A Work Project, presented as part of the requirements for the Award of a Master Degree in Management from the NOVA – School of Business and Economics and INSPER –

Instituto de Ensino e Pesquisa.

Perceived Value in Payment Modes:

Cognitive and Affective Value among Brazilian Consumers

LUIZ HENRIQUE RANZANI DE MIRANDA 4283

A Project carried out on the Master in Management Program, under the supervision of Professors Luis Martinez from NOVA – School of Business and Economics, and Carla

Ramos from INSPER – Instituto de Ensino e Pesquisa.

LUIZ HENRIQUE RANZANI DE MIRANDA

Perceived Value in Payment Modes:

Cognitive and Affective Value among Brazilian Consumers

A project carried out on the Master in Management Program from Insper Instituto de Ensino e Pesquisa as part of the requirements for obtaining a Master Degree in Management.

Advisor: Prof. Dr. Carla Ramos - INSPER Instituto de Ensino e Pesquisa.

Co-Advisor: Prof. Dr. Luis Martinez – Nova

School of Business and Economics, Universidade Nova de Lisboa.

Ranzani de Miranda, Luiz Henrique

Perceived Value in Payment Modes: Cognitive and Affective Value among Brazilian Consumers /

Luiz Henrique Ranzani de Miranda — São Paulo, 2018. 54 páginas.

Thesis (Master – Master in Management Program) – Insper Instituto de Ensino e Pesquisa, 2018.

Advisor: Prof. Dr. Carla Ramos

Co-Advisor: Prof. Dr. Luis Martinez

1. Payment Modes. 2. Scale Development. 3. Cognitive Value. 4. Affective Value. 5. Consumer Perceived Value. 6. Decision Making.

LUIZ HENRIQUE RANZANI DE MIRANDA

Perceived Value in Payment Modes:

Cognitive and Affective Value among Brazilian Consumers

A project carried out on the Master in Management Program from Insper Instituto de Ensino e Pesquisa as part of the requirements for obtaining a Master Degree in Management.

Approval date: ___/___/___ JURY CARLA RAMOS ___________________________ ADVISOR INSPER LUIS MARTINEZ ___________________________ CO-ADVISOR

NOVA SCHOOL OF BUSINESS AND ECONOMICS

ADRIANA BRUSCATO BORTOLUZZO ___________________________ INSPER

JULIANA BONIMI ___________________________

FGV FUNDACAO GETULIO VARGAS

MARIA EUGENIA MATA ___________________________

NOVA SCHOOL OF BUSINESS AND ECONOMICS

IRENE CONSIGLIO ___________________________

ACKNOWLEDGEMENTS

First of all, I would like to thank my family and my fiancé that were very supportive in this journey, even when I was absent from family events and special dates due to my master program related commitments.

Special thanks to my advisor, Prof. Carla Ramos who, always with a good mood and a lot of patience, could guide me and help me through this journey to complete this dissertation project. I also like to thank my co-advisor, Prof. Luis Martinez who also helped me along the process.

I also would like to express my gratitude to Insper that provided me the opportunity to have a double degree and live in Lisbon. I also thank all the professors that I met during the master program.

Finally, I would also like to thank my classmates from MPA-10, as well as my Lisbon flatmates, for all the good times we had in their beautiful country.

RESUMO

Consumidores têm certas percepções em relação a diferentes meios de pagamento, como dinheiro, cartão de crédito ou de débito, ou pagamentos digitais. Essas percepções influenciam nos seus gastos e no seu comportamento de compra, e cada vez mais atenção vem sendo dedicada a esse fenômeno. Apesar da extensa literatura a respeito da subjetividade referente aos meios de pagamento e seus impactos no processo de tomada de decisão do consumidor, algumas contradições são evidenciadas em estudos passados. Além do que, existe uma lacuna no sentido de não existir uma escala que avalie a percepção dos consumidores em relação aos meios de pagamento. Este estudo foca no conceito de percepção do consumidor relativamente aos meios de pagamento, baseando-se na literatura de marketing referente a meio de pagamentos e em dois modelos teóricos bem aceitos – Paradigma Comportamental Cognitivo-Afetivo e Teoria do Valor de Consumo – para sugerir três hipóteses relacionadas ao valor cognitivo e afetivo percebido pelos consumidores. Para isso, nós nos concentramos nos meios de pagamentos considerados como o “mais tradicional” e o “mais inovador”, como por exemplo, dinheiro e pagamentos digitais. Este estudo tem dois objetivos: primeiro, desenvolver uma escala para medir o valor percebido pelos consumidores em relação aos meios de pagamentos e, segundo, mostrar que os meios de pagamento “mais tradicionais” são percebidos com um menor valor do que os “mais inovadores”. A escala sugerida é uma versão ampliada e adaptada do PERVAL, uma escala bem estabelecida para avaliar o valor de bens e serviços. A escala foi validada com uma amostra de dados de 400 consumidores brasileiros, utilizando a análise fatorial confirmatória. As hipóteses sugeridas foram testadas com os mesmos dados amostrais, utilizando o modelo de comparação de médias por meio de regressão linear múltipla. Os resultados mostram que o dinheiro é percebido pelos consumidores como tendo um menor valor cognitivo do que os demais meios de pagamento, e os pagamentos digitais com o que apresenta maior valor afetivo. Além disso, os pagamentos digitais foram percebidos de uma maneira geral como tendo o maior valor, captando também a atitude mais positiva por parte dos consumidores dentre aos meios de pagamento. Este estudo contribui com a literatura, primeiro por prover uma escala de avaliação do valor percebido pelos consumidores em relação aos meios de pagamento, considerando as dimensões cognitivas e afetivas e meios de pagamentos mais atuais. Segundo, mostramos que cada meio de pagamento é percebido de maneira diferente pelos consumidores, tendo os pagamentos digitais como o meio de pagamento com maior valor percebido. De acordo com a literatura, se espera que essas percepções afetem o processo de tomada de decisão do consumidor. Esse estudo também permite uma ideia mais clara das diferenças dos valores percebidos entre meios de pagamentos, resultando em insights para gerentes e para a indústria de pagamentos em como oferecer uma experiência de pagamento diferente para cada tipo de compra, assim como para o desenvolvimento de novos meios de pagamento.

PALAVRAS CHAVE: Meios de Pagamento, Desenvolvimento de Escala, Valor Cognitivo, Valor Afetivo, Valor Percebido pelo Consumidor, Processo de Decisão.

ABSTRACT

Consumers have been found to hold certain perceptions on Payment Modes (PMs) such as cash, credit or debit card, or digital payments, which will then influence their spending and purchasing behavior (e.g., the type, value and amount of purchased goods). Increasing attention has been devoted to this phenomenon. Despite the extensive body of

research on the subjectivity underlying PMs and subsequent impact on consumers’

decision-making process, contradictory findings have been reported. Moreover, a scale to assess consumers held perceptions of PMs is still lacking. This study focuses on the concept of consumer perception of PMs. We draw on the marketing literature on payments and on two well-accepted theoretical frameworks - the Cognitive-Affective Behavioral Paradigm and the Consumption Value Theory - to put forward three specific hypotheses on the cognitive and affective value perceived by consumers. We focus on what has been classified as the ‘most traditional’ and ‘more innovative’ PMs, i.e., cash and digital payments. The aim of this project is twofold: first, to develop a measurement scale for measuring consumers perceived value of PMs, and second, we show how traditional PMs are less valued by consumers than more innovative ones. The suggested scale is an extended and adapted version of PERVAL, a well-established scale for assessing the value of goods and services. The scale was validated with a sample data of 400 Brazilian consumers employing a confirmatory factor analysis. The suggested hypothesis were tested with the same database, using a mean comparison model via multi-linear regression. Results show that consumers perceive cash having the lower cognitive value when compared to other PMs, and digital holding the higher affective value. Also, digital was found having the highest overall perceived value, also leading to the most positive attitude regarding PMs. This study contributes to the literature, first by providing a consumer perceived value measurement scale for PM scale which considers recent PMs and the cognitive and affective dimensions. And second, we show that consumers perceive PM underlying value differently, perceiving digital PM as the one which results in higher value. This is expected to affect their decision-making. The research also provides managers and the payment industry with a clearer understanding of the differences in perceived value between different PMs, reflecting insights on the strategy regarding offered payment experiences for different types of purchases, as well as for the development of new PMs.

KEYWORDS: Payment Modes, Scale Development, Cognitive Value, Affective Value, Consumer Perceived Value, Decision Making

EXECUTIVE SUMMARY

In today`s world, payments are deeply present in people’s daily life and routines, being used in different contexts and formats. For these reason and added to the digitalization phenomenon that we are facing nowadays, the payments industry is constantly improving the traditional ways of paying, such as credit and debit card, developing new PMs such as

digital payments (mobile payments and digital wallets – Apple Pay, Samsung Pay and

others), with the aim of replacing cash and giving ways to a cashless society.

Thus, when going to shop (in-store or online), you might face the decision of choosing between different PMs to complete your purchase. And what do you feel when you choose one mode of payment instead of other to complete that purchase? What are your perceptions regarding this payment mode in your purchasing experience? What do you value the most in this payment mode that makes you want to use it again for other purchases? Do you thing that it can help you controlling your spending, or does it actually make you spend more? These are some questions that justifies the relevance of this study, and that are related to consumers’ perceptions of PM.

