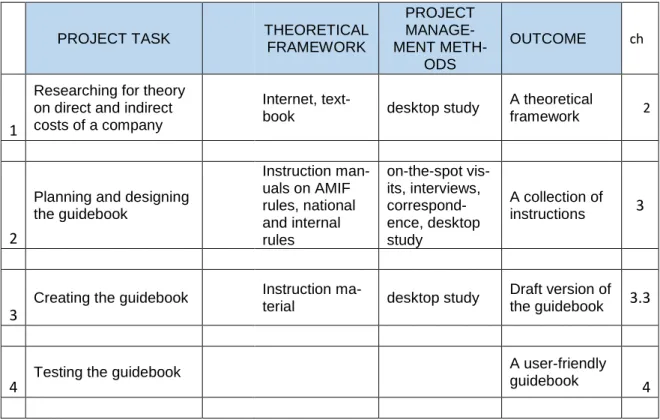

Financial management of EU-funded projects comes with its own rules, and there is no other way around them than by adapting them. The goal of the project was to create a guidebook to help with the financial management of projects financed by AMIF (Asylum, Migration and Integration Fund).

Background

During my many years of experience as a financial coordinator for EU-funded projects, it became clear that managing EU-funded project expenditure is not everyone's cup of tea. Admittedly, the eligibility rules for EU-funded projects are strict and managing project expenditure pushes one's limits, but who doesn't like a good challenge.

Project objective and tasks

Project Scope

International Aspect

Benefits

An overview of the number of AMIF projects implemented in one year compared to the number of projects implemented with the previous SOLID fund shows a significant increase in the number. In figure 2, the comparison of the number of projects between the old funding program SOLID from and the new AMIF from 2015 is presented.

Key Concepts

Case Company

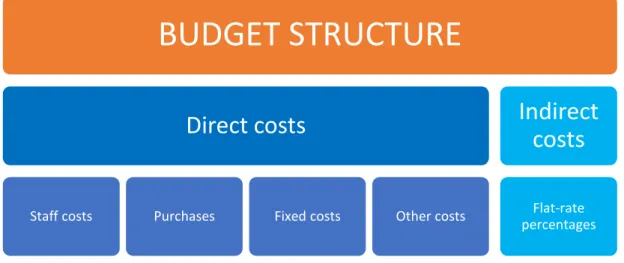

The budget structure for AMIF projects consists of direct and indirect cost classes as shown in Figure 3. At the application stage, when the beneficiary applies for funding, the estimated budget will follow the same budget structure. The AMIF budget and the for-profit company budget have different objectives.

While a company regularly checks its budget to see how things are going, the AMIF budget is checked to see if funds are being used in accordance with the budget, if the budget is overspent, underspent or simply if there is enough money available for a particular release. A company's budget can include different types of budgets depending on the type of business. This chapter presents the definition of a budget and the basic types of budgets for a company.

Types of budgets

Each cost class is budgeted and each class has its own eligibility rules with the exception of indirect costs. The master budget is used mainly in large companies and gives a complete assessment of how the management intends to run all sectors of the company in a given period (Shpak 2016). Operating budgets are used for the day-to-day management of the company and consist of the following revenue expenditures: sales, production, direct materials, direct labor, manufacturing overhead, and operating costs (Braun & Tietz. The breakdown of the operating budget is shown in Figure 4.

The financial budget is usually an estimate for a year and usually contains three budgets. In the financial budget, the company can monitor its cash inflows and outflows and its overall financial position as a whole. A static budget is a fixed budget where the numbers do not change, even though sales may change.

Budgets with direct costs

- Direct production budget

- Direct labour budget

- Direct materials budget

- Purchases budget

- Capital expenditure budget

This type of budget can be used when a fixed amount is budgeted to be spent. After the production budget is completed, the direct labor budget can be prepared, based on the number of units to be produced from the production budget. To find the total direct labor costs, the formula in Figure 7 is used.

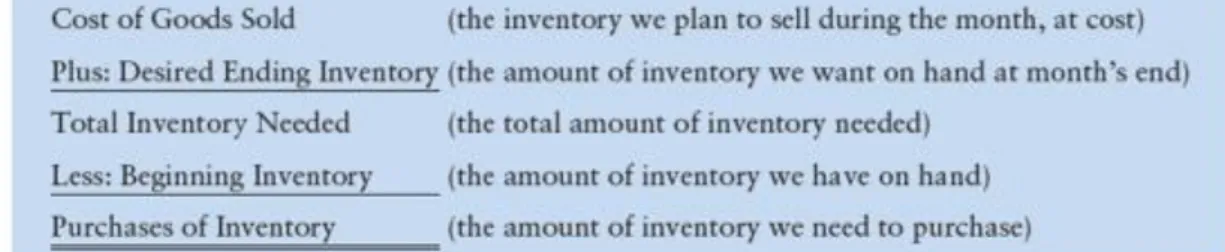

From the figures in the production budget, the amount of material required to produce the number of units can be calculated using the formula in Figure 8 (Accounting 2008). For companies that sell tangible products, the purchase budget is prepared to estimate how much material is required to be purchased as well as inventory for a certain period of time (Chron. com). For a business that purchases finished products, the budget used here is cost of goods sold (COGS), inventory and purchases budget (Braun & Tietz 2015, 545).

