Revista

de

Administração

http://rausp.usp.br/ RevistadeAdministração52(2017)15–25

Marketing

Brand

priming

effect

on

consumers’

financial

risk

taking

behavior

Efeito

do

priming

de

marca

sobre

a

propensão

ao

risco

financeiro

do

consumidor

Efecto

del

priming

de

marca

en

la

propensión

al

riesgo

financiero

para

el

consumidor

Danielle

Mantovani

∗,

Fábio

Henrique

Silva

Galvão

UniversidadeFederaldoParaná–Curitiba/PR,Brazil

Received1June2015;accepted1August2016 Availableonline10October2016

Abstract

Takingtheperspectiveofbrandprimingtheory,this studyproposesthatbrandsassociatedwithanaudaciouspersonalitytraitmayinfluence consumerstobetakemorerisksinmakingsubsequentdecisions.Twoexperiments,runinsportbrandscontexts,showedthatindividualsexposed tobrandswithhigh(vs.low)audacitytraitsdemonstratedahigherrateofrisktakinginfinancialdecisions.Thestudiesalsoshowedthatthis effectismoderatedbyindividuals’experiencewiththefinancialmarket.Thismoderationsuggeststhattherewasanactivationofagoalnotjust semanticactivation,butthroughthebrandpriming.Thisresearchprovidesinsightsintohowtoday’sconsumersdealwithbrandprimingeffectsin riskychoicesettings.Fromamanagerialperspective,itcanhelpmanagerstounderstandthelikelyeffectsofbrandprimingonbehaviorandbetter predicttheprobabilityofriskaversionorriskseekingoutcomes.

©2016DepartamentodeAdministrac¸˜ao,FaculdadedeEconomia,Administrac¸˜aoeContabilidadedaUniversidadedeS˜aoPaulo–FEA/USP. PublishedbyElsevierEditoraLtda.ThisisanopenaccessarticleundertheCCBYlicense(http://creativecommons.org/licenses/by/4.0/).

Keywords:Brand;Priming;Risktaking;NonconsciousBehavior

Resumo

Combasenaperspectivateóricadoprimingdemarca,nesteestudo,sepropõequemarcasassociadasàpersonalidadedeaudáciapodeminfluenciar osconsumidoresatomaremdecisõesmaisarriscadasemsituac¸õessubsequentes.Doisexperimentos,realizadosnocontextodemarcasesportivas, mostramqueosindivíduosexpostosamarcascomalta(vs.baixa)audáciademonstrarammaiorpropensãoaoriscoemdecisõesfinanceiras.Esses estudostambémmostramqueesseefeitoémoderadopelaexperiênciadoindivíduocomomercadofinanceiro.Essamoderac¸ãosugerequehouve aativac¸ãodeumametapormeiodoprimingdamarcaequenãohouveapenasumaativac¸ãosemântica.Essapesquisaapresentaalgunscaminhos sobrecomoosconsumidoreslidamcomoprimingdemarcaeseusefeitossobreasescolhas.Sobaóticagerencial,osresultadospodemajudaros gestoresaentenderosefeitosprováveisdoprimingdemarcasobreocomportamentoeassimpreveraprobabilidadedemaioraversãooupropensão aorisco.

©2016DepartamentodeAdministrac¸˜ao,FaculdadedeEconomia,Administrac¸˜aoeContabilidadedaUniversidadedeS˜aoPaulo–FEA/USP. PublicadoporElsevierEditoraLtda.Este ´eumartigoOpenAccesssobumalicenc¸aCCBY(http://creativecommons.org/licenses/by/4.0/).

Palavras-chave:Marca;Priming;Propensãoaorisco;Comportamentonãoconsciente

Resumen

Conbaseenlaperspectivateóricadelprimingdemarca,enesteestudiosesugierequelasmarcasasociadasconlapersonalidadosadaoaudaz puedeninfluirenlaconductadelconsumidoryllevarloatomardecisionesmásarriesgadasensituacionesposteriores.Dosexperimentos,llevadosa caboenelcontextodemarcasdeportivas,muestranquelosindividuosexpuestosamarcasconalta(vs.baja)osadíademostraronmayorpropensión

∗Correspondingauthorat:AvenidaLotharioMeissner,632,2◦andar,80210-170Curitiba/PR,Brazil.

E-mail:[email protected](D.Mantovani).

PeerReviewundertheresponsibilityofDepartamentodeAdministrac¸ão,FaculdadedeEconomia,Administrac¸ãoeContabilidadedaUniversidadedeSãoPaulo –FEA/USP.

http://dx.doi.org/10.1016/j.rausp.2016.09.002

alriesgoenlasdecisionesfinancieras.Losestudiostambiénmuestranquetalefectoesmoderadoporlaexperienciadelindividuoconelmercado financiero.Esamoderaciónsugierequehubolaactivacióndeunametapormediodelprimingdelamarcaynosolounaactivaciónsemántica. Esteestudioindicaalgunoscaminosparaentendercómolosconsumidoresserelacionanconelprimingdemarcaysuefectoenlaselecciones. Desdelaperspectivadelagestión,losresultadospuedenayudaralosgerentesenlacomprensióndelosefectosprobablesdelprimingdemarca enelcomportamientoy,así,podránpredecirlaprobabilidaddeunamayoraversiónopropensiónalriesgo.

©2016DepartamentodeAdministrac¸˜ao,FaculdadedeEconomia,Administrac¸˜aoeContabilidadedaUniversidadedeS˜aoPaulo–FEA/USP. PublicadoporElsevierEditoraLtda.Esteesunart´ıculoOpenAccessbajolalicenciaCCBY(http://creativecommons.org/licenses/by/4.0/).

Palabrasclave: Marca;Priming;Propensiónalriesgo;Comportamientonoconsciente

Introduction

Manyeverydayactionsoccurspontaneousorautomatically,

andwithoutanyregardforwhoisaffectedbythem.Barghand

Chartrand(1999)arguethatmostofaperson’sdayisnot deter-minedbyconsciousintentions,butbymentalprocessestriggered

byenvironmentcharacterisctics andtheoperation of

noncon-sciousbehavior.

Sela and Shiv (2009) explain these automatic processes

andprimingeffects.Automaticprocessesarecharacterizedby

actionswithouttheneedofaconsciousmonitoring.Basically, thisconceptisaboutinternalizedknowledgeandacquired

expe-riences that will be used whenever needed, but without any

consciouseffortonthepartoftheindividul.Thecurrentresearch

extendsthestudyofnonconsciousbehaviorbyfocusingonthe

influenceofbrandprimingonconsumers’risktakingbehavior

inthecontextoffinancialdecisionmaking.

Priming is defined as the way experiences create future

actions, without individuals’ conscious knowledge (Bargh & Chartrand,2000).Primingisanincidentalactivationof knowl-edgestructuresprocess,involvingqualitiessuchaspersonality andstereotypestraits.Thisactivationofmentalstructureswill

beresponsibleforsubsequentbehaviorbeyondconsciousness.

Theprimingeffectworksasamanipulationoffutureactions,

meaning that itpowerfully triggerssubsequent actions andis

capable of influencing consumption atitudes, behaviors and

decisionsinanonconscious way(Aarts, Custer,&Veltkamp, 2008;Brasel&Gips,2011;Chartrand,Huber,Shiv,&Tanner, 2008; Friedman & Elliot, 2008; Fitzsimons, Chartrand, & Fitzsimons,2008;Pickering,McLean,&Krayeva,2015;Sela &Shiv,2009).

Accordingly, personality and human characteristics are

usedasabrandpositioningstrategy.Subsequentconsumption

actions, attitude behavior or decisions are a consequence of

theperceptionandimportancethesebrandstakeinconsumers’

minds,basedinhowtheyidentifyandwishtohavean interac-tionwiththebrandpersonalitycharacteristics(Cesario,Plaks,& Higgins,2006;Yang,Cutright,Chartrand,&Fitzsimons,2014).