The first objective of this study is to we put forward a scale that allows measuring consumers’ perceived cognitive and affective value of different payment modes. Second, we use the developed and validated scale to understand the underlying consumer perceived value related to the modes of payments, which can be used to discuss and predict how specific PMs can influence consumers’ spending perceptions and thus their expected purchasing behaviors.

In order to do so, this study analyzed data collected from 400 respondents regarding four different types of PMs (cash, credit card, debit card and digital payments) in two purchase scenarios, low and high product price. It was a requirement that all the respondents had made a purchase in the last month and had used at least once in their life each of the four payment modes of the study. We then compared the differences between these four PMs regarding their underlying consumer perceived value.

Results showed that the different PM are perceived differently by costumers in terms of value. The cognitive perceived values are predominantly higher than the affective perceived value. Consumers perceive cash having the lower cognitive value when compared to other PMs, and digital payments holding the higher affective value. Also, digital

was found having the highest overall perceived value, also leading to the most positive attitude regarding PMs.

This study provides managers developing business in the payment industry, with the possibility of exploring with more confidence the fact that PMs are perceived differently from a cognitive-affective stand, as well as importance played by different values for specific PMs. Overall, we find that consumers are strongly willing to use payments that bring them convenience, availability and easy to use, as well as having a seamless purchasing experience.

Thus, this study contributes to the development of payments related business that are present in the market, helping them to better understand the payment consumer behavior: how consumers perceive the value underlying specific payments modes, which will affect their choice on how to pay. This can provide firms with insights on the best strategy in terms of offered consumer payment experience for different types of purchases and for insights for the payments industry to build new PMs.

LIST OF CONTENTS

1. INTRODUCTION ... 12

2. THEORETICAL BACKGROUND ... 14

2.1. Payment Modes and Payments Methods: Conceptual Definition ... 14

2.2. Payments Modes: Perception and Consumer Behavior ... 16

2.3. Consumer Decision Making and Perceived Value... 23

3. HYPOTHESES DEVELOPMENTS ... 26

3.1. Cognitive Perceived Value ... 27

3.2. Affective Perceived Value ... 28

3.3. Attitude Towards Payment Modes... 30

4. METHODOLOGY AND RESEARCH DESIGN ... 31

4.1. Data Collection ... 31

4.2. Data Analysis ... 33

5. RESULTS AND DISCUSSION ... 37

5.1 Descriptive Analysis ... 37

5.1 Multi-Linear Regression Model Analysis ... 39

6. CONCLUSIONS, LIMITATIONS AND FUTURE RESEARCH ... 43

6.1. Conclusions ... 43

6.2. Limitations and Future Research... 45

List of Tables

Table 1. Payments Modes ... 20

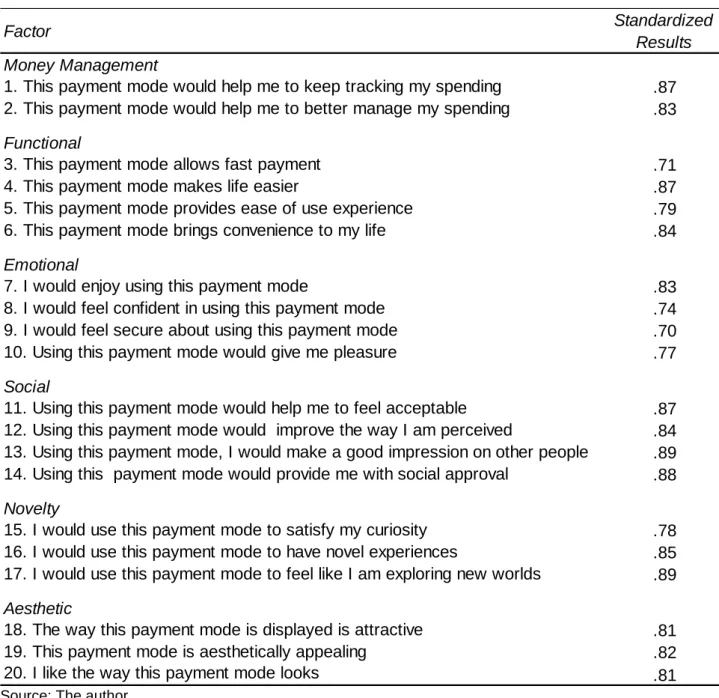

Table 2. Survey items ... 33

Table 3. Factor Analysis Results ... 34

Table 4. CFA fit statistics ... 35

Table 5. CR, AVE and Cronbach`s alpha ... 36

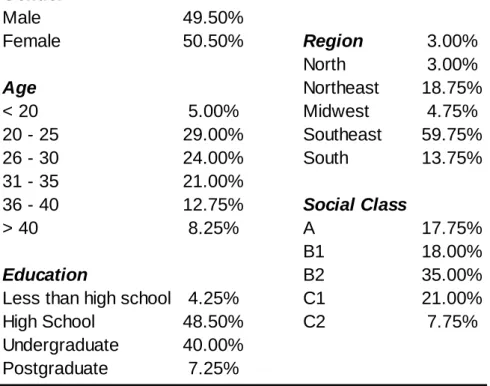

Table 6. Descriptive Analysis: Socio-demographic Information ... 37

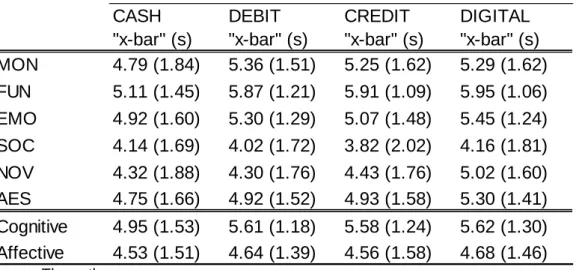

Table 7. Descriptive Analysis: Perceived Values x Payment Mode ... 39

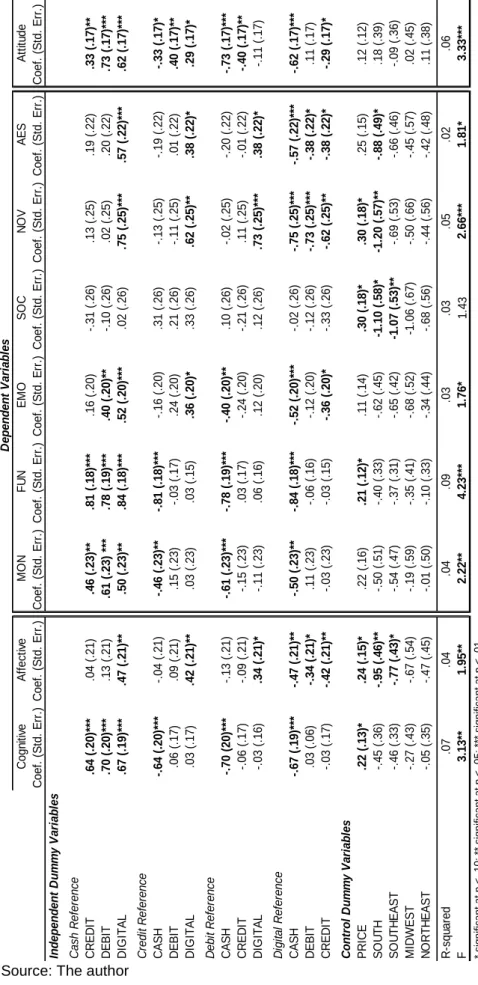

Table 8. Regression Results ... 40

List of Figures Figure 1. Payments Method and Payment Modes ... 15

1. INTRODUCTION

Payments are present and deeply embedded in people’s daily life and routines, being used in different contexts and formats. During the 1900s, cash and checks were the most

common forms of Payment Mode (PM), i.e., purchase exchange and financial transaction

format between people and organizations (Evans & Schmalensee, 2005). Since then, payment cards (credit and debit) appeared as a new way to pay in stores and to withdraw cash from automatic teller machines (ATMs) (Slawsky & Zafar, 2005). Also, Internet payments and Internet banks emerged with the electronic commerce as an alternative way for conducting financial transactions on the Internet (Zwass, 1996). The focus has recently shifted to a digital environment, where mobile phones, wearables, other objects (e.g. key cars), and digital wallets can be used as payment devices. The forecast is that, sooner or

later, cash will “die”, giving ways to a cashless society (Arvidsson & Markendahl, 2014;

Carton & Hedman, 2013; Hedman, 2012).

Payments based research can be classified as multi-disciplinary, given that it can be found in diverse areas, such as Information Systems (IS), Economics, Psychology and Business. The IS based research is mostly related to the adoption and diffusion of digital payment technologies (e.g. Dahlberg et al., 2008; Holmström & Stalder, 2001; Jonker, 2007; Schierz et al., 2010). Scholars from the economics school are mostly interested in the macro level of payment patterns (e.g. Garcia-Swartz et al., 2004, 2006; Humphrey, 2004, 2010; Prelec & Loewenstein, 1998). The scholars from the psychology stand are mostly interested in understanding how the payment context (e.g. pricing mechanism) affects the paying behavior (e.g. Gneezy et al., 2010; Jung et al., 2014; Menon et al., 1997). Finally, business scholars in consumer research and marketing are interested in understanding how different

PMs can influence consumer decision-making and spending behavior (e.g. Chatterjee &

Rose, 2012; Hirschman, 1979; Raghubir & Srivastava, 2008; Thomas et al., 2011). The latter area of payments based research has attracted the furthermost attention, having generated diverse results with implications for businesses and for the payment industry, namely in what concerns the design of new PMs driven by the digitalization phenomenon and increasing adoption of electronic payments and replacement of cash payments (Capgemini & BNP Paribas, 2017).

