While the UK housing market has transformed over 30 years, England has failed to keep pace as Wales and Scotland have introduced more regulation. This free quarterly statistical bulletin is designed for use by national government departments, regional agencies; voluntary sector organizations concerned with advice or social policy, and social policy researchers. However, there are important areas of work undertaken by bureaus that are not reflected in the advice statistics – particularly financial education/capability group work.

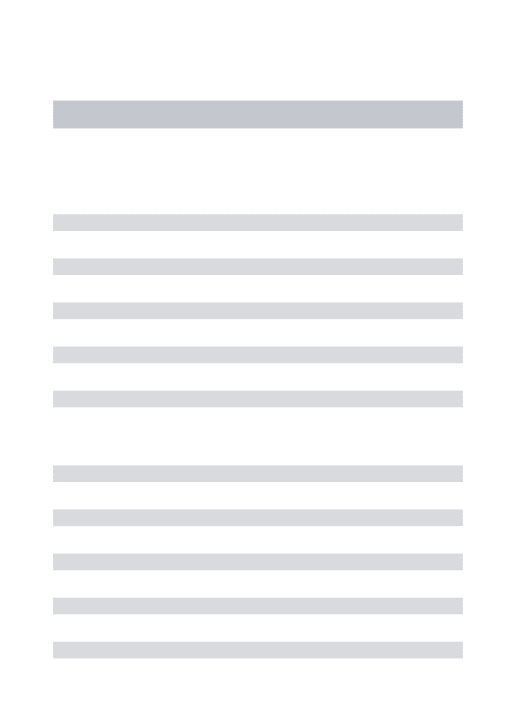

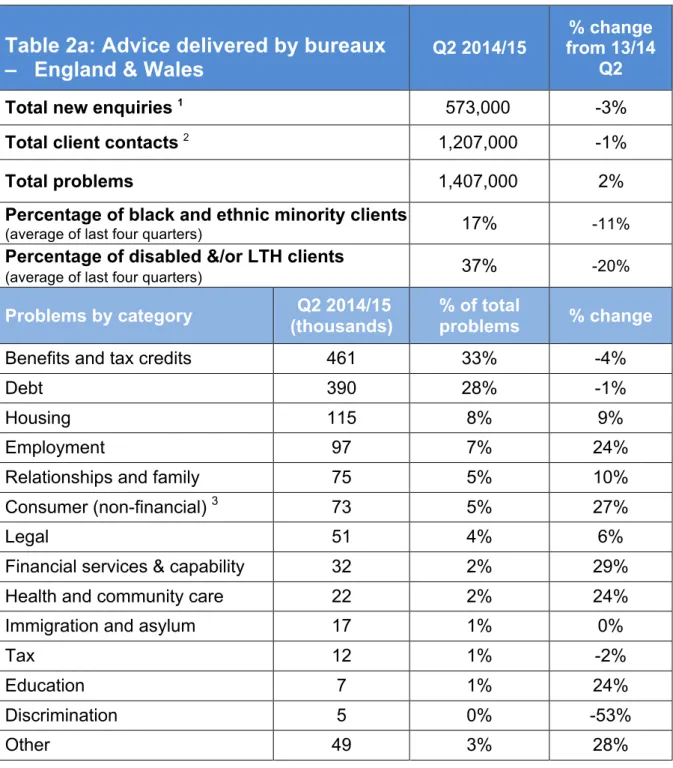

You can sign up for email alerts for the latest issue and download current and past issues at: http://www.citizensadvice.org.uk/index/publications/advice_trends.htm If you have questions or are interested in discuss further access to the data please email Peter Watson in the Corporate Management Information Team. 7 An 'enquiry' is a group of one or more contacts (phone calls or online forms) from a customer about the same problem. Citizens Advice Bureaux in England and Wales dealt with 573,000 new inquiries face-to-face or by telephone, as well as assisting their existing customers with ongoing issues.