Recentresearchdemonstrateshowbrandpriminginfluences

consumer behavior (Brasel & Gips, 2011; Fitzsimons et al., 2008).Withthisresearch,weattempttodetermineifthevisual exposuretoasportlogobrand,withahighaudacity personal-itycharacteristic,canprimeconsumerstohaveanonconscious

risk takingbehaviorinsubsequent decisions.Thesedecisions

arenotnecessarilyrelatedtosportsactivities.Inthisstudy,we investigatetherisktakinginfinancialdecisionmaking.

Our theoretical contribution is to demonstrate that brands

with more salient personality characteristics cantrigger sub-sequentactionsrelatedtothesecharacterisctics.Theseactions donotnecessarilyinvolveasituationinwhichthebrandis con-sumed.Inthisstudy,risktakingbehaviorismeasuredisacontext notrelatedtothepracticeofsports,buttothefinancialmarket.

Wealsodemonstratethattheprimingeffectonsubsequent

behaviorcomesfromconsumers’goals.Thegoalpriming

the-ory(Aartsetal.,2008;Bargh&Chartrand,2000)positsthata goalcannotbeactivatedthroughaprimingmanipulationifitis notintrinsictotheindividual’sgoals.Therefore,thisresearch showsthatriskybehaviorwillonlybeprimedbyabrandifthe individualhasexperiencewiththeriskysituation.Otherwise,the brandwillnothaveanyeffectonindividuals’behaviorbecause

thegoaldoesnotexist.Therefore,weshowhowmuch

experi-ence participantsshouldhaveforthebrandprimingtoimpact

thelikelihoodofariskychoice.

Primingtheory

Theprimingcanaffecttheactionofanindividualinapurely

cognitive way, wherethe semantic content drives the action.

Forexample,peopleexposedtothestereotypeofelderlypeople

walkedslowlywhencomparedtopeoplethatwerenotexposed

tothesamestereotype(Bargh,Chen,&Burrows,1996).Agroup of individualsexposedtoaviolentsport(boxing)presenteda

higher tendencyto choose hostile activitiesand also tohave

hostilebehaviorwhencomparedtoagroupofpeopleexposed

toanon-violentsport(Wann&Branscombe,1990).Similarly,

participantsprimedwithhelpfulnesswords,demonstrated

bet-tercommunicativequalityinnarratives,ascomparedtothose

primedwithunhelpfulwords(Pickeringetal.,2015).

Social influence is also a significant source of behavior

priming.Recentresearchshowsthatimplicitactivationofa sig-nificantother(e.g.onewhosharespersonalvalues,ideologyor religiousbeliefs)indirectlyactivatestheworldviewsharedwith thesignificantother,leadingtoitsactivepursuit,validation,and protection(Przybylinski&Andersen,2015).

Also, exposure to a prime that activates a stereotype can

leadtostereotype-consistentbehavior.Forinstance,Campbell, Manning,Leonard,andManning(2016)investigatedwhether stereotypeprimingeffectsonchildren’sfoodconsumption.

Chil-drenfrom 6 to14 yearsoldwereexposedtoeither anormal

weightoroverweightcartooncharacterprime.Theresultsshow

that overweight cartoon character primes activated the

intake.However, whenchildren’s own healthknowledgewas activatedpriortoexposuretotheprime,theoverweightcartoon

didnotincreaseconsumption.

In a similarstereotype priming investigation, Dijksterhuis and Knippenberg (1998) argue that it is possible to have

improvedintelligenceby thesimple exposuretoastereotype

thatsuggestsintelligence.Toconfirmthisprediction,theauthors

exposedagroup of peopletoa professorstereotype,another

groupwasexposedtoasecretarystereotypeandacontrolgroup

not exposedtoany stereotype. Afterexposure, anactivity to

measurethe participants intelligencewas proposed andfrom

statisticalanalysisitwasprovedthegroupexposedtoprofessor figuresobtainedbetterperformancewhencomparedtotheother groups.

Thesesituationsaresemantic,immediateandwithno

moti-vationalaspect.Thissemanticprimingisknownastrait-based priming(Barghetal.,1996;Dijksterhuis&Knippenberg,1998; Fitzsimonsetal.,2008).Theactiontriggedbyprimingoccurs immediatelyafterexposureanddissipatesovertimeandmainly

withaccomplishmentoftheprimedaction.

Ontheotherhand,dependingonthekindofexposureand

stimulationcontent,theprimingcaninfluencegoalpursuit.In thiscasethemotivationalcomponentisveryconsistent.Itiswhat literaturecallsgoal-basedpriming(Chartrandetal.,2008).To

understandhowthisprimingmechanismworksitisnecessary

tounderstandthemotivationalaspectsof goalpursuit. There-foreFitzsimons,Chartrand,andFitzsimons(2008)demonstrate

hownonconsciousgoalsareactivatedbyprimingmanipulation.

Thesegoalscanbeactivatedbysituationalfactorsandoperate automaticallytoinfluencebehavior.

Goalsarementallyrepresentedasmindstatesandthese

rep-resentations canbe activated ina nonconscious waybecause

theypre-existintheindividual’smind.Thesegoalsthatalready exist,arepartofaknowledgestructurekeptinmemory,created bytheindividual’slife(Aarts &Dikjsterhuis,2000;Bargh & Gollwitzer,1994).

Aartsetal.(2008)statethatthepursuitofnonconsciousgoal canoccurwhenapre-existingandwishedforgoalisactivated. Howevertheauthorssuggestastrengthener(ormoderator)role ofpositiveeffectinthisprocess.Forinstance,apersonthathas agoaltosavemoney,whenexposedtoastimulationwithstrong relationtolowprice andsaving, canhavethisgoalactivated andthe person’sattitudeswillbeinduced tosatisfythisgoal.

Chartrandetal.(2008)demonstratedthattheconsumers,when

exposedto a brand withstrong low price andmoney-saving

appeal (WALMART), had the goal activated andwere more

inclinedtochooseandbuycheaperclotheswhencomparedto

peopleexposedtomoreprestigiousbrands.

Someauthors(Aartsetal.,2008;Stajkovic,Locke,&Blair, 2006)suggestbehaviorchangesafterprimingexposure,as con-sequenceoftheactivationofagoalthatuntilthenwas“asleep” insidetheindividual’smind.Thegoalhadalreadyexisted,but onlyafterexposuretothepriming,thegoalwasactivated,which wouldinturn,triggerfutureactionstoachievethisgoal.

Therefore,itisunlikelythatthepriming,byitself,isstrong

enoughtogeneratesomeactionorbehaviorchange.Itismore

likelythat these motivationsare internalized andwould only

emergeafterexposureofsomethingthatwouldremindan

indi-vidualofthegoal,inspiteofanyconsciousawareness.Eitam andHiggins(2010)arguethatitisnotpossibletocreateanew motivationalstatethroughpriming,anditwillonlybeactivated iftherearepre-existentmentalrepresentations.

Ifthereisagoal,theprimingeffectshouldnotdissipateover time,butcouldincreaseuntilthegoalissatisfied.Howeverif onlyonebehaviortraitwasactivated,probablytheeffectwill dissipateinashortperiodoftime,immediatelyafterexposure (Sela&Shiv,2009).

Priming can also work, however, by influencing the

indi-vidualtoavoidthe behaviorassociated tothepriming.Laran, Dalton, and Andrade (2011), demonstrate that brands cause priming effects (i.e., behavioral effects consistent withthose

implied by the brand), whereas slogans cause reverse

prim-ing effects (i.e., behavioral effects opposite tothose implied bytheslogan).Theauthorsshowthatexposuretotheretailer

brandname“Walmart,”typicallyassociatedwithsavingmoney,

reducessubsequentspending,whereasexposuretotheWalmart

slogan,“Savemoney.Livebetter,”increasesit.Sloganscause reverseprimingeffectsandbrandscauseprimingeffectsbecause peopleperceiveslogans,butnotbrands,aspersuasiontactics.

Laran et al.(2011) suggest that priming effects are reversed

when consumers perceive a marketing tactic as a source of

persuasion.

