THIS REPORT WAS PREPARED EXCLUSIVELY FOR ACADEMIC PURPOSES BY PEDRO PEREIRA, A MASTERS IN FINANCE STUDENT OF THE NOVA SCHOOL OF BUSINESS AND ECONOMICS.THE REPORT WAS SUPERVISED BY A NOVA SBE FACULTY MEMBER, ACTING IN A MERE

ACADEMIC CAPACITY, WHO REVIEWED THE VALUATION METHODOLOGY AND THE FINANCIAL MODEL.

M

ASTERS IN

F

INANCE

After a careful evaluation, our investment recommendation for Adidas AG is BUY, with a target price of EUR 222.33, while the current stock price trades at EUR 167.15.

For the last 3 months, the stock decreased 13%, which represents a good opportunity to buy the stock.

Share: The company stock price clearly outperformed the

German stock index DAX-30, yielding a total return of 173% in the last three years. This development was mainly driven by the continuously release of strong financial performances (revenue growth rate of 16% and 14% in 2015 and 2016, respectively) Growth: Adidas is focused to increase sales growth by

driving brand desirability through product innovation, as well as by focusing on several strategic growth areas such as womenswear, athleisure, e-commerce, greater penetration of the North America and Greater China market. The company is also committed to improve margins in order to close the gap to its major rival, Nike (EBITDA margin of 16% vs 8% for Nike and Adidas, respectively) Valuation: The YE18 price target is based on a DCF

analysis of Adidas. The price target of EUR 222.33 implies a 33,0% mark-up and a total expected shareholder return of 34,2% on the current share price.

Company description

Adidas Group, with headquarters in Herzogenaurach (Germany) is the largest company in the sports footwear and apparel industry in Europe and the second largest in the world. With total revenues of EUR 19.3 billion in 2016, its product range covers the entire spectrum of apparel and footwear goods from casual sportive fashion to high performance products for competitive athletes.

ADIDAS

AG

C

OMPANY

R

EPORT

F

OOTWEAR AND

A

PPAREL

3

J

ANUARY2017

S

TUDENT

:

P

EDRO

P

EREIRA

[email protected]

Sustaining “Brand Momentum”

Riding the Athleisure and E-commerce trend

Recommendation: BUY

Price Target FY18: 222.33 €

Price (as of 31-Dez-17) 167.15 €

Bloomberg: ADS:GR 52-week range (€) 142.60-202.10 Market Cap (€b) 34.970 Outstanding Shares (m) 209.216 Source: Bloomberg In % based on 100% at 31th December 2014 Source: Bloomberg

(Values in € millions) 2016 2017E 2018F Revenues 19,291 21,529 23,743 EBITDA 1,855 2,329 2,730 EBITDA growth 30% 26% 17% Net Profit 1,020 1,075 1,526 EPS 4,87 5,14 7,29 Payout Ratio 39,6% 45,1% 39,7% Dividends per share 2,00 2,40 3,00 Net Debt 235 775 1,156 Net Debt/EBITDA 0,13 0,33 0,42 ROIC (%) 17,0% 21,0% 22,6% Source: Adidas AG Annual Report 2016, Bloomberg, own estimates

ADIDAS AG COMPANY REPORT

Table of Contents

ADIDAS CASE ... 3

COMPANY OVERVIEW ... 4

COMPANY DESCRIPTION ... 4 BRAND OVERVIEW ... 6 adidas ... 6 Reebok ... 7 SHARE PERFORMANCE ... 7SHAREHOLDER STRUCTURE AND RETURN ... 8

INDUSTRY OVERVIEW ... 9

SECTOR ANALYSIS... 9 PEER COMPANIES ... 10KEY DRIVERS ...13

Athleisure Trend ... 13 Womenswear ... 14 Digital and Ecommerce ... 15

“Speed” ... 15

Marketing Investments ... 16

Economic Drivers ... 17

“Creating the New” ... 19

FORECASTS ...19

REVENUES ... 19

EXPENSES ... 21

NET WORKING CAPITAL AND CAPEX ... 22

VALUATION ...23

COMPARABLE COMPANY ANALYSIS ... 23

DISCOUNTED CASH FLOWS ANALYSIS ... 23

WACC Calculation ... 23

Perpetual Growth ... 25

SENSITIVITY ANALYSIS ...25

SCENARIO ANALYSIS ...26

APPENDIX ...27

ADIDAS AG COMPANY REPORT

Adidas Case

Adidas Group, with headquarters in Herzogenaurach (Germany) is the largest company in the sports footwear and apparel industry in Europe and the second largest in the world (7,8% of market share - see figure 21). With total revenues of EUR 19.3 billion in 2016, its product range covers the entire spectrum of apparel and footwear goods from casual sportive fashion to high performance products for competitive athletes.

In March 2015, Adidas presented a new acceleration plan called “Creating the New” that raised Adidas’ growth expectations. Actually, due to the strong start of the strategy (EUR 19.3 billion vs EUR 16.9 billion net sales and 7.7% vs 6.5% operating margin in 2016 and 2015, respectively), the company introduced more ambitious growth targets. The new bullish forecast to 2020 (10-12% vs high-single digit sales growth per year, EUR 22 billion vs EUR 25-27 billion net sales, 11% vs 9,9% operating margin and 20-22% vs 15% EPS growth per year) are clearly possible and credible given the current brand strength, CEO Kasper Rorsted’s reputation for operational improvements and clear potential to improve direct distribution.

However, all these objectives rely on great execution, continued strength in both sportswear and sports lifestyle markets, no negative impact from any potential US border tax, no significant negative currency effects and no significant fightback by global peers (Nike and Under Armour) or the significant niche brands (such as Puma) or local players in markets such China (Li Ning).

The company’s biggest competitor is Nike, mainly due to its dominant market position in the US, the industry’s most lucrative and important region (36% of total sportswear consumption). Adidas has been successfully gaining market share in this region by altering its strategy, which appears to be paying off (+27% sales growth in the third quarter of 2017). Conversely, Nike has been investing more in other regions driven by their high dependence of US market (44% of total revenues).

The target price was calculated through a DCF model. The valuation leads to a buy recommendation, with a target price of EUR 222.33 for Adidas’ shares, representing an upside of 33,0% on the current stock price and a total shareholder return of 34,2%.

BUY recommendation with EUR 222.33 target price

Second largest company in the sports footwear and apparel industry

More ambitious growth targets after a strong start of the strategic plan “Creating the New”

Several risks associated to the company’s growth strategy

Biggest competitor is Nike, which dominates the US market

ADIDAS AG COMPANY REPORT

Company Overview

Company description

The Adidas Group is a German based company that designs, develops, produces and markets athletic and sports lifestyle products worldwide. With more than 60.000 employees in over 160 countries, the company produces more than 850 million product units every year.

In 1949, the company was registered by Adolf Dassler after a disagreement with his brother Rudolf, who ended up creating Puma. The “three parallel bar” brand rapidly gain the trust of world-class athletes through decades, being the footwear for gold medals winners in Olympic Games, apparel for record breakers and responsible for the creation of the official match ball for the 1970 FIFA World Cup and several other competitions that followed.

