MASTER’S

FINANCE

WORK MASTERS FINAL

D

ISSERTATION

E

VALUATION OF

F

INANCIAL ASSETS AND LIABILITIES

:

A COMPARATIVE

A

NAM

ARGARIDAN

ASCIMENTOD

OMINGUESMASTER’S

FINANCE

WORK MASTERS FINAL

D

ISSERTATION

E

VALUATION OF

F

INANCIAL ASSETS AND LIABILITIES

:

A COMPARATIVE

A

NAM

ARGARIDAN

ASCIMENTOD

OMINGUESS

UPERVISOR:

P

ROFESSORD

R.

F

ERNANDOF

ELIXC

ARDOSOI

Acknowledgement

A special thanks to my dear counselor, professor Fernando Félix Cardoso who showed great interest and availability to walk the path with me in this project, suggesting the main guidelines and key points for the chosen subject, always sharing his knowledge and experience in the economic and financial area.

My second acknowledgment goes to my parents, who are responsible for who i am today, with their lifelong teaching of key values and principles for the establishment of successful goals. My deepest thank you for the patience and counsel given, which motivated me so highly throughout the development of my work.

Lastly i would like to extend a special thank you to all my friends, for all the support, care, patience and understanding demonstrated in all my moments of greater absence which were necessary to accomplish this goal.

Thank you to all my professors who shared their vast knowledge over the last few years, enabling me to finish this Project.

II

Abstract

At a time when the globalization of financial markets demands that its agents act with prudence, it is important to study how the financial instruments can be registered and how that registry affects the evaluations of financial statements.

This work compares the systems used by financial institutions and regulators to determine the value of financial assets and liabilities.

Over the course of this work a comparative analysis will be performed in relation to the enforcement of evaluation norms for assets and liabilities by their classification, initial recognition and measurement as they are applied in Portugal, Brazil and USA.

The main question of this investigation will be: what is the impact of different norms on financial instruments?

In conclusion, it is the intention of this work to shed light on the principles by which financial instruments are ruled as they vary in different norms and how they are classified in financial statements.

III

Resumo

Numa altura em que a globalização dos mercados financeiros exige que os agentes atuem com prudência, é importante estudar as formas como os instrumentos financeiros podem ser registados e como esse registo afeta a avaliação das demonstrações financeiras.

Este trabalho compara os sistemas de determinação do valor dos ativos e passivos financeiros das instituições financeiras e feitas por órgãos supervisores diferentes.

Ao longo deste trabalho pretende-se fazer uma análise de comparação relativamente a aplicação das normas de avaliação dos ativos e passivos analisando a classificação, o reconhecimento incial e mensuração referentes a instrumentos financeiros em Portugal, no Brasil e nos EUA.

A questão principal desta investigação será: onde irá impatar a aplicação das normas sobre instrumentos financeiros nos diferentes normativos?

Em conclusão, com este trabalho pretendemos esclarecer quais os princípios pelos quais se regem os dos instrumentos financeiros nas diferentes normas e como se classificam nas demonstrações financeiras.

IV

Table of contents

Acknowledgement ... I Resumo ... III Table of contents ... IV Chapter 1 – Introduction ... 1Chapter 2- Accounting Harmonization ... 3

2.1 International Environment ... 4

2.2 European Union... 4

Chapter 3- Historical evolution of each norm ... 6

3.1 Historical Evolution of Financial instruments in IFRS ... 6

3.2 Historical evolution of North American accounting norms (US GAAP) ... 7

3.3 Historical evolution of accounting norms in Brazil... 8

Chapter 4- Presentation norms ... 10

4.1 Presentation norms of IFRS ... 10

4.1.1 IAS 32 Financial Instruments: Presentation ... 10

4.1.2 IAS 39- Financial Instruments’ recognition and measurement ... 10

4.1.3 IFRS 9 - Financial Instruments: Classification and Measurement ... 13

4.1.4 Comparative between norms IAS 39 and IFRS 9: ... 14

4.1.5 IFRS 7- Financial Instruments Disclosure... 15

4.2 Presentation of US GAAP norms ... 15

4.2.1 Held-to-Maturity Securities ... 17

4.2.2 Trading Securities and Available-for-Sale Securities ... 18

4.3 Presentation of BR GAAP norms ... 21

4.3.1 Segmentation and classification for purposes of measurement and presentation ... 21

Chapter 5- Comparison of different norms ... 23

5.1 Comparative between IFRS and US GAAP ... 24

5.1.1 Categorization of financial assets: ... 24

5.2 Comparative between IFRS and BR GAAP ... 27

Chapter 6- Conclusion ... 30

6.1 Limitations ... 31

6.2 Recommendations ... 31

V

Index of Figure

VI

Index of tables

Table 1- Classification norms for financial instruments ... 12 Table 2- Comparison of the classification ... .14 Table 3- Comparison of different norms ... 23

VII

Acronyms

AAPA - American Association of Public Accountants

AAUIA - American Association of University Instructors in Accounting AIA - American Institute of Accountants

AICPA- American Institute of Certified Public Accountants APB - Accounting Principles Board

ASU- Accounting Standards Update BACEN- Brazilian central bank

CAP- Committee on Accounting Procedure CMN- National Monetary Council

COSIF- Chart of Accounts for Institutions of the National Financial System CPC- Accounting Pronouncements Committee

CVM- Securities commission

FASB-Financial Accounting Standards Board IASB-International Accounting Standards Board IASC- International Accounting Standards Committee IAS-International Accounting Standard

IFRS - International Financial Reporting Standards NYSE- New York Stock Exchange

1

Chapter 1 – Introduction

The present work looks at the comparison of different types of international norms applied to financial assets and liabilities. Such use is intended to adjust the accounting to the “fair value” option.

It is proper then, to count on the norms that have different accounting systems (the main two, based on IAS/IFRS and FAS) and on the different approaches used by the regulators as they apply the methods and principles of each one.

