1 Ext ract ed fr om Resear ch Pr oj ect ; 2 Nur se, PhD in Nur sing, Facult y; 3 Nur se, Doct oral st udent , Facult y, e- m ail: m ar li.j er ico@fam er p.br ; 4 Nur se, Facult y. Medical School of São José do Rio Pr et o, Br azil

D isponible e n ca st e lla no/ D isponíve l e m língua por t ugue sa SciELO Br a sil w w w .scie lo.br / r la e

SURGERY CANCELLI NG AT A TEACHI NG HOSPI TAL: I MPLI CATI ONS FOR COST MANAGEMENT

1Már cia Galan Per r oca2 Mar li de Car v alho Jer icó3 Solange Diná Facundin4

Per r oca MG, Jer icó MC, Facundin SD. Sur ger y cancelling at a t eaching hospit al: im plicat ions for cost m anagem ent . Rev Lat in o- am En fer m agem 2 0 0 7 set em br o- ou t u br o; 1 5 ( 5 ) : 1 0 1 8 - 2 4 .

This study discusses the problem of surgery cancellation on the econom ic-financial perspective. I t was carried out in the Surgical Center Unit of a school hospital with the objective to identify and analyze the direct costs (hum an resources, m edications and m aterials) and the opportunity costs that result from the cancellation of elective surgeries. Dat a were collect ed during t hree consecut ive m ont hs t hrough inst it ut ional docum ent s and a form elaborat ed by t he researchers. Only 58 ( 23.3% ) of t he 249 cancelled scheduled surgeries represent ed cost s for t he inst it ut ion. The cancellations direct total cost was R$ 1.713.66 (average cost per patient R$ 29.54); distributed as follows: expenses with consum ption m aterials R$ 333.05; sterilization process R$201.22; m edications R$149.77 and hum an resources R$1,029.62. The hum an resources costs represented the greatest percentile in relation to the total cost (60.40% ). I t was observed t hat m ost of t he cancellat ions could be part ially avoided. Planning on m anagem ent ; redesigning work processes, training the staff and m aking early clinical evaluation can be strategies to m inim ize this occurrence.

DESCRI PTORS: hospit als t eaching/ organizat ion and adm inist rat ion; nursing; hospit al cost s; direct service cost s

CANCELAMI ENTO DE CI RUGÍ AS EN UN HOSPI TAL- ESCUELA: I MPLI CACI ONES PARA LA

GESTI ÓN DE COSTOS

Este artículo discute la problem ática del cancelam iento de cirugías bajo una perspectiva económ ico-financiera. Fue llevado a cabo en la Unidad del Centro Quirúrgico de un hospital- escuela con obj eto de identificar y analizar los costos directos (recursos hum anos, recursos m ateriales y m edicam entos) e indirectos ocasionados por el cancelam iento de cirugías no urgentes. Los datos fueron recogidos durante tres m eses consecutivos m ediante docum entos institucionales y un cuest ionario elaborado por las invest igadoras. Solam ent e 58 ( 23,3% ) de las 249 operaciones previst as y que fueron canceladas resultaron en costos para la institución. El costo directo total de los cancelam ientos fue R$ 1.713,66 ( costo m edio por paciente de R$ 29,54) , repartidos así: gastos con m ateriales de consum o R$ 333,05 y proceso de esterilización R$ 201,22, m edicam entos R$ 149,77 y recursos hum anos R$ 1.029,62. El costo de los recursos hum anos repesentó el m ayor porcentaje en relación al costo total (60,1 % ). Se constató que la m ayor parte de los cancelam ientos podría haber sido evit ada. Planificación adm inist rat iva, rediseño de los procesos de t rabaj o, m edidas educat ivas del personal y evaluaçión clínica previa constituyen estrategias recom endadas para reducción de los casos de cancelam iento.

DESCRIPTORES: hospitales escuela/ organización y administración; enfermería; costos hospitalares; costos directos de servicios

CAN CELAMEN TO CI RÚRGI CO EM UM HOSPI TAL ESCOLA: I MPLI CAÇÕES SOBRE O

GERENCI AMENTO DE CUSTOS

Este estudo discute a problem ática do cancelam ento de cirurgias sob a perspectiva econôm ico-financeira. Foi realizado na Unidade de Centro Cirúrgico de um hospital de ensino, com o objetivo de identificar e analisar os custos diretos (recursos hum anos, m edicam entos e m ateriais) e custo de oportunidade gerados pelo cancelam ento de cirurgias eletivas. Os dados foram coletados durantes três m eses consecutivos, utilizando-se docum entos institucionais e form ulário elaborado pelas pesquisadoras. Apenas 58 ( 23,3% ) das 249 cirurgias program adas canceladas representaram custos para a instituição. O custo direto total dos cancelam entos foi de R$ 1.713,66 (custo m édio por paciente de R$ 29,54), assim distribuídos: despesas com m ateriais de consum o R$ 333,05; processo de esterilização R$ 201,22; m edicam entos R$ 149,77 e recursos hum anos R$ 1.029,62. O cust o com recursos hum anos represent ou o m aior percent ual em relação ao cust o t ot al ( 60,1% ) . Observou- se que a m aior part e dos cancelam ent os eram pot encialm ent e evit áveis. Planej am ento adm inistrativo, redesenho dos processos de trabalho, m edidas educativas de pessoal e avaliação clínica prévia const it ue em est rat égias recom endadas para m inim ização da ocorrência.

DESCRI TORES: hospit ais de ensino/ organização e adm inist ração; enferm agem ; cust os hospit alares; cust os diret os

I NTRODUCTI ON

T

h e c a n c e l l i n g o f s c h e d u l e d s u r g i c a l p r oced u r es h as b een st u d ied n ot on ly in Br azil( 1 - 2 ),but also in ot her count r ies like Aust r alia( 3), I r eland( 4),

M e x i c o( 5 ), t h e U n i t e d S t a t e s( 6 ) a n d t h e U n i t e d

Kin g d om( 7 ) . Lik e Br azilian r esear ch , t h ese st u d ies

h av e in dicat ed h igh f r equ en cy of can cellin g, du e t o

organizat ional problem s in healt h inst it ut ions, including

lack of beds( 3 - 4 , 7 ), sch edu lin g er r or s, com m u n icat ion

er r or s( 3 , 5 ) and ot her adm inist r at iv e pr oblem s.