In the marketing area, research suggests that the PM affects not only how much it is spent, but also the type of purchase that is made (Thomas, Desai, & Seenivasan, 2011), as

well as the feeling of ownership regarding the purchased product (Kamleitner & Erki, 2013). For example, Van der Horst and Matthijsen (2013) studied negative emotions associated with PMs and resulting pain of making the payment. Moreover, credit card payments have been found to increase the incidence of unplanned, unhealthy, indulgent food purchases (Thomas et al., 2011); this study links emotions to PMs. Bagchi and Block (2011) found results that contradict the latter, showing that in fact cash payments increase the likelihood of such purchases. This inconsistency of findings in the payments literature suggest that the way consumers pay for what they buy differs, not only in terms of physical dimensions, but also in terms of the mental and emotional experiences that specific PMs generate before, during and after being used. It also hints to the lack of a coherent view in the marketing payments literature on how to assess consumer perception of specific PMs.

The cognitive and affective aspects of PMs have been overlooked in the literature. There are nevertheless some exceptions. For example, Khan et al. (2015) developed a conceptual framework to measure consumer perceptions of PM which integrated the cognitive and emotional dimensions (scale PPM – Perception of Payment Modes). However, this suggested scale did not show a clear differentiation between the cognitive and the emotional aspects, and focused solely on cash and card payments, not providing a widely applicable measurement of consumers’ perception of payments mode. Moreover, this study did not consider any form of digital payment associated with the innovative usage of mobile devices and digital wallets to purchase goods and service.

The aim of this study is thus twofold. First, based on the Cognitive-Affective Behavioral Paradigm and on Consumption Value Theory, we argue that to understand and

predict how specific PMs can influence consumers’ spending perceptions and thus their

purchasing behaviors, it is necessary to understand their underlying perceived value. Drawing on this premise, we put forward several hypotheses on consumers’ perceived value among different PMs (i.e., cash versus electronic PMs- credit card, debit card and digital payments). Results shed some light on consumers’ perceived differences in terms of value of different payments modes. Second, we put forward a scale that allows measuring consumers’ perceived cognitive and affective value of different PMs, namely digital modes. We believe that this distinction is necessary to allow service providers and the payments industry developing well-informed strategies regarding the usage and development of PMs.

This research entails quantitative approach. A research model was built based on the literature review and a quantitative method was used with a database of 400 Brazilian

respondents to validate the suggested scale of consumer perceived value of PMs, as well as to test the hypotheses included in our conceptual model.

This study contributes to the literature, first by improving the previously developed PM scales on the perception of PMs in two ways: it is based on well-established models of consumer behaviur - Cognitive-Affective Behavioral Paradigm and the Consumption Value theory - and it considers digital payments which are the most recent payments instruments that have been introduced in the payments industry. Second, it shows the relevance of considering the cognitive and affective value of PMs, something that has not been fully addressed in the literature. This study also makes important managerial contributions. The market can benefit from this study, as it allows better understanding expected consumer payment behavior: it grasps how consumers perceive the value underlying specific PMs, which then affects their choice of PMs and their purchasing behavior. This can provide firms with insights on the best strategy in terms of offered consumer payment experience for different types of purchases. This can result in financial benefits.

This project is divided into six major sections. In the following section, we present the literature review, as well as the suggested scale for consumer`s perceived value of PMs and our hypotheses. We then describe in section four our methodological choices and research design. In section five, we present and discuss the findings, and conclude with a section on overall conclusions, limitations and suggestions for future research.

2. THEORETICAL BACKGROUND

2.1. Payment Modes and Payments Methods: Conceptual Definition

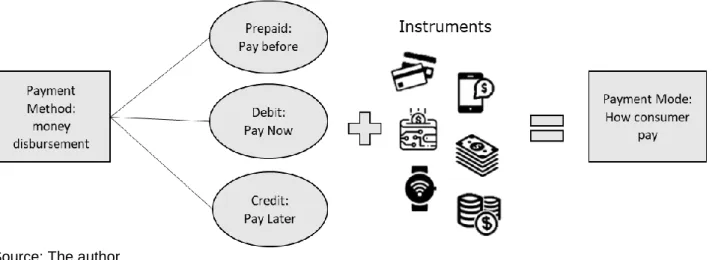

The literature on payments hints a misconception on the definition of PMs and payment methods. Previous authors have used the two concepts interchangeably, using them as synonyms to define the way or the instruments/tools (cash, checks, cards, etc.) that consumer use to make payments (e.g. Hirschman, 1979; Soman, 2011; Schuh & Stavins, 2013; Khan et al., 2015). This misconception may have its origin in the in the traditional bricks and mortar based transactions that considered cash, checks, debit cards, and credit cards as payment methods (Foster et al. 2011). However, the payments industry that is driven by two big brands (VISA and Mastercard), uses a different definition for these two concepts. In summary, Payment Methods are classified according to the moment that the user/consumer disburses the amount of money corresponding to the payment, resulting in

three types of methods: prepaid (pay before), debit (pay now) and credit (pay later) (see figure 1 below).

Payment Modes, on the other hand, result from the combination between the adopted payment method and the instruments or tools that the buyer uses to make the payment in an online or offline environment (see figure 1). Most of the times, the payment mode has a payment method embedded in the payment instrument that is used, resulting in a specific ways that consumers can use to make the payment (e.g., payment cards, digital payments - mobile phone, wearables and digital wallets - , e-cash, cash, etc.). Hove and Farhod (2011) identify six groups of payments by combining the time dimension (i.e., pay-before, pay-now, and pay-later) and the payment instrument (i.e., paper or electronic). Pay-before requires buyers to deposit funds into an account prior to the actual purchase. This type of payment includes stored-value cards, prepaid cards, and gift cards. Pay-now refers to payments settled (almost) immediately, using types such as cash on delivery and debit cards. Pay-later allows the buyers to consume the products or services first and then settle the account later, using such types as credit cards and charge cards.

Figure 1. Payments Method and Payment Modes

Source: The author

This study focuses on payment modes, and considers cash, payment cards (debit and credit) and digital payments (mobile and digital wallets). We therefore consider the payments modes that according to BACEN (Estatísticas de Pagamentos de Varejo e de Cartões no Brasil 2016) are the most used in Brazil - cash and payments cards -, as well as the mode that is considered the most trendy and innovative - digital payments. In summary, whilst cash and payment cards are either associated with pay now (cash and debit card)

and pay later (credit card) payment methods, digital payments can correspond to any payment method (i.e., pay before, now or later). Moreover, cash corresponds to disbursement of coins and federal reserve notes. The debit card allows the cardholder to make a payment that is deducted directly from a bank account at the time of purchase or bill payment. The credit card authorizes the cardholder to make a purchase by granting a line of credit that will be paid back to the card company at a later date, possibly in installments. Finally, the digital PM allows the cardholder to make cashless and card-free payment (e.g., mobile payments and digital wallets).

2.2. Payments Modes: Perception and Consumer Behavior

Earlier marketing research on PMs focused mostly in predicting how specific

perceptions and feelings underlying PMs could influence consumers’ spending and

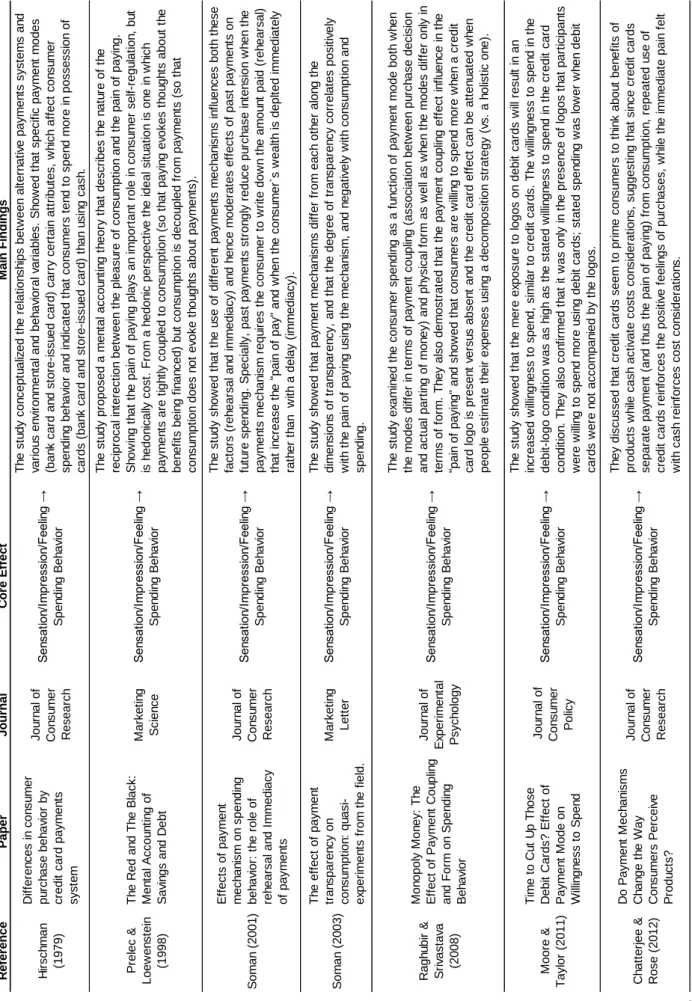

purchasing behavior. More specifically, and as shown in Table 2 included at the end of this section, previous studies on PM look into the following effects regarding consumers perceptions and behaviors: 1) how PM characteristics or attributes affect consumers’ perceptions of the PM, which then conditions consumer spending behavior; 2) how the purchasing context results in specific sensations, impressions or feelings regarding the used PM, and how these affect consumer spending behavior; or more simply as 3) the purchasing context (i.e., product price, type and amount; buying in-store or online; etc.), 4) the sensations, impressions, or feelings, and 5) the perception of a PM impact consumer spending behavior.

