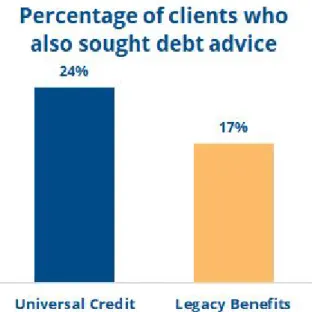

Universal Credit is one of the biggest changes to the welfare system since its inception. Rent arrears while waiting for a first payment continue to affect around half of the people we help, and debt is still more common for those on Universal Credit than those claiming older benefits.

Upcoming changes to the five week wait

Despite improvement in other areas while waiting, the proportion of people we help who are on UC and behind on their rent or mortgage has remained the same. It is clear that despite improvements, a significant proportion of the people we help continue to suffer from waiting for their first payment.

Make sure people can access adequate financial support at the beginning of their claim

Under the current UC design, the problems could be solved by providing additional financial support during the five-week waiting period. The terms of repayment of advances should be re-examined to ensure that more people can take them if needed.

Universal Credit, legacy benefits and debt

34;The government designs UC as if it assumes that people have enough income and savings to live on.

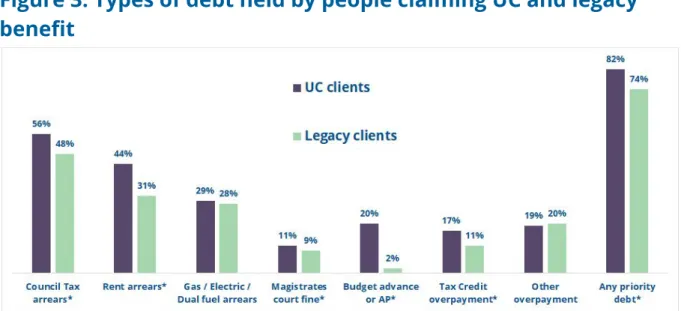

Higher levels of priority debt

Figures from the Department for Work and Pensions (DWP) also show that more than half of people who claim UC are in arrears with their rent or other housing payments or default on their financial obligations.

People on UC have less income available

Nearly half (47%) of everyone who receives debt help and claims UC no longer has money to pay creditors or has a negative budget. This is significantly higher than the 36% of people we help with debt who receive benefits and have no money left over, suggesting that many people who claim UC are in a worse financial position overall and face particular difficulties experience when repaying debts.

Larger work allowances announced in the 2018 budget

How UC design works for people’s money management?

Advance payments during the five week wait

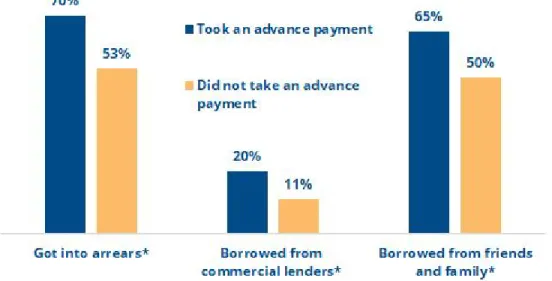

In this chapter, we examine evidence of how these features of UC work for people's money management. Two-thirds borrow from friends and family while waiting for a first payment, compared to half of those who did not. However, it does highlight financial difficulties while waiting for an initial payment that advances will not solve, and that a significant number of the people we help are likely to already be in very difficult financial circumstances when they make their claim for Universal. Credit.

Our survey data does not explain why those who take advances are more likely to have difficulty waiting. But our advisors observe financial disruptions due to changing circumstances (such as relationship breakdown), delays in making a claim because people think they can handle it, problems in making claims that cause delays and people struggling with budgeting in the first months of UC – even if they have taken advances.

Deductions leave many with reduced incomes

Deductions Explainer

There is a cap on what can be taken at 40% of your standard allowance, although this can be exceeded if decision makers think it is in your best interests. Regulations allow prepayments to be taken as a supplement as well, although in practice they tend to be treated as falling within the cap. If there is not enough money left in your premium, or your deductions would be more than can be taken within the rules, the DWP will apply a.

However, advisers report that the process is complicated and each debt repayment rate must be negotiated individually. The DWP's own data 42 shows that more than 7 in 10 people who claim UC struggle to keep up with bills and credit obligations at least sometimes.

Repayment of advances drives the prevalence of deductions

Research from February 2018 showed that only 17% of UC and Tax Credit job applicants are regularly able to put money aside. In this context of tight finances, 43 any money taken from people's monthly payments is likely to put them in difficult financial circumstances. Where people are struggling with their repayments, they can request a 3-month payment deferral, but this is currently only available if they can demonstrate they face an unforeseen circumstance.

Other debts result in large deductions, particularly early in claims

Financial hardship and knock on effects

Build up even more debts, incur new payment arrears, use credit and borrow from family or friends. In addition, interviewees also reported an impact on their mental health, such as stress and depression. Some also said their relationships became strained and they had no money in their budget to travel, leaving them stuck at home and reducing their independence.