After the end of the Dassler family control, in 1987, questionable strategic decisions put the company near bankruptcy with a record loss in 1992. Three year afterward, the company went public and, as the new century started, a new lifestyle segment was introduced, focusing on sport-inspired streetwear in addition to its sport performance products, being the pioneer in the industry. Several collaborations were established with famous designers and athletes such as Yohji Yamamoto and David Beckman in order to prove that “impossible is nothing”, one of the most memorable marketing campaigns for sports lovers.

Throughout the years, the company tried to grow by doing major acquisitions and just from that moment onwards through organic growth. In 2006 Adidas acquire its British rival Reebok for UDS 3.8 billion, in order to increase its market share in the North America market. In 2011, the company acquired outdoor specialist Five Ten for USD 25 million, and through the acquisitions of Ashworth in 2009, TaylorMade in 2011 and Adam Golf in 2012, Adidas gained access to the golfing market. More recently, the acquisition of Runtastic GmbH by EUR 220 million, an Austrian based fitness app-maker which tracks and manages health and fitness data, allowed the company to enter in the digital market.

However, included in the “Creating the New” plan, the divestiture of Mitchell & Ness as well as the decision to exit the golf and hockey business through the sale of TaylorMade, Adams Golf, Ashworth and CCM Hockey brands, marked a change in the growth strategic plan. This allows the company to reduce the complexity in their brand portfolio and to focus even more strongly on the core competencies in the areas of footwear and apparel with just the Adidas and Reebok brands.

Divestiture in brands in order to reduce brand portfolio Adidas brand linked to sports world-class events and athletes

Introduction of sport-inspired streetwear segment

Major acquisitions in order to gain market share in specific market segments

ADIDAS AG COMPANY REPORT

Figure 1: Sales by brand

Figure 2: Sales by product category

Figure 3: Sales by geographical region

Figure 4: Footwear production by region

Business Overview

The company separates its business by brands, product category, geographical region and distribution channels in order to tackle different markets and customer targets at the same time.

As can be seen from figure 1, the company’s original brand adidas is the biggest source of revenue which accounts for 85% of total group’s revenues with EUR 16.3 billion. Currency-neutral revenues for adidas brand increased 22% in 2016 mainly driven by double-digit sales increase in training and running categories as well as high-single-digit sales increase in football category. Reebok brand accounts for 9% of total sales with EUR 1.8 billion and currency-neutral sales were up 6% in 2016 versus the previous year. Other businesses include all the other brands.

In terms of product category, Adidas separates its revenues by footwear, apparel and hardware. Footwear accounts for 53% of the group’s revenues and in the recent years it has registered a strong increase, especially in the casual athletic category which continued to yield high growth rate in the last two years (double-digit growth). Regarding the other categories, the apparel represents 39% of the total group’s revenues but even though it has increased from the previous year, it has lost some importance in terms of share in relation to the value for Adidas. Finally, the hardware, which includes bags, balls, watches or fitness equipment, is the smallest category in terms of revenues accounting around 8% of the group’s revenues (see figure 2).

As per the regional distribution, Western Europe continues to be the core-market generating about 30% of total revenues, followed by North America (21%), Greater China (16%) and MEAA1 (14%) (see figure 3). In 2016, currency-neutral revenues increased in all regions, with emphasis for Greater China (28%), North America (+24%) and Western Europe (+20%). Russia/CIS registered the lowest currency-neutral revenue growth with +3%.

To minimise production costs, Adidas outsources almost 100% of manufacturing, primarily located in Asia. The company also operates a limited number of own production and assembly facilities in USA (4), Canada (3) and Germany (1). Asia accounts for 97% of footwear volume produced (see figure 4), where Vietnam represents the largest sourcing country (42%), followed by Indonesia (24%) and China (22%). Regarding apparel, Asia produced 93% of the total volume produced (see figure 5) but, in this case, China is the largest source country (27%), followed by Cambodia (22%) and Vietnam (17%).

ADIDAS AG COMPANY REPORT

Figure 6: Sales by distribution channels Figure 5: Apparel production by region

Figure 7: CAPEX by region

Figure 8: Other Operating Expenses

In order to distribute the products produced to the clients, Adidas AG relies on three different distribution channels: wholesale, retail and e-commerce. The biggest part of revenues is generated through wholesale, contributing 64% in 2016. The retail and e-commerce channels accounted for 31% and 5%, respectively (see figure 6). Adidas’ network is composed by 2.800 own-retail stores, more than 12.000 mono-branded franchise stores, over 120.000 wholesale doors and more than 50 own e-commerce sites.

The majority of the company’s capital expenditure is related to controlled space initiatives. In 2016, these investments in new or remodelled own-retail and franchise stores accounted for 55% of the total capital expenditure, followed by IT, administration and logistics with 10%, 9% and 8%, respectively. From a regional perspective, just the company’s headquarters in Herzogenaurach, Germany, accounted for 33%. In addition, Greater China, North America and Western Europe were the regions where the company invested more with 15%, 13% and 12%, respectively (see figure 7).

In 2016, other operating expenses were mainly comprised of point-of-sale and marketing investments, which represents 31% of total amount spent, and operating overhead expenses, which include marketing, logistics, sales force, administration and R&D related costs, accounts for 59% (see figure 8). The first category consists of expenses to support company’s development at the point of sale, promotion partnerships, advertising, public relations and other communication activities, while the second category refers to expenses associated with running the business.

Brand Overview

As aforementioned, the Group separates its business through two main brands, adidas and Reebok. Known as “The Badge of Sports” and “House of Fitness”, both brands have a clear core focus in the sports and fitness world, respectively.

adidas

The original brand, adidas, is separated into other several sub-brands. Adidas

Sport Performance has a clear focus on sports athletes, developing products

that are able to boost their performance. Its products cover a wide range of sports such as football, basketball, running, baseball, American football, etc.

Adidas Originals and adidas neo are focus on sports fashion lifestyle products.

While the first one brings the “iconic DNA from the courts to the street”, the latter is focus on trending fashion products. All together, they generated EUR 16.3

ADIDAS AG COMPANY REPORT

Figure 9: Revenue Adidas brand (EUR billion)

Figure 10: Revenue Reebok brand (EUR billion)

Figure 11: Adidas vs market indices

Figure 12: Peer comparison

billion of sales in 2016. In the last four years their revenues increased by 48% (see figure 9).

Reebok

The American fitness-inspired company Reebok was acquired by USD 3.8 billion in 2006, in order to increase Adidas market share in the North America market and to expand its brand portfolio. It offers a wide range of specialised products for the categories fitness training, studio, classics, fitness running and walking. The brand generated EUR 1.8 billion of sales in 2016 and in the last few years it has been struggling to increase its revenues, with a growth of 14% for the period 2013-2016 (see figure 10).

Other businesses include all the others brands such as Runtastic (fitness app),

Five Ten (outdoor climbing products), as well as other business activities of the labels Y-3, collaboration with the Japanese designer Yohji Yamamoto, and Porche Design Sport. This segment generated EUR 1.5 billion sales in 2016.

Share performance

In November 1995, Adidas went public by raising 1.8 billion marks in an issue that was 10 times oversubscribed. Since then, the company has been listed on the Frankfurt Stock Exchange (Deutsche Börse) and three years afterwards its share was included in the German stock market index DAX-30. Nowadays, Adidas share is included in several stock indices, among them the MSCI World Textiles, Apparel & Luxury Goods and, as of September 16, 2016, the EURO STOXX 50 Index.