Overall, specific PMs have been found to carry certain perceptions and associations that influence consumers’ behavior (Hirschman, 1979). More specifically, PMs underlying subjectivity have been found to affect the type, value and amount of products purchased per transaction (Prelec & Simester, 2001; Thomas et al., 2011; Runnemark, Hedman & Xiao, 2015), the probability and speed of purchasing (Feinberg, 1986), and the transaction size (Abdul‐Muhmin, 2010). Effects have also been found over consumers’ feeling of ownership

regarding the purchased product (Kamleitner & Erki, 2013) and their ‘mental accounting’

(i.e., ‘‘set of cognitive operations used by individuals and households to organize, evaluate and keep track of financial activities’’ (p. 40); Thaler, 1980).

Each PM is associated with specific perceptions of spending, which affects consumer spending behavior. For example, research demonstrates that the presence of a credit card logo only, can induce higher willingness to spend (Feinberg, 1986; Raghubir & Srivastava,

2008). Moreover, previous research shows that consumers tend to spend more when using card payments than when using cash (Feinberg, 1986; Hirschman, 1979). Consumer perceptions of spending associated with PMs also result in sensations, impressions, or feeling, such as that of ‘pain of paying’ (Prelec & Loewenstein, 1998). On this effect, previous research indicates that paying with cash is often more painful than paying with a card, an electronic PM (Prelec & Loewenstein, 1998; Raghubir & Srivastava, 2008). Moreover, this negative feeling may signal to the consumer that there is some kind of problem, and lead him to think more concretely about his spending (Schwarz, 2002; Wegner & Vallacher, 1986).

This feeling that cash based PMs are more painful than card based PMs has been widely studied and several reasons have been found to explain this phenomenon. First, cash can be classified the most transparent form of payment, with high vividness and salience (Raghubir & Srivastava, 2008; Soman, 2003), creating a more conscious understanding of the value that is being exchanged during a purchase. Cards, on the other hand, are an opaque form of payment as they do not involve the same physical price rehearsal (Soman 2003), which means that during the purchase people may not think too much about the money they are spending. As a consequence, people are expected to pay more attention be more prudent when paying with cash than with card, resulting in a more intense pain of payment. Second, card based PMs are psychologically decoupled from the purchase, and the lack of transparency makes the cost of the transaction more obscured, thus reducing the ‘pain of paying’ (Prelec and Loewenstein, 1998; Raghubir and Srivastava, 2008; Thaler, 1999; Tokunaga, 1993). Aligned with these assumptions, Chatterjee and Rose (2012)

suggest that since credit cards separate payment (and thus, the ‘pain of paying’) from

consumption, repeated use of credit cards reinforces the positive feelings of spending, while the immediate pain felt with cash reinforces cost considerations.

The third reason that can explain why card based PM are less painful than cash based PMs, is associated with consumers’ mental representations of the paying process. More precisely, paying by cash often involves a complicated process of handing over a visible amount of cash to another person and receiving back some small amount of change; it also involved counting the received change and putting it back in a wallet or pocket (Hancock & Humphrey, 1997). By contrast, the process of card based PM is often construed simply as handing in the card, signing or PIN entering, and taking the card back. Sometimes this process can be reduced to just tapping the card or other payment device in the POS

machine. Thus, the process of paying with an electronic instrument may be more likely to be associated with the feeling of ease of use while the process of paying with cash might be associated with the feeling of ‘pain of paying’.

Several other studies, some conducted in controlled environment by the use of experiments, have been able to confirm PMs’ strong subjectivity and emotional nature. For example, Thomas et al. (2011) also tried to link emotions to specific PMs, assessing the effect of the ‘pain of paying’ via happy-sad face scales and lists of words identifying negative associations. Van der Horst and Matthijsen (2013) examined the response of the brain to videos with cash and debit card payments, and found that paying with cash triggers more positive emotions than paying by debit card.

A few studies on PMs and consumer behavior focus on how some objective characteristics and attributes of PMs, which are differently perceived by the customer, influence the adoption and usage of those PMs (Schuh & Stavins, 2013), intention to use (Liao, Shi & Wong, 2012; Teoh, Chong, Lin & Chua, 2013), and consequently consumers spending behavior (Hirschman, 1982). Research revealed several PM objective attributes along which performance was perceived to differ (Hirschman, 1982). Setup and record keeping were found being especially important in explaining PM adoption, while security was identified as important in explaining which methods consumers use for transactions (Schuh & Stavins, 2013). Benefits, self-efficacy, ease of use, convenience, automatic add-value service, compact design, security, reliability, and merchant support were identified as important PMs attributes in consumer decision making regarding the usage of specific PMs (Liao, Shi & Wong, 2012; Teoh, Chong, Lin & Chua, 2013).

Despite the recognition that PMs objective features are relevant and can determine consumer spending behavior, the predominant view and research object is that consumers’ subjective perceptions and felt sensations, impressions or feelings conditions that behavior (see Table 2). However, despite the extensive body of research on the subjectivity underlying PMs and perceptions that different PMs trigger on consumers, some of previously found results are contradictory. For example, Schuh & Stavins, 2013 and Teoh, Chong, Lin & Chua, 2013 talk about different perceived attributes of the same PMs. Also, in the context of purchasing food products for immediate consumption, Inman et al. 2009 and Bagchi & Block, 2012 find different perceived values for the same PMs.

We believe these contradictory results can be explained by the inexistence of a well-established scale to assess consumers held perceptions of PMs. One exception is the scale

for measuring consumer perceptions of PMs (i.e., the PPM scale) by Khan, Belk and Craig-Lees (2015). The developed and validated scale includes constructs to capture consumers’ emotions, felt social and personal gratification and resulting money management. However, this study was developed specifically for debit and credit cards only. Therefore, the suggested PPM scale did not provide a widely applicable measurement of the consumer`s perception of different PMs. Besides not being flexible, the PPM scale not does consider more innovative modes to purchase goods and service such as digital payments (mobile devices and digital wallets). The authors did nevertheless point this gap as future avenues for research. Finally, although it mentions the cognitive and emotional perceptions underlying PMs, these are used interchangeably in the scale, not being possible to differentiate between them.

A well-established and universal scale would not only allow to identify how consumers perceive different PMs, but also which ones they prefer for each specific situation and to predict how each PM would affect consumers’ buying behavior. In this study, besides proposing (and validating) such scale, drawing on the extant literature review, we put forward specific hypothesis on the perceptions held by consumers on the most traditional and more innovative PMs: cash and digital payments. But how should this perception be captured. This is discussed in the following section.

