Revista

de

Administração

http://rausp.usp.br/ RevistadeAdministração52(2017)120–133

Marketing

Pricing

strategies

and

levels

and

their

impact

on

corporate

profitability

Estratégias

e

níveis

de

pre¸cos

e

seus

impactos

sobre

a

lucratividade

das

empresas

Estrategias

y

niveles

de

precios

y

su

impacto

en

la

rentabilidad

de

las

empresas

Deonir

De

Toni

a,∗,

Gabriel

Sperandio

Milan

b,

Evandro

Busata

Saciloto

b,

Fabiano

Larentis

aaUniversidadeCaxiasdoSul,BentoGon¸calves,RS,Brazil bUniversidadeCaxiasdoSul,CaxiasdoSul,RS,Brazil

Received13October2015;accepted13June2016 Availableonline30December2016 ScientificEditor:FilipeQuevedo-Silva

Abstract

Pricepolicydefinitionisoneofthemostimportantdecisionsinmanagementasitaffectscorporateprofitabilityandmarketcompetitiveness.Despite theimportancethatpricestakeinorganizations,itappearsthatthiselementhasnotreceivedproperattentionbymanyacademicsandmarketers sinceitrepresents,accordingtoestimates,lessthan2%ofthepapersonleadingjournalsinthefield.Thus,theaimofthisstudywastoproposeand testatheoreticalmodelshowingtheimpactsofpricingpolicyoncorporateprofitability.Tothisend,150companiesinthemetal-mechanicsector situatedintheNortheastofRioGrandedoSulState,Brazilwerestudied,integratingcustomervalue-basedpricingstrategies,competition-based pricingstrategiesandcost-basedpricingstrategieswithpricelevels(highandlow)andperformancewithrespecttoprofitability.Theresultsindicate thattheprofitabilityofthesurveyedcompaniesispositivelyaffectedbyvalue-basedpricingstrategyandhighpricelevelswhileitisnegatively affectedbylowpricelevels.Suchfindingsindicatethatpricingpoliciesinfluencetheprofitabilityoforganizationsandtherefore,amorestrategic lookatthepricingprocessmayconstituteoneaspectthatcannotbeoverlookedbymanagers.

©2016DepartamentodeAdministrac¸˜ao,FaculdadedeEconomia,Administrac¸˜aoeContabilidadedaUniversidadedeS˜aoPaulo–FEA/USP. PublishedbyElsevierEditoraLtda.ThisisanopenaccessarticleundertheCCBYlicense(http://creativecommons.org/licenses/by/4.0/).

Keywords: Prices;Pricing;Pricingpolicy;Pricestrategies;Businessperformance

Resumo

Adefinic¸ão dapolítica deprec¸osé umadasmais importantesdecisõesnoâmbito dagestão,pois afetaalucratividadedas empresasesua competitividadenomercado.Apesardaimportânciaqueoprec¸oassumenasorganizac¸ões,parecequetalelementonãotemrecebidoadevida atenc¸ãodemuitosacadêmicoseprofissionaisdemarketing,porrepresentarmenosde2%dosartigosdasprincipaisrevistasdaárea,segundo estimativas.Destaforma,oobjetivodesteestudofoiodeproporetestarummodeloteóricoqueindiqueosimpactosdapolíticadeprec¸ossobre alucratividadedasempresas.Paratanto,foramestudadas150empresasdopolometal-mecânicosituadasnaregiãoNordestedoEstadodoRio GrandedoSul,Brasil,integrando-seasestratégiasdeprec¸osbaseadasemvalorparaocliente,naconcorrênciaeemcustoscomosníveis(altos ebaixos)deprec¸ospraticadoseoseudesempenhonoqueserefereàlucratividade.Osresultadosindicamquealucratividadedasempresas estudadaséafetadapositivamentepelaestratégiadeprec¸osbaseadaemvaloreníveisaltosdeprec¸oenegativamentepelosníveisbaixosdeprec¸o. Taisachadossinalizamqueaspolíticasdeprec¸ossãoimpactantesnalucratividadedasorganizac¸õeseque,portanto,umolharmaisestratégico paraoprocessodeformac¸ãodeprec¸osconstituiumaspectoquenãopodesernegligenciadopelosgestores.