At a time when the globalization of financial markets demands that its agents act with prudence, an approach that does not take into account the different characteristics of evaluation can induce deciding bodies in error.

It is for this reason that this work will compare the systems that determine the value of financial assets and liabilities of financial institutions and the respective enforcements of different regulatory agents.

The different consequences of different procedures in financial statements will also be identified in order to understand if they are agents of volatility.

The study spans 6 chapters. The first introduces the accounting problems over its evolution. The first chapter also outlines the study, with its objectives, main questions, investigation approach and information gathering method.

In the second chapter we will introduce the accounting harmonization questions and procedures.

The third and fourth chapters detail the history for each norm and subsequently a presentation of each one.

2

The fifht chapter compares the different types of norms studied throughout the work and finally a conclusion of this dissertation will be presented.

3

Chapter 2- Accounting Harmonization

Accounting harmonization is a fundamental milestone in the history of accounting and the basis that explains the dicothomy for entities that are currently in the process of choosing a model of accounting. Succintly and as a starting point to this work, the need and objectives of accounting harmonization as well as alterations that take place at an international level as well as in Portugal will be explored.

According to Volker (2002) in spite of an emission of proper norms that respond to new developments in financial markets, the quick globalization of these on par with different accounting norms and different enforcing mechanisms actually further increase the risks.

Lima (2010) points out that due to market interactions; there is a real necessity for uniformity in respect to the standard language of international investors.

According to Silva, et al. (2009) accounting harmonization implies a profound change in countries' accounting habits, raising questions such as what factors justify the existence of different norms amongst countries and what type of impacts would be felt with this harmonization.

The question of which factors justify differences amongst countries was explored by several authors who contributed in several ways to the literature on this theme. Radebaugh e Gray (1993) justified norm differences among countries with the historical, economical and cultural differences that existed. Choi et al. (1999) e Cañibano e Mora (2000) even found a connection between the aproximation of accounting practices and the social, economical, legal, and cultural similarities of countries.

4 2.1 International Environment

In 1973 in correspondence with the need to determine accounting principles, the International Accounting Standards Committee was established. Known as IASC its main function was to be responsable by issuing international accounting norms.

Rodrigues(2011) states that this institution was responsible for the objectives, definitions, publications, acceptance and conformity of accounting norms in an international level between 1973 and 2000, having also contributed to the aproximation of reported information and account credibility.

In 2001 IASC was reestructured and became IASB (International Accounting Standard Board). The norms issued up until that year by IASC and designated as International Accounting Standards (IAS) were also subjected to changes, and became (IFRS) International Financial Reporting Standards.

While IAS encompassed only accounting, IFRS encompassed accounting and financial reporting.

The Financial Accounting Standards Board (FASB) is a private institution, whose primary purpose is to establish and improve generally accepted accounting principles (GAAP) within the United States in the public's interest. The Securities and Exchange Commission (SEC) designated the FASB as the organization responsible for setting accounting standards for public companies in the U.S. The FASB replaced the American Institute of Certified Public Accountants' (AICPA) Accounting Principles Board (APB) on July 1, 1973.

2.2 European Union

In 1995 the international environment, the European commission presented a document “Accounting harmonization: a new strategy vis-à-vis international harmonization”

5

which considered the creation of an organism responsible for creating accounting rules and applying them throughout the European Union.

IOSCO's (International Organization of Securities Commissions) objectives and principles are the main instruments for development and implementation of international regulatory, supervisory and enforcement norms, internationally recognized as the principles and orientations to apply globaly by the market agents or regulatory agents.

In 2000 while considering the needs of stock market businesses, after the announcement by the president of IOSCO, the institution abandons the idea to create an independent organism. He also reveals a document that replaces the previous and announces a plan for adopting the IASB norms until 2005 called "EU strategy for the future of corporate financial reporting"

In July 19th 2002 the EU issued the regulation (EC) n.º 1606/2002 which stated that starting january 1st 2005 all societies that transact business in one of the member states and whose bonds are negotiated publicly are obliged to present their financial statements according to internation accounting norms (article 4). In the same regulation it is allowed the member states to permit or demand financial statements for all other businesses based on IAS/IFRS (article 5).

6

Chapter 3- Historical evolution of each norm

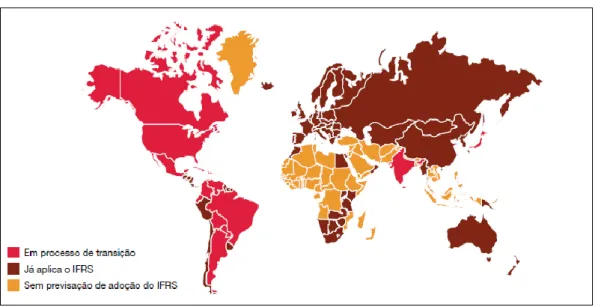

3.1 Historical Evolution of Financial instruments in IFRSThe International Financial Reporting Standards (IFRS’s) are issued by the International Accounting Standards Board (“IASB”). The first international norms then known as International Accounting Standard (IASs) were issued in 1973, but the global move to adopt IFRS only started after the Enron scandal in 2002, with the awareness that a principle based norm would be more faithful to the economic reality of transactions than norms based on rigid rulesets.

Adherence to IFRS started in 2002 when the EU determined that all 7000 european enterprises should apply the IFRS norm in their financial demonstrations starting in 2005. Other countries including Australia, Hong Kong, South Africa and some easter european nations, also joined around the same time. The next wave included Brasil, South Korea, India and Canada. The international convergence will be completed only when the USA allow the use of IFRS which is likely to be adopted.

Figure 1 - IFRS enforcement around the world

7

3.2 Historical evolution of North American accounting norms (US GAAP)

In the United States of America the accountant profession was recognized in 1904 at the time of the International Accountant Congress.

In 1916 the American Association of University Instructors in Accounting was founded, whose initial objective was to develop a curriculum for university and only later to develop themes related to accounting theory.