Table 1. Payments Modes R e fe re n c e P a p e r J o u rn a l C o re E ff e c t H ir sch m a n (1 9 7 9 ) D if fe re n ce s in co n su m e r p u rch a se b e h a vi o r b y cr e d it ca rd p a ym e n ts syst e m Jo u rn a l o f C o n su m e r R e se a rch S en sa tio n/ Im pr essi on /F ee lin g → S p e n d in g B e h a vi o r P re le c & L o e w e n st e in (1 9 9 8 ) T h e R e d a n d T h e B la ck: M e n ta l A cco u n ti n g o f S a vi n g s a n d D e b t M a rke ti n g S ci e n ce S en sa tio n/ Im pr essi on /F ee lin g → S p e n d in g B e h a vi o r S o m a n ( 2 0 0 1 ) E ff e ct s o f p a ym e n t m e ch a n ism o n sp e n d in g b e h a vi o r: t h e r o le o f re h e a rsa l a n d I m m e d ia cy o f p a ym e n ts Jo u rn a l o f C o n su m e r R e se a rch S en sa tio n/ Im pr essi on /F ee lin g → S p e n d in g B e h a vi o r S o m a n ( 2 0 0 3 ) T h e e ff e ct o f p a ym e n t tr a n sp a re n cy o n co n su m p ti o n : q u a si -e xp e ri m e n ts fr o m t h e f ie ld . M a rke ti n g L e tt e r S en sa tio n/ Im pr essi on /F ee lin g → S p e n d in g B e h a vi o r R a g h u b ir & S ri va st a va (2 0 0 8 ) M o n o p o ly M o n e y: T h e E ff e ct o f P a ym e n t C o u p lin g a n d F o rm o n S p e n d in g B e h a vi o r Jo u rn a l o f E xp e ri m e n ta l P sych o lo g y S en sa tio n/ Im pr essi on /F ee lin g → S p e n d in g B e h a vi o r M o o re & T a yl o r (2 0 1 1 ) T im e t o C u t U p T h o se D e b it C a rd s? E ff e ct o f P a ym e n t M o d e o n W ill in g n e ss to S p e n d Jo u rn a l o f C o n su m e r P o licy S en sa tio n/ Im pr essi on /F ee lin g → S p e n d in g B e h a vi o r C h a tt e rj e e & R o se ( 2 0 1 2 ) D o P a ym e n t M e ch a n ism s C h a n g e t h e W a y C o n su m e rs P e rce iv e P ro d u ct s? Jo u rn a l o f C o n su m e r R e se a rch S en sa tio n/ Im pr essi on /F ee lin g → S p e n d in g B e h a vi o r T h e st u d y sh o w e d t h a t th e m e re e xp o su re t o l o g o s o n d e b it ca rd s w ill r e su lt i n a n in cr e a se d w ill in g n e ss to sp e n d , si m ila r to cr e d it ca rd s. T h e w ill in g n e ss to sp e n d i n t h e d e b it -l o g o co n d it io n w a s a s h ig h a s th e st a te d w ill in g n e ss to sp e n d i n t h e cr e d it ca rd co n d it io n . T h e y a lso co n fi rm e d t h a t it w a s o n ly in t h e p re se n ce o f lo g o s th a t p a rt ici p a n ts w e re w ill in g t o sp e n d m o re u si n g d e b it ca rd s; st a te d sp e n d in g w a s lo w e r w h e n d e b it ca rd s w e re n o t a cco m p a n ie d b y th e l o g o s. T h e y d iscu sse d t h a t cr e d it ca rd s se e m t o p ri m e co n su m e rs to t h in k a b o u t b e n e fi ts o f p ro d u ct s w h ile ca sh a ct iv a te co st s co n si d e ra ti o n s, su g g e st in g t h a t si n ce cr e d it ca rd s se p a ra te p a ym e n t (a n d t h u s th e p a in o f p a yi n g ) fr o m co n su m p ti o n , re p e a te d u se o f cr e d it ca rd s re in fo rce s th e p o si ti ve f e e lin g s o f p u rch a se s, w h ile t h e i m m e d ia te p a in f e lt w it h ca sh r e in fo rce s co st co n si d e ra ti o n s. T h e st u d y sh o w e d t h a t th e u se o f d if fe re n t p a ym e n ts m e ch a n ism s in fl u e n ce s b o th t h e se fa ct o rs (r e h e a rsa l a n d i m m e d ia cy) a n d h e n ce m o d e ra te s e ff e ct s o f p a st p a ym e n ts o n fu tu re sp e n d in g . S p e ci a lly, p a st p a ym e n ts st ro n g ly re d u ce p u rch a se i n te n si o n w h e n t h e p a ym e n ts m e ch a n ism r e q u ir e s th e co n su m e r to w ri te d o w n t h e a m o u n t p a id ( re h e a rsa l) th a t in cr e a se t h e " p a in o f p a y" a n d w h e n t h e co n su m e r` s w e a lt h i s d e p lt e d i m m e d ia te ly ra th e r th a n w it h a d e la y (i m m e d ia cy) . M a in F in d in g s T h e st u d y co n ce p tu a liz e d t h e r e la ti o n sh ip s b e tw e e n a lt e rn a ti ve p a ym e n ts syst e m s a n d va ri o u s e n vi ro n m e n ta l a n d b e h a vi o ra l va ri a b le s. S h o w e d t h a t sp e ci fi c p a ym e n t m o d e s (b a n k ca rd a n d st o re -i ssu e d ca rd ) ca rr y ce rt a in a tt ri b u te s, w h ich a ff e ct co n su m e r sp e n d in g b e h a vi o r a n d i n d ica te d t h a t co n su m e rs te n d t o sp e n d m o re i n p o sse ssi o n o f ca rd s (b a n k ca rd a n d st o re -i ssu e d ca rd ) th a n u si n g ca sh . T h e st u d y p ro p o se d a m e n ta l a cco u n ti n g t h e o ry th a t d e scr ib e s th e n a tu re o f th e re ci p ro ca l in te re ct io n b e tw e e n t h e p le a su re o f co n su m p ti o n a n d t h e p a in o f p a yi n g . S h o w in g t h a t th e p a in o f p a yi n g p la ys a n i m p o rt a n t ro le i n co n su m e r se lf -r e g u la ti o n , b u t is h e d o n ica lly co st . F ro m a h e d o n ic p e rsp e ct iv e t h e i d e a l si tu a ti o n i s o n e i n w h ich p a ym e n ts a re t ig h tl y co u p le d t o co n su m p ti o n ( so t h a t p a yi n g e vo ke s th o u g h ts a b o u t th e b e n e fi ts b e in g f in a n ce d ) b u t co n su m p ti o n i s d e co u p le d f ro m p a ym e n ts (so t h a t co n su m p ti o n d o e s n o t e vo ke t h o u g h ts a b o u t p a ym e n ts) . T h e st u d y sh o w e d t h a t p a ym e n t m e ch a n ism s d if fe r fr o m e a ch o th e r a lo n g t h e d im e n si o n s o f tr a n sp a re n cy, a n d t h a t th e d e g re e o f tr a n sp a re n cy co rr e la te s p o si ti ve ly w it h t h e p a in o f p a yi n g u si n g t h e m e ch a n ism , a n d n e g a ti ve ly w it h co n su m p ti o n a n d sp e n d in g . T h e st u d y e xa m in e d t h e co n su m e r sp e n d in g a s a f u n ct io n o f p a ym e n t m o d e b o th w h e n th e m o d e s d if fe r in t e rm s o f p a ym e n t co u p lin g ( a sso ci a ti o n b e tw e e n p u rch a se d e ci si o n a n d a ct u a l p a rt in g o f m o n e y) a n d p h ysi ca l fo rm a s w e ll a s w h e n t h e m o d e s d if fe r o n ly in te rm s o f fo rm . T h e y a lso d e m o st ra te d t h a t th e p a ym e n t co u p lin g e ff e ct i n fl u e n ce i n t h e "p a in o f p a yi n g " a n d sh o w e d t h a t co n su m e rs a re w ill in g t o sp e n d m o re w h e n a cr e d it ca rd l o g o i s p re se n t ve rsu s a b se n t a n d t h e cr e d it ca rd e ff e ct ca n b e a tt e n u a te d w h e n p e o p le e st im a te t h e ir e xp e n se s u si n g a d e co m p o si ti o n st ra te g y (v s. a h o list ic o n e ).