The Citizens Advice Consumer Services dealt with 197 thousand new questions - Consumers, Energy and Mail (England, Wales and Scotland). The use of Advice Guide for consumer information increased by 45% compared to the second quarter of last year, reaching 3.1 million page views in the last quarter. Discrimination Healthcare & Community Care Financial Products / Services Legal Relationships & Family Employment Housing Consumer (non-financial) Debt Benefits & Tax Credits.

Discrimination Education Immigration, Asylum and Nationality Tax Financial Products and Services Health and Community Care Other Legal Consumer Goods and Services Relationships and Family Employment Housing Debt Services and Tax Credits.

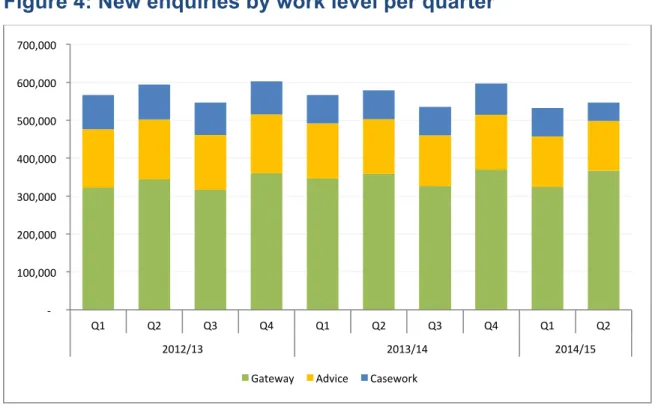

Adviceguide

Advice delivered by bureaux

Bureaux activity levels and services

Issues bureaux dealt with

Benefits and tax credits

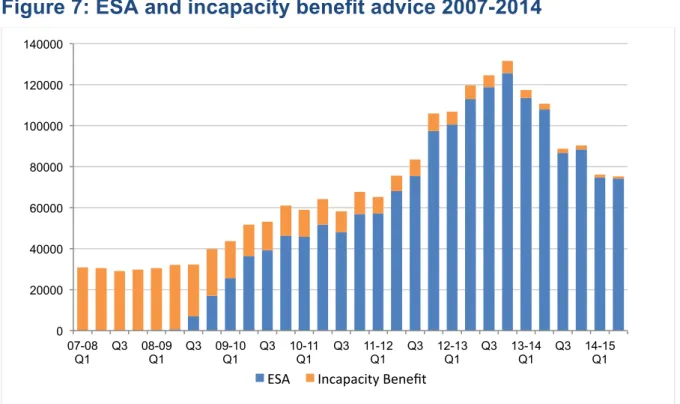

With significant changes to the benefits system and reduced consumer credit delinquencies, benefits are now a major issue. Employment and Support Allowance (ESA) accounts for 20% of all our benefits advice and has grown significantly alongside the rise in ESA claimants over the past few years. Bureaus have been overwhelmed with delayed ESA complaints, often linked to the controversial and problematic work capacity assessment.

Although advice on ESA appeals has fallen, we believe this is due to the reduced capacity of bureaus to deal with appeals following the loss of specialist benefit caseworkers, so this does not necessarily reflect a real decrease in demand. Customers were informed of 1,400 issues of rent restrictions affecting their benefit in the social rented sector, following the introduction of the under-occupancy penalty in April 2013. 62% of customers informed of the size of housing benefit restrictions in the social rented sector in the last quarter were disabled are or have had long-term health problems.

Discretionary housing payments are the only financial recourse in the benefits system for clients who have lost their benefits due to height or eligibility restrictions (e.g., benefit cap and underoccupancy penalty). Rent arrears from social landlords regularly increase – this is discussed below under Debt, but the sharp increase coincided with the introduction of rent allowance reductions due to size restriction rules. In the last quarter, there were up to 49,000 Personal Independence Payments (PIP), with PIP now accounting for 9% of all distributions.

We responded to the First Independent Review of Personal Independence Payment in September 2014, outlining the issues and making recommendations based on evidence from the bureau. Overall advice to claim tax credit increased by 17% to 49,000 and advice about debt due to tax credit overpayments increased by 37%. The drivers of this growth include; changes to the way tax credit overpayments are tracked, changes to the way annual income is calculated and an initiative within the Tax Credit Office to tackle fraud and error where some of our customers may have been wrongly considered to be overpaid.