Brands and logotypes can be used as priming

manipula-tion (Brasel & Gips, 2011; Fitzsimons et al., 2008). Brands

are important tools in this process because of their

natu-ral tendency to embody concepts, meanings, atitudes and

personality.

Brandpriming

Theuseofbrandstoinfluencesubsequentactivitieshasbeen studied inthe recentyears. Fitzsimonsetal.(2008) used the Applebrandanditscreativepersonality,constrictingitwiththe

IBMbrand.AgroupofpeoplewasexposedtoApple(word

com-posingashuffledsentence) whereasanothergroupwasgiven

brand IBM. In asecond step, participantswere given a task

involving creativity. The authors found that the Apple group

reachedabetterperformanceinthecreativitytask,when

com-paredtotheIBMgroup.

BraselandGips(2011)usedtheimageofthebrandprintedon racingcars.Thecontextofthestudywasavirtualcarracegame. Thepaintjobsonthecarswereusedasvisualstimulus,withthe logosoftheselectedbrandsprintedonthecars.Oneofthebrands wasRedBull,whichhasspeedandperformanceappeal.The ini-tialhypothesiswasthatparticipantswhoplayedthegamewith

theRedBullcarwouldpresentthebestracetimewhen

com-pared to the participants exposed to other brands(Guinness,

Coca-ColaandTropicana).However,theauthorsfoundthatthe

performanceof Red Bullgroup wasin a“U” format,

mean-ingtheywereinboththefasterandslowergroups.Thereason

isthatwhen RedBullcarswereused,themotivationfor best

chancestomakemistakesduringtherouteincreasedbecauseof thespeed,andthesemistakescausedasignificantlossoftime inthecarracinggame.

Thesepreviousstudiesdemonstratethat brandsmay

influ-enceinsubsequentactions.Inmanycases,thetriggedactions willbesemantic,whereintheindividualperceivesastrongtrait inbrandandbehavesinasimilarmanner.However,brandshave

longbeen associatedwithhumantraits, whichinfluencesnot

onlysemanticchanges,butalsobehavior.Thereasonfor this

goal-basedprimingisthatconsumersgetinvolvedwiththebrand personalitytraits(Aaker,1997;Ferraro,Bettman,&Chartrand, 2009).Thispersonalityrepresentationstriggerconsumers’ per-ceptionsof brandsaslivingentitieswiththeirownhumanlike motivations,characteristics,consciouswill,emotions,and inten-tions(Puzakova,Kwak,&Rocereto,2013).

Beyond thepriming effect, the placeboeffectthe brand is

capableofgeneratingmustbeconsidered.Forinstance,Amar,

Ariely,Bar-Hillel,Carmon,andOfir(2011)developedan

activ-ity to measure reading skills in an environment under high

brightness.Inordertodiminishluminosityeffectsandimprove visualcapacity,sunglassesweregiventotheparticipants.The firstgroupusedglassesprintedwithabrandthatcarriesahigh qualityappeal(RayBan),whereastheothergroupusedtheexact sameglasseswhichhadbeenprintedwithalowerqualitybrand (Mango).Theresultsdemonstratedthatactivitieswerecarried outinamoreefficientwaybythegroupthatusedtheglasses

printedwiththehighqualityperceptionbrandwhencompared

withtheparticipantsthatusedthesameglasses,butprintedwith thelowqualitybrand.

It is not recent that brands are capable to influence

con-sumers decisions in favor of the products they represent.

The perception of the product quality is more of a reflex

reactiontothebrandthan,infact,theproduct’sfeatures

them-selves. This was demonstrated in the classic blind beer test,

by AllisonandUhl (1964), inwhichthe authorsproved that

withoutalabelonthebottle,whenconsumerstastedthe

bev-erage, they could not distinguish the beer that, according to

them at the beginning of the experiment, was their favorite

one.

Inmostofthestudiesonbrandpriming,theactionsof indi-vidualsfollowingbrandexpositionhadahighfit withbuilt-in characteristicsofthebrands.WallMartismuchalignedto sav-ingmoneyandlowprices(Chartrandetal.,2008;Laranetal., 2011).Also,elderlypeoplearewiselyfragileandslow(Bargh etal.,1996).

Theassociationsmaybesimilarforsomesportsbrands.

Com-munication strategiesmake directassociation of thesebrands

toperformanceinsport.Thiseffectcanoccurasaresult ofa brandplaceboeffect,eitherbecauseofthepurposeofthe prod-uctstampedbythebrandorpersonality traitsassociatedwith thebrands.

Exposuretothesebrandscanmakeconsumersfeelmore

con-fident,saferorevenmoredaringand,consequently,leadtomore risktakinginsubsequentdecisions.Brandsassociatedwithan

audaciouspersonalitymayinfluenceconsumerstobemorerisk

takinginsubsequentdecisions.Therefore,thefirsthypothesis suggests:

H1. Individualsexposedtoimagesofbrandswithpersonality

traits related to audacity will be more risk taking in

subse-quentconsumptionsituations,comparedtoindividualsexposed

toimagesofbrandswhichtheaudacitytraitislesssalient.

However,brandprimingwillonlyaffectsubsequentbehavior ifthereisanimplicitgoalrelatedtothebehavioractivatedbythe brandpriming(Aartsetal.,2008;Stajkovicetal.,2006;Yang etal.,2014).Theprimingof abrandthatconveysanaudacity

idea, will onlyinduce an audaciousbehavior insituations in

whichtheconsumerhasasalientrelatedgoal.Thebrandpriming willoccurifthemotivationalstatealreadyexists,ifthereissome sortofmentalpre-existentrepresentation.

Therefore,theeffectproposedinthefirsthypothesisis

mod-erated by individuals’ experience with the primed situation.

Followingthislogic,whentheaudacityprimedbythebrandis salient,peoplewithexperienceintakingrisksinsomesituations becomemorerisktakingintheirsubsequentdecisions.Because

the priming effect should be consistent with the consumer’s

implicitgoals,weproposethat:

H2. Theimpactofbrandsthatconveyaudacityonsubsequent

risktakingbehaviorismoderatedbyconsumers’experiencein

dealingwiththeserisktakingsituations.

Overviewofthestudies

In two experiments, we test whether brand priming with

audacitytraitenhancerisktakingbehavior.Inbothstudieswe test the initialhypothesisthat brands associatedto an audac-itypersonalitymayinfluenceconsumerstobemorerisktaking

insubsequent decisions.Wealsodemonstrate themoderating

effect of consumers’experience in dealingwith risky taking

situations.

Before the experiments,we runa pre-testtoverify which

personalitytraitswereassociatedwitheachbrandthatwewere

going touseinthe brand primingmanipulations instudies1

and2.Wechosesportsbrandsforthepre-testbecausetheyare generallyassociatedwithaudacitypersonalitytraits.

Participants were students of business administration and

economicscourses.Studentsfromsportsrelatedcoursesdidnot participateinthecurrentstudies.

Pre-test

Comparingsimilarbrands,thatareactiveinthesame

mar-ketsegment,withsimilarproductportfoliocanbedifficult.To identify ifsportbrandsarereallynoticedasthemostinclined

to take risks, a pre-test was taken using abrand personality

scale proposed by Muniz and Marchetti (2012), adapted to

theBraziliancontextandoriginallyproposedbyAaker(1997). Thescalehasfivepersonalitydimensions,butforthispre-test

onlythedimension“audacity”wasanalyzed,composedbythe

Table1

Audacitydimensionofbrandpersonalitytraits.