©2016DepartamentodeAdministrac¸˜ao,FaculdadedeEconomia,Administrac¸˜aoeContabilidadedaUniversidadedeS˜aoPaulo–FEA/USP. PublicadoporElsevierEditoraLtda.Este ´eumartigoOpenAccesssobumalicenc¸aCCBY(http://creativecommons.org/licenses/by/4.0/).

Palavras-chave: Prec¸os;Precificac¸ão;Políticadeprec¸os;Estratégiasdeprec¸o;Desempenhodasempresas

∗Correspondingauthorat:AlamedaJoãoDalSasso,800,CEP95700-000,BentoGonc¸alves,RS,Brazil. E-mail:[email protected](D.DeToni).

PeerReviewundertheresponsibilityofDepartamentodeAdministrac¸ão,FaculdadedeEconomia,Administrac¸ãoeContabilidadedaUniversidadede SãoPaulo–FEA/USP.

http://dx.doi.org/10.1016/j.rausp.2016.12.004

Resumen

Ladefinicióndelapolíticadepreciosesunadelasdecisionesmásimportantesenlagestión,yaqueafectaalarentabilidaddelasempresasy sucompetitividadenelmercado.Apesardelaimportanciaqueelpreciotieneenlasorganizaciones,parecequeesteelementonoharecibidola debidaatencióndemuchosacadémicosyprofesionalesdemarketing,dadoqueeltemaapareceenmenosdel2%delosartículosdelasprincipales revistasdelárea,segúnestimaciones.Elobjetivoenesteestudioesproponeryponerapruebaunmodeloteóricoqueindiquelosimpactosdela políticadepreciosenlarentabilidaddelasempresas.Paraello,sehanestudiado150empresasdelparqueindustrialmetalmecánicoubicadoen laregiónnordestedelestadodeRioGrandedoSul,Brasil,ysehanintegradolasestrategiasdefijacióndepreciosconbaseenelvalorparael cliente,enlacompetenciayenloscostosconlosnivelesdeprecios(altosybajos)ysudesempe˜noconrespectoalarentabilidad.Losresultados indicanquelarentabilidaddelasempresasesafectadapositivamenteporlaestrategiadepreciosbasadaenelvalorynivelesdepreciosaltos, ynegativamenteporlosnivelesdepreciosbajos.Loshallazgosindicanquelaspolíticasdepreciosproducenefectosenlarentabilidaddelas organizacionesyque,porlotanto,unamiradamásestratégicaalprocesodefijacióndepreciosconstituyeunaspectoquelosadministradoresno puedendejardetenerencuenta.

©2016DepartamentodeAdministrac¸˜ao,FaculdadedeEconomia,Administrac¸˜aoeContabilidadedaUniversidadedeS˜aoPaulo–FEA/USP. PublicadoporElsevierEditoraLtda.Esteesunart´ıculoOpenAccessbajolalicenciaCCBY(http://creativecommons.org/licenses/by/4.0/).

Palabrasclave: Precios;Fijacióndeprecios;Políticadeprecios;Estrategiasdeprecios;Desempe˜nodelasempresas

Introduction

Priceisoneofthemostflexibleelementsofthemarketing mix,whichinterferesdirectlyandinashorttermoverthe profit-abilityandcosteffectivenessofacompany(Simon,Bilstein,&

Luby,2008).Despitetheimportanceapricehasonthe

perfor-manceofbusinesses,itseemsthatsuchelementhasnotreceived theproperattentionbymanyacademicsandmarketing profes-sionals(Avlonitis&Indounas,2006).Typically,inmarketing, themainfocusisplacedonthedevelopmentofnewproducts, distributionchannelsandcommunicationstrategies,and