After the “crash” in the New York stock exchange, members of Association Institute of Accountants and NYSE gathered to discuss different accounting aspects of interest to investors, stock exchanges and accountants for elaborating and publishing accounting statements.

In 1935 the American Association of University Instructors in Accounting changed its name to American Accounting Association and following that their first work “A Tentative Statement of Accounting Principles Underlyng Corporate Financial Statements”.

The American Institute of Certified Public Accountants created throughout history several committees and boards directed to the development of accounting principles most notably the Committee on Accounting Procedure created in 1938 and the Accounting Principles Board), in 1959.

In 1972 arose the Financial Accounting Standards Board as an independent organ of the American Institute of Certified Public Accountants.

8 3.3 Historical evolution of accounting norms in Brazil

The adoption of the IFRS in Brazil was inevitable considering the worldwide use of the IAS/IFRS.

We think that in a few years, the countries that dont adopt the IAS/IFRS will have difficulties operating in a global environment.

In September 2010, the Securities and Exchange Committee divulged the instruction nº 485 which requires consolidated financial statements for listed companies to be presented in conformity with IAS/IFRS and Brazilian accounting norms issued by Comité de

Pronunciamentos Contabilísticos (or CPCs).

The Comite de Pronunciamentos Contábeis (CPC) was created by the CFC Resolution nº nº 1.055/05 and has as its main objective "the study preparation and issuance of technical statements on accounting procedures and the release of informations of that nature, that allow the issuance of norms by the Brazilian regulatory body, with the aim of centralizing and uniformization of the production process, taking into account the convergence of Brazilian accounting with international standards.” However for individual financial reports only the CPC are applied.

As mentioned above, in Brazil the main focus of obligation in applying the IAS/IFRS is for consolidated accounts. There are some discrepancies between the norms applied to consolidated financial reports and norms used in reports that serve as basis for payment of dividends and taxes (individual financial reports). Brazilian corporations are also forced to apply certain accounting policies intrinsic to brazilian traditions (for example, the evaluation of assets is forbidden) and to include additional informations not required by IAS/IFRS (for example, demonstration of added value).

The norms pertaining to financial instruments are fundamental in accounting for operations carried out by financial institutions, especially due to the relevant level of financial instruments as assets and liabilities in relation to the sum of these assets and liabilities in

9

financial institutions. A financial instrument is any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity. That is the essence of the financial institutions' business as they perform their duty as intermediary of financial resources, receiving and applying them.

3.3.1 Publication of accounting statements for financial institutions in IFRS and COSIF: Brazilian financial institutions are subject to supervision by Banco Central do Brasil (Bacen) and to laws and specific regulations. The law 4.595/64 empowers the Conselho Monetário Nacional (CMN) to create general norms of accounting for the sector, and the law 6.385/76 reinforces that competence. That legal structure has allowed BACEN to prevent full adoption of the CPCs by the financial institutions except for consolidated statements produced by large institutions which elaborate them parallel to those under Brazilian criteria, even though they may not publish them together. This in spite of BACEN elaborating and issuing its own statements in IFRS guidelines for many years.

Non financial entities, regulated by the SEC (Securities and Exchange Commission) are forced to follow all determinations issued by the Comité de Pronunciamentos Contábilisticos (CPC) which obey the IFRS norms, be it for the individual statement as for the consolidated.

However the use of IFRS is null for individual statements or the published consolidated statements in case of financial institutions which must follow the regulator BACEN. This way BACEN will require issuing two financial statements, the consolidated balance sheet in IFRS (for large institutions) and individual and consolidated balance sheets published separately for all others.

10

Chapter 4- Presentation norms

4.1 Presentation norms of IFRSThe process for the normalization of International Accounting Standard Board (IASB) on financial instruments had several developments over time. Nowadays there are four norms for financial instruments:

IAS 32 – Financial Instruments: Presentation;

IAS 39 – Financial Instruments: Recognition and Measurement; IFRS 7 – Financial Instruments: Disclosures

IFRS 9 - Financial Instruments: Classification and Mensuration

4.1.1 IAS 32 Financial Instruments: Presentation

Definition of principles for the presentation of financial instruments as liability and own capital and clearing between financial assets and liabilities:

Classification of financial instruments in financial liabilities and equity instruments; classification of interest, dividends and associated wins and losses; verification of circunstances for compensation between financial assets and liabilities; presentation of compound financial instruments which are those that combine debt and equity; complementing other international norms for financial report in respect to principles for recognizing and measuring assets (IAS 39 and/or IFRS 9) as well as financial liabilities (IAS 39) and also the principles for information circulation (IFRS 7).

4.1.2 IAS 39- Financial Instruments’ recognition and measurement

It should be noted that the IAS39 is most likely the most complex of all international norms for financial reporting. It pertains to accounting of all types of financial instruments, from the simplest such as loans, to the more complex derivative structures.

11

Establish the principles to recognise and measure financial assets, financial liabilities and certain contracts to buy or sell nonfinancial items; introduction of derivative instruments and accounting for risk coverage operations. (Hedge accounting);

A financial asset will be measured by the amortized cost if the following two conditions are met: the asset is owned within a business model whose objective is to maintain assets for contractual cash flows.

In the meanwhile an entity might in the initial assessment, designate irrevocably an asset as measured to just value by means of the result, if, by doing so, it might eliminate or significantly reduce a measuring or assessment inconsistency (often times referred to as an accounting mismatch) which might otherwise result of measuring assets or liabilities, or from recognizing gains and losses over those assets and liabilities in different bases.