Over a 5-year period, Adidas share price registered a compound annual growth of 20%, while the DAX-30, MSCI World Textiles, Apparel & Luxury Goods and EURO STOXX 50 ranked behind with 11%, 9% and 6%, respectively (see figure

11). Comparing with its peers, Adidas outperformed Nike, Puma and Under

Armour which had recorded a compound annual growth of 19%, 10% and 3%, respectively. From figure 12, one can conclude that this result was mainly driven by Adidas strong performance and, conversely, the weak performance of Nike and Under Armour since the year of 2015, establishing a turning point within the industry. This development was driven by the continuously release of strong financial performances, which supports the successful execution of the strategic plan “Creating the New”, the consequently increase of the company’s outlooks, as well as the positive impact of the CEO succession and the inclusion in the EURO STOXX 50 Index. As a result, the Adidas AG share reached a new all-time high of EUR 199.95 on August 4, 2017.

ADIDAS AG COMPANY REPORT

Figure 13: Shareholder structure

Figure 14: Shareholder structure by region

Figure 15: Dividend policy

Shareholder Structure and Return

The current shareholder structure of Adidas AG has more than 60.000 shareholders and it is mainly comprised by institutional investors, who represent the largest investor group, holding 87% of shares outstanding and private investors and undisclosed holdings, accounting for 8%. Adidas currently holds 4% of the company’s shares as treasury shares, reflecting the share buyback programme and, lastly, current members of the Executive and Supervisory Boards hold less than 1% (see figure 13).

In terms of geographical spread of shareholders, North America market accounts for 40% of institutional investors, followed by the UK, France and Germany with 21%, 9% and 8% respectively (see figure 14). There is no investor holding a majority of the voting rights. BlackRoc, Inc., Elian Corporate Trustee Limited and FMR LLC are biggest institutional investors with 7,38%, 5,71% and 5,31% respectively.

The group’s dividend policy aims to distribute 30%-50% of its annual earnings to shareholders. In the past few years, Adidas was able to increase the payout ratio, reaching 39,6% in 2016, corresponding to EUR 2.00 dividend per share (see

figure 15). The company does not have outstanding preferred shares.

In 2014, the company announced a share buyback programme of up to EUR 1.5 billion. The purpose of the programme was to repurchase shares in order to reduce capital and to meet obligations that could arise from the potential conversion of the convertible bonds issued at the same year with maturity until June 2019.

ADIDAS AG COMPANY REPORT

Figure 17: Industry Sales by region Figure 16: Industry Sales Forecast (USD

billion)

Figure 18: Industry sales forecast by region

Industry Overview

Sector Analysis

Adidas Group is included in the apparel, footwear and accessories design industry, which is estimated to have total revenues of EUR 353 billion in 2017, according to Bloomberg. This industry is strongly fragmented not only because the numerous smaller players active in the market but also due to the fact that some corporation’s revenues come from several products categories (VF Corp for example) and, hence, just a share are included in the industry’ revenues. Thus, in order to have an accurate analysis of the industry that Adidas are integrated, one must take into consideration just the athletic footwear and apparel industry, also known as Sportswear industry. According to the Societe Generale’s report2, USD 282 billion were spend on sportswear in 2015. From 2010 to 2015, this industry has grown at a CAGR of 6% and is forecasted to reach USD 365 billion in 2020, implying a 2015-2020 CAGR of 5.3% (see figure 16). According to another market research, Euromonitor International, this market will reach USD 357 billion in 2021, implying a CAGR of 5.1%.

As per geographical region, North America represents the largest market with more than one third (36%) of the total consumption, followed by Asia and Western Europe with 23% and 21%, respectively (see figure 17). The same report also forecast the growth rate per region for the period 2015-2020. Comparing to the growth registered in the previous period (2010-2015), it is expected to accelerate in Asia and EMEA (Europe, Middle East and other Asian markets). Conversely, it is expected to decelerate in North America and Latin America (see figure 18).

ADIDAS AG COMPANY REPORT

Figure 19: Number of health and fitness clubs (thousands)

This industry is very appellative due to its attractive growth trends, which have been driven by the rise of athleisure, increasing global concerns regarding healthy lifestyles and higher sports participation rates. A prime example of this sportive movement is the increase of the number of health and fitness clubs. In 2016, there were over 201 thousand health clubs worldwide, a significant increase from the 128 thousand in 2009 (see figure 19). The fact that the so called stars of the sports are gaining more and more recognition and icon status, the large coverage by TV channels and internet also contributes for this positive momentum of the industry.

Since the industry is highly segmented and competitive, the barriers of entry are high, as the existing competition has high bargaining power. Adidas and Nike have a really strong market position (see figure 21), taking advantage of long-standing relationships with distributors, clients, retails and suppliers. In order to have a chance of establishing in this market, next to these apparel and footwear giants, it is vital to create something new and innovative. Under Armour and Lululemon Athletica are two examples of companies who were successful in their niche, tight-fitting synthetic t-shirts and yoga pants, respectively, and from that moment thereon, they were able to increase their product portfolio and establish a solid position within the market, although still far away from Adidas and Nike. As such, one can conclude that customers are quality sensitive, since they are more and more interested in the use of advanced materials and technologies that could increase not only their performance but also their experience while wearing the products on a daily basis. Thus, having a well-established brand that customers trust due to their continuously release of innovative and fashionable products is a sustainable competitive advantage that Nike and Adidas enjoy and differentiate them from the competition.

Peer Companies

A broad list of companies that share key performance drivers and business characteristics is obtained and investigated thoroughly in order to select the closest comparable firms for further analysis. These companies, identified in

figure 20, were generated from Bloomberg. This list is composed only by

publicity listed companies, sorted by 2016 revenues.

As stated before, Adidas is the largest company in the sports footwear and apparel industry in Europe and the second largest in the world. So, based on the companies’ reports and Societe Generale Report industry’ estimation, one is able to reach the market share of each company.

Figure 20: Athletic footwear and

apparel companies In EUR B Revenue Nike 29.25 Adidas 19.29 VF Corp 10.86 Under Armour 4.36 Puma SE 3.63 ASICS Corp 3.32 Skechers USA 3.22 Amer Sports Corp 2.62 Columbia Co 2.15

Li Ning 1.09

High bargaining power of well-established companies (Nike and Adidas)

ADIDAS AG COMPANY REPORT

Figure 21: Industry market share

It is observable that the main competitor of Adidas is, by far, Nike. In addition, there are some other competitors in the market which are smaller in size such as, VF Corp, Asics, Puma, Under Armour and Skechers, operating mainly in the US and European countries, while in Asia, Li Ning is the main rival.

In order to identify the closest comparable companies, several firms from the above list were eliminated due to their small size and others were removed due to its current unique market focus, either in terms of product categories (eg: Asics in footwear) or geographical region (Li Ning in Asia). Finally, the firms that share most business attributes are the following: Nike, Puma, Under Armour and Skechers.