Brands

NIKE (n=17)

ADIDAS (n=14)

TOPPER (n=17)

REEBOK (n=18)

Dimension Trait M s M s M s M s F p ηp2

Audacity Boldness 4.1a 0.6 3.6a 0.9 2.7b 1.1 2.8b 1.0 7.58 0.000 0.28

Modern 4.4a 0.7 4.2a 0.9 3.0b 1.0 3.5b 0.9 7.19 0.000 0.17

Update 4.5a 0.7 4.2a 0.7 3.2b 0.7 3.6b 0.6 10.7 0.000 0.16

Creative 4.1a 0.7 3.7a 0.8 2.8b 0.8 3.3b 0.8 6.26 0.001 0.11

Brave 4.3a 0.9 4.0ab 0.7 3.6b 0.7 3.4c 0.9 4.13 0.010 0.13

Young 4.2a 0.7 4.1a 0.8 3.3b 0.7 3.7bc 0.8 3.45 0.020 0.16

MEAN 4.3a 0.7 3.9a 0.8 3.1b 0.8 3.4b 0.8 6.55 0.000 0.27

Note:s,standarddeviation;meansthatdonotsharesubscriptsdifferbyp<0.05accordingtoBonferroniposthoc.ηp2,estimatesofeffectsize.

Participantsanddesign

Sixty-sixundergraduatestudents(55.2%women,meanage:

23.4yearsold)participatedinthispre-testinexchangeforcourse

credit.The pre-testwas computer based andwas run on the

Qualtricsplatform.

Using a five-point scale (1=not at all descriptive;

5=extremelydescriptive),subjectswereaskedtoratetheextend

towhich the six personality traits describeeach brand.Four

brandswererated:Nike,Adidas,ReebokandTopper.Tocontrol forcomparisonseffectwithinthebrands,weadopteda

single-factorbetweensubjectsdesignandeachparticipantrandomly

ratedonlyonebrand.

Results

Becausetheobjectiveofthisstagewastoidentifytheaudacity personalitytraitsthatweremoreassociatedwitheachbrand,an Anovawasperformed.TheresultsarepresentedinTable1.

Nikewasthebrandwiththehigherratedmeansforallthe

traits.Therefore,we describethe differences fromthisbrand relativetothe others.Forthe trait“boldness”,Nike (M=4.1;

σ=0.6)presentedasignificantdifferencefromReebok(M=2.8; σ=1.0)andalsofromTopper(M=2.7;σ=1.1);F(3,62)=7.58;

p=0.000,ηp2=0.28.Nikewasalsoconsideredmore“modern” (M=4.4;σ=0.7)than Topper (M=3.0; σ=1.0) and Reebok

(M=3.5; σ=0.9); F(3,62)=7.19; p=0.000, ηp2=0.17. For the trait “update”, Nike (M=4.5; σ=0.7) is also different

fromReebok(M=3.6;σ=0.6)andTopper(M=3.2;σ=0.7);

F(3,62)=10.72;p=0.000,ηp2=0.16.

And for the “creative” trait, there was a significant

dif-ferencebetweenNike(M=4.1;σ=0.7)andTopper (M=2.8; σ=0.8)andNikeandReebok(M=3.3;σ=0.8),F(3,62)=6.26,

p=0.001, ηp2=0.11. For the “brave” trait, Nike (M=4.3;

σ=0.9)wasdifferentfromTopper(M=3.6;σ=0,7)andReebok

(M=3.4;σ=0.9),F(3,62)=4.13,p=0.010,ηp2=0.13.Thetrait

“young” also presented significant differences between Nike

(M=4.2;σ=0.7)andTopper(M=3.3;σ=0.7),F(3,62)=3.45,

p=0.020, ηp2=0.16. The audacity dimension (alpha=0.88), indicatedthatNikescorewasstatisticallydifferentfromTopper andReebok,F(3,62)=6.55,p=0.000,ηp2=0.27.

Thepre-testresultsshowedNikeandAdidasdidnotdiffer

inanyofthetraits,butNikedemonstratedthelargestdifference

fromtheotherbrands.NikeandTopperwerethemostdiscrepant inalltheaudacitytraits.ThenNikeisprobablythebrandthat cantriggertheaudacityprimingand,consequently,inducerisk takinginsubsequentdecisions,whereas,Topperistheleastone.

For the experiments Nike andTopper will be the brandsfor

primingmanipulation.

Experiment1

The goalofexperiment 1was toinvestigatetheimpactof

brandprimingonrisktakinginsubsequentdecisions.Basedon the pre-testresults,we expectedthat Nikewill haveahigher primingeffectonrisktaking,comparedtoTopper.Wealsotest themoderationeffectofexperienceintherelationshipbetween

brandpriming andconsumers’risk takinginsubsequent

situ-ations of consumption. Respondents in experiment1 did not

participateagaininexperiment2.

Participantsanddesign

Eighty-twoundergraduatestudents(57.1%men,meanage:

21yearsold)participatedinthisstudyinexchangeforcourse credit.

Thestudydesignwasasingle-factorbetweensubjectswith

twoprimingconditions(Nikevs.Topper)randomlyallocatedto

oneofthetwoconditions.Theexperimentwascomputerbased

andwas run onthe Qualtrics platform. Allparticipants were

seatedatindividualworkstations.

Procedure

Thefirstmanipulationwasthebrandprimingstimulus,which wasnothingmorethanasimplevisuallogoexposure.This expo-sure, inspiredby Fitzsimonset al.(2008) study, consistedin exposingexactlythesamebrandimageintwelvedifferentcolor optionsand,fromthere,theparticipantswereaskedtochoose onlyoneoptionofcolorthatbestsuitedthebrand.

In theNikebrandgroup,participantswereexposedtotwo

Fig.1.Brandprimingmanipulation.

suspicionregardingthisfirststage’spurpose.Thesetwoother

brandswereSadiaandHavaianas.Fig.1showsanexampleof

thestimulusforthebrandprimingmanipulation:

Participantshadfreetimetodothechoices.Afterthelogo

choicefor each brand,participantswere askedtoexplainthe

reasonforthespecificcolorchoiceforthelogo.Therefore,they wouldbemoreinvolvedwiththetaskandgetevenmoreexposed tothebrandpriming.Afterthistask,participantswere imme-diately invited to participate in another, supposed unrelated, research.

Participants were directed toa second stage of the study,

in whicha risk taking behavior was evaluated. The scenario

wasbasedonAtalay(2007)study,alsorunwithundergraduate

students.Tomeasurerisk,twochoiceoptionswereoffered.The followingcoverstorywaspresented:

“Yourfamilyestablishedatrustfundinyournamewhenyou

were aninfant. The money in the fund is being managed

bythebankuntilthetrustagreementexpiresonyour25th

birthday.Themoneyinyour trustfundwillswitchtoyour

managementafteryour25thbirthday.Thebank,withyour

family’spermission,isinterestedinunderstandingyour pre-ferenceswhenitcomestomakinginvestmentdecisions.The

bankmanagertellsyouthathehasresearchedsomeoptions

forinvestingandcomeupwithtwoinvestmentoptionsthat

seemreasonable.Hewantsyoutoreviewtheseoptionsand

indicatewhichoneyouwouldprefertoinvestinifyouwere investing$5000.”

Thentheoptionswerepresented:OptionA:Thefirst

invest-mentoption isaninvestmentportfolio witha60%chance of

gaining 20% on your investment, and a40% chance of

los-ing20%ofyourinvestment.OptionB:Thesecondinvestment

optionisaninvestmentportfoliowitha70%chanceofgaining

10%onyourinvestment,anda30%chanceof losing10%of

yourinvestment.OptionAwasthemostriskyone.

Aftertheseinformationanalysis,allparticipantswereasked

to point out their preferences in a 8-point scale, where

1=“stronglypreferoptionA” and8=“stronglypreferoption B”.Fordataanalysis,scaleswereinverted,makingdata inter-pretationeasier,sothehigherthemean,thehighertherisktaking behavior.

After the investment option, participants indicated their

investing experienceinmakinginvestments(“Iusuallyinvest

mymoneyinthefinancialmarket”),measuredina7-pointscale (1=“completelydisagree”and7=“completelyagree”).

Inthemanipulationcheckfortheriskmanipulationscenario, respondentsindicatedwhichofthe2optionswerethemostrisky one.

Results

Manipulation check. The majority of the respondents in fact foundoption AriskierthanoptionB,withnosignificant

dif-ferencesamongtheotherbrandprimingmanipulationgroups.