Client case study - Repayment of an advance contributes to unmanageable deductions

More than four in five of our advisers felt that deductions did not strike the right balance between helping people pay their bills and ensuring they had enough to live on. When unaffordable amounts are taken, there is a risk that people will fall 50 behind on their bills and take on additional debt.

What people think it’s fair to take?

Wider debts fall outside the cap if they are not deducted directly

DWP discretion and people’s understanding of deductions

Advisers report that many of those we help do not fully understand why deductions occur, how they are calculated or how long they will last. Because finances are tight, budgeting for the month is difficult and unexpected deductions can make things worse. Advisers describe the withdrawal process as confusing, unclear and unpredictable, and report that the people they help often feel out of control and helpless, reducing their financial independence.

Those we spoke to often found out about their deductions, either by realizing they had received less than they expected, or when they were told by an adviser or third party. Although some deductions do not apply to those who earn more than their work allowance, the remaining deductions are set as a prescribed percentage of the standard.

Client case study - deductions for wages and other debts not factored into calculations

Deductions are being made for a tax credit overpayment, advances and social security loans being deducted at a rate of 40% of her standard allowance, or £127.13 - which comes from her housing element. Both of these priority debts will exceed the recovery of tax credit and social security funds, but neither her landlord nor her council have made a claim for third-party relief, so she must try to pay these separately. Our councillors, who regularly seek reductions in hardship relief, told us they are often frustrated by the lack of flexibility and discretion used by decision makers.

Some advisers feel frustrated at having to challenge individual debts when hardship is caused by the overall level of multiple deductions. People who have large single arrears, such as overpayments or housing debt, can negotiate deductions with DWP on the basis of hardship or fault.

Upcoming changes to deductions policy

The impact of this will vary depending on the size of a reward and the amount people choose to borrow. The difference between a limit of £127 and £95 per month for a single person over the age of 25 is significant and would have helped 13% of families claiming UC. However, as explored above, many people who claim UC lack significant financial resilience or flexibility.

People we help experience hardship, even if less than 30% of the amount is deducted. Slowing the pace of advance recovery will ultimately mean that most people with deductions will have a smaller reduction in income.

Ensure Universal Credit provides enough to live on

Any write-offs after a set period or in case of hardship should be considered to ensure that debt does not overwhelm people in the long term. Repayment holidays and write-offs for people who can't repay overpaid debt (from UC or legacy benefits) so they no longer apply to as many people in the first few months of their claim. Include debts that can be deducted directly from Universal Credit in 'respite' and statutory debt repayment plans, including prepayments and other deductions already being taken.

A survey of people Citizens Advice helps with UC found that more than half of the people we help are not paid monthly. If you are paid fortnightly by your employer, you will have a significantly lower UC payment (or no payment at all) once a year; if you are paid weekly, you will have significantly lower UC payments four months out of the year.

Alternative Payment Arrangements are falling short

Often people struggle to budget for these changes to their UC allocation, which even after changes in pay are taken into account, can include drops in income from month to month and changes in eligibility for passport benefits. During the year, some people may find themselves worse off, while others face challenges because the timing of their UC assessment period is linked to the date they made a claim, rather than the dates they receive pay or the time for their essential bills to reflect changing patterns of income. This design choice can prevent UC from smoothing out people's income changes and can actually increase the month-to-month volatility of their income.

Compared to legacy benefits, UC appears to be based on white-collar workers, their savings levels and types of work. This new direction is therefore welcome, but problems with the current provision of APA need to be addressed.

Managed payments to landlords

The managed payment option can also be particularly useful for those who have moved to UC from legacy benefits. This means that people can be in arrears without realizing it, because they believed their rent was being paid in full through the managed payment. Secondly, government guidelines state that the managed payment should only be available when a person is already significantly in arrears with rent, or when they meet the vulnerability criteria.

Landlords can only request a managed payment 61 for their tenants when they are already in a substantial arrears of rent. It is therefore particularly worrying that less than a third of the people we help with UC (31%) know about the possibility of the managed payment.

Upcoming changes

If your personal UC payment varies from month to month, any delay in your managed payment can make it even more difficult to calculate any additional rent you will have to pay your landlord and when it will be due. The Government is right to recognize the problems caused by the 4 week payment cycle and to announce its intention to move to a monthly cycle for managed payments. If the managed payment is made on the same date as people receive their UC payments, it will make it easier for them to understand how UC works - but it will still be paid in arrears when most of the rent is due in advance and is unlikely to be settled. with the date of their tenancy.

Their landlord started the process of eviction but agreed not to evict them if the managed payment was completed. Some of the advisers we interviewed told us they had seen people threatened with eviction as a result of the managed payment APA issues, even when the housing provider knew the arrears were not the tenant's fault.

Twice monthly payments

Split Payments

The study concluded in July that the current way in which UC is paid may put some survivors of domestic violence at increased risk.

Help people to budget by designing Universal Credit around real lives

A disregard should be considered for small changes to income at a similar level to the current tax credit system.

We help people