Nike Inc. - Considered the most valuable brand among sports business, this

American multinational corporation is engaged in the design, development and manufacturing and sales of footwear, apparel and accessories. Nike’s dominant position in the North America market, which is considered the most valuable region within the sporting goods industry have been allowing the company to have a big advantage against its competition .The company was founded in 1964 and has currently a market capitalisation of EUR 85 billion. With total revenues of USD 32.4 billion in 2016, the company aims to reach USD 50 billion sales for the year 2020.

Puma SE - This German multinational company also designs and manufactures

athletic and casual footwear, apparel and accessories products. Founded in the same year of Adidas, 1949, after the family disagreement that resulted into the creation of Adidas and Puma, quickly became business rivals since then. Currently has a market capitalisation of EUR 5.5 billion and total revenues of

ADIDAS AG COMPANY REPORT

Figure 22: Financial performance (EUR billion) and margins (%)

EUR 3.63 million in 2016, 14% higher than the previous year. In 2017, the company raised its outlook for sales and operating earnings for the third time, enjoying a revival especially in the US market.

Under Armour Inc. - This American group was founded in 1996 by a former

University football player which originally started with a simple plan to make superior quality t-shirts. Nowadays, it is a global corporation that manufactures sports and casual footwear and apparel products with EUR 5.1 billion of market capitalisation and total revenues of USD 4.83 million in 2016. The company, which has been seen as the biggest up-and-comer in this industry, having counted almost seven straight years of 20% or better sales growth, already cut its 2017 full year sales forecast twice, presenting a 5% decline in revenues in the third quarter of 2017.

Skechers Ltd. - It is an American corporation that offers lifestyle and

performance footwear for men, women and children. Founded in 1992, the company is one of the fastest growing footwear companies recording impressive sales growth year over year (higher than 100% in some years). Currently has a market capitalisation of EUR 5.0 billion and total revenues of EUR 3.22 million in 2016, 12% higher than the previous year.

When analysing the financial performance of these five companies, one can easily point out that Nike has the leading position within the group. Together with Adidas, their aggregate revenue accounts for 82% of the total revenues of the group. Regarding margins, Nike continues to yield better results regarding EBITDA margin (16%) and income margin (12%). On the opposite side, Puma presents the worst margins, both in EBITDA (5%) and net income (2%).

ADIDAS AG COMPANY REPORT

Figure 23: Peer comparison - Revenue growth rate

Figure 24: Category analysis of global apparel and footwear industry

From the figure 23, one is able to conclude that Under Armour and Skechers have been releasing some impressive results regarding revenue growth rate, with double-digit growth for four consecutive years. It is also important to emphasize the positive results of all the five companies in the last two years, reflecting the positive momentum of the industry.

Key Drivers

Identifying monitoring the key drivers of a business is extremely important in order to understand where growth is coming and, hence, allows for more reliable forecasts. These may arise from internal or external factors and from the

company’s ability to adapt from the latter. The following categories are some of key drivers that drive Adidas’ growth:

Athleisure Trend

Nowadays, “athleisure” is the hottest trend in the industry. The term stands for wearing sports gear outside the gym or while doing sports, such as at the workplace, at school, etc. Known as “Gym-to-the-office” clothes, this trend has becoming more and more acceptable and wide-spread across genders and geographies. While the customer is still accustoming to its comfortable fell, due to the improvement in materials and new manufacturing processes, demand is estimated to further increase leading to ample opportunity for companies to build a high-profitable business around this trend.

The report provided by the strategic market research Euromonitor International, points out that the sales of sportswear outpaced all other categories for three consecutive years, increasing 7% in 2016 (see figure 24). Although performance sportswear is still the leader in terms of market size, “sports-inspired is the category driving growth”, according to the report. Sports-inspired footwear registered an increase of 10%, reflecting the continued dominance of casual sneakers, while apparel increased by 6%.

The two main regions driving this growth are the USA, the world’s largest activewear market, and China with 40% and 37%3 of the total athletic-wear market in 2015, respectively. For Instance, in China, the share of population aged 6-69 that exercise at least three times a week rose 28% in 2007 to over 31% in 2014, according to the report from Morgan Stanley4. Moreover, the Chinese

3 Source: Euromonitor International

ADIDAS AG COMPANY REPORT

Figure 25: Category distribution for apparel industry

government is planning to develop sports infrastructures by 60% by 2025, making China a strategic key market-target for the following years.

Adidas has been able to capitalise the consumer shift away from regular apparel and footwear products to retro and lifestyle products (adidas Originals and adidas neo brands), stealing some market share from non-athletic apparel brands (see

figure 25)5. The relaunching of historic designs, such as Adidas Superstar and Stan Smith, and the development of new styles with modern details, such as the Kanye West designed “Yeezys”, were some of the company’s recent successful products.

Womenswear

The importance of women in the global sports sector has been significantly increasing, due to the fact that women are at the forefront of this athleisure trend by wearing yoga pants and other apparel outside of the sports spaces. Several innovations, such as the sport bra and the tank, have increase comfort while exercising and simultaneously their fashionable look creates an incremental driver for growth in the women’s market. This trend is also related to lifestyle, with activities such as yoga, zumba and spinning becoming even more common in health and fitness clubs, being one of the main reasons for its increase (see

figure 19)

According to Verdict report, almost 70% of women want activewear that is fashionable and stylish, whereas men are more interested in technical attributes. The same report also reveals that between 2010 and 2015 the women’s activewear market grew 26.1%, against 22.6% for men’s and forecasts that female related sales will increase 22.6% by 2020, against 19.9% for men’s. As such, it is imperative to focus on this tremendous growth potential market and, indeed, womenswear is one of the Adidas’ targeted growth areas. Currently, it represents 23% of Adidas’ revenues in 2016 and the company is committed to reach 28% by 2020. In order to achieve this goal, the company already started to create specific women design shoes, rather than adaptations of men’s shoes, and included a former Lululemon Athletica CEO to the Group as a strategic adviser, best known for being one of the pioneers of this athleisure era by creating yoga pants for women to wear all day. Besides, several partnerships were established with famous athletes, supermodels and fitness icons.

Nike, which is currently the market leader in both men’s and women’s activewear, according to NPD Group, is also capitalizing this athleisure trend, especially in women’s category. Currently, this category represents around 20% of Nike’s

ADIDAS AG COMPANY REPORT

Figure 27: Forecasted Retail Ecommerce sales (USD trillions)

Figure 26: Internet Users (billion)

revenues in 2016 (USD 6.6 billion) and the company plans to reach USD 11 billion sales by 2020. The opening of the first European women’s-only store in London and marketing campaigns focus on its women’s offering are some of the efforts made by the company in order to address this market.

Digital and Ecommerce

In 2015, Adidas acquired one of the most promising e-health start-ups, Runtastic, in order to compete against Nike+ and MyFitnessPal, Nike’s and Under Armour’s fitness apps, with the intention to expand its market position within the digital health and fitness space. This Austrian based fitness app-maker, has shown strong user growth with more than 70 million registered customers and 140 million downloads worldwide, as of 2015.

Beyond the possible additional revenue source from the app itself, which is negligent, the major reason for this acquisition was to use it as a revenue driver for the existing categories. Thus, through the app, the company ensures that its clients can use online platforms and, at the same time, promote its products. The high user engagement on mobile apps often leads to stronger brand connection and, consequently, additional sales.