Alt h ou g h sev er al au t h or s ack n ow led g e t h at

t he im pact of surgery cancelling raises t he operat ional

an d f in an cial cost s of t h e Su r g ical Cen t er Un it an d

reduces t he efficiency of t he service, few st udies have

a n a l y ze d t h e t h e m e f r o m t h e e co n o m i c- f i n a n ci a l

asp ect , esp ecially in t er m s of d ir ect cost s ( h u m an

r e so u r ce s, m e d i ca t i o n a n d m a t e r i a l ) a n d co st o f

o p p o r t u n i t y. As t h e su r g i ca l m o v e m e n t h a s b e e n

appoint ed as an int er venient fact or in pr oduct ivit y and

hospit al qualit y rat es( 8), t he m axim um use of sur gical

capacit y is one of t he m ain m easures for t he efficiency

of f i n an ci al r esou r ce u se. A st u d y p er f or m ed at a

t eaching hospit al( 9) dem onst r at ed t hat sur gical pat ient s

represent 24% of t ot al hospit alizat ions and cont r ibut e

t o 43% of r ev enues.

Sur ger y cancelling is an er r or r esult ing fr om

non com pliance wit h t he unit ’s adm inist rat ive planning

r e q u i r e m e n t s. I t co r r e sp o n d s t o o n e o f t h e f o u r

com ponent s of qualit y cost , classified in cost s of int ernal

and ext ernal errors, cost s of prevent ion and analysis.

To ach iev e excellen ce, t h e h ospit al m u st con t in u ally

be com m it t ed t o t he problem solving capacit y, qualit y

and low cost s of m edical pr ocedur es. Ther efor e, t he

elim inat ion of wast e is needed, as well as t he abilit y t o

im pr ov e t h e h ospit al pr ocess ( diagn osis, t r eat m en t ,

h o s p i t a l i z a t i o n , m a n a g e m e n t s u p p o r t ) t h r o u g h

adequat e aut om at ion, m ore inform at ion and decrease

of t he pat ient ’s hospit al st ay( 10).

Wa st e ca n b e co n si d e r e d a s a n y a n d a l l

r esour ces used, bey ond t he necessar y, t o execut e a

pr odu ct or ser v ice ( con su m pt ion m at er ial, su pplies,

hum an effor t , ener gy, t echnology, am ong ot her s) . I t

is ext r a expendit ur e added t o t he pr oduct or ser vice’s

r egular cost s w it hout any kind of im pr ovem ent t o t he

clien t( 1 1 ). Wh en w or k pr ocesses ar e in adequ at e, t h e

cost of pr oduct s or ser v ices incr eases. Consequent ly,

t he inst it ut ions incur financial losses due t o r ew or k ,

absor bin g t h e t im e t h at w ou ld be u sed f or an ot h er

act iv it y.

Th e r e p e r c u s s i o n s o f s u r g e r y c a n c e l l i n g

negat ively affect not only t he client , w ho experiences

a br ok en bond of t r ust in r elat ion t o t he inst it ut ion,

but also t he nur sing t eam ( w or k oper at ion, t im e and

m a t e r i a l r e so u r ce co n su m p t i o n , d i m i n i sh e d ca r e

qualit y) and t he hospit al it self( 1). The cancelling of t he

sur gical pr ocedur e incr eases oper at ional and financial

cost s, causing losses t o t he inst it ut ion. The financial

loss is cau sed b y t h e d ef icien t p r ocess an d can b e

ev id en ced b y t h e r eser v at ion of t h e su r g er y r oom

and loss of oppor t unit y t o schedule anot her pat ient ,

under used sur ger y r oom s, longer hospit alizat ions ( and

r isk of hospit al infect ion) and, consequent ly, incr ease

in t he bed pr ice/ day and dim inished bed av ailabilit y.

Ot h e r so u r ce s o f l o ss a r e t h e w a st e o f st e r i l i ze d

m at er i al , r ew o r k o f t h e p er so n n el i n v o l v ed i n t h e

pr epar at ion of t he sur gery r oom and in t he st er ilizat ion

p r ocess( 2 ).

The cost of oppor t unit y can be defined as t he

v alue of a r esour ce in it s best alt er nat iv e use( 12). I t

r ep r esen t s t h e v alu e t h at is n ot g ain ed d u e t o t h e

d e c i s i o n o f i n v e s t i n g t h e r e s o u r c e i n a n o t h e r

a l t e r n a t i v e , t o t h e d e t r i m e n t o f o t h e r s. D i f f e r e n t

p a r a m e t e r s h a v e b e e n u s e d t o a d d r e s s c o s t o f

o p p o r t u n i t y, su ch a s t h e m e a su r e m e n t o f p r o f i t ,

incom e, am ong ot her s. Since each decision inv olv es

a d if f er en t cost of op p or t u n it y, t h e con cep t can b e

a s s o c i a t e d w i t h d i f f e r e n t a t t r i b u t e s( 1 3 ). Th e

im plem ent at ion of t he concept guides t he m anager ’s

decision in t he use of a cer t ain r esour ce dur ing t he

w h ole decision pr ocess, i. e. in t h e ph ase pr ecedin g

t h e d e c i s i o n , a s a n e l e m e n t f o r e v a l u a t i n g t h e

per for m ance of t he m anager r esponsible for t he act ion

and also t o evaluat e t he result s of t he decision, aft er

i t s i m p l e m e n t a t i o n( 1 4 ). Th e f o c u s o n e c o n o m i c

m easu r em en t b y cost of op p or t u n it y is a r elev an t

in st r u m en t of f eedback f or plan n in g an d con t r ol( 1 5 ).

Thus, t his st udy aim s t o suppor t nur sing in t he decision

m aking pr ocess based on qualit y and oppor t unit y cost

in f or m at ion .

OBJECTI VES

- I dent ify and analy ze t he dist r ibut ion of dir ect cost s

r e l a t e d t o h u m a n r e so u r ce s, co n su m e d su p p l i e s

( c o n s u m p t i o n a n d r e p r o c e s s e d m a t e r i a l s ) a n d

m edicat ions, gener at ed by t he cancelling of elect iv e

su r g er ies at t h e Su r g ical Cen t er Un it of a t each in g

- Ver ify t he dir ect cost r elat ed t o t he t im e spent by

dif f er en t pr of ession al cat egor ies.

- I dent ify t he cost of oppor t unit y at t he sur gical cent er.