accord-ingtoLancioni (2005)thiscould leadtoprecipitatedpricing

decisionswithoutproperlyevaluatingmarketandcostfactors. Thus,pricingistreatedasthesimpleststrategywithin market-ing,perhaps because manycompanies determinetheir prices basedonintuitionandthemanager’smarketexperience(Simon, 1992).Inaddition,onlyfewmanagersstrategicallythinkabout pricingwhileproactivelyadministratingtheirpricesinorderto createfavorableconditionsthatleadtoprofits(Nagle&Holden, 2003).Consideringthis,LiozuandHinterhuber(2012)highlight theneedformoreresearchregardingthepricingpreferencesand practicesbecause,accordingtotheauthors,lessthan2%ofall publishedarticlesinmarketingjournalsarefocusedonpricing. Strategic pricing requires a stronger relationship between marketingandtheothersectorsofacompany.Inordertoenhance companies’ economic and financial performance, the pricing policies shouldbedefined bytheir internalcapacitiesandon the basic systematical understandingof needs andwishes of theircustomers,inadditiontomarketconditionssuchas, eco-nomicconditionsanddegreeofcompetition(Besanko,Dranove,

Shanley,&Schaefer,2012;DeToni&Mazzon,2013b).Inthis

context,thisstudy’sobjectivewastoproposeandtesta theo-reticalmodelthat indicatestheimpacts ofpricing policieson company’sprofit. Onthis regard,the theoreticalassumptions consideraspricingpoliciesthedefinitionsthatcomprisethe pri-cingstrategiesandthepricelevelsusedbycompaniesintheir respectivemarkets.

In this study, the considered pricing strategies are based

on Nagle and Holden (2003) studies, namely value-based,

competition-based andcost-based pricing strategies; whereas thepricinglevelsareclassifiedashighandlowprices(Urdan&

Osaku,2005).Besidesidentifyingthedirecteffectsofthese

ele-mentsoverprofitability,thisresearchalsoanalyzedtheimpacts ofmoderatingeffects consideringsomeindependentvariables onthebusinessprofitability(dependentvariable).

Itisimportanttomentionthatthisstudywasperformedon 150metal-mechaniccompaniessituatedintheNortheastofRio GrandedoSulState,Brazil,alsocallregionofSerraGaúcha, alongwiththepeopleresponsiblefortheircompanies’pricing process.By usingahierarchicalregressionanalysis,we were abletotestthemainmodelandtheinteractionmodelsagainst ourproposed hypothesis,whichwill be presentedthroughout thisproject.

Theoreticalbackground

Pricingstrategies

According to Monroe (2003), price decisions are one of themostimportantdecisionsofmanagementbecauseitaffects profitability andthe companies’ returnalong with their mar-ketcompetitiveness.Thus,thetaskofdevelopinganddefining prices is complex and challenging, because the managers involvedinthisprocessmustunderstandhowtheircustomers perceivetheprices, howtodevelopthe perceivedvalue,what aretheintrinsicandrelevantcoststocomplywiththisnecessity, aswellasconsiderthepricingobjectivesofthecompanyand their competitivepositioninthe market(De Toni&Mazzon,

2013a,b;Hinterhuber&Liozu,2014;Monroe,2003).

In this way, Nagle and Hogan (2007) argue that

not only does it depend on the perceived value, but also depends on the prices set by the leading competitors. Con-sequently, mistaken or inexistent pricing policies could lead buyersto increasethe volumeof information while allowing themtoaugmenttheirbargainingpowerthusforcingprice reduc-tionsanddiscounts.Thedifferencebetweenconventionalprice settingandstrategicpricingconsistsonsettingpricesby reac-ting to the market conditions or managing them proactively, being their sole purpose to exert the most profitable pricing by generating more value for customers without the obliga-tionofincreasingthebusiness’salesvolume(Nagle&Holden,

2003)

Logically,thereisnotauniquewayfordefiningprices.Before settingaprice,thecompanymustdecidewhatisgoingtobethe strategyfortheproductinadditiontowhatwillbetheproposed objectives,sincetheclearerthesedecisions,theeasieritwillbe toestablishprices(Hinterhuber&Liozu,2013).

AccordingtoHinterhuber(2008),priceshaveahighimpact on companies’ profitability, and pricing strategies vary con-siderablybetweensectors andmarket situations.Nonetheless, researchersmostlyagreethatpricingstrategiescanbe catego-rizedinthreebiggroups:cost-basedpricing,competition-based pricing and customer value-based pricing (Nagle & Holden,

2003).