Therefore, as part of this digital transformation, one of the possible distribution channels available is, indeed, e-commerce which grew 59% on currency-neutral basis in 2016. This rapid expansion takes advantage of the commercial opportunities across mobile technologies and the increase of internet users across the globe (see figure 26). Adidas plans to increase its e-commerce revenue from EUR 1 billion in 2016 to EUR 4 billion in 2020 and its main rival, Nike, also expects to increase its web sales from USD 1.2 billion in 2015 to USD 7 billion in 2020.

According to eMarketer report6, retail ecommerce sales will increase to USD 4.479 trillion in 2021, from its USD 1.859 trillion in 2016, of which China and USA, the most successful ecommerce nations, accounted for 69% of the global ecommerce sales. Nowadays, this distribution channel makes up 10.1% of total retail sales and it is expected to surpass 16% by 2021 (see figure 27).

“Speed”

Nowadays, sportswear companies, especially Nike and Adidas, are focused on increasing efficiency throughout its supply chain and production process, in order to decrease “speed to market”. It allows the company to react more quickly to changes in style and fashion and, at the same time, enables the company to get products to consumers faster, which, consequently, will have a positive impact on

ADIDAS AG COMPANY REPORT

sales. In 2016, newly launched products accounted for 72% of Adidas’ sales and, according to the company’s outlook, it is expected to increase until 2020. Moreover, this type of products exhibits higher gross margins (more full-price products) than those that have been on the market for more than a season, which will positively contribute for the outlined margin improvements established in the 2015-2020 acceleration plan “Creating the New”.

Booking orders with several months in advance is not representative of the current dynamic world trends. According to a Cotton Incorporated Lifestyle Monitor survey, 47% of consumers say they want their favourite apparel store to offer new styles once per month or more often. For people age 35 and younger, it increases to 65%.

As such, Adidas is creating a “flexible” supply chain, known as “Speed Factory”. By using 3D intelligent robots, they are able to bring production where the customer is and, hence, reducing significantly time to shops which is highly valuable in this fast desirability industry. Nowadays, the two existing plants (Germany and USA) do not even account for 1% of total production but it is expected that its importance will significantly increase in long-term (20% of the production in 2023). Nike is also working towards this technological production shift, by using powerful printing machines which allow them to produce photorealistic 3D image, which significantly reduce the time between designing and final production with nearly no prototyping needed.

Marketing Investments

The recent boost in sales (see figure 33) were also driven by important marketing investments on partnership assets, which represents almost half of its marketing investments (24% of other operating expenses) in 2016. The company intends to decrease this ratio of marketing investments spent on promotion partnerships to less than 45%, but it will nonetheless continue to bring its products to the biggest sport stages in the world.

FIFA World Cup, the UEFA EURO, the UEFA Champions League, the Roland Garros and the Boston Marathon are some of the major sports events on which Adidas plays an important role as tournament’s sponsor. It also is the main equipment supplier of many high-profile teams (Real Madrid, Manchester United and FC Bayern Munich) and endorse some of the world’s best and most recognised individual athletes (Leonel Messi and Paul Pogba in football and James Harden in basketball). Alongside with Nike, being Cristiano Ronaldo their most valuable partnership, both brands are at the centre of the battle to maximise the advertising and sponsorship for the majority for sports events.

ADIDAS AG COMPANY REPORT

Figure 28: Real GDP growth

Adidas has been an official partner of FIFA7 and UEFA8 since 1972, being responsible to supply the tournament’s gear and, as expected, the company will be one of the main sponsors of the WORLD CUP 2018 that will take place in Russia. Hence, adidas’ revenues will be propel by the event’s related products, especially in Europe and Russia/CIS. The company is also be the main kit sponsor (12 of 32 total teams) and has the best geographical representation with at least one nation from all five continents, where Europe is the most representative region (5 of 14 European teams).

In addition, the company has a significant number of strategic partnerships and collaborations with world famous designers such as Stella McCartney and Yohji Yamamoto, as well as with several personalities from the entertainment industry, including Kanye West, Pharell Williams and Rita Ora. All these efforts allow the company to have its logo visible in the tournament’s marketing and the brand linked to some of best and well-known high sports practitioners and famous personalities, enhancing the brand image worldwide.

Economic Drivers

By analysing the GDP growth rate, one is able to have a reasonable perspective of the economic conditions within each region where Adidas operates. As an additional market sign, the percentage of people at the age of 15-64 years was analysed.

Since 1986, GDP growth rate is around 3% on average per year, but the actual year-to-year growth rate is highly inconsistent throughout the years and across regions. Over the past 30 years, Asia were able to grow 6% on average, while the other regions grew at lower rates with 4% for Africa, 3% for North America and Latin America and 2% for Europe. Taking into consideration the differences between developed and developing economies, they yielded, as expected, different growth rates with 2% on average for the first group and 5% on average for the latter (see figure 28).

Nowadays, several geopolitical tensions and political discords such as the unexpected UK vote in favour of leaving the European Union (“Brexit”), the electoral outcome in the USA as well as the Russia/USA dangerous tension remained major sources of uncertainty. Nevertheless, accommodative monetary policies as well as improving labour market conditions support the overall economy growth.

7 International Federation of Association Football 8 Union of European Football Association

ADIDAS AG COMPANY REPORT Annual % change 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F World 7,3% 6,9% 6,3% 6,1% 6,8% 7,1% 7,1% 7,1% 7,1% Western Europe 1,7% 2,3% 2,2% 2,2% 3,6% 3,4% 3,4% 3,5% 3,5% North America 3,4% 4,4% 3,1% 2,9% 4,7% 4,6% 4,5% 4,2% 4,1% China 10,6% 9,4% 8,4% 8,8% 8,7% 9,1% 9,0% 9,0% 8,8% Russia 8,7% 8,6% 12,3% 6,8% 6,1% 5,6% 5,6% 5,6% 5,6% Latin America 7,6% 6,2% 5,6% 4,6% 5,5% 5,6% 6,0% 6,2% 6,2% Japan 2,3% 3,1% 1,9% 0,9% 1,9% 1,2% 1,9% 1,8% 2,0%

Middle East and Africa 12,3% 10,7% 9,7% 11,8% 11,9% 12,6% 11,0% 10,8% 10,5%

Nominal GDP growth by Geographical Area

Figure 29: Real GDP growth forecast

Figure 30: Nominal GDP growth forecast

Figure 31: % of population aging 15-64 years

According to the IMF outlook, the real GDP growth rate is expected to increase from the year 2017 onwards. For the year 2017 is expected a worldwide GDP growth of 3,6% and 3,8% from the year 2021 onwards. The World Bank prospects reveals more conservative projections, with an expected global GDP growth rate of 2,7% for 2017 and 2,9% for 2018 onwards. This development will be supported by a stabilisation in commodity prices, an uptick in consumer confidence, improvements in global trade and manufacturing activity as well as continuous accommodative fiscal and monetary policies.

Developing economies are forecasted to remain a major contributor to the global economic expansion in 2017 with a projected growth rate of 4,5%, which strongly contributes the Emerging and Developing Asia with 6,5%. Regarding the developed countries, GDP is expected to grow at 2,0% in 2017, where Western Europe and North America are expected to grow at a steadily rate of 2,0% and 2,2% in 2017, respectively (see figure 29).