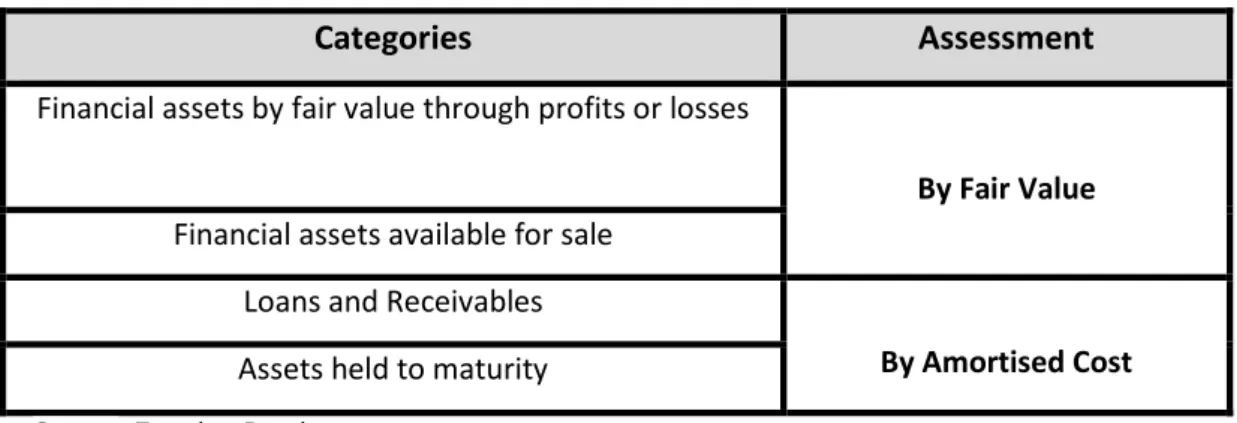

According to IAS 39, the financial assets may be classified in the following categories:

Financial assets by just value through profits or losses.

This group of assets may be subdivided in two parts: the first includes assets which during initial assessment are measured or valued by just value and whose variations are regulated through profits or losses. It is important to reference that, once initially recognized, financial assets must be well maintained to the end. This is a revocable decision.

The second includes the assets maintained for negotiation or for transaction and constitute the trading book.

Financial assets available for sale: these assets are valued by just value with the corresponding variations recognized on own capital and highlighted in a variation board within the own capital.

12

Loans and Receivables are non derivative financial assets with fixed or determined treasury flows which are not quoted in the active market and are generated within the entity.

Active investments held to Maturity: Investments held to maturity are financial assets with fixed or determined payments which the entity intends or is able to maintain until its deadline and are not those which the entity in initial assessment designates as available for sale, loans and receivables or by just value regulated by results. They are evaluated by the amortized cost method with and effective interest rate.

The first two categories lead to evaluated assets measured by just value, while the last two lead to the use of amortized cost. This highlights the importance of financial assets’ classification.

Table 1- Classificationnorms for financial instruments

Categories

Assessment

Financial assets by fair value through profits or losses

By Fair Value

Financial assets available for sale Loans and Receivables

By Amortised Cost

Assets held to maturity

Source: Ferreira, Domingos

An entity will classify all financial liabilities as measured to amortized cost using the effective interest rate method except for:

The fair value trough profit or loss- these losses, including derivatives which are losses, will be measured by fair value; non classified financial losses such as fair value by result, financial guarantee contracts.

13

After initial recognition an issuer will be measured by the greater value between:

The value determined according to IAS 37 – Provisions, Contingent Liabilities and contingent Assets; the amount initially recognized less, when appropriate, cumulative amortization recognized in accordance with IAS 18 Revenue.

Commitments to provide a loan at a below market interest rate.

After initial recognition, an issuer of such a contract shall measure it at the higher of: the value determined according to IAS 37; the amount initially recognized less, when appropriate, cumulative amortization recognized in accordance with IAS 18 Revenue.

4.1.3 IFRS 9 - Financial Instruments: Classification and Measurement

This norm was created to substitute IAS39, by simplifying and reducing its complexity when using financial instruments. It was introduced in a approach to the first phase of its structure (November 2009) with news requisites for classification and measurement financial assets, since they form the base of support for financial instruments reporting.

In accordance to commitments made in 2008 the, IFRS 9 was developed by IASB in the following three phases:

Phase 1: classification and measurement of financial assets and financial liabilities- the first phase was concluded by defining new classification and measurement rules for financial assets and liabilities.

Phase 2: impairment methodology- the second phase was concluded by defining a new methodology of identification for losses by impairment

Phase 3: hedge accounting- the third phase was concluded by defining improvements to the current rules of hedge accounting.

14

However IFRS 9 is not yet applied to financial institutions and, consequently, all the assumptions of IAS 39, are kept.

According to IFRS 9, upon recognizing for the first time a financial asset, an entity must classify it according to the entities business model for financial assets and respective contractual cash flow.

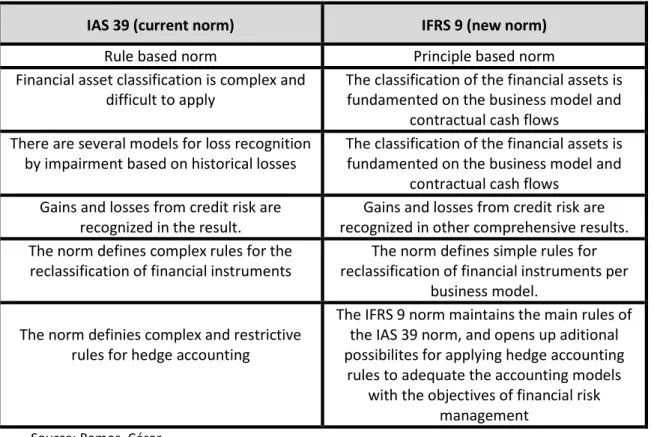

4.1.4 Comparative between norms IAS 39 and IFRS 9:

The following table presents a summary of the comparison of the classification rules and disclosure of financial instruments as defined by IAS 39 and IFRS 9:

Table 2- Comparison of the classification

IAS 39 (current norm) IFRS 9 (new norm)

Rule based norm Principle based norm

Financial asset classification is complex and difficult to apply

The classification of the financial assets is fundamented on the business model and

contractual cash flows There are several models for loss recognition

by impairment based on historical losses

The classification of the financial assets is fundamented on the business model and

contractual cash flows Gains and losses from credit risk are

recognized in the result.

