance.

It is also important to understand which brands are the preferred brands when talking about those products. In the conducted interviews respondents quoted that they usually do not buy private labels. Instead, they buy men’s grooming products from well-known brands, such as Nivea and L’Oreal, as they perceive them as good quality brands. Also loyalty among the respondents was assessed. Thereby the loyalty appeared to be depending on the specific product at hand, with higher loyalty towards facial products and more openness to try new brands for instance in deodorants and shower gel.

After understanding the respondents’ perceptions regarding men’s grooming products in general, the interviewers presented them with a preliminary value proposition that was later adjusted (Exhibit 18.2). The insights gathered were that most respondents (9/12) considered the concept interesting, highlighting the colours and the original packaging as differentiating factors.

In the end of the interview, it was important to understand how respondents perceived Renova. Thereby all respondents knew the company and all of them associate Renova with tissue products, especially toilet paper. Also, when asked “If Renova was a person, how would it be?” respondents mentioned simple, trendy, young, classy and elegant, multifaceted, storyteller and good communicator. To get further detailed insights regarding the interviews, see exhibit 18.3. 4.3 Quantitative Research

4.3.1 Marketing Problem

In addition to the prior qualitative research, a quantitative analysis was performed in order to have a better understanding of the consumers’ preferences regarding the men’s grooming category and to test the proposed concept.

4.3.2 Sample

A sample of 176 male subjects was gathered, comprehending three different age segments: a younger segment aged between 25 and 34 years old (69,32%), a middle-aged segment between 35 and 45 years old (11,36%) and an older segment aged above 45 years old (19,32%). Although an even distribution of the sample would be favourable there is an observable higher number of subjects from the younger segment, which is due to limited resources of the project team to reach older age segments. Furthermore, 95% of respondents live in an urban area and 83% hold a university degree. To get further details please refer to exhibit 19.1.

4.3.3 Methodology and Questionnaire

The questionnaire used for this research was divided into three different sections (Exhibit 19.2) and featured open and closed questions. The first section had the objective to better understand the consumer behaviour and benefits sought in the men’s grooming category. In the second section of the questionnaire respondents were presented with a new concept of men’s grooming

products (with no brand associated) with the goal of evaluating its attractiveness. The last section was created in order to assess Renova’s brand awareness and brand image.

4.3.4 Key Insights

By analysing the results of our quantitative research, it was important to first understand the beard grooming routine trends of the 176 respondents, and how these would differ with the “age” variable. It was possible to deduce that there’s a growing tendency to be clean shaven as men get older: 88,24% of the respondents in the older segment usually shave, and most of them do it daily (67,64%). By contrast, most of the subjects of the younger segment answered they keep a beard (36,89%), or they do both (shave and keeping a beard) (40,98%) and usually shave once or less than once a week (60,66%), thus indicating that there’s a tendency for keeping a beard, for at least a week (Exhibit 19.3.1).

It was also inferred that the products most subjects use at least once a week are the deodorant (90,91% of the subjects use it at least once a week), the bath and shower gel (86,93%), and the perfume (81,82%) (Exhibit 19.3.2).

Regarding motivations behind purchase these do not show a significant discrepancy between the different age segments. On the one hand, necessity represents the main motivation behind the purchase of products such as shaving foams/gels/creams, deodorants, soaps and shower gels. On the other hand, the will to improve appearance and the positive feeling of using men’s grooming products also pose as purchase motivators. Deodorants and perfumes are the products for which one of the main motivators is the desire to smell good (Exhibit 19.3.3).

Another important finding is that the choice for private labels, in general, remains very low, with the exception of soaps and shower gels. Regarding brand loyalty, soaps and shower gels are the products on which the subjects are more open to switch brands, together with the beard oil. In general, most men are “moderately responsive” to new brands in the men’s grooming category, thus occasionally trying out new brands (Exhibit 19.3.4).

Concerning the importance of different factors influencing the decision process, on a scale from 1 to 5, quality is the factor most respondents attributed an importance level of 5 (65,94%), followed by fragrance (44,2%), brand reputation (36,96%) and accessibility (34,78%) considered as a level 4 of importance. Packaging and price were considered as less important when compared to the factors described above, with most respondents considering them as a 3 in level of importance (Exhibit 19.3.5).

In the second part of the questionnaire, respondents were presented to the preliminary concept of men’s grooming products that was based on convenience of facilitating product choice through using colours to differentiate products by type (e.g. yellow for deodorants, blue for post-shave), with the main objective of understanding how they felt about it and get some insights on what needs to be improved to better satisfy them. It was concluded that although 47,48% of the subjects demonstrated a “moderately positive” feeling about the concept (in a scale ranging from “very positive” to “very negative”), most of them did not find it very innovative (33,13% answered “relatively innovative” and 33,09% “not so innovative”, in a scale ranging from “very innovative” to “not innovative at all”). Moreover, among those who did not show interest in the concept, 67,53% answered they are satisfied with the existing brands on the market, suggesting this concept would not bring anything new (Exhibit 19.3.6). Thus, it can be concluded that the concept was not sufficiently attractive for the customers and for this reason adjustments were made so the final concept is the one described in the concept part of this report.

The final part of the questionnaire had the main objective to assess the brand awareness and brand image of Renova. It was inferred that Renova has a very high brand awareness (98,56% of the subjects know the brand) and the brand image is mainly associated with toilet paper (79,14%), napkins (56,83%) and innovation (44,60%) (Exhibit 19.3.7).

4.4 Second Qualitative Research

4.4.1 Marketing Problem

Understand the willingness to pay in regards to men’s grooming products.

4.4.2 Methodology and Sample

For the second qualitative research a sample with three different age groups was selected. Thereby, 14 men were questioned: 6 men between 25 and 34 years old, 2 men between 35 and 45 years old, and 8 men above 46 years old (Exhibit 20.1).

● Problem definition - Launch of a men’s grooming line.

● Research objectives - Descriptive research with the goal to understand the maximum price at which men would buy the products and the price for which the product would start to be perceived as having an inferior quality.

● Research Plan - 14 in-depth individual semi-structured interviews (Exhibit 20.2). The interviews were made knowing that the respondents have some understanding of what men’s grooming products are priced at, and so it made sense to ask explicitly about price.

● Collecting and analysing the data - The interviews were recorded, making sure all topics are covered and after that we did an analysis of the registered content.

● Interpreting and reporting the findings - see below.

4.4.3 Key Insights

From the responses an expected price range for the products was derived taking into account the upper boundary of the price range considered as too cheap and the lower boundary of the price range considered as too expensive.

Figure 1 – Expected Price Range

The research helped to understand the price range men are willing to pay for the various products, and so it is useful when determining the price for each product of the Renova Men grooming line.

5 The Concept

Having determined to choose the men’s grooming sub-category and taking into account the findings from the situation analysis and market research, the next step is to develop a concept that would fit the brand Renova and that would offer a novelty to consumers. Thereby, the brand identity was used to determine the main topics the brand Renova owns and how they offer an opportunity to differ from the concepts already present in the market of men’s grooming products.

Thus, in order to outline the brand identity for Renova, the Kapferer brand identity prism was used comprising six different dimensions as outlined below (Kapferer, 2012).