Taking into consideration the inflation rate from IMF outlook, one was able to compute the expected nominal GDP growth rate for all regions where Adidas operates (see figure 30), which is considered to be the bottom regional revenue growth rate for some of the regions. Further explanation in the following chapter.

The target customers for the activewear industry are the people between the ages 15 and 64. This age group are at the forefront of this athleisure trend and together with the increase interest to do sports as a leisure activity or on a semi-professional level (see figure 19), makes them spend a lot of money on lifestyle and performance products. From figure 31, it is observable that the percentage is increasing worldwide, especially in Middle East & North Africa, Latin America and East Asia. In Europe and North America it is also increasing, but with a more modest growth.

ADIDAS AG COMPANY REPORT

Figure 32: Adidas’ growth targets for 2020 (EUR billion)

Figure 33: Adidas revenues (EUR billion)

“Creating the New”

In 2015, Adidas AG introduced a new strategic plan known as “Creating the New”, which defines the company’s strategies and targets until 2020. The company’s strategy is focused on improving top-line growth, market share, gross margins and operating leverage, taking advantage of the aforementioned key drivers and through company’s adjustments and improvements. As mentioned before (see page 3) these objectives were raised after the first year of implementation due to its strong start, but they are still far away to achieve them in full, as we can see from figure 32. From the company’s quarterly reports and guidance for the full year results, 2017 will be a step forward in terms of accomplishing 2020 goals.

Forecasts

Revenues

Firstly, in order to have accurate forecast for revenues, one must understand where growth has been coming in the last few years. Adidas’ revenues has grown significantly and it is observable from figure 33, that the year of 2015 market a turning point in the company performance, the exact same year when the new strategy plan “Creating the New” started. The company was able to present for two consecutive years, currency-neutral double-digit sales growth (10% in 2015 and 18% in 2016).

Much of the company’s recent success can be attributed to their focus on fashion-forward consumers, through Adidas Superstar, Stan Smith and Yeezys products, but they were also able to increase its performance products sales with the “Ultra Boost” which was considered the “greatest running sneaker ever”9. This over-reliance on fashion products could present a risk for the company because it could constraint future growth and margins, but, based on recent data, this athleisure movement proved to be more than just a passing trend, it is a culture change (see page 13-14). Moreover, ecommerce channel was also a major growth driver taking advantage of the increase of online shopping (see

ADIDAS AG COMPANY REPORT

page 15). These two strategic growth areas will continue to drive growth in some

regions where Adidas operates.

Following the company’s internal management reporting, the projected revenues were forecasted for each geographical segment: Western Europe, North America, Greater China, Russia/CIS, Latin America, Japan and MEEA (Middle East, Africa and other Asian markets).

Taking into consideration the analysis presented in the “key drivers” chapter (pages 13-19), Greater China, North America and Western Europe were able to fully capitalise these ongoing trends. Their revenues grew by 28%, 24% and 20% in currency-neutral terms (22%, 24% and 17% on euro basis) in 2016, respectively. According to Adidas’ 9 months Quarterly Report in 2017, this growth trend continues, being Greater China and North America the main drivers with 28% and 23% sales growth, while Western Europe just grew 7% in currency-neutral terms. Thus, until 2020, the revenue growth rate for these regions will continue to outperform the industry’s forecasts obtained in the study published by Societe General (see figure 16) and the economy prospects (see figure 30). The others regions revenue, where the activewear and ecommerce penetration is lower, are expected to have lower growth rate compared with the aforementioned regions. Although some of them yielded strong performances in 2016 (16% for Latin America, Japan and MEAA), their revenues are forecasted to decrease until 2020, until they reach a value close to the industry’ estimation.

Western Europe and Russia/CIS will have an incremental factor in revenues in 2018 due to the expected increase of World Cup 2018 related products (see page 16-17). From 2020 onwards, it is expected that the revenues of Latin America, North America and MEEA regions will follow the growth rate presented in the study of Societe General for each region, respectively (see figure 16). All the other regions revenue growth rates will be equal to their correspondent nominal GDP growth rate forecast (see figure 30), due to the lack of data for these specific regions.

It is important to have in mind that these projected growth rates are only possible due to the comparative advantages that Adidas enjoys within this industry (see

page 13). Having a well-established brand is one of the most important factors

that influence product demand. Moreover, as explained on page 16-17, the strong brand’s image, through marketing investments, is also another incremental factor for enhancing brand connection and, hence, further sales increase. The figure 34 exhibits the forecasted revenue growth rate for all regions.

ADIDAS AG COMPANY REPORT

Figure 34: Forecasted revenue growth rate per region

Revenue growth 2015A 2016A 2017E 2018F 2019F 2020F 2021F

Western Europe 20% 17% 10% 12% 6% 4% 4% North America 5% 24% 24% 12% 8% 4% 4% Greater China 18% 28% 26% 14% 9% 9% 9% Russia/CIS -11% 3% 2% 7% 6% 6% 6% Latin America 12% 16% 11% 8% 6% 6% 6% Japan 0% 16% 9% 5% 2% 2% 2% MEAA 14% 16% 11% 6% 5% 4% 4% Total 16% 14% 12% 10% 7% 5% 5%

Expenses

The analyst community is pretty confident that under Kasper Rorsted command, Adidas will be able to increase its margins and make headway towards closing the operational margins gap with the rival Nike, as analyzed in figure 22. Previously, as CEO of the German consumer staples company Henkel, Rorsted improved operating margin by 6% from 2008 through 2014, which give him a good reputation in terms of operational improvements.

Adidas had a strong start in terms of accomplish its goals. In 2016, excluding the TaylorMade and CCM Hockey business, gross margin was 49,2% and by the third quarter of 2017, it improved to 50,1%. This developments were achieved by strong enhancements made in terms of product mix and quality of distribution channels. This results were negatively affected by currency differences, which will allow for further improvement. Additionally, as analyzed in pages 15-16, the expected increase of speed products and ecommerce sales, will also contribute for these improvements. The “Speed Factories” will not have an immediate impact because they are still in an early stage of development. Nonetheless, it is a clear sign for more future margins improvements.

The operating expenses are mainly comprised by marketing related costs and overhead expenses (see figure 8). Since the company have the intention to decrease the ratio of marketing investments spent on promotion partnerships (see page 16-17), its value will increase at a lower rate compared to the overall revenue growth rate. The overhead expenses were estimated by using the constant historic value of these costs as a percentage of net sales in 2016, in order to reproduce the projected expansion of Adidas business. Operating margin increased from 7,7% in 2016 to 8,4% in the third quarter of 2017.

The figure 35 exhibits the forecasted margins, which are lower than the ambitious targets presented in the company’s outlook for 2020 (see figure 32).

