I am pleased to present the report of the local pension board for the West Yorkshire Pension Fund (WYPF) for the year 2019/2020. Maintaining a good level of understanding among pension board members is important to maintaining a strong level of leadership.

PLEASE INSERT CLLR LAL’s PICTURE

The workshops were run by WYPF staff and designed to give employers a good understanding of the pension scheme. WYPF was the winner of the Pension Scheme Trustee of the Year Award hosted by European Pensions in June.

PARTICIPATING EMPLOYERS

Accounting policies Basis of preparation

A financial liability is included in the net assets statement on the date the fund becomes a party to the liability. From this date, any gains or losses resulting from changes in the fair value of the liability are recognized by the fund. Any amount not received at the end of the reporting period is disclosed in the statement of net assets as a current financial asset.

A financial asset is recognized in the net assets statement on the date the fund becomes a party to the contractual acquisition of the asset. From this date, any gains or losses resulting from changes in the fair value of the asset are included in the fund account. The values of investments shown in the net assets statement have been determined at fair value in accordance with the requirements of the Code and IFRS13 (see note 16).

Contingent liabilities are not recognized in the statement of net assets, but are disclosed in note 22 to the financial statements.

Acquisition costs of investments, excluding brokerage commissions, fees, stamp duties and currency exchange costs, are charged to the capital cost of investments. Brokerage commissions, fees, stamp duties and currency charges paid as part of the cost of acquiring investments are charged as revenue and included in investment management costs. A contingent liability arises when an event has occurred that gives the fund a possible obligation whose existence will be confirmed only by the occurrence or non-occurrence of uncertain future events that are not entirely within the fund's control.

Contingent liabilities also arise in circumstances where a provision would otherwise be made, but either it is not probable that an outflow of resources would be required, or the amount of the obligation cannot be measured reliably. Irrevocable liabilities relate to outstanding call payments due on unlisted limited partnership funds held in private equity, real estate and infrastructure portions of the portfolio. Investment transactions that take place until 31 March 2020, but are only completed later, are accrued in the accounts.

In accordance with the Code and IFRS13, the fund classifies financial instruments carried in the statement of net assets at fair value using a three-level hierarchy, as disclosed in Note 16. Financial instruments classified in level 1 are valued using quoted market prices. prices and therefore there is minimal judgment used in determining fair value. However, the fair value of financial instruments classified in level 2 and especially level 3 is determined using valuation techniques, including discounted cash flow analysis and valuation models.

Reliance is placed on third parties to carry out these assessments and due diligence is carried out by the fund to maintain confidence in the data provided. Under IFRS, the fund is required to disclose the actuarial present value of the promised retirement benefits. This is disclosed as a note in note 10 and does not form part of the financial statements.

Significant judgments and estimates are used in formulating this information, all of which are disclosed in note 10.

Events after the balance sheet date

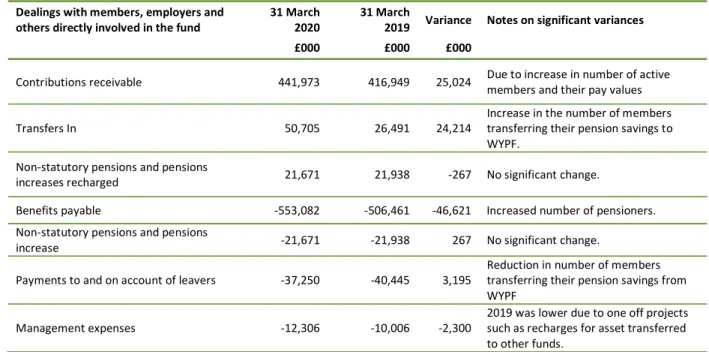

Contributions receivable

In addition, some employers are also required to pay an additional sum of money to cover any past shortfalls, which can be recovered over an appropriate period. Employee contributions are as set out in the LGPS regulations from 1 April 2014, and there are various differentiated employee contributions.

Transfers in from other pension funds

Non-statutory pensions increase and recharges

Benefits payable

Payments to and on account of leavers

AVC Scheme – Equitable Life, Scottish Widows and Prudential

Actuarial present value of promised retirement benefits

The actuarial present value of the defined benefit liability at March 31, 2019 includes the estimated liability in connection with the McCloud/Sargeant El 33.15M ruling. The actuarial present value of the defined benefit liability includes the estimated liability in respect of equalization and indexation of Guaranteed Minimum Pensions (GMP) in addition to the arrangements already in force and applicable to members whose State Pension Age (SPA) is between 6 April 2016 and inclusive 4/5/2021. The actuarial present value of the defined benefit obligation does not take into account any additional obligations that may arise from cost containment valuations.

The last full three-year actuarial valuation of the Fund's liabilities was carried out on 31 March 2019. This crisis has also caused a reduction in corporate bond yields, which will result in an increase in the value of the defined benefit liability (liability) on an accounting basis. In both of the above cases, the effect on longevity can be positive or negative.

When calculating the actuarial present value of the promised pension benefits, the future cash flows from the Fund are projected many years into the future.

Management expenses

The increase in pensions in payment and pensions deferred increases the assumption and revaluation percentage of the pension accounts. The costs associated with setting up and running Northern LGPS specifically relating to WYPF are included in the above administration costs; the cost for the 2019/20 reporting period is £106,000.