METHODOLOGY

This is an ex plor at or y and descr ipt ive st udy,

ca r r i e d o u t a t t h e Su r g i ca l Ce n t e r o f a Te a ch i n g

Hospit al of ex t r a capacit y in a cit y in t he int er ior of

São Pau lo, Br azil. Th is h osp it al is a r ef er r al cen t er

an d deliv er s h ospit al an d ou t pat ien t car e in sev er al

m ed i ca l sp eci a l t i es, t o t a l i n g a n a v er a g e o f 2 , 5 0 0

h osp it alizat ion s/ m o. an d 1 , 6 0 0 lar g e, m ed iu m an d

sm all- size sur ger ies/ m o. The sur gical pr ogr am cov er s

t he per iod fr om 7am t o 7pm , daily, fr om Monday t o

Fr i d a y a n d o n Sa t u r d a y m o r n i n g s. Ni g h t p er i o d s,

w eekends and holidays ar e r eser ved for em er gencies.

Th e st u d y p o p u l a t i o n i s co m p o se d o f a l l e l e ct i v e

sur ger ies in t he per iod fr om Sept em ber t o Novem ber

2 0 0 4 a t t h e s t u d y h o s p i t a l , c a n c e l l e d a f t e r t h e

pr epar at ion of t he sur ger y r oom ( SR) and dur ing t he

sur ger y it self. This cr it er ion w as used because t hese

t y p es of can cellin g im p ly cost s ( con sid er ed in t h is

st u d y ) .

The m ap w it h t he m ont hly sur gical schedule

w a s u s e d t o v e r i f y t h e o c c u r r e n c e o f s u r g e r y

cancelling. For t he ident ificat ion of causes, a st ruct ured

for m w as elabor at ed, cont aining 4 gr oups of dat a: 1

-D em o g r a p h i c Ch a r a ct er i st i cs ( a g e, g en d er, h ea l t h

in su r an ce, su r g er y r oom an d t im e of su r g er y ) ; 2

-Cir cu m st an ce in w h ich t h e su r ger ies w er e can celled

( befor e and aft er t he pr epar at ion of t he sur ger y r oom

and dur ing t he sur gical pr ocedur e) ; 3 - Pr ofessional

Cat eg or ies in v olv ed in t h e ar r an g em en t of t h e SR,

t im e spent and act ivit ies developed; 4 - Mat er ial and

equipm ent used in t he ar r angem ent of t he SR w hich

w ere not included in t he debt bill of t he Surgical Cent er

Un it ( SCU) , su ch as clot h i n g ( sh eet s, g ow n s) an d

in st r u m en t s.

D a t a c o l l e c t i o n s t a r t e d a f t e r f o r m a l

au t h or izat ion w as obt ain ed f r om t h e in st it u t ion an d

fr om t he head nur se at t he SCU, and aft er or ient at ion

o f t h e n u r s e s w h o w o r k e d i n t h e m o r n i n g a n d

aft er noon shift s about how t o fill out t he inst r um ent

t o b e u s e d . A p p r o v a l b y t h e Re s e a r c h Et h i c s

Com m it t ee w as not necessar y because t his r esear ch

d i d n o t i n v o l v e h u m a n b e i n g s . Th e r e s e a r c h e r s

c o l l e c t e d t h e f o r m s e v e r y d a y a n d d a t a w e r e

com p lem en t ed .

An elect r on ic w or k sh eet w as elab or at ed in

Micr osof t Ex cel f or d at a t r eat m en t . Th is con t ain ed

infor m at ion on t he client ’s ident ificat ion, healt h plan,

h o sp i t a l i za t i o n u n i t , su r g er y, d a t e a n d r ea so n f o r

ca n ce l l i n g . Th e sh e e t w a s d i v i d e d i n f o u r p a r t s:

m at er ials, fees, m edicat ion and hum an r esour ces. The

cost id en t if icat ion w as b ased on t h e BRASI NDI CE,

fact or y pr ice fr om Apr il 2005 and AMB t able ( Br azilian

Med ical Associat ion ) . Dat a r eg ar d in g salar ies w er e

p r o v i d ed b y t h e Per so n n el Dep ar t m en t . To su r v ey

cost s r elat ed t o t he t im e spent on hum an r esour ces,

t h e m i n i m u m r e m u n e r a t i o n o f t h e p r o f e s s i o n a l

cat eg or ies in v olv ed an d social ch ar g es ( FGTS, PI S,

v acat ion an d 1 3t h salar y at t h e pr opor t ion of 1 / 1 2 )

w er e t ak en in t o accou n t . Th e t ax es t ot aled 2 1 . 6 7 %

of added cost . To est im at e t h e cost of oppor t u n it y,

t he sur ger ies w er e classified accor ding t o anest het ic

size and t he SR and Post Anest hesia Car e Unit ( PACU)

fees fr om t he AMB t able w er e used.

RESULTS

I n t o t a l , 2 4 9 s c h e d u l e d s u r g e r i e s w e r e

cancelled at t he Surgical Cent er unit during t he st udy

per iod. Fr om t hese, 191 ( 76.7% ) occur r ed befor e t he

p r ep ar at ion an d ar r an g em en t of t h e su r g er y r oom ,

54 ( 21.7% ) aft er it s pr epar at ion and only four of t hem

( 1 . 6 % ) d u r i n g t h e a n e st h e t i c- su r g i ca l p r o ce d u r e .

Ca n c e l l a t i o n s b e f o r e t h e S R p r e p a r a t i o n w e r e

e x c l u d e d f r o m t h e a n a l y s i s s i n c e t h e y d i d n o t

r ep r esen t a d d i t i o n a l co st s. Th u s, t h e sa m p l e w a s

com posed of t he 58 ( 23. 3% ) r em aining sur ger ies.