ADIDAS AG COMPANY REPORT

Figure 35: Forecasted margins

2015A 2016A 2017E 2018F 2019F 2020F 2021F Gross margin 48,3% 49,2% 50,0% 50,4% 50,8% 51,0% 51,0%

Other Operating Expenses margin 43,1% 42,8% 42,2% 41,9% 41,6% 41,5% 41,4%

Operating margin 6,3% 7,7% 8,8% 9,4% 10,0% 10,3% 10,3%

Net Income margin 3,8% 5,3% 5,0% 6,4% 6,9% 7,1% 7,1%

Net working Capital and CAPEX

Regarding Net Working Capital, all assets and liabilities that derive from the operational activity of the company were included. A historic ratio of revenues or cost of sales were used in order to determine the majority of the items. The estimation for 2017 were adjusted taking into consideration the formally completed divestiture of CCM Hockey and TaylorMade brands.

The company did not disclose any future forecasts regarding capital expenditures, rather than the projected value for the following year. In the last two years, the company achieved a lower CAPEX than the one reported in the company’s outlook, mainly due to the delay of new stores openings. Thus, the estimated capital expenditure for 2017 was considered to be at a lower value (EUR 900 million) of the investment target reported in Adidas annual report in 2016 (EUR 1.1 billion).

This value for 2017 represents a significant increase from EUR 651 million in 2016 and it can be explained by the new corporate strategy. By 2030, it is forecasted that around 60% of the global population will live in cities and, hence, Adidas began to “disproportionally” invest in six major metropolitan centres: London, Los Angeles, New York, Paris, Shanghai and Tokyo.

Taking into consideration the CAPEX distribution (see page 6), the historic percentage of the investment made in the company’s headquarters in Herzogenaurach (Germany) in 2016 was used in order to calculate its value for 2017 onwards. For the investments in the reportable segments, it is expected that the company will continue the aforementioned major investments and the historic percentage of revenues in 2016 was used in order to reproduce the projected expansion (see appendix 3).

ADIDAS AG COMPANY REPORT

Peer Group Price/Earnings EV/Sales EV/EBITDA Adidas AG 25,21 1,43 14,41

Nike Inc. 27,08 2,47 15,52

Puma SE 42,06 0,94 18,26

Under Armour Inc. 34,05 2,76 23,66

Skechers USA Inc. 23,63 0,91 7,44

Peer Group Average 31,71 1,77 16,22

Implied price per share 210,2 205,9 187,3

Adj. Peer Group Average 28,09 2,32 15,68

Implied price per share 186,2 270,4 181,0

Figure 36: Comparable Analysis

Valuation

Comparable Company Analysis

This methodology functions as a market benchmark for the current valuation of Adidas. In this sense, the EV/EBITDA, EV/Sales as well as the Price/Earnings multiples were used for this valuation. All the peer group average multiples yield an implied higher price per share compared to the current market value (EUR 167.15), indicating that the market may be underestimating Adidas.

In addition, all multiples were adjusted according to their market capitalisation which gives Nike, the closest comparable firm, a large weight on the valuation. In this case, all multiples yield the same conclusion as before, which given even more support that the market is, indeed, underestimating Adidas (see figure 36).

Discounted Cash Flows Analysis

WACC Calculation

In order to evaluate the Adidas Group business, the Weighted Average Cost of Capital (WACC) was estimated. Since the group’s financial structure includes both debt and equity, the cost of each was calculated separately.

The cost of debt was estimated by subtracting the credit loss rate (probability of default multiply by the loss given default) from the company’s debt yield. For calculating the latter, it is crucial to analyse all public bonds outstanding, where two Eurobonds with an overall volume of EUR 1 billion were identified. One matures in 2021 and has a coupon rate of 1,25% and the other matures in 2024 and has a coupon rate of 2,25%. Taking only into consideration the longer-maturity bond, its yield (1,42%) was considered as a good proxy for the company’s current debt yield since it reflects the future market cost of debt.

ADIDAS AG COMPANY REPORT

Figure 37: Linear regression Adidas vs MSCI World

Regarding the other component, a process that estimates a synthetic credit rating was used due to the fact the company’s debt is not rated. By calculating the interest coverage ratio, which is commonly used as an auxiliary to estimate credit ratings, one is able to estimate the probability of the default. By applying this procedure, a synthetic credit rating of AAA was achieved, which corresponds to an annualized default probability of 0,139%. Assuming a recovery rate based on Moody’s historic average (49,5%), the estimated cost of debt for Adidas is 1,41%. The cost of equity was calculated using the Capital Asset Pricing Model (CAPM). The risk-free rate, the levered beta and the market risk premium (MRP) are the inputs needed. The current 10-year German Treasury Bond yield was used as the risk-free rate and yields a value of 0,427%10. The MRP was estimated to be 5,75%, based on the recommendation of KPMG research11.

The beta factor was calculated by regressing the excess returns of Adidas against the excess returns of the MSCI World index of the past five years (see

figure 37)12. The resulting levered beta equals 0.89, with a 95% confidence interval between 0,25 and 1,54. In addition, a comparable method was conducted, using the four peer companies previously selected, in order to complement and support the previous assumption. The obtained levered betas for each company were unlevered at their current financial leverage (Debt-to-equity ratio), respectively. Then, the unlevered beta for Adidas is calculated through an average of the peers’ unlevered betas, including Adidas’s and, finally, on the basis of Adidas’ target level of financial leverage, one is able to reach the levered beta. The company’s capital structure is characterized for having relatively low and stable financial debt due to the issuance of instruments with mid to long term maturities and the subsequent renewal throughout the years, while market capitalisation is expected to increase. Consequently, the target debt-to-equity ratio is expected to be close to 3%13, lower than its current value (5%)14.

A levered beta of 1.05 was reached, which includes the outlier value of Under Armour (1.65)15. Taking only into consideration Nike’s, Puma’s and Skechers’ levered betas, this value decrease to 0.93, close to the value previously calculated through the linear regression (see figure 38).

Lastly, with all the inputs needed for the calculation of WACC, a cost of capital of 5,43% was used to discount the company’s free cash flow (see figure 39).

10 As of 31th December 2017

11 “Equity Market Risk Premium – Research Summary” 12 Weekly data, two years

13 The same D/E ratio is used for the WACC calculation

14 All peer companies have debt-to equity lower than 5%, except Under Armour (18%)

Figure 38: Comparable betas

Peer Group Unlevered Beta

Adidas 0,87 Nike 0,92 Under Armour 0,75 Puma 1,49 Skechers 1,09

Peer Group Av. 1,02

Levered Beta Adidas AG 1,05 Adj. Adidas AG 0,93

Figure 39: WACC calculation

Risk free rate 0.43% Equity risk premium 5,75%

Levered beta 0.89

Cost of equity 5.56%

Cost of debt 1.41%

Tax rate 29,5%

Target D/E ratio 3%

ADIDAS AG COMPANY REPORT

Figure 40: Perpetual growth calculation

Geographical Region Net Sales in % GDP growth 2022F Weighted GDP Western Europe 30% 1,5% 0,45% North America 21% 1,8% 0,38% Greater China 16% 4,7% 0,75% Russia/CIS 4% 1,5% 0,06% Latin America 9% 2,4% 0,22% Japan 6% 0,6% 0,04%

Middle East and Africa 14% 2,5% 0,35%

2,1%

Perpetual Growth

In order to determine the company’s long-term growth, one should take into consideration the geographical spread of Adidas and their specific overall economic development in the long term. Therefore, the IMF outlook forecasts of the real GDP for 2022 for each of the seven segmental regions Adidas operates were used. By weighting each by their share to the company’s total revenue, one is able to determine the perpetual growth (see figure 39).