Gains and losses from credit risk are recognized in other comprehensive results. The norm defines complex rules for the

reclassification of financial instruments

The norm defines simple rules for reclassification of financial instruments per

business model. The norm definies complex and restrictive

rules for hedge accounting

The IFRS 9 norm maintains the main rules of the IAS 39 norm, and opens up aditional possibilites for applying hedge accounting

rules to adequate the accounting models with the objectives of financial risk

management Source: Ramos, César

15 4.1.5 IFRS 7- Financial Instruments Disclosure

Disclosing informations that allow the users of financial demonstrations to evaluate on one hand the importance and significance of financial instruments in relation to the financial position and company performance, and on the other hand the nature and extent of the associated risks in long or short positions assumed by companies during the analysis period and the report date, and also to evaluate the management policy of those risks.

The complex of the principles, mentioned in norms (IAS 32 and 39 and/or IFRS 7).

4.2 Presentation of US GAAP norms

Financial instruments have been the subject of numerous issuances of technical guidance interpretation, revisions in standards, and harsh criticism from the investor community. While some instruments are recorded at historical cost, similar to property plant, and equipment, many are regularly revalued to fair value.

Because financial instruments are liquid, meaning they can be turned into cash quickly, the standard setters prefer reporting at fair value since it is useful and relevant to users of the financial statements in assessing the amount, timing, and risk of cash flows. This near-cash quality is what makes financial instruments so different from other non cash assets.

As a compromise to counter the volatility that fair value reporting can impart on an entity’s results, current rules required the classification of financial instruments into three classes: Held-to-maturity, available-for-sale and trading.

A financial liability is any liability that is a contractual obligation to deliver cash or another financial asset to another entity; or to exchange financial assets or financial liabilities with another entity under conditions that are potentially unfavorable to the entity.

16

What qualifies as a financial instrument is the first question that must be answered before embarking on accounting or reporting for an investment. Let’s start with the definitions under respective standards:

Under US GAAP, a financial instrument is defined as follows: cash, evidence of an ownership interest in an entity, or a contract that both imposes on one entity a contractual obligation either to deliver cash or another financial instrument to a second entity and to exchange other financial instruments on potentially unfavorable terms with the second entity.

This conveys to that second entity a contractual right either to receive cash or another financial instrument from the first entity and to exchange other financial instruments on potentially favorable terms with the first entity.

The Financial Accounting Standards Board (FASB) has been the designated organization in the private sector for establishing standards of financial accounting that govern the preparation of financial reports by nongovernmental entities. Such standards are important to the efficient functioning of the economy because decisions about the allocation of resources rely heavily on credible, concise, and understandable financial information.

Through SFAS 115, this statement addresses the accounting and reporting for investments in equity securities that have readily determinable fair values and for all investments in debt securities. Those investments are to be classified in three categories and accounted for as follows:

i. Debt securities that the enterprise has the positive intent and ability to hold to maturity are classified as held-to-maturity securities and reported at amortized cost;

17

ii. Debt and equity securities that are bought and held principally for the purpose of selling them in the near term are classified as trading securities and reported at fair value, with unrealized gains and losses included in earnings;

iii. Debt and equity securities not classified as either held-to-maturity securities or trading securities are classified as available-for-sale securities and reported at fair value, with unrealized gains and losses excluded from earnings and reported in a separate component of shareholders' equity.

This Statement does not apply to unsecuritized loans. However, after mortgage loans are converted to mortgage-backed securities, they are subject to its provisions. This Statement supersedes FASB Statement No. 12, Accounting for Certain Marketable Securities, and related Interpretations and amends FASB Statement No. 65, Accounting for Certain Mortgage Banking Activities, to eliminate mortgage-backed securities from its scope. This Statement is effective for fiscal years beginning after December 15, 1993. It is to be initially applied as of the beginning of an enterprise's fiscal year and cannot be applied retroactively to prior years' financial statements. However, an enterprise may elect to initially apply this Statement as of the end of an earlier fiscal year for which annual financial statements have not previously been issued.

At acquisition, an enterprise shall classify debt and equity securities into one of three categories: held-to-maturity, available-for-sale, or trading.

4.2.1 Held-to-Maturity Securities

Investments in debt securities shall be classified as held-to-maturity and measured at amortized cost in the statement of financial position only if the reporting enterprise has the positive intent and ability to hold those securities to maturity.

18

The following changes in circumstances, however, may cause the enterprise to change its intent to hold a certain security to maturity without calling into question its intent to hold other debt securities to maturity in the future. Thus, the sale or transfer of a held-to-maturity security due to one of the following changes in circumstances shall not be considered to be inconsistent with its original classification: evidence of a significant deterioration in the issuer's creditworthiness, a change in tax law that eliminates or reduces the tax-exempt status of interest on the debt security (but not a change in tax law that revises the marginal tax rates applicable to interest income), a major business combination or major disposition (such as sale of a segment) that necessitates the sale or transfer of held-to-maturity securities to maintain the enterprise's existing interest rate risk position or credit risk policy, a change in statutory or regulatory requirements significantly modifying either what constitutes a permissible investment or the maximum level of investments in certain kinds of securities, thereby causing an enterprise to dispose of a held-to-maturity security, a significant increase by the regulator in the industry's capital requirements that causes the enterprise to downsize by selling held-to-maturity securities, a significant increase in the risk weights of debt securities used for regulatory risk-based capital purposes.

4.2.2 Trading Securities and Available-for-Sale Securities

Investments in debt securities that are not classified as held-to-maturity and equity securities that have readily determinable fair values shall be classified in one of the following categories and measured at fair value in the statement of financial position: Trading securities- securities that are bought and held principally for the purpose of selling them in the near term (thus held for only a short period of time) shall be classified as trading securities. Trading generally reflects active and frequent buying and selling, and trading securities are generally used with the objective of generating profits on short-term differences in price. Mortgage-backed securities that are held for sale in conjunction with mortgage banking activities, as

19

described in FASB Statement No. 65, Accounting for Certain Mortgage Banking Activities, shall be classified as trading securities and available-for-sale securities. Investments not classified as trading securities (nor as held-to-maturity securities) shall be classified as available-for-sale securities.