Am ong t he pat ient s w ho had t heir sur ger ies

cancelled, 30 were m en and 28 wom en, wit h an average

age of 43.1 ± 24.2 years ( ranging from 6 m ont hs t o 80

years old) . Most pat ient s ( 82.7% ) used t he Single Healt h

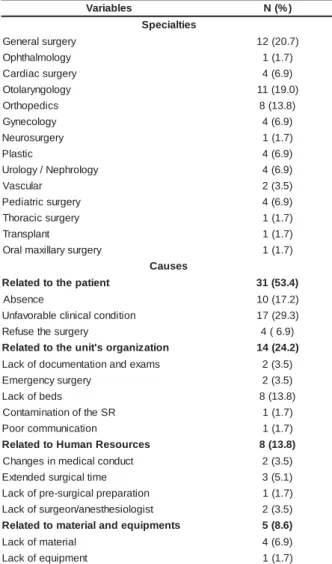

Syst em ( SUS) . As can be observed in Table 1, t he m ost

fr equent m edical specialt ies in t he cancelled sur gical

procedures wit h cost s for t he inst it ut ion were: general

surgery ( 20.7% ) , followed by ot olaryngological surgery

( 1 9 % ) an d or t h op ed ic su r g er y ( 1 3 . 8 % ) . Th e m ain

causes for cancelling were relat ed t o t he pat ient ( 53.4% ) ,

su ch a s u n f a v o r a b l e cl i n i ca l co n d i t i o n ( a r t e r i a l

hypert ension and respirat ory diseases, am ong ot hers)

- 29.3% and absence ( 17.2% ) . Problem s relat ed t o t he

unit ’s or ganizat ion ( 24. 2% ) also caused a significant

share of cancelling, m ainly because of t he lack of beds

a t t h e I n t e n si v e Ca r e Un i t ( 1 3 . 8 % ) . La ck o f

cont am inat ion of t he SR were responsible for a sm aller

par t of can cellat ion s, r espect iv ely, 3 . 5 % , 3 . 5 % an d

1.7% . I n only 8 of t he 58 surgeries t hat were cancelled

( 13.8% ) , t he m ain causes of cancelling were relat ed t o

t he allocat ion of hum an resources, such as, ext ended

surgical t im e ( 5.1% ) , changes in m edical conduct ( 3.5% )

and lack of surgical t eam professionals ( anest hesiologist

a n d su r g e o n ) - 3 . 5 % . Th e ca u se s r e l a t e d t o t h e

a l l o ca t i o n o f h u m a n r e so u r ce s a n d e q u i p m e n t

represent ed only 8.6% of t he t ot al causes of cancelling.

Table 1 - Medical Specialt ies and causes for cancelling

t he surgeries t hat ent ailed cost s for t he st udy inst it ut ion

( N= 58) . São José do Rio Pr et o, SP, 2004

Table 2 - Direct cost s of surgeries cancelled at t he st udy

inst it ut ion ( N= 58) . São José do Rio Pret o, SP, 2004

s e l b a i r a

V N(%)

s e i t l a i c e p S y r e g r u s l a r e n e

G 12(20.7)

y g o l o m l a h t h p

O 1(1.7)

y r e g r u s c a i d r a

C 4(6.9)

y g o l o g n y r a l o t

O 11(19.0)

s c i d e p o h t r

O 8(13.8)

y g o l o c e n y

G 4(6.9)

y r e g r u s o r u e

N 1(1.7)

c i t s a l

P 4(6.9)

y g o l o r h p e N / y g o l o r

U 4(6.9)

r a l u c s a

V 2(3.5)

y r e g r u s c i r t a i d e

P 4(6.9)

y r e g r u s c i c a r o h

T 1(1.7)

t n a l p s n a r

T 1(1.7)

y r e g r u s y r a ll i x a m l a r

O 1(1.7)

s e s u a C t n e i t a p e h t o t d e t a l e

R 31(53.4)

e c n e s b

A 10(17.2)

n o i t i d n o c l a c i n il c e l b a r o v a f n

U 17(29.3)

y r e g r u s e h t e s u f e

R 4(6.9)

n o i t a z i n a g r o s ' t i n u e h t o t d e t a l e

R 14(24.2)

s m a x e d n a n o i t a t n e m u c o d f o k c a

L 2(3.5)

y r e g r u s y c n e g r e m

E 2(3.5)

s d e b f o k c a

L 8(13.8)

R S e h t f o n o i t a n i m a t n o

C 1(1.7)

n o i t a c i n u m m o c r o o

P 1(1.7)

s e c r u o s e R n a m u H o t d e t a l e

R 8(13.8)

t c u d n o c l a c i d e m n i s e g n a h

C 2(3.5)

e m i t l a c i g r u s d e d n e t x

E 3(5.1)

n o i t a r a p e r p l a c i g r u s -e r p f o k c a

L 1(1.7)

t s i g o l o i s e h t s e n a / n o e g r u s f o k c a

L 2(3.5)

s t n e m p i u q e d n a l a i r e t a m o t d e t a l e

R 5(8.6)

l a i r e t a m f o k c a

L 4(6.9)

t n e m p i u q e f o k c a

L 1(1.7)

The dir ect cost s r elat ed t o hum an r esour ces

a n d s u p p l i e s ( m e d i c a t i o n , c o n s u m p t i o n a n d

r epr ocessed m at er ial) t ot aled R$ 1 , 7 1 3 . 6 6 ( av er age

cost per pat ient R$ 29.54) , w hile R$ 1,169.08 ( 68.2% )

w er e r elat ed t o can cellat ion s du r in g t h e pr epar at ion

of t he sur ger y r oom and R$ 544. 58 ( 31. 8% ) dur ing

t he sur gical pr ocedur e ( Table 2) .

l a c i g r u S e c n a t s m u c r i

c N HR Material Medication SPD Total(%)

g n i r u D n o it a r a p e r

p 54 R$922.22 R$55.89 R$31.30 R$159.67

8 0 . 9 6 1 . 1 $ R ) 2 . 8 6 ( g n i r u D e r u d e c o r

p 4 R$107.40 R$277.16 R$118.47 R$41.55

8 5 . 4 4 5 $ R ) 8 . 1 3 ( ) % ( l a t o

T 58R$1,029.62 ) % 1 . 0 6 ( 5 0 . 3 3 3 $ R ) % 4 . 9 1 ( 7 7 . 9 4 1 $ R ) % 7 . 8 2 2 . 1 0 2 $ R ) % 8 . 1 1

( R$1,713.66

HR: Hum an r esour ces; SPD: St er ile Pr ocessing Depar t m ent

Nu r sin g ( n u r sin g t ech n ician s an d aids) w as

t h e ca t e g o r y t h a t t o t a l e d t h e h i g h e st n u m b e r o f

m in u t es w or k ed ( 2 , 2 5 5 ) cor r espon din g t o 4 6 . 7 % of

t he w or k load dur ing t he pr epar at ion of t he SR and

54. 9% dur ing t he anest het ic- sur gical pr ocedur e. The

t i m e o f t h i s ca t e g o r y w a s d i st r i b u t e d a m o n g t h e

f u n c t i o n s o f t h e s c o u t n u r s e , h e l p t o t h e

anest hesiologist and sur gical inst r um ent at ion. At t he

st u d y i n st i t u t i o n , t h e n u r si n g p r o f e ssi o n a l h a s a

m a n a g e m e n t f u n c t i o n a n d i s r e s p o n s i b l e f o r

su p e r v i si n g t h e su r g e r y r o o m s. Be ca u se i t i s a n

i n d i r e c t c o s t , t h i s p r o f e s s i o n a l ’ s t i m e w a s n o t

consider ed. The findings show ed t hat t he scout nur se

spends m or e t im e w or king bot h in t he pr epar at ion of

t h e SR ( 3 0 . 5 % ) an d d u r in g t h e su r g ical p r oced u r e

( 24.1% ) . The highest cost for t he inst it ut ion is r elat ed

t o t he sur geon ( R$ 446.40) and t he anest hesiologist

( R$ 286.75) ( Table 3) .