A chi-square test indicated that there is no significant

asso-ciation between the primed brand and risk perception, χ2(1,

n=82)=0.00,p=1.00,phi=−0.02,as93%of thegroup

par-ticipantsexposedtoNikeindicatedthisoptionAasmostrisky

andwithinthegroupexposedtoTopper,94%consideredoption

AriskiertakingthanoptionB.

In ordertorule out differencesin overallexperience with

the financial market investment across the groups of brand

priming,anIndependentsamplest-testwasconducted.Results

showedthattherewasnodifferenceinparticipantsexperience withthefinancialmarketinvestment(MNike=2.91,SDNike=1.6 vs.MTopper=2.70,SDTopper=1.4;t(80)=0.62,p=0.53),which

means that the Nike groupdid not present aprevious higher

experience withthefinancialmarket,comparedtotheTopper

group.Eventhoughtheundergraduatestudentsdonothavehigh experiencewiththefinancialmarket,theyareawareoftherisks involvedinthisdecisionbecausetheyconfirmedthatoptionAis substantiallyriskierthanB.Also,theuseoffinancialdecisionsas ameasureofrisktakingisoftenusedinstudieswith undergrad-uatestudents.SeeforinstanceDuclos,Wan,andJiang(2013).

The authorsrunfourstudieswithundergraduatestudents.All

thestudieswererelatedtofinancialrisktakingbehavior.

Hypothesis test. Weexpectedthat participantsexposedtothe

Nike logos would be more inclined tochoose option A, the

riskiestone,toinvesttheir money.Beyondthat,itisexpected thiseffectismoderatedbyindividualsexperienceininvestingin thefinancialmarket,becauseagoalcannotbeactivatedthrough aprimingifitisnotalreadypresent(Aartsetal.,2008;Chartrand etal.,2008).Primingonlyactivatesagoaltheconsumeralready possesses.

Totestifriskbehaviorismoderatedbyexperiencein

invest-inginthefinancialmarket,wefollowedtherecommendations

ofHayes(2013),inwhichtheindependentvariableeffectover

the dependentvariableoccursindirectlythrough amoderator.

Hayes(2013)explainsthatforthisanalysis,boththedirectand indirecteffectsoftheindependentvariableoverthedependent variableshouldbeconsidered.

For the moderating role of experience in investing in the

financial market,we conductedaregressionanalysiswiththe

investmentchoiceasthedependentvariable,brandprimingand theinteractionofexperienceandbrandprimingasthe indepen-dentvariables.

The modelcompared exposuretoNikeversus exposureto

significancecalculationarebytheconfidenceinterval,generated throughbootstrapping.Thebootstrappingtechniqueisbasedon theassessmentofthedirectandinteractionpathspresentedinthe moderationmodel.Howeveritprovidesthesignificancecalculus of the effects withnormal distribution(significant coefficient “p”)andnon-normaldistribution(CIsuperiorandinferior),for

valuesof −1 D.P.,average and +1D.P. of the moderator M

(Prado,Korelo,&Silva,2014).Besidesthis,themodelcanbe

calculatedwithscriptPROCESS,developedbytheHayes(2013)

for SPSS andfreely available.For each dataset, a bootstrap

sampleofncasesisgeneratedbydrawingfromthesamplewith replacement,andeachpath(e.g.,“a”and“b”)iscalculatedin eachbootstrapsample.Thisprocessisrepeatedatotalof5000

times for each data set, yielding 5000bootstrapestimates of

the“ab”(Hayes&Scharkow,2013).Theprocedurealsooffers

optionsfortestingmorethanonemoderatorandprovidesdata

forgeneratingthemoderationfunctiongraphic,whichmayhelp inthevisualizationoftheinteractioneffects.

Therefore,wedonotrelyonthe“p”valueforsignificance

evaluation.In thiscaseHayes(2013)recommends evaluation

ofthe confidenceintervalof 95%,wherecannotexistsignals

changesbetweensuperiorandinferiorlimits,whichwouldbe

thepresenceofnulleffect.

Themoderationanalysiswasconductedusingprocess

mod-uleinSPSSwith5.000samples(Hayes,2013),runningmodel

1,whichrepresentsthesimplemoderation.Themodelwas

sig-nificant,withaR2=0.35,p<0.05.Therewasasignificantdirect effect of brand priming on risk taking (coeff=3.20, t=2.52,

p<0.05).Therewasalsoamaineffectofinvestingexperience (coeff=0.32,t=2.46,p<0.05).Asexpectedwefounda signifi-cantinteractioneffectofbrandprimingandinvestingexperience (coeff=0.42,t=2.07,p<0.05).

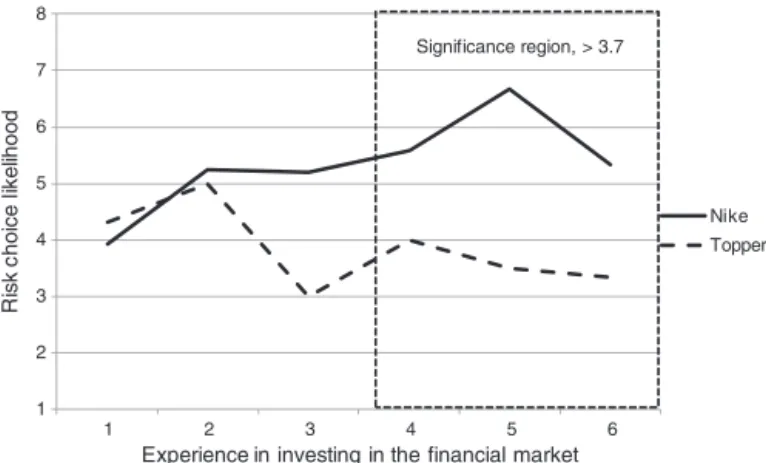

Theresultsshowtheparticipantswithahabittoinvestaverage fromM=3.70(coeff=0.75,95%C.I.=[0.00,1.49])regarding financialmarketinvestinghabittookariskieroptionafter expo-suretoNike(vs.Topper).Participantswithlowhabittoinvest didnot presentsignificative differencesinrisk tendency. The natureofthisinteractionispresentedinFig.1.

Toinvestigateatwhatlevelsofexperienceininvestinginthe financialmarketledtodifferencesinriskyinvestmentchoice,

weusedJohnson–Neymantechniquetoidentifythesignificance

region(Hayes, 2013; Preacher, Curran, &Bauer, 2006).The

Johnson–Neymantechniqueprimarycontributionisthe

deter-minationof significance of differences ingroup performance

(Johnson&Fay,1950).With theJohnson-Neyman technique theanalysisoftheproblemiscarriedfurther,inthata“regionof significance”isestablished.Ifthisregionofsignificanceisfound toexistinaparticularproblem,itbecomespossibletospecify

allthe systems of valuesof the basic charactersof matching

forwhichthenullhypothesisinvolvingsuchsystemswouldbe

rejected(Hayes,2013).

Our results revealed that participants with approximately

M=3.70(coeff=0.75,95%C.I.=[0.00,1.49])experiencewith thefinancial marketchosethe riskierinvestment.Participants

withlowexperience inthefinancial market didnot haveany

significantdifferencesintheinvestmentchoicelikelihood.The natureofthisinteractionisalsodisplayedinFig.2.

1 2 3 4 5 6 7 8

6 5 4 3 2 1

Ri

s

k

c

h

o

ice

li

k

e

lih

oo

d

Experience in investing in the financial market

Nike Topper Significance region, > 3.7

Fig.2.Brandpriming×experienceinteractiononinvestmentriskchoice like-lihood(Study1).

Discussion

Study1establishesthatconsumersbehaveinamanner

con-sistent with that implied by a brand (a priming effect). The

centralhypothesisofthisstudyisthatpeopleexposedtoabrand imagewithcharacteristicsofaudacitywillbemorerisktaking

insubsequentdecisionscomparedtothoseexposedtoabrand

imagenotassociatedwithaudacitytraits.Theresultsconfirmed

thispremises.TherewasamaineffectofNikebrandpriming

on financial risk choice likelihood. The moderator effectfor

financial market investingexperience shows when thiseffect

occurs.