The SFAS150 norm is the north american norm that defines the way an issuer will classify and quantify financial instruments with both passive and own capital characteristics, which requires that the instruments are treated as liabilities because many of these instruments were treated, prior to their emission. Some of these proposals are in line with the definition present in the FASB Concepts statement Nº 6 and others are consistent with the FASB proposal to verify the definition to contemplate certain obligations that entities may or need to liquidate through issuing their own stock, depending on the nature of the relation between the owner of the instrument and the issuer.

The objective of this norm requires the issuer of a financial instrument to classify the following instruments as liabilities (or assets in certain circunstances):

Mandatorily Redeemable Financial Instruments― A mandatorily redeemable financial instrument shall be classified as a liability unless the redemption is required to occur only upon the liquidation or termination of the reporting entity. A financial instrument issued in the form of shares is mandatorily redeemable if it embodies an unconditional obligation requiring the issuer to redeem the instrument by transferring its assets at a specified or determinable date (or dates) or upon an event certain to occur.

A financial instrument that embodies a conditional obligation to redeem the instrument by transferring assets upon an event not certain to occur becomes mandatorily redeemable and, therefore, becomes a liability if that event occurs, the condition is resolved, or the event becomes certain to occur.

20

Obligations to repurchase an issuer´s equity shares that require a transfer of assets: A financial instrument, other than an outstanding share, that, at inception:

- embodies an obligation to repurchase the issuer’s equity shares, or is indexed to such an obligation,

- requires or may require the issuer to settle the obligation by transferring assets shall be classified as a liability (or an asset in some circumstances.

- Examples include forward purchase contracts or written put options on the issuer’s equity shares that are to be physically settled or net cash settled.

Certain Obligations to issue a variable number of shares: A financial instrument that embodies an unconditional obligation, or a financial instrument other than an outstanding share that embodies a conditional obligation, that the issuer must or may settle by issuing a variable number of its equity shares shall be classified as a liability (or an asset in some circumstances) if, at inception, the monetary value of the obligation is based solely or predominantly on any one of the following:

A fixed monetary amount known at inception (for example, a payable settleable with a variable number of the issuer’s equity shares);

Variations in something other than the fair value of the issuer’s equity shares (for example, a financial instrument indexed to the S&P 500 and settleable with a variable number of the issuer’s equity shares);

Variations inversely related to changes in the fair value of the issuer’s equity shares (for example, a written put option that could be net share settled).

21 4.3 Presentation of BR GAAP norms

Financial institutions must divulge several information’s about the nature and extent of risks that derive from financial instruments to which they are exposed. In this work the following aspects of financial instruments shall be analyzed:

i. Segmentation Definitions and effects of financial instruments;

ii. Segmentation and classification for measurement and presentation purposes; iii. Categories of financial instruments;

iv. Impact no result and comprehensive impact of the exercise; v. Measuring financial instruments (fair value and amortized cost);

4.3.1 Segmentation and classification for purposes of measurement and presentation

Financial institutions segment financial instruments by means of measurement basis as suggested by the norm IFRS and by category for purposes of presenting these instruments in the balance sheet.

The CPC 14 – financial instruments: Recognition, Measurement and Disclosures was issued in 2008 and represents the first step taken by the CPC in direction of the IAS/IFRS no the matter of accounting financial instruments, basing itself in certain elements of IAS 32 – Financial Instruments: Presentation and the IAS 39 – Financial Instruments: Recognition and Measurment.

The new legislation on Financial Instruments in Brazilian norms, determines that all financial instruments are classified in 4 major groups with the follow accounting form:

i. Loans and Receivables that are recognized and maintained to historical values. They are subject to the creation of provisions for losses and fair value if relevant. This, in case it is relevant. The specialization of revenues and expenses for these instruments is made through, which assumes that the CPC 14 uses to measure the amortized cost;

22

ii. Held to maturity investments are those for which the financial entity intends to maintain such condition, registered by their historical value plus charges or financial yields, which means amortised cost. The apropriation of revenue or expense for those instruments occurs by the interests effective rate.

iii. Financial asset or financial liability measured at fair value through profit or loss, composed of assets and liabilities meant for negotiation and already classified as such, evaluated by their fair value (usually market value) with all the offsetts in the value accounted directly to the result;

iv. Available for sale financial assets destined to be negotiated in the future, recognized by amortised cost and measured at fair value. The adjustment offsetts go to the result and the fair value offsets are held in own capital until the assets and liabilities are effectivily traded.

23

Chapter 5- Comparison of different norms

The inclusion of a financial instrument in a classification of financial instruments shall state the initial recognition mode, initial measurement and subsequent measurement of the instrument.

Following comparison table:

Source: Created by the author

Table 3- Comparison of different norms

Difference description

IFRS US GAAP BR GAAP

Classification of financial instruments

On 4 items:

I. Financial assets by just value through profits or losses II. Financial assets available for sale III. Loans and Receivable

IV.Active investments held to Maturity

On 3 items:

I. Financial assets by just value through profits or losses;

II. Active investments held to Maturity; III. Financial assets available for sale

On 4 items:

I. Financial assets by just value through profits or losses II. Financial assets available for sale III. Loans and Receivable

IV.Active investments held to Maturity

Initial recognition

At fair value through profit or loss

Companies initially have free choice to recognize the fair value through

profit

At fair value through profit or loss

Initial Measurement

All instruments are initially measured at fair

value.

They are initially measured at cost, except

for derivatives and securities classified as trading or available for

sale, as well as at fair value through profit

All instruments are initially measured at

fair value.

Subsequent measurement

Loans and receivables and instruments held to

maturity are measured at amortized cost. The rest are measured at

fair value.