By analysing the Cash Flow structure of Adidas in the explicit period between 2017 up to 2021, ROIC is, in fact, almost constant in 2020 and 2021, at a level of 24%. Therefore, it is safe to assume, due to this stability in the ROIC, that in the year of 2022, the FCF will be perpetual (terminal value). By putting all parts together, one is able to reach a target price of EUR 222.33 as per year-end 2018, as can be seen in appendix 3 and 4. This result are in line with the comparable analysis that Adidas stock is undervalued (page 23)

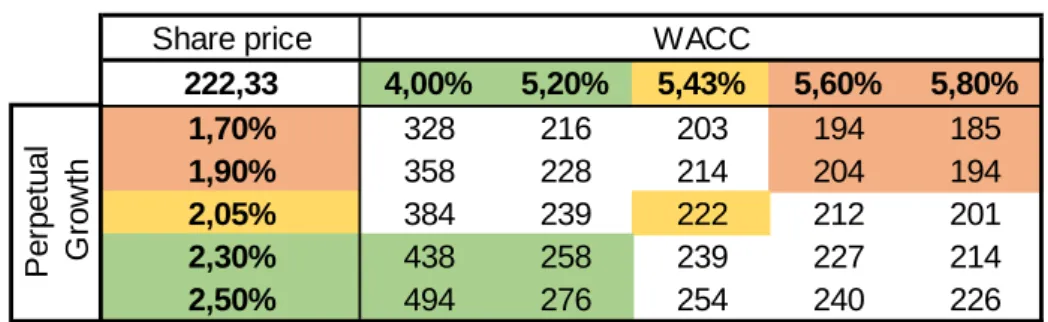

Sensitivity Analysis

Due to the heavy reliance of a Discount Cash-Flow model on its assumptions, it is required to conduct a sensitivity analysis on the variables that have major impact on the output. The perpetual growth rate plays a vital role, since it represents most of the terminal value. Whereas, the WACC is important because it is the rate to discount all future cash flows, including the terminal value. Thus, the sensitivity analysis evaluates all potential valuations by changing these two assumptions.

From figure 41, one can conclude that even in the worst case scenario, by increasing WACC and reducing the long-term growth, the share price reaches a

ADIDAS AG COMPANY REPORT

Figure 40: Sensitivity Analysis

Share price

222,33

4,00%

5,20%

5,43%

5,60%

5,80%

1,70%

328

216

203

194

185

1,90%

358

228

214

204

194

2,05%

384

239

222

212

201

2,30%

438

258

239

227

214

2,50%

494

276

254

240

226

WACC

Pe

rp

e

tu

a

l

G

ro

w

th

2017E 2018F 2019F 2020F 2021F Revenue growth (base) 12% 10% 7% 5% 5%Revenue growth (new) 12% 6% 4% 2% 2%

Gross margin (base) 50,0% 50,4% 50,8% 51,0% 51,0%

Gross margin (new) 50,0% 49,8% 49,6% 49,5% 49,5% Figure 41: Scenario Analysis

higher value compared with its current value, which emphasizes our previous conclusion that the company seems to be undervalued.

Scenario Analysis

There are some risks the business and the company is exposed to and most of them are extremely unpredictable. Hence, a negative scenario were estimated in order to reflect some of the most probable risks and events that the company may experience in the future.

Since almost all of the company’s production is outsourced in Asia (see page 5), the rising prosperity across the region means that the cost of production may increase and, hence, deteriorate margins. Moreover, in this scenario, one will considered that Adidas will not be able to achieve the expected revenue growth rate either due to a strong fightback from Nike, a slowdown on the athleisure and ecommerce trends or even a strong negative currency effect. These effects will be reflected in the new forecasted revenue growth and gross margin (see figure

41).

In this pessimistic scenario, the target price is EUR 162.86, which reflects a difference of -2.6% from its current market value. Thus, even in this negative scenario, the stock yield a value close to its current market value, which also emphasizes the previous conclusion that the company seems to be undervalued.

ADIDAS AG COMPANY REPORT

Appendix

Appendix 1: Balance sheet

2016 2017E 2018F 2019F 2020F 2021F CURRENT ASSETS:

Cash and cash equivalents 1 510 1 536 1 536 1 536 1 536 1 536

Short-term financial assets 5 5 5 5 5 5

Accounts receivable 2 200 2 455 2 708 2 885 3 028 3 179

Other current financial assets 729 467 515 549 576 605

Inventories 3 763 4 054 4 471 4 763 4 999 5 248

Income tax receivables 98 109 121 129 135 142

Other current assets 580 632 697 743 780 818

Total current assets 8 886 9 259 10 053 10 610 11 060 11 533 NON-CURRENT ASSETS:

Property, plant and equipment 1 915 2 387 2 814 3 202 3 557 3 885

Goodwill 1 412 1 228 1 228 1 228 1 228 1 228

Trademarks 1 680 1 309 1 309 1 309 1 309 1 309

Other intangible assets 167 159 156 158 160 165

Long-term financial assets 194 207 220 229 236 244

Other non-current financial assets 96 160 176 188 197 207

Deferred tax assets 732 758 836 891 935 981

Other non-current assets 94 105 116 124 130 136

Total non-current assets 6 290 6 313 6 856 7 328 7 753 8 156 TOTAL ASSETS 15 176 15 572 16 909 17 937 18 813 19 689

LIABILITIES: CURRENT LIABILITIES:

Short-term borrowings 636 710 1 247 1 625 1 729 2 355

Accounts payable 2 496 2 639 2 888 3 052 3 190 3 349

Other current financial liabilities 201 345 380 405 425 447

Income taxes 402 449 495 527 554 581

Other current provisions 573 598 655 720 752 790

Current accrued liabilities 2 023 2 124 2 324 2 456 2 568 2 695

Other current liabilities 434 470 519 553 580 609

Total Current Liabilities 6 765 7 336 8 508 9 338 9 798 10 826 NON-CURRENT LIABILITIES:

Long-term borrowings 982 985 988 991 994 396

Other non-current financial liabilities 22 25 27 29 31 32

Pensions and similar obligations 355 317 317 317 317 317

Deferred tax liabilities 387 406 444 469 491 515

Other non-current provisions 44 48 52 55 58 61

Non-current accrued liabilities 120 130 143 151 158 165

Other non-current liabilities 46 51 57 60 63 67

Total non-current liabilities 1 957 1 962 2 028 2 073 2 111 1 553 TOTAL LIABILITIES 8 721 9 299 10 536 11 410 11 909 12 379 EQUITY: Share capital 201 203 203 203 203 203 Reserves 749 749 749 749 749 749 Retained earnings 5 521 5 339 5 438 5 592 5 968 6 376 Shareholders' equity 6 472 6 291 6 390 6 544 6 920 7 328 Non-controlling interests (17) (17) (17) (17) (17) (17) TOTAL EQUITY 6 455 6 274 6 373 6 527 6 903 7 310

TOTAL EQUITY AND LIABILITIES 15 176 15 572 16 909 17 937 18 813 19 689

Balance Sheet

ASSETS