Table 3 - Professional Cat egories/ funct ions t hat worked

in t he cancelled surgeries which incurred cost s for t he

st udy inst it ut ion. São José do Rio Pret o, SP, 2004

s a i r o g e t a C / s i a n o i s s i f o r p s e õ ç n u f O S a d o r a p e r

P ProDceudraimnteento H C ) n i m ( % o t s u C ) $ R ( H C ) n i m ( % o t s u C ) $ R ( m e g a m r e f n

E 2.255 46,7 209,72 365 54,9 33,95 e t n a l u c r i

C 1.475 30,5 137,18 160 24,1 14,88 r o d a t n e m u r t s n

I 250 5,2 23,25 100 15 9,30 a i s e t s e n a à o i l í x u

A 530 11 49,29 105 15,8 9,77 a t s i g o l o i s e t s e n

A 825 17,1 255,75 100 15 31,00

o ã i g r u r i

C 1.325 27,4 410,75 115 17,3 35,65 e t n e t s i s s a o ã i g r u r i

C 425 8,80 34,00 85 12,8 6,80

l a t o

T 4.830 100 920,12 665 100 107,4

HL - Hour Load

Due t o t he high num ber of it em s am ong t he

d i f f er en t m a t er i a l s, i n t h i s st u d y, t h e t h r ee m o st

r epr esent at iv e it em s of each m at er ial w er e select ed.

Th e m ost u sed con su m p t ion m at er ials t h at cau sed

h i g h e r s p e n d i n g f o r t h e i n s t i t u t i o n d u r i n g S R

p r e p a r a t i o n w e r e m e d u l l a r y p u n c t u r e n e e d l e s ,

elect rode; during t he sur gical procedur e, t he m at er ials

w e r e m e d u l l a r y p u n c t u r e n e e d l e s , s u r g i c a l

c o m p r e s s e s a n d m a l l e a b l e p e r i p h e r a l v e n o u s

p u n ct u r e ca t h e t e r s. I n t e r m s o f m e d i ca t i o n , t h e

m a t e r i a l s w e r e : a n e st h e t i c e y e d r o p s, l i d o ca i n e ,

i so b a r i c b u p i v a ca i n e a n d o x y g en ( SR p r ep a r a t i o n

p h ase) an d p r op of ol, lid ocain e an d su x am et h on iu m

( dur ing t he sur gical pr ocedur e) .

Th e m a t e r i a l r e p r o c e s s e d b y t h e St e r i l e

Pr ocessin g Depar t m en t ( SPD) u sed in t h e can celled

su r ger ies w as classif ied in in st r u m en t s an d su r ger y

clot h in g. Th e t ot al cost of in st r u m en t al r epr ocessin g

w as R$ 5 9 . 3 2 ( t h e m ost ex p en siv e it em s w er e t h e

s m a l l s u r g e r y b o x , s e p t o p l a s t y b o x a n d

g l o sse ct o m y ) . Su r g e r y cl o t h i n g r e p r o ce ssi n g co st

a m o u n t e d t o R$ 1 4 1 . 9 0 f o r t h e i n s t i t u t i o n ; t h e

g en er a l l a p a r o t o m y p a ck a g e i n cu r r ed i n a h i g h er

cost . To su r v ey SR an d PACU cost s, t h e can celled

su r g e r i e s w e r e cl a ssi f i e d a cco r d i n g t o a n e st h e t i c

size, w h ich v ar ies f r om 0 t o 7 . Th e m ost f r eq u en t

su r g er i es w er e o f si ze 2 . Ho w ev er, su r g er i es t h at

in cu r r ed a h ig h er cost of op p or t u n it y w er e of size

5 , r esp o n si b l e f o r 2 2 . 1 % ( R$ 2 , 3 8 8 . 0 8 ) , f o l l o w ed

by size 2 w it h 1 9 % ( R$ 2 , 0 5 0 . 8 0 ) an d sm aller size

( s i z e 0 ) w i t h 0 . 7 % ( R$ 7 8 . 9 6 ) . T h e c o s t o f

op p or t u n it y at t h e Su r g ical Cen t er Un it t ot aled R$

1 0 , 7 8 2 . 4 0 .

DI SCUSSI ON

Fift y- eight of all surgeries t hat w ere cancelled

ent ailed cost s. The m ain causes w er e r elat ed t o t he

pat ient ( 53.4% ) , such as unfavorable clinical condit ion

( hyper t ension and r espir at or y diseases am ong ot her s)

- 29.3% and absence ( 17.2% ) . St udies per for m ed in

Mex ico( 5 ) an d Au st r alia( 3 ) also sh ow ed alt er at ion s in

pat ient s’ clinical condit ions as sour ces of cost s, w it h

4 0 % a n d 1 7 . 1 % r esp ect i v el y. Pr e- su r g er y cl i n i ca l

assessm ent is appoint ed as an im por t ant fact or t o be

considered for reducing t he rat es of cancelled surgical

pr ocedu r es( 6 , 1 6 ).

Reg ar d i n g t h e p at i en t ’ s ab sen ce f r o m t h e

scheduled surgery, research in t eaching hospit als have

in d icat ed v alu es of 4 1 % ( cat ar act su r g er y )( 1 7 ) an d

54. 3% ( sev er al specialt ies)( 1), higher t han w hat w as

f o u n d i n t h i s st u d y ( 1 7 . 2 % ) . Th e r easo n s f o r t h e

p a t i e n t ’ s a b s e n c e h a v e b e e n a s s o c i a t e d t o t h e

inst it ut ional condit ion ( unaw ar eness and alt er at ion of

t he dat e of sur ger y, hospit alizat ion difficult y, lack of

vacancy and lack of pr e- sur gical exam ) ; t o t he clinical

con d it ion , social con d it ion ( occu p at ion al p r ob lem s)

and also per sonal condit ion( 1).