According to IFRS, except for loans held for sale, measured at cost or market: whichever is lower. Loans and receivables and instruments held to maturity are measured at amortized cost. The rest are measured at

24 5.1 Comparative between IFRS and US GAAP

In regard to recognition and measurement of financial assets the IASB and the FASB have numerous projects with respect to financial instruments. In November 2009 the IASB issued ED/2009/12, Financial Instruments: Amortized Cost and Impairment, which would replace the current requirements with an expected loss model.

In May 2010 the IASB issued ED/2010/4, Fair Value Option for Financial Liabilities, which retains the existing requirements for classification and measurement of financial liabilities, except for the effects of changes in own credit risk, which would be transferred to other comprehensive income. In the same year the FASB issued the Accounting Standards Update (ASU), Accounting for Financial Instruments and Revisions to the Accounting for Derivative Instruments and Hedging Activities. The ASU proposes a comprehensive approach to the accounting of financial instruments, including classification, measurement, impairment, and hedge accounting.

5.1.1 Categorization of financial assets:

The IAS/IFRS divides financial assets into the following categories:

i. Financial assets at fair value through profit or loss ii. Loans and receivables

iii. Held to maturity – defined narrowly with strict conditions; covers only assets with fixed or determinable payments and fixed maturity that the enterprise has the positive intent and ability to hold to maturity, other than loans and receivables originated by the enterprise;

iv. Available-for-sale financial assets – all financial assets not falling under another category (any financial asset other than one that is held for trading may be designated into this category on initial recognition).

25

In US GAAP there are no explicit categorization schemes for financial assets. They could be categorized as follows: eligible financial assets that the entity elects to measure at fair value – fair value option, loans and receivables, trading, held-to-maturity.

In IFRS Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market, other than: held-for-trading assets; those designated on initial recognition as at fair value through profit or loss or as available-for-sale.

An entity may reclassify out of fair value through profit or loss if certain criteria are met, those where the holder may not recover substantially all of its investment (other than due to credit deterioration), which are classified as available-for-sale.

In US GAAP a loan is a contractual right to receive money on demand or on fixed or determinable dates that is recognized as an asset in the creditor’s balance sheet.

Loans are not considered debt securities and hence may not be categorized in the trading, available-for-sale, or held-to-maturity categories.

Measurement on initial recognition:

In IFRS when a financial asset is recognised initially, an entity measures it at its fair value plus in the case of a financial asset or financial liability not at fair value through profit or loss, transaction costs that are directly attributable to the acquisition of the financial asset.

In the case of the US GAAP financial assets are recognized initially at fair value. This may lead to the recognition of premiums and discounts on loans and debt securities acquired. Except for certain costs associated with certain lending activities and loan purchases, transaction costs that are directly attributable to the purchase of a financial asset.

26 Subsequent measurement:

In IFRS of financial assets at fair value through profit or loss at fair value with gains and losses going to the income statement; held-to-maturity financial assets; loans and receivables at amortized cost; available-for-sale financial assets to fair value and take gains or losses through equity (comprehensive income) until date of sale (when recycled to income statement).

Investments in equity instruments that do not have quoted prices in active markets and whose fair value cannot be reliably measured shall be measured at cost.

In the case of US GAAP the remeasure of financial assets at fair value is assessed through earnings at fair value with gains and losses going to the income statement; held-to-maturity securities, loans held for investment, and trade receivables at amortized cost. Special rules apply for certain acquired loans with deterioration in credit quality;

Remeasure available-for-sale securities to fair value.

Unrealized gains and losses are included (net of tax) in shareholder’s equity in other comprehensive income. All or a portion of the unrealized holding gain and loss of an available-for-sale security that is designated as being hedged in a fair value hedge is recognized in earnings during the period of the hedge. Realized gains and losses are reported in earnings.

27 5.2 Comparative between IFRS and BR GAAP

Initial Recognition and Classification:

In IFRS all financial assets and liabilities are recognized initial by fair value. Usually the fair value of these assets and liabilities will be the fair value delivered (if it is an asset) or what was received (if it is a liability). When there is a difference between the two, that difference must be analysed and accounted for accordingly. For example, the difference might be generated in case of a loan at lower rated than the market with similar characteristics. In this case the difference is tread as an immediate loss (or gain) if its justified in essence. The initial fair value of a financial asset or liability must include the transaction costs, unless they are measured by the fair value with an offset in the result.

Financial assets held for trading are those which were aquired or generated by the entity with the purpose of short term negotiation, or those assets which are part of a class of assets. Derivative financial instruments are by definition always classified in this cathegory unless they are designated hedge instruments.

The assets defined above are those which at initial recognition, and only at this time, were classified at fair value by the entity regardless of their nature or characteristic.

The category of loans and receivables includes fixed payment financial assets which are not quoted in a market considered active by the norms criteria. Assets with these characteristics even if acquired in market, as long as they are not quoted in an active market are also classified in this category.

Assets held to maturity are financial assets with fixed payments with due date, that an entity intends and is able to hold until it expires. Other entities stock investments may not be classified under this category for their lack of due date. The intent and ability to maintain an asset till its due date must be evaluated at each balance sheet day. In cases where more than

28

an insignificant sale/reclassification occurs the entity is forced to reclassify all financial assets of this category to one of available for sale assets.

In the category available for sale finance are assets which have not been classified in the categories above. The entity is entitled to designate the asset as available for sale at the initial recognition, as long as it doesnt attend to the definition of fair value on result.

As for financial liabilities, they must be classified under one of the following two categories: Financial assets and financial liabilities at fair value through profit and loss and other financial liabilities

Similarly to the existing category for financial assets they must be classified as financial assets and financial liabilities at fair value through profit and loss those who follow the definition of assets maintained for negotiation or those who have been designated for this category at the initial recognition. The concepts are the same as the existing ones for financial assets. All financial liabilities which are not classified in this fair value through profit and loss category must be classified as other financial liabilities.

According to BR GAAP norms this is not forseen in brazilian accounting practices. Usually these instruments are recognized by their value, which might not be their fair value.