NagleandHolden(2003)arguethattheremustbeabalanced

considerationofinformation,perceptionandintrinsicbehavior ofthe3C’softhisprocess(Cost,CompetitionandCustomers)as awaytoreachtheoptimalprice.Themanagementofsuch infor-mationisacrucialfactorforthesuccessofthepricingdefinition strategy and the price settlement. In some cases, these prac-ticeshavealsobeendesignatedaspricingmethods(Avlonitis,

Indounas,&Gounaris,2005).

Customervalue-basedpricingstrategy

Valueestablishmentcanbedefinedastheofferofbenefitsof equalorsuperiorvaluetothesacrificesincurredbythepurchaser foraproductand/orservice.Withinthepossiblesacrifices,there isthefinancialsacrifice,whichistranslatedbythepricetobe chargedoractuallypaidbythebuyer(Juran&DeFeo,2010;

Porter, 1986; Zeithaml, 1988).Besides, the process of value

settlement includesthetransformation ofthe resultsfromthe organizationalstrategyonprogramsaimedtoextractanddeliver valuetothecompany’scustomers.Inaddition,itidentifiesthe benefits andcosts (or sacrifices)of products andexperiences resultingfromtherelationshipbetweenthecustomersandthe organization.Thesuperiorvalueproposalrepresentsanofferfor thecustomerswhichincreasesthevalueorsolvesaproblemin abetterwaythanthoseofferedbysimilarcompetitors(Payne&

Frow,2014).

Perceivedvalue-basedpricingisapricingpracticeinwhich themanagerstakedecisionsbasedontheperceptionofbenefits fromtheitembeingofferedtothecustomerandhowthese bene-fitsareperceivedandweightedbythecustomersinrelationship to the price they pay (Ingenbleek, Frambach, & Verhallen, 2010). Therefore, as a cultural orientation of businesses, value-basedpricingisderivedfromasetofroutinephilosophies

and organizational strategies that a specific company could useinordertofocusoncustomersatisfactionand,asaresult, increasestheirprofitability(Cressman,2012).Becauseofthis,

Liozu(2013)highlightsthatusingpricesbasedoncustomer’s

perceptionofvalueisamoremodernpricingapproach,although sometimes it incitesaprofoundorganizational changeon the established organizational structure, the current corporate structureorthepre-existingprocessesandsystems.

In this sense, Ingenbleek, Debruyne, Frambach, and

Verhallen (2003) affirm that perceived value-based pricing,

alongwithpricingpracticesthatrefertotheuseofinformation aboutcostsandcompetitors’prices,areintimatelyrelatedtothe product’sperformance,theserviceandthebusinessasawhole. Theseauthorsdemonstratedthattheusageofvalue-based pri-cingisakeypricingpracticeforobtaininglargerreturnsandfor creatingsomekindofcomparativeadvantageforthecompanies offers.ThiswasdemonstratedinastudyconductedbyFüreder,

Maier, and Yaramova (2014), on medium-sized companies

in Austria which used with higher frequency the perceived value-basedpricingstrategy.Theseauthorsidentifiedthatthese companieshadlargercontributionmargins,between11–30%, against 0–10%of thosecompaniesthatdidnot usethissame strategy.Thus,theapproachof avalue-based pricingstrategy is considered superior to other approaches in relationship to the results obtained by other companies (Hinterhuber,

2004; Ingenbleek et al., 2003; Liozu & Hinterhuber,

2013). Therefore, we propose the following research hypothesis:

H1a. Adoptingavalue-basedpricingstrategyhasadirectand positiveimpactonprofitmargin.

The constantchangesinthe market,influencedby techno-logical advances andby increasing change inthe customers’ expectations,areleadingorganizationstoconstantlysearchfor newproductsinordertocontinuebeingprofitableand compet-itive(Boehe,Milan,&DeToni,2009;Cooper,2000).

Theinnovationanddevelopmentof newproductsareways of addingvaluetothe productsor serviceswhile differentiat-ingthemfromtheir competitors,thusprovidingbetterresults. Therefore, in orderfor a business to maintain itself as com-petitive andprofitableinthemarket, thedevelopmentof new products (DNP), and the innovation of their products and processesarefundamentalfactorsforanorganization’s perfor-mance(Cooper&Kleinschmdt,1987).Thus,anewproductthat grantsvaluetothecustomer,duetoitsquality,costreductionor innovationconstitutesacompetitiveadvantagecontributingto abetterperformanceoftheorganization.