Investment expenses

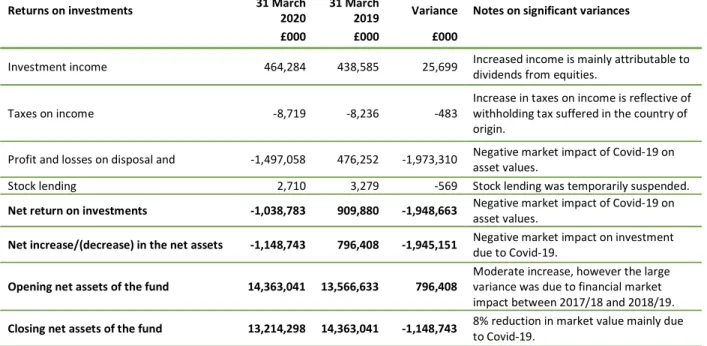

Investment income

Direct property holdings

Investments

Fair value – basis of valuation

The values reported in the annual accounts are therefore based on February end-of-month values, adjusted according to investment fund estimates. Valuations may be affected by material events that occur between the date of the financial statements provided and the pension fund's own reporting date, by changes in expected cash flows and by any differences between audited and unaudited accounts. These are based on valuations provided by the managing partners to the private equity funds in which the West Yorkshire Pension Fund has invested.

Valuations can be affected by significant events that occur between the date of the accounts and the pension funds' own accounting date, by changes in expected cash flows and by any differences between audited and unaudited accounts. The Department has determined that the valuation methods described in the table above are likely to be accurate within the following ranges and has indicated below the potential impact on the final value of investments held as of March 31, 2019. The valuation of financial assets has been classified into three levels according to the quality and reliability of the information used to determine the fair values.

The table below provides an analysis of the fund's financial assets and liabilities held at fair value in the fund's Net Asset Statement, grouped into levels 1 to 3 based on the extent to which fair value is observable.

Financial instruments – classification

Current assets – debtors

Current liabilities – creditors

Related party transactions

No senior officers responsible for the administration of the Fund entered into any contract, other than their employment contract with City of Bradford Metropolitan District Council, for the supply of goods or services to the Fund. The Fund has identified key management personnel as the Director West Yorkshire Pension Fund and the Chief Executive of Bradford Council. Details of the remuneration for these two posts are included in Note 33 of the City of Bradford Metropolitan District Council's statement of accounts.

Nature and extent of risks arising from financial instruments Risk and risk management

This is due to investments held by the fund for which the future price is uncertain. The fund invests in financial assets with the primary objective of achieving a return on investments. The Fund recognizes that interest rates may vary and may affect both the income to the Fund and the value of the net assets available to pay benefits.

Credit risk represents the risk that the counterparty to a transaction or financial instrument will fail to fulfill an obligation, causing the fund to suffer a financial loss. Essentially, the fund's entire investment portfolio is exposed to some form of credit risk. Liquidity risk represents the risk that the fund will be unable to meet its financial obligations as they fall due.

The fund therefore takes steps to ensure that there are sufficient cash resources available to meet its obligations.

Contractual commitments

The market values of investments generally reflect an assessment of credit in their pricing and consequently provision is made implicitly for the risk of loss in the carrying value of the fund's financial assets and liabilities. However, choosing high quality counterparties, brokers and financial institutions reduces credit risk that may occur from failure to settle a transaction on time. The credit risk associated with stock lending is managed by holding collateral of a greater value than the amount of stock being lent at any one time.

In addition, the fund is fully indemnified by our financial securities custodian for share lending activities. This will be especially true for cash, from the cash flow matching mandates of the main investment strategy to cover retiree payroll costs, and also for cash to meet investment obligations.

Accounting developments

Investment Strategy Statement

- Regulatory framework and purpose 2. Review of the strategy

- Liaison and communication

- Employer duties and responsibilities 5. Payments and charges

- Administering authority duties and responsibilities 7. Unsatisfactory performance

- Appendices

- Regulatory framework and purpose

- Review of the strategy

- Employer duties and responsibilities

- Payments and charges

- Administering authority duties and responsibilities

- Unsatisfactory performance

- Introduction

- Purpose of Funding Strategy Statement (FSS)

- Aims and Purpose of the Pension Fund

- Responsibilities of Key Parties

- Solvency Issues, Target Funding Levels and Long-term Cost Efficiency

- Governance and Audit Committee

- WYPF Investment Advisory Panel

- WYPF Joint Advisory Group

- WYPF Pension Board

- Annual meetings

- Training/expenses/facility time

- Register of interests

- Investment decision making process

- Variety of investments to be held

- Suitability of particular types of investment

- Risk

- Expected return on investments

- Collaborative investment and pooling

- Transaction costs

- Environmental, social and corporate governance policy

- Exercise of rights attached to investments

- Myners’ Report

- Effective decision-making

- Clear objectives

- Risk and liabilities

- Performance assessment

- Responsible ownership

- Transparency and reporting

- Aims and objectives

- Application of this policy

- Legislative and related context

- Other administering authority requirements

- What is a conflict or potential conflict and how will it be managed?

- Responsibility

- Operational procedures

- Operational procedures for advisers

- Monitoring and reporting

- Key risks

- Costs

Every three years, the fund's actuary carries out an actuarial valuation of the fund. Together they measure the degree of risk (and therefore also the degree of caution) of the financing strategy. Further details about the governing body's policy on exit valuations are included in Appendix 2.

This assessment must be to the satisfaction of the Scheme employer (ie the employer letting the contract) and the Administering Authority. In the event of unfunded liabilities upon termination of the admission, the Scheme employer's contribution rate to the Fund will be revised accordingly. Other relevant circumstances as determined by the Administrative Authority on the advice of the Fund Actuary and after discussion with the ceding employer as appropriate.

When determining this margin of caution, the governing body took into account the guidelines drawn up by the SAB1 and the advice of the Fund Actuary. Details about the fund's voting policy and its voting activities are published on the fund's website. Details about the fund's voting policy and voting activities are also published on the website.