Su r g e r y ca n ce l l i n g d u e t o o r g a n i za t i o n a l

pr oblem s at t he unit ( 24.2% ) is m ainly r elat ed t o t he

lack of beds at t he I nt ensiv e Car e Unit and also for

h o sp i t a l i za t i o n ( 1 3 . 8 % ) . I n a st u d y p er f o r m ed i n

I reland( 4), t he lack of beds r epr esent ed 31% of sur ger y

ca n ce l l a t i o n s, a g a i n st 1 8 . 1 % i n Au st r a l i a( 3 ). Th e

f in din gs of t h is r esear ch r ev ealed t h at can cellat ion s

d u e t o h u m a n r e so u r ce f a ct o r s r e p r e se n t e d o n l y

1 3 . 8 % of t he t ot al, in w hich ex t ended sur ger y t im e

pr edom inat ed ( 5 . 1 % ) . Values of 1 8 . 7 % for pr ev ious

su r g er ies t h at ex ceed ed est im at ed t im e h av e b een

r ep or t ed in lit er at u r e( 3 ), as w ell as t h e ob ser v at ion

t hat sur geons w ho fr equent ly under est im at e t he t im e

n e ce ssa r y f o r t h e su r g e r y h a v e a l so p r e se n t e d a

significant ly higher num ber of cancellat ions t han t hose

w ho do not .

Measu r es t o m in im ize can cellat ion s ar e an

im por t ant at t r ibut ion for t he head nur se at t he sur gical

cen t er. I t is est im at ed t h at ar ou n d 6 0 % of elect iv e

pr ocedu r e can cellat ion s is pot en t ially av oidable an d

cou l d b e p r ev en t ed b y u si n g q u al i t y i m p r ov em en t

t e ch n i q u e s. Th e ca n ce l l a t i o n s sh o u l d b e se e n a s

ad v er se ev en t s an d b e r ou t in ely m on it or ed in t h e

clinical sy st em s of hospit al incident s, since t hey ar e

t he m ain cause of inefficient t im e use at t he SR and

w ast e o f r eso u r ces( 3 ). Th ese au t h o r s co n si d er t h e

follow ing t ypes of cancellat ion as pot ent ially avoidable:

pr evious sur ger ies t hat exceeded t he est im at ed t im e,

sch edu lin g er r or s, adm in ist r at iv e cau ses, equ ipm en t

an d t r an sp or t at ion p r ob lem s, p oor com m u n icat ion ,

e r r o r s i n a d e q u a t e p a t i e n t p r e p a r a t i o n a n d n o n

-av ailab le su r g eon .

The Unit ed Kingdom ’s ex per ience( 7) in using

au d it in g as an in t er v en t ion p r ocess h as p r esen t ed

p r om i si n g r esu l t s. Th e f i r st au d i t f ou n d a su r g er y

cancellat ion r at e of 16.1% , w hile t he r easons r elat ed

t o t he hospit al ( m ainly lack of beds) r epr esent ed 42%

of t ot al cancellat ions, clinical reasons 34% ( especially

lack of anest het ic and sur gical condit ions) and pat ient

-r elat ed cancellat ions 21% ( absence) . The second audit

w as per for m ed 1 5 m on t h s aft er t h e m easu r es w er e

im plem ent ed ( im provem ent in bed dist ribut ion, clinical

assessm en t b ef or e sch ed u lin g an d im p r ov em en t in

com m u n i cat i on w i t h t h e p at i en t b y d i scu ssi n g t h e

sur gical dat e and his( er ) convenience and pr e- sur gical

or ien t at ion ) . Th e can cellat ion r at e w as r ed u ced b y

T h e r e s u l t s o f t h i s s t u d y s h o w e d t h a t

su r g er y can cellin g p r esen t ed a t ot al d ir ect cost of

R$ 1 , 7 1 3 . 6 6 , a sm all am ou n t if w e con sider t h e size

o f t h e st u d y i n st i t u t i o n . I t al so r ev eal ed t h at t h e

co st o f h u m a n r eso u r ces r ep r esen t ed t h e h i g h est

p er cen t ag e o f t o t al co st ( 6 0 . 1 % ) . Th e d i r ect co st

g e n e r a t e d b y t h e ca n ce l l i n g o f e l e ct i v e su r g e r i e s

i n d i c a t e d t h a t e r r o r s o c c u r r e d i n t h e i n t e r n a l

en v ir on m en t of t h e Su r g ical Cen t er Un it an d t h at ,

c o n s e q u e n t l y , t h e a d m i n i s t r a t i v e p l a n n i n g

r e q u i r e m e n t s w e r e n o t m e t . I t i s a l o ss f o r t h e

h o s p i t a l , s i n c e i n t e r n a l e r r o r s d o n o t r e s u l t i n

p r oced u r es t h at w ill ev en t u ally g en er at e r ev en u es.

S i n c e m o s t o f t h e c a n c e l l a t i o n s w e r e

p o t e n t i a l l y a v o i d a b l e , t h e s e f i n d i n g s e v i d e n c e

con cr et e possibilit ies of r edu cin g t h e lev el of su r gical

can cellat ion s by an aly zin g cau ses t h at gen er at e t h e

p r ob lem . We ar g u e t h at ch an g in g on ly on e f act or,

t h e m a i n r ea so n f o r t h e ca n cel l i n g , p r o b a b l y w i l l

n ot ex er t a p osit iv e ef f ect if ot h er f act or s ar e n ot

ch an ged sim u lt an eou sly( 3 ). For t h e h ospit al t o r edu ce

t h e r at e of can cellat ion s, each pr oblem n eeds t o be

s o l v e d i n t h e p r o c e s s , s t a r t i n g w i t h s u r g e r y

s c h e d u l i n g , e f f e c t i v e d i s t r i b u t i o n S CU a n d

n ot if icat ion t o t h e pat ien t . I n t h e qu alit y appr oach ,

t h e cost s m u st b e com p osed m ain ly b y p r ev en t iv e

c o s t s ( e m p h a s i z i n g t h e e d u c a t i o n o f s e v e r a l

c a t e g o r i e s w i t h r e s p e c t t o u n n e c e s s a r y

e x p e n d i t u r e s) t o t h e d e t r i m e n t o f e v a l u a t i o n o r

cor r ect ion cost s( 1 8 ).

