Brazil. J. Polit. Econ. vol.31 número5

Texto

Imagem

Documentos relacionados

The general objective of the workshop was to analyze the repeated financial crises in middle income developing countries and 2008 global financial crisis, and to evaluate

Given the central role of financial governance in the discussion, the content of Phase 2 evolved to- wards a second workshop to be held in São Paulo (March 10-11, 2011), that will

However, in contrast to previous episodes of international liquidity constraint, in 2008-2009 the Brazilian government was able to offset part of the liquidity constraint in foreign

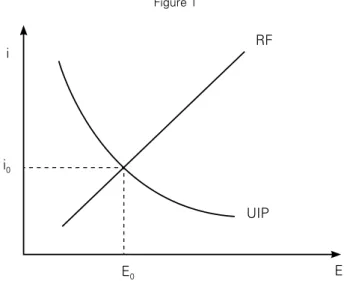

These notes deals with Brazil’s episode in which the expectation of a sustained appreciation of the currency has led to investment banks selling struc- tured derivative product

During this time, the Central Bank implemented prudential measures related to market risks, particularly with respect to currency mismatches in banks’ balance sheets, as well

Private banks, in spite of having reached a high degree of concentration, re- mained attached to the short term financing and only get involved in long term financing when public

First, the fact that 1995 banking distress did not cause a banking crisis as it was the case of Argentina and Mexico, so that the domestic private banks that survived such

On the other hand, according to Prates and Cintra (2009), the international financial crisis generated mechanisms by which it was transmitted to the Brazilian economy, including: