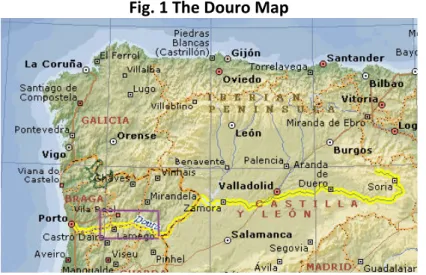

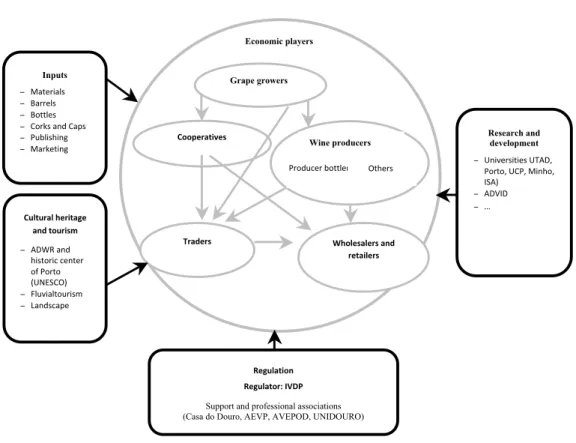

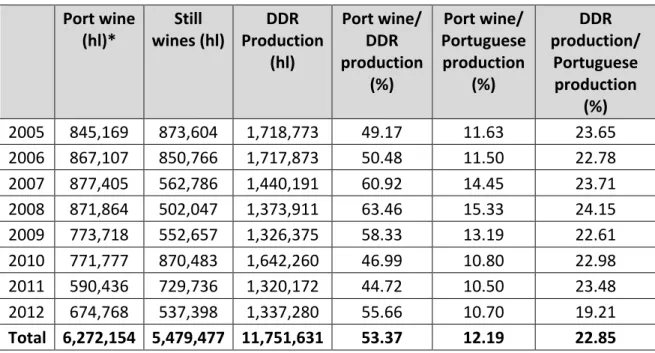

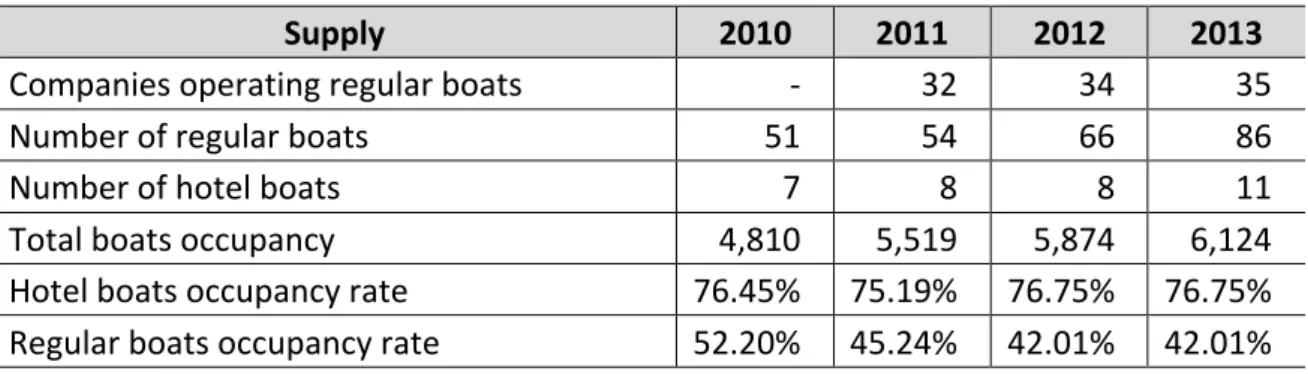

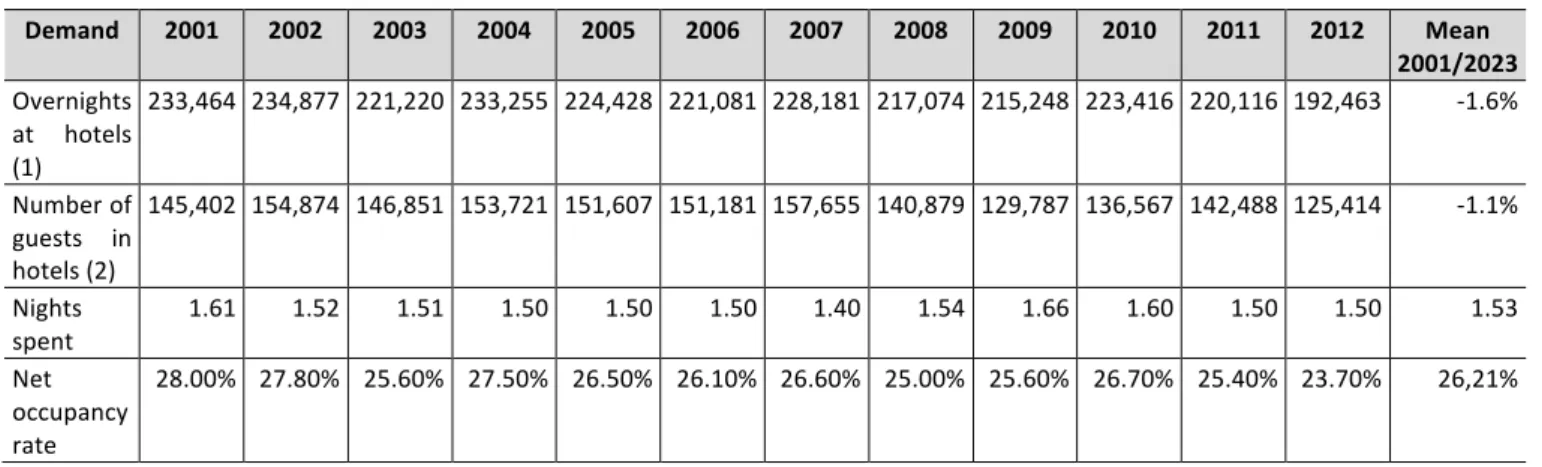

The Douro Region: Wine and tourism

Texto

Imagem

Documentos relacionados

Porcentagem de braconídeos ectoparasitoides idiobiontes e endoparasitoides cenobiontes por armadilha do tipo Malaise compartilhados entre dois ou mais talhões e

obriga a estudarmos mais, a nos esforçarmos mais e consequentemente agregar mais valor para nós mesmos. As instituições por sua vez, estão se dando conta de

The validation of the European Portuguese SDS scale in the context of cancer patients is an added value in nursing clinic practice because this tool may facilitate the

requisitos de segurança do trabalho, evitando, desta forma, possíveis lesões e mortes oriundas do trabalho. Pois, trata-se de vidas de trabalhadores que saem todos os

Através do questionário pretendíamos identificar as razões que levaram as alunas finalistas a optar pela licenciatura em educação de infância; conhecer as suas

O presente relatório foi desenvolvido no âmbito do Mestrado em Educação Pré-Escolar e Ensino do 1.º Ciclo do Ensino Básico. Apresenta o percurso profissional e pessoal da

15 O códice relaciona-se com outros manuscritos musicais do Arquivo Distrital de Évora, nomeadamente, os P-EVad 1 & 34, dois livros de coro, que na realidade são apenas um

Especialmente relevante para a presente análise é o emprego do termo “sanção econômica” pela Alta Comissária das Nações Unidas (ONU), Michelle Bachelet, bem como