Figure 2 - Brand Identity Prism of Renova

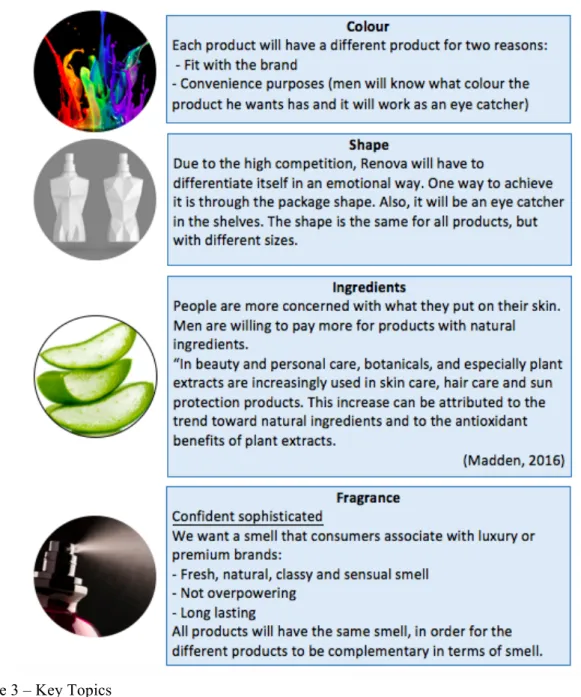

The main topics identified from the brand identity are the colours, the passion and sexiness and the art, which translates into fun. Moreover, Renova has previous experience in the skincare and cosmetics category to build upon through the discontinued cosmetics brand Dosha. It is important to note that, before doing the qualitative and quantitative research, a proposed concept based on the main topics and in a convenience benefit had been envisaged. However, adjustments were made in accordance to the main findings of the research as the customer’s needs and wants became more apparent. Thereby, taking into account the identity of Renova, the key topics and the conducted research, the proposed concept changed to developing a men’s grooming line focused on the well-being, and to the adoption of a liberated masculinity approach. The idea is that consumers have a pleasant experience that makes them feel good when using the products of Renova with different colours and an artistic male shape for the package, the natural ingredients and the fragrance that will altogether appeal to senses. The table below presents in more detail these key topics.

Figure 3 – Key Topics

Furthermore, the liberated masculinity approach tries to part with previous attempts of focusing on certain stereotypes of men, such as toughness and strength, as they are considered to be outdated. Instead, one should stop trying to define what it really means to be a man (Simpson, 2016). Men should be free to embrace their inner-core, without feeling pressured to follow any kind of stereotype, and consequently achieving psychological and physical well-being.

Hence, as Kotler and others (2008) said “customers are really buying much more than just products and services. They are buying what those offers will do for them”. Therefore, Renova does not want to deliver a simple men’s grooming line, but a unique one that today's men can

identify with. The following parts will go into more detail with the positioning of the product line named Renova Men.

6 Brand

6.1 Segmentation

Through segmentation the market is split “into distinct groups of homogeneous consumers who have similar needs and consumer behaviour, and who thus require similar marketing mixes” (Keller et al., 2012). In the process of market segmentation, the following variables were considered: geographic (country), demographics (age), psychographics (lifestyles, interests, opinions), behavioural (usage rate, loyalty, involvement) and benefits sought (value, status, convenience). Two distinct segments were established: “The new well-being men” and the “Traditional men”, as shown in the figure below. Different perceptions of masculinity and the consequent men’s grooming routines were used as the main differentiator factors between the two segments, which is translated into the variables mentioned earlier.

Segments/Variables “The New Well-being Men” “Traditional Men”

WHO

Geographic Living in Portugal

Demographic Men between 25 and 45 years old Men above 45 years old

Psychographic

- Image seeker: has concerns about the appearance;

- Wants to feel confident and

good about himself; - “Experiencer – Young, enthusiastic, impulsive people who seek variety and excitement.

Spends a comparatively high portion of income on fashion, entertainment, and socializing”

(The VALS Segmentation System: An eight-part typology

(as cited in Kotler & Keller (2016)).

- Believes a true man doesn’t need to take care of his

appearance;

- Doesn’t dare to move away from any traditional male

stereotype;

- “Believers – Conservative, conventional, and traditional people with concrete beliefs. Prefers familiar brands and is loyal to established brands” (The VALS Segmentation System: An eight-part typology (as cited in

Segments/Variables “The New Well-being Men” “Traditional Men”

WHAT Behavioural

- Motivation behind purchase: to take care of himself and feel

good;

- Uses a variety of different men’s grooming products; - Looks for new and innovate

products/brands. - Less price sensitive (looks for quality products able to provide

the desired look).