In the specific case of financial institutions, the categories are similar to those existent in the IFRS: in trading securities, kept through maturity and available for sale.

In the Central Bank there is no norm for fair value option as the one in the Internation norm.

In IFRS measurement of a financial instrument is dependent on its classification: Assets with fair value through profit or loss – fair value in result offsets;

Loans and Receivables – amortised cost and result offsets; Kept through maturity – amortised cost and resutl offsets; Available for sale – fair value offset in net values.

29

Other financial liabilities – amortised cost and result offset.

According to BR GAAP in general financial assets and liabilities are accounted by amortised cost. Specifically in the case of financial institutions, the classification like in IFRS is the one that determines the accounting format:

Kept for negotiation – fair value through profit and loss Held to maturity – amortised cost through profit and loss Available for sale – fair value through profit and loss.

In general, derivative instruments are acounted by amortised cost, except in the case of financial institutions, for whom these instruments have a similar treatment to IFRS.

30

Chapter 6- Conclusion

Financial instruments constitute an area of great complexity as the markets display a growing relevance in business and financial institutions.

This study determines if there are significant differences in methodology in respect to different norms for accounting of financial assets and to identify respective impacts on financial statements.

The main purpose in elaborating this paper was to analyse the divergences witnessed in the enforcement of the three norms, (US GAAP e US GAAP) in reporting for assets and liabilities through an analysis of financial instruments' classifications: initial recognition, initial and final measurement.

Adherence to IFRS began to occurr in 2002 when the European Union determinned that all european businesses should apply IFRS in their financial reporting as of 2005. The next wave of adoption included Brazil, South Korea, India and Canada. International convergence will only be achieved when the United States of America allow the use of IFRS, a decision that might be taken soon.

The differences of norms in how they classify financial instruments can be observed.

In IFRS and BR GAAP's norms there is a requirement that the issuer of a financial instrument classify them as : Financial assets or liabilities by just value through profit or loss, held to maturity investments, loans and receivable accounts and financial assets available for sale. On the other hand, US GAAP classifies a financial instrument as an asset or liabilitie through its just value in profit and loss, held to maturity investments and assets available for sale.

Because the adoption of IFRS in Brazil was inevitable, since IAS/IFRS are fast becoming the reporting language of the world, there is a great similarity between IFRS and BR GAAP.

31

It is the conclusion of this work that both brazilian norms and IFRS determine that all financial instruments are to be classified in the following reporting fashion: in the initial recognition they are accounted to just value through results; in the initial recognition as financial instruments are measured initially by just value, and by this causing the following measurement to account for loans and receivables, while instruments kept until due date are measure by amortization cost.

The US GAAP norms for initial recognition state that corporations are free to recognize just value through results; in turn in the initial measurement they are measured by cost with the exception of derivatives and assets available for sale as well as just value through results.

However, special rules are applied for certain loans adquired with quality credit deterioration; the assets available for sale are recognized by just value. Unrealized gains and losses are included(output tax) in the net assets in other results. The total or pacial gain when holding unrealised and the loss of bonds available for sale which is designated as covered in just value is recognized in the results during the covered period. Realised Gains and losses are reported in results.

6.1 Limitations

This work was conditioned by the overall lack of information on the subject matter deriving from the norms which are not fully developed or are in a state of enforcement. The subject matter is also very complex in its nature, since the norms vary slightly from regulator to regulator or from one country’s interpretation to the other.

6.2 Recommendations

When finishing a work of this sort, it is important to assess which aspects were beneficial to its construction and those who had a less positive effect. The main recommendation for future studies is centered on the use of financial instruments around the world and their impact on the respective market evaluations by the regulators.

32

Bibliographic references

Ball, R. (2006), “International Financial Reporting Standards (IFRS): Pros and cons for investors”, Routledge, 36 Edição

César Ramos, Instrumentos Financeiros. Introdução às regras de mensuração, contabilização e divulgação. Editora César Ramos, São Paulo, 1a Edição, Outubro 2014

Calixto, L. (2010), “Análise das Pesquisas com Foco nos Impactos da Adoção do IFRS em Países Europeus, Revista Contabilidade Vista & Revista, 21(1): 157-187, ISSN 0103-734X Ferreira; Domingos (2011), “Instrumentos Financeiros, Normas Internacionais de Relato Financeiro ”, Rei dos Livros, 1ª Edição.

LIMA, I. G. Índice de Conformidade de Evidenciação (ICE): Uma aplicação. 2010. 133 f. Dissertação (Mestrado em Ciências Contábeis). Fundação Escola de Comércio Álvares Penteado – FECAP. São Paulo, 2010.

Rodrigues, J. (2011), “SNC – Sistema de Normalização Contabilística – Explicado”, Porto Editora, 2ª Edição.

Silva, F.; Couto, G.; Cordeiro, R (2009), “Measuring the Impact of International Financial Reporting Standards (IFRS) in Firm Reporting: The Case of Portugal, Universo Contábil, 5(1): 130-144

Shamrock, Steven E. (2012), IFRS and US GAAP a comprehensive comparasion, WILEY John Wiley & Sons, Inc.

Volcker, P. (2002). Prepared Statement of Paul Volker (Tweedie and Volker testify to US Congress). February 14, 2002.

33

International Financial Reporting Standards, available at

http://www.ifrs.org/IFRSs/IFRStechnicalsummaries/Documents/Portuguese%20Web%20Sum maries%202013/IFRS%209.pdf;

Financial Accounting Standards Board, available at

http://www.fasb.org/jsp/FASB/Document_C/DocumentPage?cid=1218220125231&acceptedDi sclaimer=true

Comitê de Pronunciamentos contábeis available at,

http://static.cpc.mediagroup.com.br/Documentos/228_Sumario_CPC_14.pdf

Ernst and Young, available at

http://www.ey.com/Publication/vwLUAssets/An%C3%A1lises_sobre_IFRS_no_Brasil/$FILE/EY _Fipecafi_2013_Web.pdf