Previousstudieshavedemonstratedthatbrandsandlogotypes can be used as priming manipulation (Brasel & Gips, 2011; Chartrandetal.,2008;Fitzsimonsetal.,2008).

Although theseresults support hypothesis1 and 2, a few

concernsmustbehighlighted.Themainconcernisthatweneed

todemonstratethattheprimingwasgoal-basedandnotjusta

trait-basedpriming.Primingmanipulationthat activatesgoals willhaveastrongereffectalongthetimeorwhilethegoalis not achieved(Bargh etal., 1996).If participantshadanother

unrelatedtasktospendafewminutesbeforebeingexposedto

the risk choice scenario, andafter that the priming effect on likelihoodriskchoicedisappears,thenweprobablydonothave agoal-basedpriming,butonlyatrait-basedprimingbased.

Anotherlimitation isthat wedonot haveacontrolgroup.

Therefore,itisnotcleariftheprimingeffectisaconsequence

of the Nike prime increasing risk taking choices or Topper

primedecreasingthisriskbehaviorlikelihood.Theseissuesare addressedinexperiment2.

Experiment2

ThemainpurposeofExperiment2wastoreplicatethe find-ingsobtainedinthefirststudywhileaddressingthetwomain concernsemphasizedpreviously.Precisely,thisexperimentuses (a)adifferentprimingmanipulationand(b)acontrolgroupwas included.

Participantsanddesign

Atotalofonehundredandforty-fiveundergraduatestudents

for course credit. The design was a single factor between

subjects, with three priming conditions (Nike vs. Topper vs.

Control),randomlyallocatedtooneofthethreeconditions.The

experimentwascomputerbasedandwasrunontheQualtrics

platform.

Procedure

Brandprimingmanipulationfollowedthesameproceduresof

thepreviousstudy.Theonlydifferencehereisthatweincludeda controlgroup,whichdidnotreceiveanyprimingstimulus.After that,participantswereaskedtoresolveacrosswordpuzzleand

theyhadthreeminutes tofind as many words as theycould.

ThisprocedurewasadoptedbyChartrandetal.(2008)between

priming exposureandthedependent variablemeasuring.The

purposeofthisnonrelatedtaskwastoverify ifbrandpriming hadonlyasemantic oragoalactivation.Ifthesecondoption wastrue,thebrandprimingeffectwouldnotdissipateaftersome minutesandadifferentactivity.

The third and final part of the study was the risk taking

behavior.Thesameproceduresofexperiment1weretakenin

study2.

Results

Manipulation check. Again, the majority of the respondents foundoptionAriskier thanoptionB,withno significant

dif-ferences among the brand priming manipulation groups. A

chi-square test indicated that there is no significant

associ-ation between the primed brand and risk perception, χ2(1,

n=145)=0.07,p=0.9,phi=−0.04,as90%ofthegroup

partic-ipantsexposedtoNikeindicatedthisoptionAasmostriskyand

withinthegroupexposedtoTopper,94%consideredoptionA

morerisktakingthanoptionB.Withinthecontrolgroup,88%

choseoptionAastheriskiestone.

AnAnovashowedtherewasnosignificantdifferenceamong

the groups regarding the average number of words found

in the crossword puzzle task (MNike=6.4, SDNike=2.6 vs.

MTopper=6.1, SDTopper=2.3vs.MControl=5.6, SDControl=2.3; (F(2,142)=1.52,p=0.22),asexpected.

There were no differences in overall experience with the

financialmarketinvestmentacrossthegroups.Resultsindicated nosignificant difference infinancial market investing experi-ence(MNike=2.8,SDNike=2.1vs.MTopper=2.7,SDTopper=2.0 vs.MControl=2.0,SDControl=1.9;(F(2,142)=1.05,p=0.38).

Hypothesis test. Anova analysis showed that the groups dif-ferentiatedinfinancialinvestmentrisklikelihood(MNike=5.2, DPNike=2.3vs.MTopper=4.0,DPTopper=2.3vs.MControl=4.3, DPControl=2.4; (F(2,142)=3.59, p<0.05, ηp2=0.12). The groupexposedtotheNikelogoexpressedthehigherintentionof choosingtheriskiestinvestmentoption.Posthocconstrasts indi-catedtherewasasignificantdifferenceonlybetweenNikeand Topper(p<0.05).Thisresultdemonstratesthat Nikepriming increasedrisktakingbehaviorinsubsequentdecision.

Forthemoderationeffectofexperience ininvestinginthe financialmarket,thesametestsmentionedintheprevious

exper-imentweredone,followingHayes(2013)predictions.However,

aswehadthreegroups,threemodelsweretested.Thefirstone 1 2 3 4 5 6 7 8

6 5 4 3 2 1

Ri

s

k

ch

o

ice

li

k

e

lih

ood

Experience in investing in the financial market

Nike Topper Significance region, > 3.4

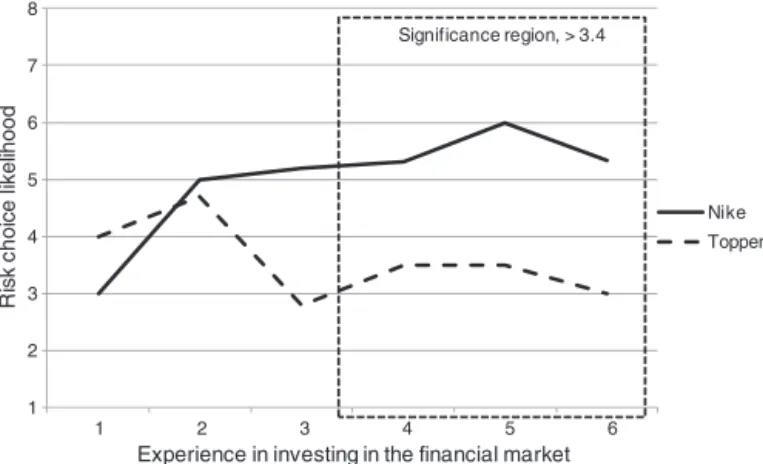

Fig.3.Brandpriming×experienceinteractiononinvestmentriskchoice like-lihood(Study2).

comparedexposuretoNikeversusexposuretoTopper,codedas

“1”and“0”respectively.Thesecondmodelcomparedthegroup

exposedtoNikeandthecontrolgroup,alsocodedas“1”and“0”

respectively.ThethirdmodelcomparedthegroupsTopperand

Control,codedforthisanalysisas“1”and“0”respectively.For alltheanalysiswerunmodel1(Hayes,2013),whichrepresents

thesimplemoderation.

For the Nike vs. Topper analysis, the model was

signif-icant, with a R2=0.29, p<0.05. There was no significant direct effect of brand priming on risk taking (coeff=−0.94,

t=−1.15, p=0.25). However, the expectedinteraction effect

of brand priming and investing experience on investment

risk choice likelihood was significant (coeff=0.55, t=2.33,

p<0.05).

Toinvestigateatwhatlevelsofexperienceininvestinginthe financial marketledtodifferencesinriskyinvestmentchoice,

weusedJohnson-Neymantechniquetoidentifythesignificance

region(Hayes,2013).Resultsrevealedthatparticipantswithan approximatelymeanof3.4experiencewiththefinancialmarket chosetheriskierinvestment.Participantswithlowexperiencein thefinancialmarketdidnothaveanysignificantdifferencesin theinvestmentchoicelikelihood.Thenatureofthisinteraction isdisplayedinFig.3.

The analysis for Nike brand priming moderation vs.

con-trolgroup,themodelwassignificant,withaR2=0.27,p<0.05. Also,theresultsshowedanotsignificantdirecteffectofbrand exposure on risk choice (coeff=−0.46, t=−0.61, p=0.54),

and no direct effect of the experience (coeff=0.01, t=0.03,

p=0.97). However the interaction effect of brand priming

andinvestingexperienceoninvestmentrisk choicelikelihood

wasmarginallysignificant(coeff=0.50,t=1.91,p=0.06).The

Johnson-Neyman test showed the participants with

approxi-matelymeanof2.88experiencewiththefinancialmarketchose theriskierinvestmentafterexposuretoNikewhencomparedto participantsinthecontrolgroup.