- Motivation behind purchase is necessity: only uses the products

he needs;

- Don’t have a complex grooming routine;

- Conservative attitude: uses always the same products from

well-known brands. - Has a certain level of price sensitivity (looks for quality but

at the cheapest price possible).

WHY Benefits Sought psychological) and sensorial - Well-being (Physical and gratification.

Functional benefits that get the job done for the basic grooming

needs. Figure 4 – Segments identified

6.2 Target

“Targeting involves evaluating the attractiveness of each market segment, selecting one or more segments to pursue, and then designing marketing programs to serve them” (Gupta, 2014). While deciding on which target(s) to serve, two factors must be considered: the segment’s overall attractiveness and the company’s objectives and resources (Kotler & Keller, 2016). Thus, following the recent trends predicting an increasing number of men having concerns about their appearance and consequently investing more in personal care and beauty products (Euromonitor, 2016 A), Renova Men is going to target “the new well-being men” segment, being the one with bigger potential growth and profitability, as well as the one with a better fit with the company Renova. The segment represents Portuguese men between 25 and 45 years old, who seek men’s grooming products that go beyond the functional basic needs, offering a sensorial gratification that creates joy using the product and makes them feel good about themselves.

6.3 Positioning

According to the Customer-Based Brand Equity model developed by Keller and others (2012), there are four questions one needs to answer in order to determine brand positioning: (1) who the target consumer is, (2) who the main competitors are, (3) how the brand is similar to the competitors, and (4) how the brand is different from them.

With the target consumer described above, the next step includes the development of a competitive frame of reference. To do so, one should start by establishing the category leading to the identification of the competing brands. As follows, Renova Men competes directly with the brands present in the men’s grooming sub-category, hence providing a line specifically designed for men, and indirectly with the brands that offer the same products inside different sub-categories of personal and beauty care such as the deodorant, skin care and bath and shower categories (e.g. unisex deodorants or shower gel) (Exhibit 21).

Right after it is necessary to identify the brand’s POPs. Using category POPs, these represent the necessary but not sufficient attributes or benefits, that a brand shares with the other brands present in the same product category (Keller et al., 2012). Considering Renova Men’s direct competitors, the POPs within the men’s grooming category lay on the hygienic and beauty functionalities, specially designed for men.

The last topic includes defining the brand’s PODs. In other words, determining on which attributes or benefits the brand is differentiated from the competitors, producing strong, favourable and unique associations in the consumers’ minds (Keller et al., 2012). Based on the quantitative research it was inferred that, besides necessity, the two main purchase motivators in the men’s grooming category are the desire to improve appearance and the positive feeling of using these products. Thus, Renova Men is focusing on the men’s well-being, described as the state “when individuals have the psychological, social and physical resources they need to meet a particular psychological, social and/or physical challenge” (Dodge et al., 2012).

Additionally, according to Hauser and Koppelman (as cited in Kotler & Keller, 2016), in order to understand the positioning of other brands competing in the men’s grooming sub-category and to identify unmet consumer needs, which can be translated in new marketing opportunities, the creation of a perceptual map (Exhibit 22) can be useful. Hence, as a first POD, by adopting a liberated masculinity approach, Renova Men inspires men to stay true to themselves instead of following any kind of stereotype, leading to their psychological well-being. Moreover, as a second POD, Renova Men offers a pleasurable experience that appeals to senses, underlined by the colourful and artistic male-shaped packaging, by the natural ingredients and the enjoyable and compatible fragrance between the different products, which in turn lead to physical well-being. The last is supported by the primary qualitative research which indicated that fragrance is one of the three main decisive factors while purchasing men’s grooming products, and that the mix of different smells from different grooming products represents a problem.