R e fe re n c e P a p e r J o u rn a l C o re E ff e c t F e in b e rg (1 9 8 6 ) C re d it C a rd s a s S p e n d in g F a ci lit a ti n g S ti m u li: A C o n d it io n in g I n te rp re ta ti o n Jo u rn a l o f C o n su m e r R e se a rch P ur ch ase C on te xt → S en sa tio n/ Im pr essi on /F ee lin g → S p e n d in g B e h a vi o r P re le c & S im e st e r (2 0 0 1 ) A lw a ys L e a ve H o m e W it h o u t It : A F u rt h e r In ve st ig a ti o n o f th e C re d it -C a rd E ff e ct o n W ill in g n e ss to P a y M a rke ti n g L e tt e r P ur ch ase C on te xt → S pe nd in g B e h a vi o r A b d u l‐ M u h m in (2 0 1 0 ) T ra n sa ct io n si ze e ff e ct s o n co n su m e rs' r e ta il p a ym e n t m o d e ch o ice In te rn a ti o n a l Jo u rn a l o f R e ta il & D ist ri b u ti o n M a n a g e m e n t P ur ch ase C on te xt → S en sa tio n/ Im pr essi on /F ee lin g → S p e n d in g B e h a vi o r T h o m a s e t a l. (2 0 1 1 ) H o w cr e d it ca rd p a ym e n ts in cr e a se u n h e a lt h y fo o d p u rch a se s: V isce ra l re g u la ti o n o f vi ce s Jo u rn a l o f C o n su m e r R e se a rch P ur ch ase C on te xt → S en sa tio n/ Im pr essi on /F ee lin g → S p e n d in g B e h a vi o r K a m le it n e r & E rki ( 2 0 1 3 ) P a ym e n t m e th o d a n d p e rce p ti o n s o f o w n e rsh ip M a rke ti n g L e tt e rs P ur ch ase C on te xt → S en sa tio n/ Im pr essi on /F ee lin g → S p e n d in g B e h a vi o r R u n n e m a rk, H e d m a n & X ia o ( 2 0 1 5 ) D o co n su m e rs p a y m o re u si n g d e b it ca rd s th a n ca sh ? E le ct ro n ic C o m m e rce R e se a rch a n d A p p lica ti o n s P ur ch ase C on te xt → S en sa tio n/ Im pr essi on /F ee lin g → S p e n d in g B e h a vi o r T h e st u d y e xa m in e d t h e u n d e rl yi n g m e ch a n ism o f th e r e la th io n sh ip b e tw e e n p a ym e n t m e th o d s a n d sp e n d in g b e h a vi o r b y in ve st ig a ti n g w h e th e r co n su m e rs p a y m o re f o r id e n ti ca l p ro d u ct s u si n g d e b it ca rd s co m p a re d t o ca sh . T h e y sh o w e d t h a t p e o p le a re w ill in g t o p a y m o re f o r id e n ti ca l p ro d u ct s w it h d e b it ca rd s th a n w it h ca sh , su g g e st in g th a t is b e ca u se o f th e r e p re se n ta ti o n o f m o n e y, l e a d in g t o sa lie n ce o f p h ysi ca l fo rm a n d th e sa lie n ce o f th e a m o u n t p a id w it h t h e ca rd . T h e y a lso su g g e st e d t h a t th e f o rm a t o f m a n e y m a tt e rs. T h e st u d y sh o w e d t h a t p a ym e n t m o d e s a lso i n fl u e n ce h o w co n su m e rs fe e l a b o u t th e a cq u ir e d g o o d , fo cu s o n t h e e ff e ct s o f th e p a ym e n ts m o d e o n p sych o lo g ica l o w n e rsh ip (p e rce p ti o n o f a n o b je ct a s m in e ). T h e y sh o w e d t h a t ca sh p a ym e n t is st ro n g e r p sych o lo g ica l o w n e rsh ip b e ca u se i t in fl u e n ce s th e e xt e n t o f p e rce iv e d i n ve rst m e n t in a n o b je ct ( ca sh p a ye rs fe e l m o re p o sse ssi ve a b o u t a n a cq u ir e d o b je ct t h a n ca rd p a ye rs) . M a in F in d in g s T h e y sh o w e d t h a t th e e ff e ct s o f m o d e o f p a ym e n t a re co n ti n g e n t o n t h e t yp e o f p ro d u ct (u n h e a lt h y fo o d ). T h e ir r e su lt s q u a lif ie d t h e t h a t p a in o f p a ym e n t a ff e ct s th e w ill in g n e ss to sp e n d m o n e y b y d e m o n st ra ti n g t h a t re la ti ve to d e lib e ra ti ve p u rch a se d e ci si o n s, im p u lsi ve p u rch a se d e ci si o n s a re m o re l ike ly to b e i n fl u e n ce d b y p a in o f p a ym e n t. T h e y a lso co n tr ib u te d t o t h e d e b a te o n w h e th e r im p u lsi ve d e ci si o n s to p u rch a se u n h e a lt h y p ro d u ct s ca n b e ch a ra ct e ri ze d a s ra ti o n a l ch o ice s. T h e r e su lt t h a t p u rch a se s o f im p u lsi ve p ro d u ct s a re i n fl u e n ce d b y p a in o f p a ym e n t, b u t th o se o f p la n n e d p ro d u ct s a re n o t, i m p lie s th a t th e i m p u lsi ve p u rch a se d e ci si o n s ca n n o t b e a d e q u a te ly e xp la in e d b y th e r a ti o n a l ch o ice m o d e l. F u rt h e r, t h e ir r e su lt s su g g e st t h a t se lf -co n tr o l is n o t e n ti re ly vo lit io n a l; i t ca n b e f a ci lit a te d o r im p e d e d b y co n te xt u a l fa ct o rs th a t ch a n g e t h e v isce ra l re sp o n se s. T h e st u d y e xa m in e d h o w t h e m o n e ta ry va lu e o f a r e ta il tr a n sa ct io n ( tr a n sa ct io n si ze ) im pa ct s co nsu m er s’ p re fe re nce s fo r ca sh , de bi t an d cr ed it ca rd p aym en t . T he y sh ow ed th a t p re fe re n ce s fo r d e b it a n d cr e d it ca rd p a ym e n t m o d e s a re si m ila r a t lo w t ra n sa ct io n va lu e s (b o th a re l e ss p re fe rr e d ), w h ilst t h o se f o r d e b it a n d ca sh p a ym e n t a re si m ila r a t la rg e t ra n sa ct io n v a lu e s (a g a in , b o th a re l e ss p re fe rr e d ). T h e y a lso su g g e st e d t h a t e le ct ro n ic p a ym e n t m o d e s a re co lle ct iv e ly a su b st it u te f o r ca sh f o r lo w t ra n sa ct io n va lu e s, w h ilst cr e d it ca rd s a re a su b st it u te f o r ca sh a n d d e b it ca rd s fo r h ig h t ra n sa ct io n va lu e s. T h e st u d y sh o w e d t h a t cr e d it ca rd st im u li d ir e ct e d sp e n d in g su ch t h a t th e p ro b a b ili ty, sp e e d , o r m a g n it u d e o f sp e n d in g w a s e n h a ce d i n t h e p re se n ce o f cr e d it ca rd cu e s. T h e st u d y p re se n te d n e w e vi d e n ce su p p o rt in g t h e p ro p o si ti o n t h a t co n su m e rs a re w ill in g to sp e n d m o re f o r a p ro d u ct w h e n u si n g a cr e d it ca rd ( in a t le a st so m e p u rch a se co n te xt s) . T h e r e su lt s a re su rp ri si n g b o th d u e t o t h e si ze o f th e p re m iu m a n d t h e u b iq u it y o f cr e d it ca rd u se . T h e ir r e su lt s re ve a l a p o te n ti a lly la rg e cr e d it ca rd p re m iu m , b u t th e e ff e ct i s n o t a lw a ys p re se n t. I n t h e f ir st st u d y, w h ich u se s g o o d s w it h u n ce rt a in m a rke t va lu e , w a s o b se rv e d a l a rg e p re m iu m ( m o re t h a n 1 0 0 % ). H o w e ve r, i n t h e se co n d st u d y, u si n g a g o o d w it h a kn o w n m a rke t va lu e ( a r e st a u ra n t g if t ce rt if ica te ) th e p re m iu m d o e s n o t a lw a ys a ri se .

Source: The author R ef er en ce P ap er Jo u rn al C o re E ff ec t H irsch m an (1 98 2) C on su m er p aym en t sys te m s: t he r el at io nsh ip o f at tr ib ut e st ru ct ur e to pr ef er en ce a nd u sa ge . T he Jo ur na l of B usi ne ss R ese ar ch C ha ra ct er ist ics → Pe rce pt io n → S pe nd in g B eh av io r Li ao , S hi & W on g (2 01 2) C on su m er p er ce pt io ns of th e sm ar tca rd in r et ai lin g: an e m pi rica l S tu dy. Jo ur na l o f in te rn at io na l C on su m er M ar ke tin g C ha ra ct er ist ics → Pe rce pt io n → S pe nd in g B eh av io r S ch uh & S ta vi ns (2 01 3) H ow C on su m er s P ay: A do pt io n an d U se o f P aym en ts C on su m er P aym en ts R ese ar ch C en te r C ha ra ct er ist ics → Pe rce pt io n → S pe nd in g B eh av io r T eo h, C ho ng , Li n & C hu a (2 01 3) F act or s af fe ct in g co nsu m er s’ p er ce pt io n of el ect ro ni c pa ym en t: a n em pi rica l a na lysi s In te rn et R ese ar ch C ha ra ct er ist ics → Pe rce pt io n → S pe nd in g B eh av io r K ha n, B el k & C ra ig -L ee s (2 01 5) M ea su rin g co nsu m er pe rce pt io ns of p aym en t m od e Jo ur na l o f E co no m ic P syc ho lo gy Pe rce pt io n → Sp en di ng B eh av io r T he y de ve lo pe d a co nce pt ua l a nd e m pi rica l f ra m ew or k an d sh ow ed h ow t he co nst ru ct s an d th e sca le s ca pt ur e pe rce pt io ns of p aym en t m od es( P P M ). T he P P M sca le re pr ese nt ed f ou r di m en si on s: e m ot io ns re la tin g to ca sh a nd ca rd b ase d pa ym en t m od es, so ci al a nd p er so na l g ra tifica tio n an d m on ey m an ag em en t. It al so sh ow ed th at co nsu m er p er ce pt io ns of p aym en t m od es in flu en ce sp en di ng b eh av io r a nd p re di ct ow ne rsh ip o f fin an ci al ca rd s in p osse ssi on , i nd ica tin g th at th e PP M sca le is use fu l i n un de rst an di ng co nsu m er co gn iti ve a nd e m ot io na l a sso ci at io ns w ith p aym en t m od es, pa rti cu la rly to th e use o f ‘ ‘o w ne d m on ey’ ’ a nd h ow th ese a sso ci at io ns im pa ct o n pa ym en t m od e ch oi ce . T he st ud y ex pl or ed t he f act or s in flu en ci ng p er ce pt io n to w ar ds el ect ro ni c pa ym en t (e -pa ym en t) fro m th e M al aysi an co nsu m er s’ p er sp ect ive . T he y fo un d th at b en ef its, se lf-ef fica cy, a nd e ase o f u se e xe rt si gn ifi ca nt in flu en ce s on co nsu m er s’ p er ce pt io n to w ar ds e-pa ym en t. H ow ev er , th e in si gn ifi ca nt r esu lts ob ta in ed f or t ru st a nd se cu rit y w ar ra nt fu rt he r in ve st ig at io n. T he y est im at ed t he a do pt io n (f irst st ag e, e xt en si ve m ar gi n) a nd u se ( se co nd st ag e, in te nsi ve m ar gi n) o f se ve n pa ym en t m et ho ds an d fo un d th at t he ch ar act er ist ics of pa ym en ts ar e im po rt an t in d et er m in in g co nsu m er p aym en t be ha vi or , ev en w he n co nt ro lli ng f or d em og ra ph ic an d fin an ci al a tt rib ut es: se tu p an d re co rd ke ep in g ar e esp eci al ly im po rt an t in e xp la in in g ad op tio n, w hi le se cu rit y is im po rt an t in e xp la in in g w hi ch m et ho ds co nsu m er s use f or t ra nsa ct io ns. T he st ud y ex pl or ed co nsu m er p er ce pt io ns of t he sm ar tca rd o n th e de m an d si de a nd ve rif y th e m aj or a tt rib ut es of t he sm ar tca rd f or e -p aym en t in r et ai lin g, sh ow in g th at pe rce iv ed e ase o f use , co nv en ie nce , au to m at ic ad d-va lu e se rv ice , co m pa ct d esi gn , se cu rit y, r el ia bi lit y, a nd m er ch an t su pp or t ar e im po rt an t at tr ib ut es. I n pa rt icu la r, it is im po rt an t to e ff ect iv el y pr ot ect t he in di vi du al p riv acy of a p er so na liz ed sm ar tca rd . It is al so n ece ssa ry to e nco ur ag e m or e po pu la r m er ch an ts an d se rv ice p ro vi de rs to pa rt ici pa te in t he im pl em en ta tio n of t he sm ar tca rd n et w or k. T he st ud y sh ow ed t ha t th e ch ose n pa ym en t m od e im pa ct s co nsu m er sp en di ng b eh av io r an d di ff er en t pa ym en t m od es (ca sh , pe rso na l ch eck, b an k an d re ta il ca rd s) w er e pe rce iv ed d iff er en tly by co nsu m er s. A d iff er en tia l p at te rn o f at tr ib ut es (b ud ge tin g, co nt ro l sp en di ng , do cu m en ta tio n, r ev er si bi lit y, t ra nsa ct io n re co rd , le ve ra ge p ot en tia l, tr an sa ct io n tim e, se cu rit y, so ci al d esi ra bi lit y/ pr est ig e an d tr an sf er t im e) w er e pe rce iv ed to co m po se t he p aym en t m od es an d a co m pa ra tiv e an al ysi s of t he p aym en t m od es at tr ib ut es re ve al ed se ve ra l d im en si on s al on g w hi ch p er fo rm an ce w as pe rce iv ed t o di ff er . M ai n F in d in g s