Asexpected,themoderationanalysisforToppervs.Control

on risk choicelikelihood did not show any significant direct

Discussion

The results of experiment 2 properly replicated those of

experiment 1. Nike brand priming effect increases risk

tak-inginsubsequentdecisions.Wedemonstratedthiseffectwith

investment risk choice likelihood situation. Beyond that, the

moderation effect of experience with the financial market

showed consistent results. Comparing to the control group,

resultsshowtheeffectreallycomesfromexposuretotheNike

logo,because Toppercondition didnot differentiatefromthe

controlgroup.

Severalstudies(e.g.,Aarts&Dikjsterhuis,2000;Aartsetal., 2008;Bargh&Gollwitzer,1994;Stajkovicetal.,2006)showed thatagoalcanonlybeactivated,eitherthroughabrand prim-ingoranyotherincentive,ifthegoalisalreadyintrinsicinthe individuals’mind.Foranindividualthatdoesnotinvestinthe financial market, itwould be difficult for abrand priming to changehisbehavior.

Inthisstudyitwaspossibletotestthepossibility thatrisk choice likelihood, for some participants, is part of a list of implicitgoals, andexpositiontothebrandawakensthisgoal. Similareffectwasobservedinotherstudies(e.g.,Aartsetal., 2008;Chartrandetal.,2008; Stajkovicetal.,2006).Another aspectthat contributesinthisdirectionwasthe insertionof a

task (crossword puzzle) between the brand priming

manipu-lationandthesubsequent dependentvariablemeasure.Aswe

replicatedthefindingsof experiment1,wedemonstratedthat

theprimingeffectreallyactivatedagoal.

Conclusion

Thefindingsreportedhereraisequestionsofinterestto

con-sumerresearchers and to marketing practitioners. This work

highlightsthebrandprimingeffectonconsumers’subsequent

decisions,specificallyinthe domainof risktaking.Itisnota recentdevelopmentthatconsumerbehaviorliteraturehas inves-tigatedtheantecedentsandconsequencesofrisktakingbehavior.

Weshowevidencethat brandsperceived withaudacious

per-sonality traits can trigger subsequent risk taking in decision making.

Another theoretical contribution is the demonstration that

predictedbehaviorisnotonlyaconsequenceofsemantic prim-ing.Earlierresearchshowedthatsemanticprimescanfacilitate the processing of conceptually related visual stimuli (Brasel &Gips, 2011;Ferraro, Bettman, &Chartrand, 2009). Going

beyond these observations, the present studies highlight that

visualexposuretobrandlogosthathavenopre-existing mean-ingfulassociationwiththebrandinquestion(e.g.,asportbrand andafinancialdecision)caninfluencesubsequentbehavior.

On a practical front, marketing managers have long been

aware of the complex factors underlyingconsumer behavior.

Brandimageandpersonalityarequiteconnectedtotheimages

associatedwiththem.Consumersaremorewillingtohavecloser relationshipwiththeir favoritebrands.Nowadays, itis

possi-ble to“talk” toabrand through social networks, andbrands

arealwaysinteractingwithconsumersaboutinterestingtopics, suchassports,politics,socialevents,andsoon.Giventhatthe mostpartofourinformationprocessingisunconscious,itisnot

surprisingthat thisincreasinginteractionbetweenbrandsand

consumerswillhavepsychologicalconsequencesforconsumer

behavior.Understanding how consumersconstruetheir brand

interactions can help managers todevelop brand positioning

strategies.

Recently, Nike launched an advertising campaign named

“RiskEverything”,gatheringthe bestsoccerplayerstospeak

aboutthebrand’sconceptanditsessence.Inaninterview,those responsibleforthecampaignexplainedthemainpurposeofthis

ad:“Thefilmwantstoshowhowsomeoftheworld’sbest

soc-cerplayershaveaccesstosuccessdealingwithsuchpressure, duetotheirwillingnesstoriskeverything”.Thiscampaignisa pictureofhowtoinsertmeaningtoincreasetheconstructionof astrongbrandimage.

The observed findings may also have direct managerial

implications concerning risk taking behavior in consumption

situation. Under many circumstances, consumers can either

become more or less risk seeking during the browsing and

purchasingprocesses.Identifyingthesemomentscanhelp

com-panies tofind the message frame that best fits the situation. Thecurrentworkshowsthatfinancialinvestmentsaredirectly affectedbyverytemporarybrandpriming.Indeed,therelevance offinancialmanagementforwell-beingisnotdenied.Giventhe

number of consumption situations demanding somemode of

balancingbetweenrisk andfinancial reward(e.g.investingin stockmarket,savingforthefuture,etc.),itismanagerially sig-nificanttounderstandwhenconsumersaremorewillingtotrade riskforreward.

However,financialdecisionisnottheonlytypeofriskona dailybasis.Probably,theimpactofbrandprimingexposureis likelytoinfluenceavarietyofriskychoicesettings.For market-ingmanagers,understandingtheimpactofbrandprimingonthe choicesoftheircustomersisimportanttopotentiallyincrease itseffectsonsales(Atalay,2007).Managersthatexposebrands associatedtorisktakingmayincreasetheirsalesinother prod-uctcategories.Thisbrandexposurecan,forinstance,increase

newproductadoption,whichisalsoriskyconsumerbehavior.

Limitationsandfutureresearch

Consumers see many brands during the course of a day

butoftenpayvery littleattention tohowsuch exposureswill influencetheirsubsequentdecisions.Futureresearchcould

ana-lyze brand priming effect in stores,supermarkets andonline

shopping, so brand priming theory would increase external

validity.

Recently,astudyfromYangetal.(2014)analyzedtheeffect ofexposuretoagroupofsimilarversusdissimilarbrandsover consumersevaluation.Besidesthat,futurestudiesthatevaluate groupsofbrandsstillrequirefurtherinvestigation.Itispossible thatconsumersdonotformperceptionsofabrand’straitsand characteristics inisolation,butinsteadusethe context,which couldincludeanotherbrandorthecontextinwhichthebrandis presented,toformtheirimpressionsandjudgments.

thatotherbrandsthatraiseconsumers’confidenceand perfor-mance.Futurestudiescouldreplicatethepreviousfindingswith differentbrands.

It isimportant tohighlightthat the scenarioof afinancial investmenttomeasurerisktakinglikelihoodwaschosenbecause itisasituationwhereriskiseasilynoticed.However,otherrisk takingdecisionmeasurescouldbeusedasdependentvariable.

One potential limitationof the current paper isthat it did notuseabrandpriminginareallocalsituation.Abrand

prim-ingmanipulationoutside ofthe labwould haveincreasedthe

external validity of the study. However,because of the

diffi-cultyincontrollingpossibleconfoundingsources,weadopted

amanipulationsimilartothatadoptedinpreviousstudies(e.g.,

Chartrand,Huber,Shiv,&Tanner,2008;Fitzsimonsetal.,2008; Laranetal.,2011).

Althoughthetwostudiesinvolvedfinancialdecision-making,

it is not the only decision domainwhere risk taking plays a

significant role.Forinstance,BraselandGips(2011)

investi-gatedthebrandpriming onriskydrivingbehavior.Therefore,

otherconsumptionsituationscouldbetestedinfutureresearch,

such as the willingness to adopt a new product or a new

brand.

Ourresultsmayalsobelimitedbytheconvenientsampleof undergraduatestudents.Futurestudiescouldresearchdifferent

samples to determinewhether the results are consistent with

thoseprovidedbyourstudy.

Conflictsofinterest

Theauthorsdeclarenoconflictsofinterest.