To summarize what have been described above, a positioning statement was developed. 6.4 Positioning Statement

To 25-45 years old Portuguese men, well-being and outer appearance concerned (Target), Renova Men is a brand of men’s grooming products that focuses on the men’s well-being (FOR) by inspiring them to stay true to themselves and by offering a pleasurable experience that appeals to the senses (POD). This happens due to the liberated masculinity approach, the colourful and artistic packaging, the enjoyable and compatible fragrance between the products and its natural ingredients (RTB).

Additionally, translating Renova Men’s PODs, a different positioning was made for each product of the line, which can be seen in exhibit 23.

6.5 Renova Men Brand Identity

“Identity draws upon the brand’s roots and heritage – everything that gives it its unique authority and legitimacy within a realm of precise values and benefits” (Kapferer, 2012). Renova Men brand identity was built based on Kapferer’s Brand Identity Prism Model (2012). Physical: Renova Men’s most salient features are the vivid colours of the products, together with the artistic packaging that will stand out in the shelves. Secondly, related with the product category, the image of a well-groomed man also represents an important physical component of Renova Men. Finally, Renova’s logo, associated with the brand’s quality.

Personality: If Renova Men were a person, it would be a man that truly enjoys taking care of himself, a man that enjoys looking good and tidy. Furthermore, it would be regarded as a young and genuine man, with an open-mind and willing to try new things.

Culture: This facet of the prism is consistent between Renova and Renova Men. A Portuguese company that, not being afraid of risk, was able to achieve national and international success through innovation and culture of “why not?”. Moreover, a company that supports people genuineness, inspiring people to show their true colours and be just like they are.

Relationship: The main goal of Renova Men is to offer its customers a pleasant and trustful grooming experience. The brand aims to provide fun and cleanliness through products that will allow consumers to feel good while using them. A brand that promises commitment to its customers and that can be trusted.

Customer Reflection: The perceived type of costumer of Renova Men represents authentic and liberated men, confident of who they are. The typical consumer should be a man with a little bit of sexiness and mystery inside them and someone who appreciates to experience new things. Self-Image: While purchasing/using Renova Men’s products, there are several feelings that should stand out: “I feel inspired to be myself”, “I feel well”, “I feel that I’m taking proper care

of myself”, “I feel powerful and sexy”. Renova Men is a brand that emphasizes men’s well-being (Exhibit 24).

7 Product

7.1 Range Policy

Derived from the outcome of the presented project, Renova will launch a men’s grooming product’s line under the name of the brand - Renova Men. It will develop the brand through a brand category extension: it will extend the existing brand name to a new product category, launching men’s grooming products.

Thus, when expanding its business to other categories, Renova has to make three product-mix decisions, as presented below.

7.2 Product Mix Breadth

It is of importance to understand the product mix of a company, meaning the complete set of all products a business offers to a market. This is made up of both product lines and individual products (Boundless, 2016). Hence, the product mix breadth “refers to the variety and number of product lines offered” (Dolan, Product Policy, 2015). Having this said, regarding the product breadth of Renova, the brand is currently concentrated on a single product category, namely the tissue and hygiene category. The presented work project expects Renova to offer a completely different line focusing on men’s grooming products.

7.3 Product Line Depth

The product line depth is “the number of items in a given product line” (Dolan, Product Policy, 2015), or Stock Keeping Units (SKUs). Renova Men will offer 8 different products with different variations. However, Renova required to launch a maximum of 4 SKUs per year. Each product will have 2 variations to ensure visibility on the shelf. However, there is a difference regarding men’s post-shave, offering three variations, and the oil for beard with only one. The

reason is because the oil for beard is a new product to the market, and so it would be less risky offering only one variation. The sequence of launches (outlined in the table below) was determined by launching the products with the biggest market volume at the beginning, balancing the categories so that large categories would be entered early on.