Th e e co n o m i c a m o u n t t h a t co m p o se s t h e

cost of oppor t unit y of t he cancelled sur ger ies under

st udy w as R$ 10, 782. 40. The differ ence bet w een t he

SR u sage capacit y an d it s ef f ect iv e u se det er m in es

t h e e c o n o m i c v a l u e t h a t c o u l d b e o b t a i n e d a n d

r epr esen t s t h e r elat iv e econ om ic loss in r elat ion t o

t he oppor t unit y cost of not using t he sur ger y r oom .

Th i s co st i s r e l a t e d t o m a n a g e m e n t i n e f f i ci e n cy,

because it is an econom ic consum pt ion and ident ifies

an in efficacy, sin ce in com e t h at w ou ld con t r ibu t e t o

t h e r esu lt if t h e su r g er y h ad b een p er f or m ed w as

n ot g en er at ed .

Consider ing t hat econom ic pr ofit is obt ained

b y t h e i n c o m e m i n u s a l l c o s t s i n v o l v e d i n i t s

ach iev em en t , t h e m easu r em en t of t h e r esu lt s, f or

t h e sak e of m an ag em en t p er f or m an ce assessm en t ,

should t ak e int o account t he cost of oppor t unit y( 1 4 ).

How ever, it is obser v ed t hat it is difficult t o per ceive

t his cost in t he st udy inst it ut ion for t w o r easons. The

fir st is r elat ed t o a high dem and for sur ger ies, w it h a

c o n s e q u e n t w a i t i n g l i s t . On t h e o n e h a n d , t h i s

pr ev ent s t he inefficient pr ocess fr om being r eflect ed

in t he idle capacit y of t he SR and PACU and, on t he

ot her side, it hinder s t he j udgm ent of w hat is a r ight

or w r on g d ecision d u e t o t h e ex p ect ed r esu lt . Th e

seco n d i s r el a t ed t o t h e co m m o n h a b i t o f l et t i n g

p a t i en t s w i t h n o n - sch ed u l ed su r g er i es, f a st f o r a

p ot en t ial su r g er y.

Thus, t he inst it ut ional st r uct ur e t r ansfer s t he

inefficiency of t he pr ocess t o t he pat ient ( usually an

SUS user ) , w ho ends up car r ying t he r elat ive cost s of

t h e s u r g e r y c a n c e l l a t i o n ( w a i t i n g t i m e , f a s t i n g ,

em ot ional cost s) . Pat ient s w it h ot her healt h insurances

t h an t h e Sin gle Healt h Sy st em ( SUS) , h ow ev er, ar e

n ot w illin g t o deal w it h poor ly elabor at ed pr ocesses

or inefficient m anager s. These char act er ist ics of t he

in st it u t ion , su ch as h ig h d em an d f or su r g er ies an d

k e e p i n g n o n - s c h e d u l e d p a t i e n t s f a s t i n g c a n g o

u n n ot iced an d u n cor r ect ed f or a lon g t im e becau se

t h ey h av e been accept ed as a n at u r al par t of daily

w o r k .

Th e im plem en t at ion of t h e oppor t u n it y cost

concept in m easur ing t he cost of a good is t he m et hod

t h a t b e s t r e f l e c t s a m a n a g e r ’ s e f f i c a c y i n t h e

m anagem ent of t he r esour ces used( 15). The focus on

e co n o m i c m e a su r e m e n t b y o p p o r t u n i t y co st i s a

r el ev a n t i n st r u m en t o f f eed b a ck f o r p l a n n i n g a n d

cont r ol( 16). Measur em ent is t he fir st st age t hat leads

t o cont r ol an d, ev en t ually, t o t he im pr ov em ent of a

pr ocess( 1 9 ).

CONCLUSI ON

Th i s st u d y h i g h l i g h t ed t h e m i cr o eco n o m i c

aspect s of su r ger y can cellin g, in clu din g dir ect cost s

and cost of oppor t unit y, and allow ed for a sit uat ional

diagnosis of t he Sur gical Cent er Unit . Based on t his

i n f o r m a t i o n , n u r s e s c a n u s e s t r a t e g i e s i n t h e i r

m a n a g e m e n t w o r k t o m i n i m i z e t h i s o c c u r r e n c e .

Adm inist r at iv e planning, r edesigned w or k pr ocesses,

educat iv e m easur es and pr ev ious clinical assessm ent

ar e r ecom m en d ed st r at eg ies.

Alt h ou g h t h e r esu lt s r ef lect t h e ex p er ien ce

of a public t eaching hospit al and, t her efor e, m ay not

be r epr esent at ive of ot her hospit als, t he aut hor s hope

t h a t t h e s e f i n d i n g s c a n h e l p h o s p i t a l s i n t h e

developm ent of st r at egies t o r educe t he cancelling of

s c h e d u l e d s u r g e r i e s a n d i t s i m p a c t o n c o s t

REFERENCES

1 . Pa sch o a l MLH. Ta x a d e su sp en sã o d e ci r u r g i a em u m

hospit al univer sit ár io e os m ot ivos de absent eísm o do pacient e

à cir ur gia pr ogr am ada. [ disser t ação] . São Paulo ( SP) : Escola

d e En f er m ag em / USP; 2 0 0 2 .

2 . Cav alcan t i JB, Pag liu ca LMF, Alm eid a PC. Can celam en t o

de cir ur gias pr ogr am adas em um hospit al- escola: um est udo

ex plor at ór io. Rev Lat ino- am Enfer m agem 2000 j ulho- agost o;

8 ( 4 ) : 5 9 - 6 5 .

3 . Sch of ield WN, Ru b in GL, Piza M, Lai YY, Sin d h u sak e D,

Fear n sid e MR, Klin eb er g PL. Can cellat oin of op er at ion s on

t h e day of in t en ded su r ger y at a m aj or Au st r alian r ef er r al

h osp it al. Med J Au st 2 0 0 5 Ju n e 2 0 ; 1 8 2 ( 1 2 ) : 6 1 2 - 5 .

4 . Robb WB, O‘Su lliv an MJ, Br an n igan AE, Bou ch ier - Hay es

D J. A r e e l e c t i v e s u r g i c a l o p e r a t i o n s c a n c e l l e d d u e t o

i n cr e a si n g m e d i ca l a d m i ssi o n s? I r J Me d Sci 2 0 0 4 Ju l y

-Sep t em b er ; 1 7 3 ( 3 ) : 1 2 9 - 3 2 .

