In the medium term, different adjustment costs as well as the transfer of income from oil-importing countries to oil-exporting countries prevent demand from immediately adjusting to its new long-term equilibrium. Next, we examine the effect of a sustained 25% increase in the oil price, assuming that the shock causes an increase in the oil price markup. In the long run, the effects on total employment are negligible, although real producer wages and the return on capital fall in proportion to the decline in output.

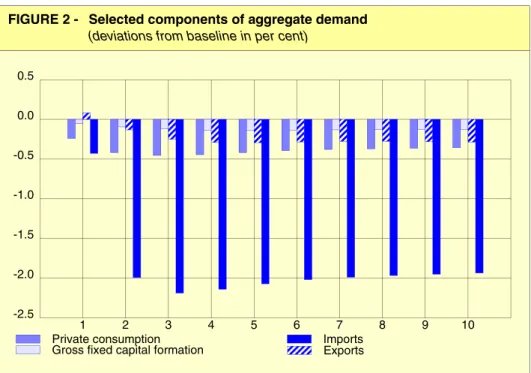

In the medium term, various adjustment costs prevent demand from immediately adjusting to its new long-run equilibrium. As a result, certain components of aggregate demand may deviate significantly from their new long-term solution in the medium term. Moreover, as the impact of the oil price shock deepens, imports continue their decline and bottom out at 2.21 percent below the baseline in the third year, compared to 1.91 percent below the baseline in the new steady state.

I Introduction and summary

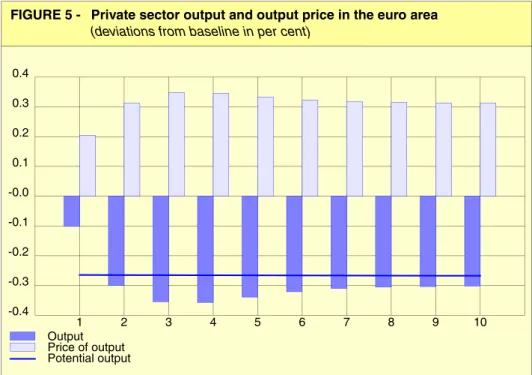

In this paper we examine the macroeconomic effects of a permanent 25 percent increase in the price of oil, due to an increase in the oil price markup. Indeed, in the first year, private consumption prices rise by 0.30 percent, while producer prices rise by only 0.20 percent. In the western non-euro EU member states, private sector output falls by 0.07 percent in the first year, bottoms out at 0.43 percent in the third year, and reaches 0.30 percent below the baseline in the long run.

In the member states, production falls by 0.21 percent in the first year and reaches 0.71 percent below baseline in the long term. In the United States, private sector output falls 0.22 percent in year one and bottoms out at 0.55 percent in year four, before leveling off at 0.33 percent below baseline over the long term . In Japan, private sector output falls 0.24 percent in the first year and stabilizes at 0.23 percent below baseline in the long run.

II The NIME model

At the same time, the price of total imports is a total of the price of oil imports and the price of non-oil imports. Earlier versions of the NIME model1 assumed that importers were long-run price makers for all imported goods and services, so that the price of total imports converges with their long-run productivity. However, we now also assume that the oil-importing country blocs are price takers with regard to the price of oil.

As a result, the price of oil may change due to a change in its productivity (ie energy efficiency) or due to a change in the price mark-up. First, if energy efficiency improves, the price of oil will rise and producers will demand less oil. Second, if the markup increases, the price of oil will rise and producers will demand less oil.

III Effects of a permanent oil price shock

The comparative statics

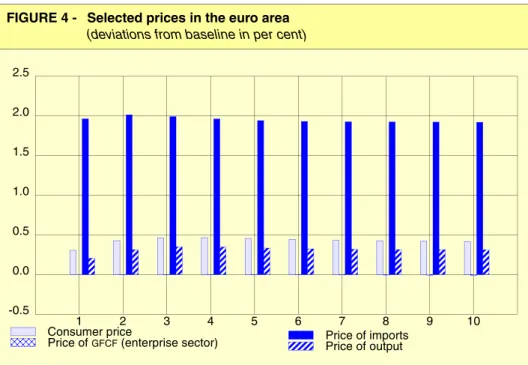

The effect of an oil price shock on the price level depends on monetary policy, while the change in relative prices is independent of monetary policy. In the long term, the price of imports in the euro area increases by 1.89 percent, which reflects the impact of the exogenous increase in the oil price mark-up and the share of oil imports in the total imports of the euro area. . The price of exports of the euro area increases by 0.24 percent, which compensates for the rise in the level of foreign effective prices and the unchanged nominal effective exchange rate.

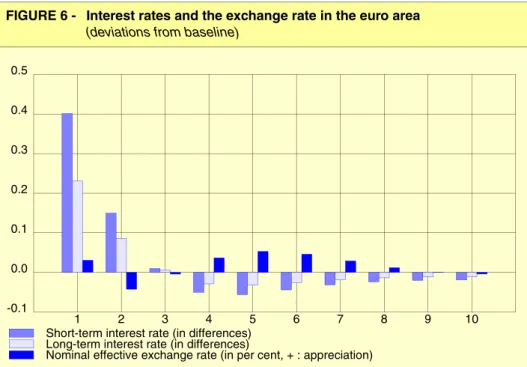

This decline reflects the fall in capital stock productivity due to the long-term decline of 0.27 percent in total private sector output. In addition, the GDP deflator does not change much, as the increase in the price of exports is accompanied by an increase in the price of imports. In the new steady state, interest rates in the euro area are not affected by the oil price shock.

