According to the central bank's judgment, exchange rate expectations exert the most direct influence on the path of inflation. Concurrent with the strengthening of the forint (see Chart II-8) there was a shift in the composition of capital flows. From mid-December, there were changes in the signs of the on-balance sheet and off-balance sheet positions.

In the central projection for 2002, the economy's needs for external financing are expected to increase slightly.

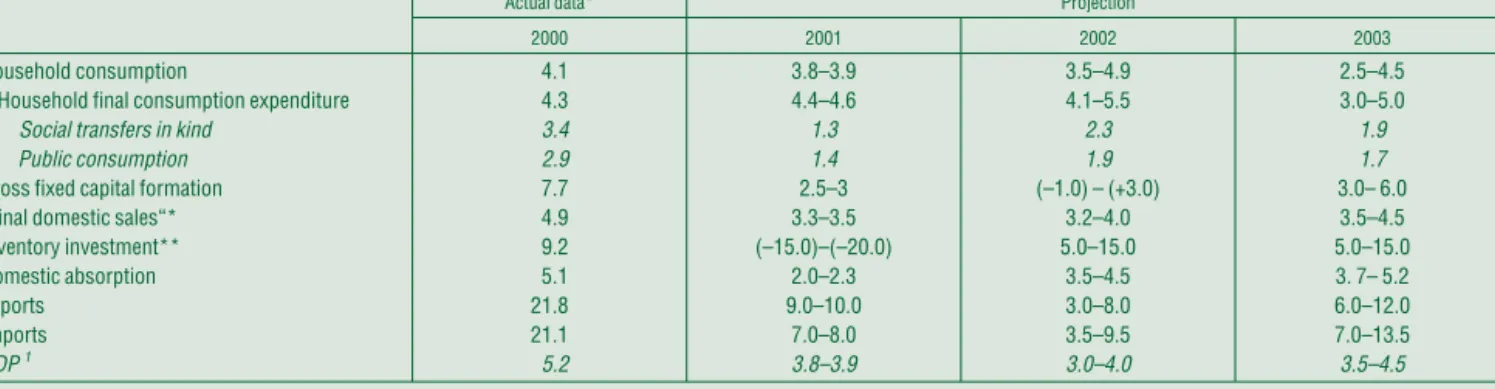

External demand and net exports

Companies are expected to continue their last year's practice in the first half of the year and reduce their capital accumulation to a greater extent than the fall in their disposable income. This trend will reverse in the second half of the year, when companies' profitability and investments will increase as a result of accelerating foreign demand. Still, signs of more robust growth will only emerge from the middle of the year.

Based on the lessons of the previous projections, the projection range is not symmetrical with the central path, the balance of risks is on the negative side (see Chart III-2). Among the potential measures of the real exchange rate, the real effective exchange rate based on unit labor costs in manufacturing is chosen for two main reasons. Secondly, this measure can also be considered a relatively good quality index from a statistical point of view.4 Under the central projection, the size of the real appreciation in 2001 and 2002 based on unit labor costs in manufacturing will exceed 15%. (see section 2.2), a measure not seen since 1991.

Companies' adjustment to weak external demand and to the appreciation of the forint led to a slowdown in domestic absorption. The reason for this is that the factors that delayed the slowdown in exports in 2001 are no longer working, and the effects of the real appreciation will be felt to a greater extent this year. The negative figures for net exports projected for 2002 and 2003, reflecting a weakening of the external balance, therefore appear to be a natural concomitant of cyclical recovery.

Household consumption

In the current projection, the nominal adjustment of the private sector to disinflation in 2002 is relatively faster (in other words, wage increases are more in line with future inflationary expectations), which should affect the reduction of real wage growth in the sector. In 2002, real wages in the public sector are expected to increase significantly faster than the mass of wages in the private sector. Wage growth in the private and public sectors is expected to lose momentum in 2003, but incomes in the public sector will continue to grow faster than in the private sector.

The speed with which the private sector adjusts its nominal wages to faster-than-expected disinflation (ie, the ratio of forward-looking to backward-looking wage formation) affects household consumption expenditures through real earnings developments. The "immediate" nominal adjustment (forward-looking wage formation) discussed in the chapter on the labor market will cause the volume of consumption expenditures in 2002 to be 0.1 percentage points lower than the central projection. Uncertainty regarding household savings is the result of an increase in the sector's net financing capacity in November and December 2001.

There is not yet enough information to indicate whether the increase in the savings rate is the result of a temporary accumulation of savings from higher year-end wage payments in 2001 or the start of a sustained upward trend in the savings rate. . 6See Special Topics: The Effects of Fiscal Policy on Economic Growth and Hungary's External Balance in 2001–02, in the November 2001 issue of Inflation Report. In the balance of short-term and long-term trends, the Bank expects that the propensity of individuals to save will remain unchanged in the central projection, carrying a symmetrical balance of risks.

Investment

Portugal and Spain), for example, the downturn in business activity during 1992–93 involved an average drop of 3.3% in the level of investment over the two years, compared with 4.7% growth in the preceding years. It took an average of two years to bring investment growth back into the positive range. It seems likely that volume growth in this sector last year was higher than the 8–10% projection in the November report.

While the effect of the motorway investment projects seems to have shown up in the statistics, institutional investment8 grew faster than expected in the final months of the year. The expected investment profile for this year also exceeds 10% when taking into account the spill-over effects of the motorway construction and municipal authorities' expenditure on the rental housing programme. In the bank's hypothetical fiscal projection (see below), public sector investment will decrease in 2003.