Manufacturing overhead budget

A capital expenditure budget falls under the financial budget and simply shows how much money a company invests in real estate, equipment, etc. In the previous chapter, an overview of budgets in the company was presented and budgets related to direct and indirect were explained in more detail. The budget structure of AMIF projects also consists of direct and indirect costs, but these have their own rules.

In order to create a guidebook based on the AMIF budget structure, certain things had to be taken into account. There were new laws, updated changes, a new budget structure, electronic reporting, etc., so different instructions were needed for different topics. To ensure that the data collected was up-to-date and appropriate for the guideline, the author had to ensure that all the right sources were examined.

Defining the areas and methods of research

Visiting the commissioning company

The guide was being prepared for a new fund AMIF from a new program that officially started in 2014, but only started in 2015. In this chapter, the author will guide you through the different project management methods used to implement project task 2. Nevertheless, after reviewing the material collected from the visit, the author requested that additional information be sent by e-mail.

After analyzing all the information provided by the commissioning company, the author made another visit to collect further details and to ensure that some of the instructions were understood correctly. Throughout the process, the author contacted both the staff and the planning and finance departments to ensure that all essential information was included, that instructions were up to date and were interpreted correctly.

Focusing on AMIF and the budget structure

Differentiating between AMIF and SOLID

The next step was to determine how these employee costs are implemented in the HR and planning and finance units of the client company. Information on this was collected in the Planning and Finance Unit and included in the guide. From all these data, the author gathered the essential data for inclusion in the guide.

In the last phase, reporting, auditing and archiving processes marked the completion of the project. In the final preparation, the focus was on the written part and the cohesiveness of the entire guide. All data collection methods were absolutely necessary in the process of creating the guide.

Focusing on classes of expense in the AMIF budget

Staff costs

Lots of information about the eligibility requirements was found in the instruction manual and all the important points were noted and presented in the guide. Although the personnel department handles personnel matters, the monitoring of project expenses takes place in the Planning and Finance Unit. The core of the problem is with the recording of hours worked, meaning that if the hours stamped on a time recording machine do not match the hours recorded by the worker on the time sheet, they will not balance.

The core of this problem also lies in the recording of working hours in the time sheet, but there is an additional problem. If the supervisor does not approve the previous month's recorded hours by the fifteenth day of the following month, the hours for the project will not be reflected in the accounting report. The importance of time stamping was again noted and taken on board to be pointed out in the guide book.

Purchases

According to rules about part-time employees of the project, workers must record their working hours daily in a time sheet. The stamping of working hours also affects the calculation of the vacation allowance share for the project. Without certain attachments, purchases in the project may be rejected, so instructions for this are included in the guidebook.

They also require attachments when the invoice appears in the system and is ready for payment. There is enough information about these cards in the intranet and internal rules, but they still need to be included in the instructions. Depending on whether the person is domestic or from abroad, certain tax forms and some personal information must be filled out, but not everyone is familiar with this process.

Fixed costs

Supplies, materials and other costs

Indirect costs

Creating the guidebook

As an added benefit, the old instructions of the old fund called SOLID were analyzed and key differences were taken into account to identify the areas where changes are visible between the new AMIF and the old SOLID. In a normal scenario, if some changes are integrated into instructions and it is not brought to the fore, it will most likely go unnoticed, so it was necessary to include in the instructions. After each topic, the author noted the areas that had too much information and those that lacked information.

The areas with too much information were edited, and for the areas that needed more information, the author returned to the material to collect more information and contacted the initiating company for additional information. Instructions were adjusted, pictures were added, references were checked and the guidebook was ready to be tested. In this chapter, I will cover the main findings of the project tasks and data collection methods, research reliability, theory assessment, feedback and the final outcome of the project.

Main results

- Reliability of the research

- Assessing the theory

- Feedback

- Overall outcome of the project objective

For feedback, a draft of the guidance was distributed to two people who have many years of experience working with project expenditure from the former SOLID fund. Everyone provided constructive feedback and most of the fixes were made based on their feedback. The guide was limited to only instructions on financial management, but since this is part of project management, project managers could include their part of the process to complete the big picture.

Already during the preparation of this manual, the responsible authority has published a new version of the manual with instructions for AMIF projects on its EUSA website. Unfortunately, some of my messages went unanswered and some of the information provided was out of date. The table of contents and other information in the guide have been tweaked and updated too many times to perfect each part of the guide.

Reflections on own learning

In the beginning, the idea of making this guidebook sounded exciting, and once the process started, there was no turning back. In the end I got what I wanted, but I could have done it in less time. On the positive side, I managed to collect and combine data from various sources and assign them to their own category.

As my main focus was on the eligibility rules of the projects and their requirements, each expenditure class of the budget structure was presented in as much detail as possible. The fact that this guide was being created for a commissioning company made a big difference in how the manual took shape. On the matter of time management, I should have finished this thesis a long time ago, but one can never put a time limit on creating a manual.

The guidebook attached separately

Gantt chart