References

Aaker, J. (1997). Dimensions of brand personality. Journal of Marketing Research,34(3),347–356.http://dx.doi.org/10.2307/3151897

Aarts,H.,&Dikjsterhuis,A.(2000).Habitsasknowledgestructures: Auto-maticityingoaldirectedbehavior.JournalPersonalitySocialPsychology,

78(1),53-63.doi:10.1037/0022-3514.78.1.53.

Aarts,H.,Custers,R.,&Veltkamp,M.(2008).Goalprimingandthe affective-motivationalroutetononconsciousgoalpursuit.SocialCognition,26(5), 555–577.http://dx.doi.org/10.1521/soco.2008.26.5.555

Allison,R.I.,&Uhl,K.(1964).Influenceofbeerbrandidentificationontaste perception.JournalofMarketingResearch,1(3),36–39.

Amar,M.,Ariely,D.,Bar-Hillel,M.,Carmon,Z.,&Ofir,C.(2011).Brand namesactlikemarketingplacebos.TheHebrewUniversityofJerusalem. Centerforthestudyofrationality.DiscussionPaper,566,1–8.

Atalay,A.(2007,May).Mortalitysalienceandconsumerrisktaking:Strivingfor personalcontrolandself-esteem.DoctoralDissertation.ThePennsylvania StateUniversity,Pennsylvania,USA.

Bargh,J.A.,&Chartrand,T.L.(2000).Themindinthemiddle:Apractical guidetoprimingandautomaticityresearch.InH.T.Reis,&C.M.Judd (Eds.),Handbookofresearchmethodsinsocialandpersonalitypsychology

(p.235085).NewYork:CambridgeUniversityPress.

Bargh, J.,& Chartrand,T. (1999). Theunbearable automaticity of being.

American Psychologist, 54(7), 462–479. http://dx.doi.org/10.1037/0003-066X.54.7.462

Bargh,J.,&Gollwitzer,P.(1994).Environmentalcontrolofgoal-directedaction: Automatic andstrategic contingenciesbetween situationsand behavior. InW.D.Spaulding(Ed.),NebraskaSymposiumonMotivation(41)(pp. 71–124).Lincoln:UniversityofNebraskaPress.

Bargh,J.,Chen,M.,&Burrows,L.(1996).Automaticityofsocialbehavior: Directeffectsoftraitconstructandstereotypeactivationonaction.Journal ofPersonalityandSocialPsychology,71(2),230–244,doi:10.1.1.318.3898. Brasel,S.,&Gips,J.(2011).RedBullgivesyouwingsforbetterorworse: A double-edged impact of brand exposure on consumer performance.

Journal of Consumer Psychology, 21,57–64. http://dx.doi.org/10.1016/ j.jcps.2010.09.008

Campbell, M.C.,Manning,K.C.,Leonard,B.,&Manning,H.M.(2016). Kids, cartoons, and cookies: Stereotype priming effects on children’s food consumption. Journal of Consumer Psychology, 26(2), 257–264. http://dx.doi.org/10.1016/j.jcps.2015.06.003

Cesario,J.,Plaks,J.,&Higgins,E.(2006).Automaticsocialbehavioras moti-vatedpreparationtointeract.JournalofPersonalityandSocialPsychology,

90(6),893–910.http://dx.doi.org/10.1037/0022-3514.90.6.893

Chartrand,T.L.,Huber,J.,Shiv,B.,&Tanner,R.J.(2008).Nonconscious goalsandconsumerchoice.JournalofConsumerResearch,35(2),189–201. http://dx.doi.org/10.1086/588685

Dijksterhuis,A.,&Knippenberg,A.(1998).Therelationbetweenperception andbehavior,orhowtowinagameoftrivialpursuit.Journalof Personal-ityandSocialPsychology,74(4),865–877. http://dx.doi.org/10.1037/0022-3514.74.4.865

Duclos,R.,Wan,E.W.,&Jiang,Y.(2013).ShowMetheHoney!Effectsof socialexclusiononfinancialrisk-taking.JournalofConsumerResearch,

40(1),122–135.http://dx.doi.org/10.1086/668900

Eitam,B.,&Higgins,E.T.(2010).Motivationinmentalaccessibility: Rel-evanceofarepresentation(ROAR)asanewframework.Personalityand Social Psychology Compass, 4(10), 951–967. http://dx.doi.org/10.1111/ j.1751-9004.2010.00309.x

Ferraro,R.,Bettman,J.R.,&Chartrand,T.L.(2009).Thepowerofstrangers: Theeffectofincidentalconsumer-brandencountersonbrandchoice.Journal ofConsumerResearch,35(5),729–741.http://dx.doi.org/10.1086/592944 Fitzsimons, G. M., Chartrand, T. L., & Fitzsimons, G. J. (2008).

Auto-mated effects of brand exposure on motivated behavior: How Apple makesyouthinkdifferent.JournalofConsumerResearch,35(1),21–35. http://dx.doi.org/10.1086/527269

Friedman,R.,&Elliot,A.J.(2008).Exploringtheinfluenceofsportsdrink exposureonphysicalendurance.PsychologyofSportsandExercise.,9(6), 749–759.http://dx.doi.org/10.1016/j.psychsport.2007.12.001

Hayes,A.F.(2013).Introductiontomediation,moderation,andconditional processanalysis.NewYork:TheGuilfordPress.

Hayes,A.F.,&Scharkow,M.(2013).therelativetrustworthinessofinferential testsoftheindirecteffectinstatisticalmediationanalysis:Doesmethod reallymatter?PsychologicalScience,24(10),1918–1927.http://dx.doi.org/ 10.1177/0956797613480187

Johnson,P.O.,&Fay,L.C.(1950).TheJohnson–Neymantechnique,itstheory andapplication.Psychometrika,14(4),349–367.http://dx.doi.org/10.1007/ BF02288864

Laran, J., Dalton,A.,& Andrade, E. (2011).The curious caseof behav-ioralbacklash:Whybrandsproduceprimingeffectsandslogansproduce reverse primingeffects.Journal of ConsumerResearch, 37,999–1014. http://dx.doi.org/10.1086/656577

Muniz, K., & Marchetti, R. (2012). Brand personality dimensions in the Brazilian context. Brazilian AdministrationReview, 9(2), 168–188. http://dx.doi.org/10.1590/S1807-76922012000200004

Pickering,M.J.,McLean,J.F.,&Krayeva,M.(2015).Nonconsciouspriming ofcommunication.JournalofExperimentalSocialPsychology,58,77–81. http://dx.doi.org/10.1016/j.jesp.2014.12.007

Prado,P.H.M.,Korelo,J.C.,&Silva,D.M.L.(2014).Mediation,moderation andconditionalprocessanalysis.RevistaBrasileiradeMarketing,13(4), 4–24.http://dx.doi.org/10.5585/remark.v13i4.2739

Preacher,K.J.,Curran,P.J.,&Bauer,D.J.(2006).Computationaltoolsfor probinginteractioneffectsinmultiplelinearregression,multilevelmodeling, andlatentcurveanalysis.JournalofEducationalandBehavioralStatistics,

31(4),437–448.http://dx.doi.org/10.3102/10769986031004437

Puzakova, M., Kwak, H., & Rocereto, J. (2013). When humanizing brandsgoeswrong:Thedetrimental effectofbrand anthropomorphiza-tionamid product wrongdoings. Journal of Marketing, 77(3),81–100. http://dx.doi.org/10.1509/jm.11.0510

Sela,A.,&Shiv,B.(2009).Unravelingpriming:Whendoesthesameprime activateagoalversusatrait?JournalofConsumerResearch,36(3),418–433. http://dx.doi.org/10.1086/598612

Stajkovic,A.,Locke,E.,&Blair,E.(2006).Afirstexaminationofthe rela-tionshipsbetweenprimedsubconsciousgoals,assignedconsciousgoals,

andtaskperformance.JournalofAppliedPsychology,91(5),1172–1180. http://dx.doi.org/10.1037/0021-9010.91.5.1172

Wann, D.,& Branscombe,N. (1990). Personperception when aggressive ornonaggressivesportsareprimed.AggressiveBehavior,16(1),27–32. http://dx.doi.org/10.1002/1098-2337