The number of completed homes increased by 30% in 2001, and the number of building permits issued indicates a 25% increase in the number of homes completed in 2002 (assuming completion time is between 1 and 1.5 years). As regards public and household investment, uncertainty surrounding investment growth appears to be more on the upside, while the risk of a prolonged external recession could lead to lower investment volumes in the corporate sector in 2003. The balance of risks around the central projection appears positive this year and negative in 2003.

The fiscal stance

The earlier projection assumed that - in addition to last year's excess receipts - there would be further excess receipts in 2002, which now amount to just 0.3% of GDP, but even at the outset it was thought that this would be used up as a result of the wear. -over-effect of 2001 fiscal policy decisions and the granting of additional tax allowances. It is no longer assumed that fiscal developments would generate savings this year, with projections of significant increases in both local government expenditure and spending on specific projects from the budget, which would have increased demand by 0.5% of GDP. This improvement is derived from a hypothetical path, with its endpoint corresponding to meeting the Maastricht convergence criteria in 2004 to join EMU in 2006.

In light of stronger economic activity, a tightening of fiscal policy can be considered countercyclical. Such an improvement in the primary balance should not be considered exceptional as it corresponds to the magnitude of the fiscal demand tightening in 1999 and 2000. The two categories differ not only because of the cash flow approach, but also a number of other considerations.

The calculation of the operational deficit is based on the assumption that neither the inflation compensation incorporated in the interest rate nor its annual volatility affects demand. Other factors represent the channels of demand tightening or expansion that are not reflected in the official primary balance. These factors include the effects on demand from the Hungarian Development Bank, the State Privatization Agency and the National Motorway Company.

Business cycle developments on the supply side

Firms' nominal adjustment to the appreciating exchange rate and faster-than-expected disinflation brings a high degree of uncertainty to the assessment of developments in 2002 and 2003. In addition to the central projection, the section on the labor market also discusses two extreme adjustment scenarios nominal. If firms choose mainly to adjust to the nominal shock by reducing the number of employees (“backward scenario/high inflation expectations”), then output value added could be lower by up to 0.5 percentage points in in 2002.

Since the projection of external demand carries a negative risk, the uncertainty of the forecast of the added value of manufacturing activities is negative. In line with the growth in household consumption, value added growth is also projected to be around 4% in 2001 and 2002. The service sector will also be subject to a certain degree of uncertainty in 2002 and 2003 due to the speed with which companies adjust paid wages, but this uncertainty will be less pronounced than in the manufacture of.

Based on the above factors, the projection of growth on the market supply side of GDP (which consists of production, market services and imports) lags behind the projected volume of market demand in 2001 and exceeds it since mid-2002 (see graph III-11). This means that inventory levels are forecast to decline in 2001 and increase markedly in 2002 and 2003. This trajectory for inventory levels is consistent with international experience regarding the cyclical correlation of inventories (see Special Topics: Assessment of inventories can play a role in cyclic analysis?).

The labour market

In addition to the cyclical effects, this may have contributed to a decline in employment in the final months of the year. However, a cautious increase could occur in the second half of the year, in line with the expected recovery in external demand. Wage inflation in market services developed largely in line with the forecast; wage growth stagnated or declined slightly for most of the year.

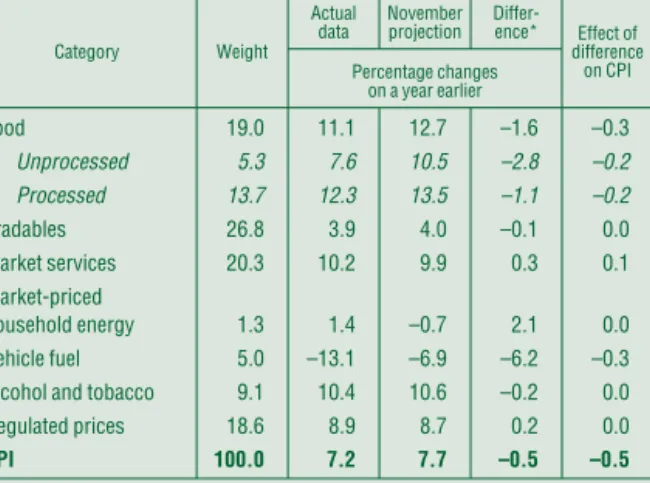

In previous forecasts, the average price of the last calendar month was forecast six quarters ahead. Consequently, a 12% increase in household gas prices is assumed in the central projection. However, prices in the last two months of the year fell more strongly than analysts expected.

According to the Ministry of Economic Affairs' staff projection, based on constant oil prices, the CPI falls within the lower half of the inflation target for the period 2002-2003. Second, an analysis of actual data necessitated a reduction in exchange rate pass-through. Note: The graph shows changes in the price level of tradable goods over a period of five years after a constant weakening of the forint exchange rate by 1%.

These were (i) the extent of exchange rate flows, (ii) the increase in labor costs, (iii) expected increases in regulated prices (including changes in taxes, in addition to the prices of goods and services administered by the central and local authorities) and (iv) the future movements in the world market price of oil. Analysts' expectations are mostly at the upper end of the bank's projection of the most likely outcome in the period 2002 Q3-December 2003.