InastudydevelopedbyMilan,DeToni,Larentis,andGava

(2013) about pricing and expenditure strategies, the authors

which adopts a constant innovative strategy, mainly on the products released on the market, can add more value to the customerand, consequently,obtain betterprofitability(Boehe

etal.,2009;DeToni,Milan,andReginato,2011).Considering

this,weformulatedthefollowingresearchhypothesis:

H1b. Levelofdevelopmentofnewproducts(DNP)moderates therelationshipbetweencustomervalue-basedpricingstrategy andprofit margin, and such relationship is stronger in those companieswhichlaunchmoreproductsintothemarket.

Competition-basedpricingstrategy

Competition-basedpricingusesaskeyinformationthe com-petitors’pricelevels,aswellasbehaviorexpectations,observed inrealcompetitorsand/orpotentialprimarysourcestodetermine adequatepricinglevelstobepracticedbythecompany(Liozu

&Hinterhuber,2012).Themainadvantageofthisapproachis

consideringtheactualpricingsituationofthecompetitors,and itsmaindisadvantageisthatthedemandrelatedaspectsarenot considered.Furthermore,astrongcompetitivefocusamongthe competitorscanincreasetheriskofstartingapricewaramong competitorsinthemarket(Heil&Helsen,2001).

Liozu,Boland, Hinterhuber, and Perelli (2011) conducted

aresearchmappingthepricingprocessesofcompanieswhich based their prices on competitors and they found that man-agers use their knowledge and experiences to define prices, as well as models of costs, contribution margin goals, and well-structuredprofitgoals.Inaddition,thesecompanieswere stronglyconsideringthepricesoftheirmaincompetitorswhile addingapricerewardbyalwayssharingthedecisionbasedon themanager’sintuition,whichisnotascientificmethodtodefine prices.

Inthissense,competition-basedpricingstrategies arevery dangerousbecausethecompanydoesnoteffectivelyhaveclear cost or profit information from its competitor who, in some instances,may be workingwith very low margins (Nagle &

Holden,2003).Insomesituations,thecompetitordevelopeda

moreefficientproductionprocess,thusthecostswouldnotbe equivalent,evenbecauseofthescalegains.Therefore,by fol-lowingthisstrategy,the companyis atriskof operating with minimalmarginsorevenhavingnegativeprofits.Pricing reduc-tionstrategiesbasedoncompetition,inwhichcompaniesmay seektoincreasethevolumeofsales,canalsoencouragethe com-petitorstolowertheirpriceswhilecontributingtoapredatory competitionandapricewar,resultinginreducedprofitmargins andsmallercompanies’profitability(Diamantopoulos,2005).

Besides,inhighlycompetitivemarkets,thepriceinformation fromcompetitorsbecomes obsoletevery quickly(Ingenbleek etal.,2010).Inthiscase,itisnecessarytomanagethecapacity thatcompetitorshavetoreacttothepricingstrategydefinedby thecompany,whilenotingthatincompetitivemarketsthiscan increasetheriskofstartingapricewaranddecreasingprofit

mar-gins(Simonetal.,2008).Therefore,wepresentthefollowing

researchhypothesis:

H2. Adoptingacompetition-basedpricingstrategyhasadirect andnegativeimpactonprofitmargin.

Cost-basedpricingstrategy

Cost-based pricingisthemost simpleandpopularmethod for settingprices.Historically, itisthe mostcommonpricing strategybecauseitcarriesasenseoffinancialprudence(Simon etal.,2008).Thisinvolvesaddingaprofitmarginoncosts,such asaddingastandardpercentagecontributionmargintothe prod-uctsandservices.First,thesaleslevel(revenue)isdetermined, and thenthe unit andtotal costs are calculated, followed by checkingthecompany’sprofitobjectivesandfinallyestablishing theprices.Thus,fortheprofessionalsinvolvedinthisprocess,it isnecessarytoshowtocustomersenoughvalueonproductsand commercialized servicesinordertojustifythepricescharged bythecompany(Urdan,2005).