5 . Ag u ir r e- Cor d ov a JF, Ch av ez- Vazq u ez G, Hu it r on - Ag u illar

GA, Cor t es- Jim en ez N. Wh y is su r g er y can celled ? Cau ses,

im p licat ion s, an d b ib liog r ap h ic an t eced en t s. Gac Med Mex

2 0 0 3 No v em b er - D ecem b er ; 1 3 9 ( 6 ) : 5 4 5 - 5 1 .

6. Tait AR, Voepel- Lew is T, Munr o HM, Gut st ein HB, Rey nolds

PI . Cancellat ion of pediat r ic sur ger y: econom ic and em ot ional

im plicat ions for pat ient s and t heir fam ily. J Clin Anest h 1997

May ; 9 ( 3 ) : 2 1 3 - 9 .

7. Abdellaoui A, Addison A. A st udy of cancelled oper at ions

in an or t h opaedics depar t m en t . Clin Gov Bu ll 2 0 0 5 Mar ch ;

5 ( 6 ) : 6 - 9 .

8 . Gat t o MAF, Jou clas VMG. Ot im izan d o o u so d a SO. Rev

SOBECC 1 9 9 8 j an ei r o - m ar ço ; 3 ( 1 ) : 2 3 - 8 .

9 . S i l v a S H d a . Co n t r o l e d a q u a l i d a d e a s s i s t e n c i a l :

im plem ent ação de um m odelo. [ t ese] . São Paulo ( SP) : Escola

d e En f er m ag em / USP; 1 9 9 4 .

1 0 . Rob les A Ju n ior. Cu st os d a q u alid ad e: u m a est r at ég ia

par a a com pet ição global. São Paulo ( SP) : At las; 1994.

11. Souza D de LE. CCQ - Fazendo acont ecer. Belo Hor izont e:

Ch r ist ian o Ot t on i/ Escola d e En g en h ar ia/ UFMG; 1 9 9 6 .

1 2 . Per eir a GBS, Bar aú n a MLPS de. Cu st o de opor t u n idade

s o b o e n f o q u e d o m o d e l o g e s t ã o e c o n ô m i c a . I n : 9 º

Con gr esso Br asileir o de Cu st os; 2 0 0 2 . Ou t u br o 1 3 - 1 5 ; São

Pau l o, São Pau l o. [ ci t ad o 2 0 0 4 set em b r o 2 1 ] . Di sp on ív el

e m : U RL : h t t p : / / w w w . a b c c u s t o s . o r g . b r / t e x t o /

v i e w p u b l i c?I D _ TEXTO= 1 4 4 3 .

13. Silva AS, Reis EA dos, Leão LCG. Cust o de oport unidade.

I n : 4 º Con g r esso Br asileir o d e Cu st os; 1 9 9 7 . Nov em b r

o-Dezem br o 28- 01; Belo Hor izont e, Minas Ger ais. [ cit ado 2004

s e t e m b r o 2 1 ] . D i s p o n ív e l e m : URL: h t t p : / /

w w w . abccu st os. or g. br / t ex t o/ v iew pu blic?I D_ TEXTO= 2 0 5 .

1 4 . N a s c i m e n t o A M , S o u z a M A d e . C u s t o s d e

op or t u n id ad e: ev olu ção e m en su r ação. I n : 1 0 º Con g r esso

Br a si l e i r o d e Cu st o s; 2 0 0 3 . Ou t u b r o 1 5 - 1 7 ; Gu a r a p a r i ,

Es p ír i t o Sa n t o . [ c i t a d o 2 0 0 4 s e t e m b r o 2 1 ] . D i s p o n ív e l

e m : U RL : h t t p : / / w w w . a b c c u s t o s . o r g . b r / t e x t o /

v i e w p u b l i c ?I D _ TEX TO = 1 7 2 9 .

15. Cat elli A. Cust os de opor t unidade na gest ão da cadeia de

valor. I n: 9º Congr esso Brasileir o de Cust os; 2002. Out ubr o

1 3 - 1 5 ; São Pau lo, São Pau lo. [ cit ad o 2 0 0 4 set em b r o 2 1 ] .

D i sp o n ív el em : URL: h t t p : / / w w w . a b ccu st o s. o r g . b r / t ex t o /

v i e w p u b l i c?I D _ TEXTO= 1 4 2 1 .

16. Ar iet a CEL, Taiar A, Kar a-José N. Ut ilização e causas de

su sp en são d e in t er v en ções cir ú r g icas ocu lar es em Cen t r o

Ci r ú r g i co am b u l at o r i al u n i v er si t ár i o . Rev Asso c Med Br as

1 9 9 5 ; 4 1 ( 3 ) : 2 3 3 - 5 .

1 7 . Lir a RPC, Nascim en t o MA, Tem p or in i ER, Kar a- José N,

Ar iet a CEL. Suspensão de cir ur gias de cat ar at a e suas causas.

Rev Saú d e Pú b lica 2 0 0 1 ; 3 5 ( 5 ) : 4 8 7 - 9 .

1 8 . Pi n h o RCS, Pesso a MNM, Pet er MGA, Co ch r an e TMC,

Pet er FA. Cust os da qualidade na at iv idade de audit or ia. I n:

1 0 º Con gr esso Br asileir o de Cu st os; 2 0 0 3 . Ou t u br o 1 5 - 1 7 ;

Gu a r a p a r i , Esp ír i t o Sa n t o . [ ci t a d o 2 0 0 4 se t e m b r o 2 1 ] .

D i sp o n ív el em : URL: h t t p : / / w w w . a b ccu st o s. o r g . b r / t ex t o /

v i e w p u b l i c?I D _ TEXTO= 1 6 8 3 .

19. Maia JRC, Nascim ent o M do, Kielw agen KE, Cost a FA. A

g est ão d os cu st os d a q u alid ad e ot im izan d o o p r ocesso d e

gar ant ia da qualidade. I n: 8º Congr esso Br asileir o de Cust os;

2003. Out ubr o 3- 5; São Leopoldo, Rio Gr ande do Sul. [ cit ado

2 0 0 4 s e t e m b r o 2 1 ] . D i s p o n ív e l e m : U RL: h t t p : / /

w w w . ab ccu st os. or g . b r / t ex t o/ v iew p u b lic?I D_ TEXTO= 2 1 0 9 .