There has been wide variation in what local authorities have given and whether they have actually spent all the money. We have seen a steady increase in the number of customers requesting emergency food. And secondly, clients whose benefits have been sanctioned and are therefore left without any income.

Debt

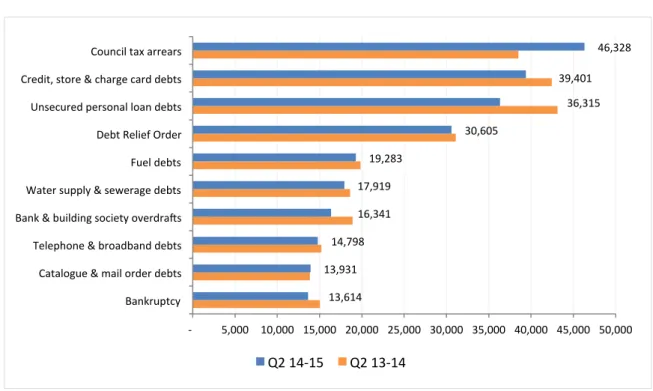

Council tax delinquencies are now the largest category of debt with an increase of 20% to more than 46,000 issuances. This follows localization and, in most areas, council tax cuts in April 2013. Consumer credit debt and mortgage arrears continue their long-term downward trend as a result of the after-effects of the recession and lower incomes in real terms, resulting in lower spending, alongside the less readily available consumer.

Priority debts have varied with some rising and some falling - council tax (up 20%), fuel (down 3%), water (down 4%) and private sector rent arrears (up 10%). Catalog and mail order debts Telephone and broadband debts Bank and building society debts Water supply and sewerage debts Fuel debts Debt relief orders Unsecured personal loan debts Loan, shop and card debts of the rate Council tax arrears. Rent arrears to social landlords has risen from 3% to 6% of all debt advice since.

The increase in advice to clients with rent arrears from social landlords advising them about possession or eviction action increased by 12% to 6,000. This is probably a reflection of the much tougher action many social landlords are taking on rent arrears for all their tenants. The Citizens Advice project "Making work locally" spoke to a number of social landlords who, despite their numbers, have lost housing benefit, preventing rent arrears from rising.

That's because they were intervening much more quickly with all their tenants at risk of arrears, both with tougher enforcement and greater support. 34% of these social housing clients advised for possession/eviction actions due to arrears were disabled or had long-term health problems.

Homelessness

Discrimination

Consumer Service

Issue description

Issues at level 3

Energy cases

Types of complaint

Appendices

Appendix 1a: Client profile charts (rolling 4 quarter average)

Appendix 1b: Client profile (rolling 4 quarter average)

Advice Issue statistics – last eight quarters

Understanding the advice statistics – what is recorded All clients are recorded on a single database. Within a bureau there will be a single

Benefits and tax credits contain all advice on new and existing entitlements, except for debts resulting from overpaid benefits or loans. Debt includes all debt problems, including all utility debts, rent or mortgage arrears, benefit and tax credits. Financial products and services therefore contain consumer problems, with the exception of consumer credit repayment problems.

Consumer goods and services include all other consumer concerns – with the exception of travel, transport and holidays, which have their own category. If a client returns for further assistance on the same inquiry, a new contact person is added. However, advisors will not add a duplicate code of existing issue codes if the work continues on the same topic (eg negotiation of refunds).

Further issues are added only if the client presents an additional related problem (such as a new debt) or needs a new type of advice. Cases can run for many months and issues can still be added as cases evolve. In a complex debt case, a code would be recorded for each debt (for example, five separate credit card debts would yield five codes).

If you require a second-level breakdown for categories not included in Appendix 3, or if you are interested in third-level statistics, please contact us. A count of customers with specific types of problems and a profile of such customers can also be produced, although this is subject to the availability of our human resources and requires payment.