This increase in taxes is necessary to keep fiscal accounts in balance in the face of changes in the relative price of private consumption. Thus, an imbalance appears in the government's fiscal accounts, which the authorities must compensate with an increase in the current rate of income tax2. In the default version of the model, public consumption of goods and services simply falls in proportion to private sector production.

This results in a long-term increase in natural unemployment, although only by 0.01 percentage points. At the same time, the price of private consumption rises by 0.43 per cent. in the western non-euro EU. In the long run, the financial variables are all close to their baseline levels.

In the oil-exporting rest of the world, long-term aggregate supply is unaffected by the oil price shock1.

The adjustment process

Investments in housing construction fall by 0.48 per cent. the first year, primarily as a result of the fall in household income and assets as well as interest rate increases. Euro area exports increase by 0.08 per cent. the first year, which reflects an increase of 0.08 per cent. in foreign effective demand and a 0.05 per cent. appreciation of the euro area's real effective exchange rate. Imports fall by a relatively modest 0.43 per cent. the first year, despite the immediate increase of 1.94 per cent. in the price of intermediate imports.

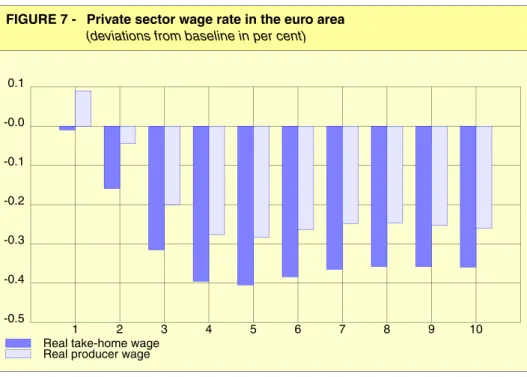

At the same time, real GDP of the euro area falls by just 0.04 percent in the first year, as total imports fall sharply. The price of private sector output rises by 0.20 percent in the first year, thus carrying most of its adjustment to its 0.25 percent steady increase. The real producer wage rate increases by 0.09 percent in the first year, but then falls to 0.28 percent below the baseline in the fourth year, compared to 0.27 percent in the long run.

In the first year, private consumption prices increase by 0.30 percent, while producer prices only increase by 0.20 percent. Although the nominal wage rate in the private sector increases by 0.29 percent in the first year, this growth is too small to keep up with the growth in private consumption prices. Therefore, the real take-home pay rate falls in the first year, followed by a further decline to 0.41 percent below baseline in the fifth year.

In the United States, total private supply falls 0.22 percent in the first year and reaches a low of 0.55 percent in the fourth year. In Japan, private supply falls by 0.24 percent in the first year and reaches a low of 0.28 percent in the second year. In fact, the export of the oil-exporting RW bloc drops by only 0.19 percent in its first year, while the bloc's (in euro-denominated) export price rises by 2.73 percent.

However, exports then fall to 0.83 percent below the baseline in the second year, and 2.33 percent below the baseline in the tenth year of the shock.

Detailed area tables

IV Appendix: Modifications to the NIME model

- Oil and the price of imports of the major country blocs

- The supply side effects of an oil price shock in the major country blocs: some analytical results

- PMT/(PASP (NITR)) = - 0.199553 wm = 0.13714

- Exports of the major country blocs

- Stock market effects for the major country blocs

- The rest of the world bloc

- Data

Supply-side effects of an oil price shock in major blocs of countries: some analytical results blocs of countries: some analytical results. In the NIME model, an increase in the oil price can be caused by an increase in oil productivity, YMTOIL, or by an increase in the mark-up over the oil price, TR_MP. Here, we consider a permanent oil price shock caused by a permanent change in lift, TR_MP.

Note that in the main text the special case of oil_imp = 1 is discussed.). In the first variant of this paper, it is shown that an oil price shock affects real GDP. In fact, real GDP is reduced by 0.04 per cent. compared to the baseline, in response to a permanent increase of 25 per cent. in the oil price.

Equation (35) shows that the larger the discrepancy between the inverse of real GDP oil intensity (in the baseline) and the inverse of GDP oil intensity. The price of oil not only influences the price of imports in the long run, but also in the short run. Equation (37) states that the change in the rule-of-thumb price equals the price change, expressed in foreign currency, of the previous period, corrected for the simultaneous change in the exchange rate.

In the previous version of the model, the equilibrium export price of blocks of oil importing countries is determined by: where we define the effective foreign productivity, EFYMT, as:. In the previous section, we made a distinction between the price of oil and the price of other imports. The increase in the price of oil as a result of the increase in the mark-up, reduces the production.

Next, we specify an equation for aggregate demand in the RW block, taking into account the effects of a temporary income transfer due to a change in the price of oil. Remember that in the NIME model the export price for the RW block is denominated in Euros. Secondly, the shares of oil in a country bloc's total imports, i.e. wool, the observed shares available in OECD trade statistics, except for the new one.

V References

Selected NIME studies and publications

Selected research on oil price shocks