SKU / Year Oil for beard Post-Shave Balm Deodorant Roll On Deodorant Spray Post-Shave Gel Post-Shave Lotion Anti-Ager 1st wrinkles Complete Anti-Aging 1 ✓ ✓ ü ü 2 ü ü ✓ ✓ 3 x 4 SKU / Year Fresh facial moisturis er Facial moisturizer for sensitive skin Pre-Shave Gel Pre-Shave Foam Bath and shower gel extra fresh Bath and shower gel sensitive skin Body Moisturizer fast dry Body Moisturiz er sensitive skin 1 2 3 ✓ ✓ ✓ ✓ 4 ✓ ✓ ✓ ✓

Figure 5 – SKUs per year

However, there are exceptions to this logic concerning the beard oil, the pre-shave and the aftershave. The beard oil was included in the launch year due to its innovative character. The aftershave will start with 1 SKU in the first year adding 2 more SKU in year two. This is done to accommodate the launch of deodorants in order to start with 3 products instead of 2 products yet still staying within 4 SKUs. The launch of the pre-shave is delayed to a later stage to

establish the brand first to have a stronger position to face the market leader Gillette in one of their core products.

Spreading the launch of the products across several years is also done because as items are added, costs arise for design and production, inventory carrying, order processing transportation and promotions (Kotler & Keller, 2016). In addition, this approach enables Renova Men to lengthen the men’s grooming line or add more product variants in the future, offering constantly new products that satisfy consumers’ needs and wants.

7.4 Product Item Design

The next decision to make is referring to the actual specifications for the items that will be developed and sold within each product line (Dolan, 2015). In this section two topics will be developed: intrinsic characteristics of the product and design policy and packaging.

7.5 Intrinsic characteristics of the product

These are the real, objective and observable attributes that can be classified into three categories: the formula of the product, its performances and its external visual aspects (Lendrevie et al., 2015). Thus, the formula of the products will be the chemical ingredients that are used for the product’s composition and these are determined by the supplier and Renova, in accordance to the desired performance. According to the concept of the line the products will feature natural ingredients (a differentiation between natural and organic products is provided in exhibit 25). The product development will also include the fragrance development. The fragrance will be the same for all products and it will be classy, fresh, natural and sensual, that consumers associate with luxury and premium brands, which it is not overpowering but long lasting. The perfume will be the same for all products, since this was something that our interview respondents pointed as something positive. The visual aspects are related to the packaging, and so those will be specified in more detail in the next topic. Regarding performance, the figure below presents the specificities for each item of the line which were

derived from secondary data analysis and taking into account the competitors’ products’ performances.

Performance Men’s

Post-Shave Soothes and repairs irritated skin. Pleasant fragrance.

Oil for Beard Make beards shiny and soft and healthy. Stimulates beard growth. Pleasant fragrance. Men’s Facial

Moisturiser

Makes the skin look good through protection and making skin healthier. Makes skin soft and not dry. Pleasant fragrance.

Men’s

Anti-Agers Prevents and reduces wrinkles and fatigue. Pleasant and discreet fragrance. Men’s Body

Moisturiser

Protects and avoids dry skin, giving a good a healthy look. Dries fast. Pleasant fragrance.

Men’s Bath and

Shower Ensure cleanliness. Pleasant fragrance.

Men’s

Deodorants Pleasant fragrance and long lasting protection against odours. Men’s

Pre-Shave

Makes shaving easier. Provides a comfortable and refreshing shaving experience. Avoids dry and irritated skin after shaving. Pleasant fragrance. Figure 6 – Products’ Performance

7.5.1 Design policy and packaging

Design refers to “the totality of features that affect the way a product looks, feels, and functions to a consumer” (Kotler & Keller, 2016). One of the main aspects in regards to design relates to the package. It includes “all the activities of designing and producing the container for a product” (Kotler & Keller, 2016). Renova Men will feature a highly recognizable and artistic packaging design that will help the brand to stand out from the competition. Please refer to exhibit 26 to see examples of this artistic packaging (bear in mind that the package features should be developed by a professionals and that the ones presented are only examples).