2.3. Consumer Decision Making and Perceived Value

In this section, we suggest what we believe being a comprehensive and appropriate way of capturing consumers’ perceptions of PMs. The discipline of decision making “captures the dynamic nature of decision processes by prescribing a decision strategy that indicates what action should be chosen” (Keeney, 1982, pg. 808). Many models have been

developed to explain decision making, including the Cognitive–Affective Behavioral

paradigm (Foxall & Goldsmith, 1994), which incorporates the affective aspect and other neuroscience psychology results (Furedy & Riley, 1987). This cognitive-affective model suggests that two processes are likely to occur when an individual is exposed to an alternative. The first produces cognitions about the alternatives given. In this case, the decision making and information processing is date-driven, rational and utilitarian (Furedy & Riley, 1987; Fishbein & Ajzen, 1975). This cognitive process includes a series of psychological processes, such as learning, developing knowledge and comprehension, thinking, making judgments, etc. Factors such as functionality, use of logic, price-quality relationship etc., affect the choice of behavior, and are examples of dominantly cognitive decision making. On the other hand, the second process provokes affective reactions to those choices. In this affective process, the decision making and information processing is feelings-driven, intuitive, and hedonic, being related to the feelings and affective behaviors such as joy, excitement, love, happiness, pride, sympathy, lust, ecstasy, fear, bewilderment, etc. (Holbrook & Hirschman, 1982). Irrational, impulsive and intuitive consumer behaviors are examples of dominantly affective decision making (Foxall & Goldsmith, 1994).

In the context of decision making for PMs, and drawing on the marketing payments literature, we argue that both the cognitive and the affective components have a fundamental

role in consumers’ decisions. For example, one can expect that as a seamless use

experience of a PM increases (i.e., a purchase experience that has no friction, neither

interruption during the payment process, is called in the payment industry as ‘seamless

experience’; it does not generate ‘pain of paying’), the decision-making process tends to be further based on affective factors (enjoyment, confidence and secure). This means that, for example, in digital payments (e.g., mobile payments or digital wallets), which is currently a highly seamless PM, a more affect driven approach is expected to be predominant in the decision-making process.

A more holistic approach to consumer decision making has been offered by the value perspective, which is based on the idea that consumers are “value driven” (Holbrook, 1996;

Woodruff, 1997; Sheth, Newman, & Gross, 1991; Zeithaml, 1988). The concept of perceived value is widely recognized as one of the most important aspects for determining the success of a business, especially due to its direct influence on consumer buying intention and behavior (Chen & Dubinsky, 2003; Parasuraman & Grewal, 2000; Fernandez & Bonillo, 2007; Wang et al., 2004; Zeithaml, 1988). There are two major research streams within the perceived value literature. The first stream conceptualizes perceived value as a single overall concept (unidimensional), and commonly defines it as “the customer's overall assessment of utility of a product based on perceptions of what is received and what is given” (Zeithaml, 1988, p. 14). This approach is grounded in the notion that consumer choice is driven by the maximization of utility, and considers perceived value to be a trade‐off between benefit and sacrifice (Dodds, Monroe, & Grewal, 1991; Zeithaml, 1988). While this unidimensional approach has produced significant implications, some authors have suggested that this approach is too simplistic and narrow to fully capture the complexity of perceived value (Mathwick, Malhotra, & Rigdon, 2001; Sweeney & Soutar, 2001).

As a result, broader multidimensional approaches to perceived value (second stream) began to emerge, including the Consumption Value Theory (CVT) that was developed by Sheth et al. (1991). Unlike the unidimensional approach that only captures the utilitarian aspect of perceived value, the CVT includes both utilitarian and hedonic aspects. Sheth et al. (1991) suggests that consumer choice is a function of five consumption values: functional, emotional, social, epistemic, and conditional. The functional value reflects whether or not a product is able to perform its attribute-related, utilitarian, or physical purposes. Social value refers to social and symbolic benefits offered by a product. Emotional value is related to various affective states, experiential or emotional benefits deriving from a product (e.g. joy or excitement). Epistemic value is concerned with a desire for knowledge, whether motivated by intellectual curiosity or the seeking of novelty. Finally, conditional value reflects the fact that some market choices are contingent on the situation or set of circumstances faced by the consumers.

Later on, Sweeney and Soutar (2001) extended the CVT (Sheth et al., 1991), dividing the functional value into two separate dimensions (quality and price) and removing the epistemic and conditional values. This resulted in the development of a 19-item PERVAL (Perceived Value) scale, which consists of four different dimensions: emotional perceptions, social perceptions, quality/performance perceptions and price/value for money. The introduction of the PERVAL scale enabled empirically testing the consumption value

dimensions, and consequently, encouraged the adoption of CVT in various contexts. The types of perceived value that research on CVT identified can be further categorized into two generic dimensions, namely the cognitive value dimension and the affective value dimension (Roig, Garcia, Tena, & Monzonis, 2006; De Ruyter, Wetzels, Lemmink, & Mattson, 1997).

Since CVT captures both the utilitarian and the hedonic aspects of perceived value, we believe that this multidimensional theory is more appropriate to study PMs perceptions related to decision-making when compared to a more unidimensional approach that focuses mainly on the utilitarian aspect. In addition, previous research suggests that CVT is an effective tool for investigating perceived value within many contexts (Wang et al., 2004; Williams & Soutar, 2009; Deng, Lu, Wei, & Zhang, 2010). For this reason, we extended the CVT (Sheth et al., 1991) and PERVAL scales (Sweeney & Soutar, 2001) for measuring perceived value in the context of PMs.

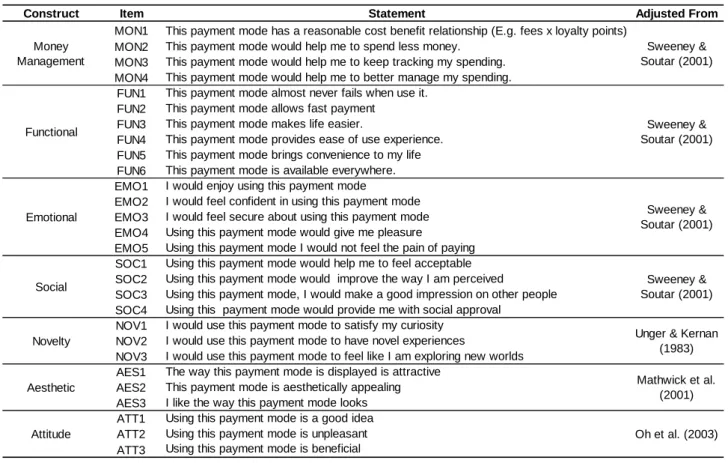

Having in mind our specific context of PMs and the literature explained before, some adjustments were made in some of the dimensions indicated in the PERVAL scale: the functional value (value for money) was renamed as money management value, to capture

the consumer’s mental accounting of spending and saving decisions, more specifically

related to spending control (tracking and managing of spending’s). The functional value (quality/performance) that represent the utility derived from the perceived quality and expected performance of the PM, was adapted to capture the perception that effective task fulfilment of PMs that has been related to convenience (flexibility and portability), availability (well-accepted) and ease of use. Emotional value, besides being associated to the originally emotional values included in PERVAL scale, was modified to also include security (safe,

privacy and anonymity) and ‘pain of pay’; and social, value was adopted with no major

changes to the original scale.

