We also show that the presence of the second externality has a strong influence on instrument choice under uncertainty between taxes and tradable permits, and that the influence depends on the design of the instruments. First, we ask how the simultaneous presence of negative externality (emissions) and positive externality (technological spillover) affects market-based instrument designs.1 Second, we ask how adding the positive externality to the negative affects instrument choice between market-based instruments ( negotiable permits and environmental taxes) under uncertainty. With regard to the second question, we show that instrument choice is influenced by the presence of the second externality.

However, the extent and the direction of the impact are case-specific.2 Firstly, the impact depends on the extent of the policy, so it matters whether the positive externality is valued or not. Second, if the positive externality is priced, the impact depends on the specific design of the instruments. The subsidy can either be fixed (zero or non-zero) or the size of the subsidy can follow the changes in the permit price.

At the end of the work, we briefly discuss the effects of a negative technological externality in our model. In the first case, a subsidy rule is used for the implementation of the permit, whereby the amount of the subsidy follows the course of the permit price according to a formula announced in advance (“the linking rule”). Intuitively Lemma 1 follows, since our framework includes both variable and fixed costs and the unit price is needed in regulating the variable costs.

So according to equation (15), the amount of the subsidy is equal to the change in the expected benefits of externality in sector r that follows from a slight increase in green investments in sector g.

Implementation of the Optimal Policy

The implementation of the permit is based on the project, whereby the amount of the subsidy is explicitly dependent on the price of the permit. According to the subsidy rule introduced in equation (18), the values of the random variables that will increase (decrease) the price of the permit will also increase (decrease) the size of the subsidy. When comparing the proposed instruments, we must further investigate the social costs of regulation.

It can enter through the emission price, independent of the emission price, and through the interaction of uncertainty and. emission price.10. It is time to move on to the main question of our study, namely instrument selection under uncertainty. Based on the expected response function of the polluter's industry, the agency implements a price or quantity instrument.

The novel feature in our framework concerns the presence of the technological externality and its internalization under uncertainty. Theorem 1 Let γ > 0 be the slope of the marginal reduction function, d >0 be the slope of the marginal damage function, and φ >0 be the amount of externality that an. The choice of instrument thus depends on the slope of the abatement cost function (γ) and the damage function (d).

In addition to creating a cross-product term, the technological externality changes the traditional instrument comparison in another way.12 To see the effect, we first write the slope of the marginal emission reduction function in the absence of spillover as . It reflects the fact that, ceteris paribus, a positive externality offsets the slope of the overall emission reduction marginal function. We interpret the multiplier >1 as an additional weight given to the marginal damage when choosing the instrument.

By following the basic principles of instrument choice (Weitzman [12]), more weight will be given to damage as the marginal cost curve flattens. The basic explanation for this is the positive correlation that emerges endogenously as a result of the cost complementarity in the abatement cost function.15 As in Meunier [8], complementarity favors the price instrument, environmental tax. 14The term 1n outside the parentheses is, strictly speaking, greater than zero and thus only reinforces the sign of the comparative advantage, but does not change it.

Hybrid Implementation

In response to realization of uncertainty x1(θ), the hybrid system will cause more intense price movements than the pegged system. In summary, the hybrid and the pegged permit systems produce identical expected emissions and expected emission prices under optimal policy designs. Since the implementations will differ ex-post, a question arises about the choice between these systems.

Note that the comparison between permit systems is entirely dependent on differences in abatement costs. Proposal 2 Let's assume that the regulator can decide whether the subsidy is fixed or not in the implementation of the permit. Our model does not provide an unequivocal answer to this problem, since the answer depends on the parameters of the minimization cost functions.

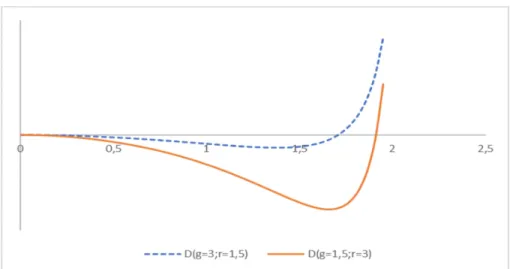

Basically, these results follow as the two differences in comparative advantage pull in opposite directions. Since the vertical axis represents differences in expected abatement costs between fixed and variable subsidy rules, negative (positive) values mean that fixed (variable) subsidy rule should be used.17. Moreover, the pegged rule is seen to become the preferred rule as the spillover effect grows strong enough.