AccordingtoastudybyGuilding,Drury,andTayles(2005)

in187companiesintheUnitedKingdomandin90companies inAustralia,threefactorsthat caninterferewithacost-based strategywereidentified:(i)intensityofcompetition:inahighly competitivemarket,theintensityofcompetitionmayresultin a loss of contribution andprofit margins dueto the pressure toequaltheirpricestothecompetition,whichturnscostsina highlyrelevantelementsinceitprovidesthelimitsofpricesto becharged;(ii)companysize:largercompanieshaveagreater capacityofinfluencingprices,becausetheyhavethepropensity toact asaguideforthepricerangesprevailinginthemarket, evenbecausetheyfrequentlyhavescalegains;and(iii)typeof industries:manufacturingindustrieshavehigherexpensesdue totheirhighinvestmentsonphysicalfacilitiesandonresources used inmanufacturing processes, which makes it difficult to accuratelydefinetheindividualcostsofproductsandpotentially forceanincreaseonthetotalcost.

Similarly,astudyof84companiesperformedbyMilanetal.

(2013)showedthatinthesecompaniesthereisagreaterfocus

onpricesettingbasedoncosts.Thus,thisstrategyencourages companiestousebetterexpendituretechniques.

Inaddition,Liozuetal.(2011)conductedastudyonfifteen small andmedium-size Americancompaniesby interviewing forty-fouroftheirmanagers.Insuchstudy,theyaddressedthe threemainpricingstrategies:customervalue-basedpricing(in four companies), cost-based pricing (in six companies) and competition-basedpricing(infivecompanies).Theyidentified thatthemajorityofthecompaniesbasingtheirpricesoncosts developedadvancedcostmodels,allofwhichusedcontribution andprofitmargingoalsinordertosettheirprices.Inthismatter, thefollowingresearchhypothesisisproposed:

H3a. Adoptingacost-basedpricingstrategyhasadirectand positiveimpactonprofitmargin.

Among these alternatives, the import of raw materials and supplies has emerged as a strategy for cost reduction and, consequently,fortheimprovementoftheprofitmargins(Boehe etal.,2009).Hence,itisassumedthattherelationshipbetween the cost-based pricing strategy and the profit margin could be strongerat the companies that operatewith importedraw materialsandsupplies.Consideringthis,thefollowingresearch hypothesisemerges:

H3b. Import of raw materials and supplies moderates the relationshipbetweencost-basedpricingstrategyandprofit mar-gin,andthisrelationshipwouldbestrongerforcompaniesthat import.

Pricelevels

Accordingto Hinterhuber(2004),the impactof price lev-elsonprofitabilityishigh, whichmeansthat eventheimpact ofsmallincreasesofpriceonprofitsandcorporateprofitability byfarexceedstheimpactofotherleveragesinmanagingbest results.Inhisstudy,itwaspossibletodetectedthata5%increase inaveragesalespricesmayincreasetheearningsbefore inter-estandtaxes(EBIT)by22%,onaverage,comparedtoa12% increaseonthesalesvolumeanda10%costreductionofsold goods,respectively.Inotherwords,ofalltheelementsavailable tomanagers,thepriceiswhathasthelargerimpacton corpo-rateresults,reflectingonrepresentativegains(Kohlia&Surib, 2011).Evidenceof thisnaturesuggeststhatmanagers should abandontherationaleofhavingagreatermarketshareandan

increasedbusinessvolume(sales,revenues)infavorofavision morefocusedtoprofits(Simonetal.,2008).Theresultsindicate thatcompaniesthatpracticeahigherpriceagainstthepriceof theircompetitorsobtaingreaterprofits,whichprobablyisrelated tosuperiorcustomervalue.Thisjustifiesthechargeofhigher pricesand,asaresult,enhancesthebusinessperformance.

AsreportedinastudydevelopedbyMilanetal.(2013), mar-ket penetration-based pricing strategies,meaning the practice oflowerorsmallerprices,presentedasignificantandnegative relationship withthe business performance of the companies investigated.Suchfactcouldbeexplainedbyitsrelationshipsto offeringlowerpricesthanthecompetition.Therefore,lowprices aremorestronglyassociatedwithlowerprofitsandviceversa

(Simonetal.,2008).Thus,weproposethefollowingresearch

hypotheses:

H4. Adoptinghighpricelevelshasadirectandpositiveimpact onprofitmargin.