7.5.1.1 Package conception

It refers to the elements that are supposed to help in the protection, conservation, use and storage of the product (Lendrevie et al., 2015). One of the important features of the product's package is the materials used which will be plastic for the whole line. This is a less costly material, makes the product lighter and less prone to breakage and, on the contrary of glass, there is no need for protections and it saves space in the shelves.

The exhibit 27 depicts another two important features of each product’s package related to the conception, which are the package shape and size. The package shape for almost all products will be similar to a male body, as already shown in the concept description, with the exception for the men’s facial moisturizer and men’s anti-agers which will be cylindrical shaped, because these are smaller bottles and designing a male body will be difficult. The sizes of the packages were determined taking into account the offerings from the competition and are presented in ml.

7.5.1.2 Decoration

It refers to the purely visual elements of the package (Lendrevie et al., 2015). The Renova Men line will be very simple in terms of graphics. There won’t be any pictures neither drawings on the label. Therefore, the logo/brand name, the name of the product and variation, the purpose of use, the expiry date and the ingredients will be the only present elements. The colours are a particularly important aspect for Renova Men’s grooming line, as already mentioned. Thereby, each of the 8 products will have a different colour.

The proposed colour scheme should comprise bright and bold hues similar to the ones used in Renova Red Label products, as a way of making a connection to the mother brand.

8 Pricing

8.1 Pricing Strategies

Price is the element of the marketing mix that captures the value created by the other elements, and it “can have a substantial impact on sales, profitability and market share” (Warc Best Practice, 2016). Thereby, by following a value-based pricing approach that will capture that value, a neutral pricing strategy will be implemented to all the products with the exception for the beard oil and the men’s anti-agers, that will follow a skim pricing strategy. The reason for this exception is that for the beard oil Renova Men will be a first mover for the channel in which it operates, and in regards to the men’s anti-agers, Renova Men will develop an offer covering the entire male segment: a 1st wrinkles product for the younger part of the customers’ segment,

and a complete anti-aging for the older customers. 8.2 Neutral Pricing Strategy

The neutral strategy entails following a value-based focus, meaning the coordination between the competition, the costs and the value perceived by the customers. “This cross-functional focus requires a balance between the customer’s need to obtain good value for the price and the firm’s need to cover costs and earn a suitable profit” (Nagle & Hogan, 2011).

In this sense, Renova already has defined the market segment and the benefits the potential customers seek. In the following, the price the customers can be convinced to pay will be established. In the final stage, Renova is going to challenge its producer to develop the products at a cost low enough to serve that market segment profitably (Nagle & Hogan, 2011). The way to capture the key elements of value-based pricing strategy is through the Value-Pricing Thermometer (Exhibit 28).

8.2.1 True Economic Value

The TEV “is the value that a fully informed buyer would or should ascribe to the product” (Dolan & Gourville, 2014) and is computed as follows:

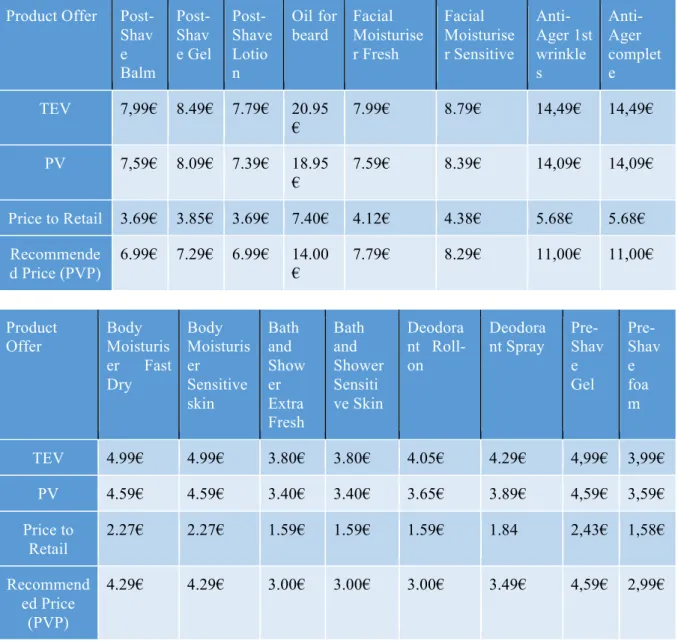

TEV = cost of the next-best alternative + value of the performance differential The way to assess TEV takes into account the cost of the next-best alternative (the reference value), which in the case of Renova Men is Nivea Men, and the value of the performance differentials (see exhibit 29 for the main assumptions). Thereby, the premium assumed will be of 1€ with the exception for beard oil and anti-agers, as we will see next. For the TEV values for each SKU please refer to exhibit 30. Note that these values of TEV mean that a fully informed, rational buyer should be indifferent between the next-best alternative and the new product under this cost structure. However, buyers are not fully informed and are not rational buyers, therefore it is important to understand the PV.

8.2.2 Perceived Value

The PV “is the perceived value of the product in the mind of the consumer” (Dolan & Gourville, 2014). The way to calculate the PV is as follows:

PV = cost of next-best alternative + perceived value of performance differential Therefore, in order to assess a customer’s PV it is needed to look to the major findings of the second qualitative research presented in the report, and understand the customer’s belief about the specific benefits offered by Renova Men products. See exhibit 31 for the PV for each SKU.

8.2.3 Sourcing Costs

The sourcing costs generally act as a price floor and “represent a lower bound on the price an organization would be willing to set” (Dolan & Gourville, 2014) (Palmeira, 2016). Since Renova Men will outsource the production, in order to come up to the sourcing costs the process applied was: define the price to the consumer, which was based taking into account the current

prices of the market competitors and the maximum price consumers are willing to pay (that were determined in the previously conducted research), then taking out VAT of 23%, taking out the retail margin of 35%, taking out the margin for Renova Men of 50%, and in the end establish a cost for the sourcing of the product (see exhibit 29 for the main assumptions). It is important to bear in mind that these sourcing costs are the costs from the producer to Renova, which do not include the transportation costs from Renova to the retailers. The computations for deriving the sourcing costs can be seen in exhibit 32.

Having this said, the recommended prices per SKU are presented in the figure below and Renova Men will be able to achieve a 50% margin.

Product Offer Post-Shav e Balm Post-Shav e Gel Post-Shave Lotio n Oil for beard Facial Moisturise r Fresh Facial Moisturise r Sensitive Anti-Ager 1st wrinkle s Anti-Ager complet e TEV 7,99€ 8.49€ 7.79€ 20.95 € 7.99€ 8.79€ 14,49€ 14,49€ PV 7,59€ 8.09€ 7.39€ 18.95 € 7.59€ 8.39€ 14,09€ 14,09€ Price to Retail 3.69€ 3.85€ 3.69€ 7.40€ 4.12€ 4.38€ 5.68€ 5.68€ Recommende d Price (PVP) 6.99€ 7.29€ 6.99€ 14.00 € 7.79€ 8.29€ 11,00€ 11,00€ Product

Offer Body Moisturis

er Fast Dry Body Moisturis er Sensitive skin Bath and Show er Extra Fresh Bath and Shower Sensiti ve Skin Deodora nt Roll-on Deodora

nt Spray Pre-Shav e Gel Pre-Shav e foa m TEV 4.99€ 4.99€ 3.80€ 3.80€ 4.05€ 4.29€ 4,99€ 3,99€ PV 4.59€ 4.59€ 3.40€ 3.40€ 3.65€ 3.89€ 4,59€ 3,59€ Price to Retail 2.27€ 2.27€ 1.59€ 1.59€ 1.59€ 1.84 2,43€ 1,58€ Recommend ed Price (PVP) 4.29€ 4.29€ 3.00€ 3.00€ 3.00€ 3.49€ 4,59€ 2,99€