This happens when the price volatility in the hybrid system becomes large enough compared to the fixed execution. Naturally, both curves intersect the horizontal axis at φ = 0, since the spillover effect disappears there. In the previous section, we discussed the inefficiencies that are subsequently caused by the use of simple subsidy instruments.

They differ in that they apply different types of subsidies, but both instruments use tradable permits in the emission regulation. Regarding the choice between price and quantity of instruments under fixed subsidy rule, we can calculate a comparative advantage (a counterpart of Equation (37)) as We skip the derivation by noting that it closely follows the derivation of comparative advantage in the previous section.

Zero-Subsidies

Moving from one inefficient implementation to another affects both the variance-related factor (E[x1(θ)]2) and the correlation-related factor (E[y1(θ)x1(θ)]) and that these changes ( described in equations (43) and (44)) pull the instrument selection in the opposite direction. Since γsbxs 6= 1 and zsbγsb > 0, the emission price ssb deviates from the first best rule Es=dEe(s). Furthermore, emission levels between instruments are related by the relationship esb(τsb, θ) =lsb +x1(θ). 52) The analysis shows that the additional policy constraint affects the overall design of the instrument.

Despite this, the instrument choice between price and quantity instruments is still influenced by the positive externality. By equations (40) and (46) we can also write the comparative advantage as 53) whereγ is the slope of the reduction function under the pegged-subsidy rule (Equation (22)). System 3 Assume that there is a change of policy regime from the non-subsidized to the subsidized hybrid regime.

If the regime changes to allow for substitution (thus making the design best), Theorem 3 states that ∆(τh, ph)>0, so the quantities become the instrument of choice. Overall, our analysis has shown that the positive technological externality has variance-related (E(x1(θ))2) and covariance-related ((y1(θ)x1(θ))) effects. Moving from zero grant implementation to fixed grant implementation does not change the covariance related effect at all.

Essentially, this occurs as the implementation of the fixed subsidy removes a constraint from the ex-ante policy as it captures the positive externality, the spillover effect, in an efficient manner.

Negative Technological Externality

We show how pricing only the negative externality (pollution) and setting the price of the positive externality to zero does not result in an optimal social outcome. We also develop a study of instrument choice under uncertainty (Weitzman [12]) by including another externality in the framework. In the first case, the environmental agency has a mandate to regulate only negative externalities.

In the second case, the optimality conditions promote subsidization, but they do not explicitly state its form. We end up experimenting with two rules in the permit implementation, a linear rule that explicitly depends on the unit price of emissions, and a fixed rule that both the permit and tax systems use in their implementations. Our analysis shows that the instrument choice is influenced by the presence of the second externality.

Technological externalities cause dependence between technological choices, which is further reflected as an additive correlation factor in the instrument choice formula. First, the effects are shown to depend on the scope of the policy, so it matters whether a positive externality is estimated or not. Second, if a positive externality is estimated, the effects depend on the specific design of the permitting instruments, namely whether implementation uses a linear or fixed rule.

In this regard, our approach does not question the identification of the effect, but rather takes the spillover effect as a known parameter. A natural extension would be to incorporate the uncertain spillover effect into the instrument selection problem. Prices versus quantities in the presence of another, unappreciated externality. Journal of Public Economic Theory.

Social costs SC arise as a sum of abatement costs C and emissions damages D, i.e., they are. Regarding the subsidy in the receiving sector of externalities, it is found that Ir(b∗r) = Fr+ηr+crb∗r =Fr+ηr+cr. It holds that Es=ED0(e) at the social optimum, so the optimal (expected) subsidy satisfies.

In the following derivations, we find it convenient to write the discontinuity signatures as