We also included Novelty and Aesthetic values to complement PERVAL scale, as novelty has been study as the innovativeness perception on consumers’ propensity to adopt a product or service (Roger & Shoemaker, 1971; Hirschman, 1980); and aesthetic as the salient visual elements perceived by the customers due to the design, physical attractiveness and beauty of the product (Bellenger, Steinberg & Stanton, 1976; Deighton & Grayson, 1995; Holbrook, 1994). So, both dimensions are expected to be important aspects related to consumers’ value perception of PMs.

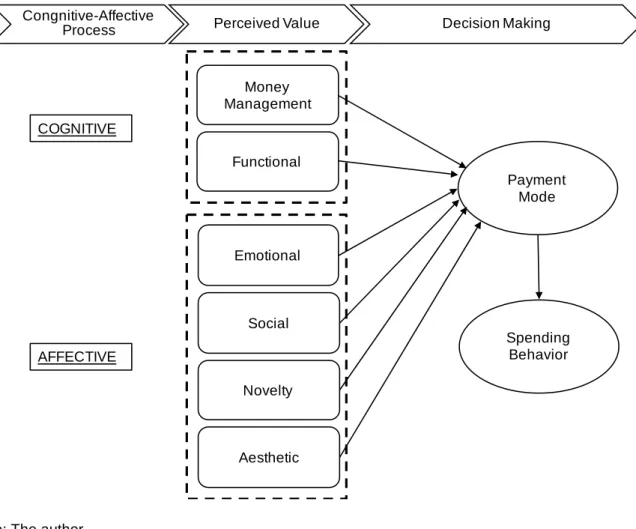

The conceptual model presented below in figure 2 integrates the core idea that the way consumes choose a specific PM and behave in their spending choices is dependent

upon their perceived and multi-attribute cognitive and affective value underlying specific PMs. The mental processes underlying the formation of a perceived value result from a stimulus associated with previous consumer-payment mode interaction experiences (Bettiga & Lamberti, 2017). In this research project, we focus our attention in a specific part of this model: the perceived value. As discussed in the previous section, there is no consensus on how consumers’ perceived value of PMs should be captured.

Figure 2. Decision Making Framework in Payment Mode

Source: The author

3. HYPOTHESES DEVELOPMENTS

Based on the Cognitive-Affective Behavioral Paradigm, money management and functional forms of value are cognitive, as they are results of the mind. More specifically, these two form of value refer to cognitive responses, involving thinking, understanding and interpreting the payments environment. In addition, emotional, social, novelty and aesthetic forms of value can be considered as affective. They refer to feelings-driven responses,

Money Management Functional Emotional Social Novelty Aesthetic COGNITIVE AFFECTIVE Payment Mode Congnitive-Affective

Process Perceived Value Decision Making

Spending Behavior

which are often irrational and impulsive. These forms of value and suggested hypotheses are developed below.

3.1. Cognitive Perceived Value

The ‘mental accounting theory’ has been used in the literature to explain how PMs influence consumers’ money management practices. Thaler (1980) conceptualized mental accounting as a ‘‘set of cognitive operations used by individuals and households to organize, evaluate and keep track of financial activities’’ (p. 40). At the transaction level, people are

said to mentally ‘‘open’’ an account for each transaction, and to base their decisions by

evaluating the perceived benefit deriving from consumption and associated cost. These mental accounts help reducing the cognitive load on the decision makers. Over time, people develop mental filters as shortcuts to make decisions on how to pay. Thaler (1985, 1999) and Gourville and Soman (1998) explain this mental accounting phenomenon as a pseudo-sunk cost effect. This effect is evident when people withdraw cash from an ATM to pay for the bus fare, lunch, parking fees or weekly pocket money. When consumers withdraw money from the ATM, the cash is, from a mental account perspective, mentally spent.

The cognitive perceived money management value is also directly associated with spending control regarding consumer purchasing behavior. Some researchers argue that the difference in consumer purchasing behavior associated with the usage of different PMs results from the opacity of non-cash PMs, showing that consumers tend to spend more when using a credit card than cash (Feinberg, 1986; Hirschman, 1979). Srivastava and Raghubir (2002) demonstrate that when compared with cash, credit card usage might lead people to remember the expense they have made with less accuracy. Cash payments are more transparent than card payments for purchase transactions, making it easier to control spending (Hirschman, 1982); moreover, this effect is not solely due to cash-on-hand constraints (Runnemark, Hedman & Xiao, 2015).

The cognitive perceived functional value is aligned with previous research on perceived payment attributes related to PMs (e.g., Trütsch, 2016; Schuh & Stavins, 2013; Liao, Shi & Wong, 2012; Hirschman, 1982). These previous studies focused on the importance of certain attributes of specific PMs, such as convenience, ease of use, speed, record keeping and security. Cash payments revealed to be primary perceived as higher widespread acceptable, self-budgeting device, and to help consumers in control spending (Hirschman, 1982).

Digital Payments (mobile payments and digital wallets), on the other hand, are perceived being more convenient, as well as easier to use, and more capable of providing better records than the remaining PMs (Mallat, 2007). These functional features can make electronic payments more attractive than cash payments, due to the convenience resulting from technological modifications (Jonker, 2007). Perceived ease of use, usefulness, and trustworthiness have been found to be the most important factors in the context of electronic payments use (Dahlberg et al. 2008).

Based on the presented explanation of the cognitive perceived value for different PMs, we can argue that the perceived money management value tends to be higher for cash payments than for any other PMs, given that cash payments reveled to be primary perceived as widespread acceptable, self-budgeting device, and to help the consumer control spending (Hirschman, 1982). On the other hand, the functional perceived value is prone to be lower for cash payments when compared to other PMs, as digital payments. Hirschman (1982) showed that perceived PMs attributes revealed several dimensions along which performance was perceived to differ, and as performance are related to functional attributes (Sweeney & Soutar, 2001), we can thus consider that the functional values play a greater role than the money management values on the cognitive value perceptions. Therefore, it can be hypothesized that:

Hypothesis 1: The cognitive perceived value is lower for cash than for electronic payment modes.

3.2. Affective Perceived Value

Perceived emotional values of different PMs are associated with security (safe, privacy and anonymity) and pain of pay (Prelec & Loewenstein, 1998; Raghubir & Srivastava, 2008; Thaler, 1999; Tokunaga, 1993). In the context of payment services, the security aspect is directly linked with privacy risk, the consumer’s assessment on ‘‘potential losses to the privacy and confidentiality of personally identification information’’ (Featherman and Wells, 2010), which can lead to potential identity theft. Privacy risk, and in particular identity theft, is one of the main causes that makes consumers hesitate to complete their transactions. Tsai et al. (2011) showed that some online consumers are more willing to purchase items from a website with privacy protection than from one without, even if they need to pay a price premium. Security were showed to be one of the most strongly perceived

attributes of PMs (Schuh & Stavins, 2013; Liao, Shi & Wong, 2012) and indicated to be higher in electronic PMs.

Yet, as we have discussed earlier, the affective factor of ‘pain of paying’ is associated with transparency, vividness and salience of PMs (Raghubir and Srivastava, 2008; Soman, 2003) and these are stronger in cash payments. This generates a stronger emotional link to the amount of money being spent during a transaction, while electronic payments are the opposite. The psychologically decoupled effect generated by electronic payments from

purchase, may also result in a reduced the emotional ‘pain of paying’ (Prelec and

Loewenstein, 1998; Raghubir and Srivastava, 2008; Thaler, 1999; Tokunaga, 1993). Also, the mental representation of the process of paying for cash and digital influence the extent of ‘pain of paying’: by cash, the representation often involves a more complicated process of paying (Hancock & Humphrey, 1997), than the one involved in the seamless and easier process of electronic based PMs. For these reasons, paying with cash is often more painful than paying with electronic payments (Prelec and Loewenstein, 1998; Raghubir & Srivastava, 2008). This justifies why the affective feeling of ‘pain of paying’ is less felt for electronic PMs.

The affective social values are related with social status, sophistication, sensation and pleasure to measure social gratification. Nowadays, people do not display stacks of cash in public, due to safety and security concerns (Khan et al., 2015). However, paying by premium credit and debit cards (e.g., gold or platinum or black) or using mobile phones and

other devices, resemble the age-old symbols of status, and serve to communicate one’s

purchasing power and sophistication (Khan et al., 2015). Neuroscience provides evidence that money and social status are processed in the same brain region (the striatum), and that people tend to define social standing by weighing their spending and wealth (Zink et al., 2008). Because differently from the credit card, the debit card can signal having money in the bank, debit card usage might be associated with higher social status than the remaining PMs.

The affective novelty value is associated with a desire for knowledge, whether motivated by intellectual curiosity or the seeking of novelty (Sheth et al., 1991). Previous payment based research has investigated its influence on the intention of using different technologies, such as the use of mobile phone cameras for e-shopping (Rouibah, 2011) and electronic payment system (Yang et al., 2012; Dahlberg et al., 2008). In addition, previous research has investigated the novelty value effect on different variables, such as ease of