H5. Adoptinglowpricelevelshasadirectandnegativeimpact onprofitmargin.

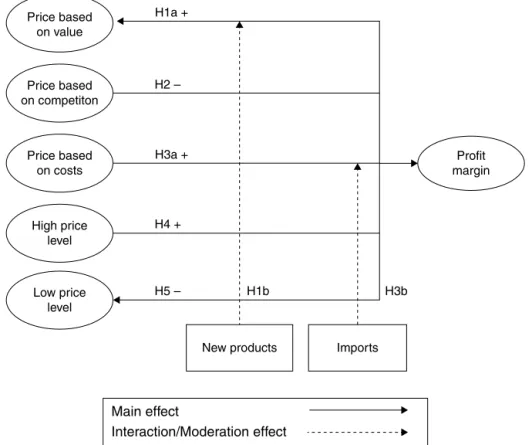

Tofacilitatecomprehension,Fig.1showstheproposed theo-reticalframeworkwhichindicatesthemaineffectsbetweenthe constructsandthetestedinteraction(moderation)effectsalong withtheproposedresearchhypotheses.

Main effect

Interaction/Moderation effect Price based

on value

Price based on competiton

Price based on costs

High price level

Low price level

New products Imports H3b H1b

H5 – H4 + H3a + H2 – H1a +

Profit margin

Fig.1.Proposedtheoreticalframeworkandresearchhypotheses.

Researchmethod

Targetpopulation,sampleanddatacollectionprocedures

The target population, for study purposes, according to SIMECS (Trade Union of Metallurgical, Mechanical and Electric Material Industries of Caxias do Sul) represented approximately 2600 companies totaling around 45 thousand jobsdividedamongthemetal-mechanic,automotiveand elec-tronics sectors. However, service-providing companies were excluded,as,for example,surfacemetal treatmentfirmssuch as galvanizing, painting or those that manufacture products developed by others, which generally hire smaller firms to produce components that eventually would be added to the final product of the other company. It may be cited, as an example, companies linked to the molding sector and some milling companies. After defining these criteria, we reached to a target company population that have their own products and fit the objectives of this study, totaling 730 companies.

The data collection process occurred by a structured sur-veywhichwas validated through apre-test(Malhotra,Birks,

&Wills,2012).Thequestionnaireswereelectronicallysentto

companies.Withtheobjectivetoformalizetherequestto par-ticipateintheresearch,wesentalonganexplanatorytextwhich requestedthatthequestionnairewouldbedirectedtotheperson responsibleofdefiningthepricesofthecompanyortosomeone whoacteddirectlyinthepricingprocess.Withthisapproach,we soughttodirecttheresearchinstrumenttoaresponsibleperson inthecompanywhohadgreatercontrolandrelativeexperience intheanalyzedcontext.

ThedatacollectionwasperformedbetweenJuneandAugust of2014.Inordertoincreasethereturnofrespondents,wesent follow-upmessagesviae-mailinordertoraiseawarenessofthe potentialrespondents.Asforthelargercompaniesonthelist,we madetelephonecallsreinforcingtheresearchrelevanceandthe importanceofobtaining themanager’sperception.Attheend oftheprocess,157questionnaireswereobtained(validcases), havinga21.5%return

Dataanalysisprocess

According to Hair, Black, Babin, Anderson, and Tatham

(2009),theAnalysisofVariance(ANOVA)allowstheresearcher

toconcludethat therearestatisticaldifferencesatsomepoint betweenthegroups’means.Inthisregard,consideringtheneed forposthocanalysis,weoptedtoconducttheTukeyHSDtest, whichismoreaccurate,becauseitgeneratesconfidence inter-valswithloweramplitudefacilitatingthecontroloftypeIerror

rate(Field,2013).

The data were also analyzed by hierarchical regression (OLS),whichresultedinfourmodels.Thefirstonewithonly twocontrolvariables;thesecondonewiththecontrolvariables andtheindependentvariables;andthethirdandfourthmodels withthecontrolvariables,independentvariablesandthe interac-tioneffectsbetweenthecontrolandindependentvariables.Itis importanttonotethatwheninteractioneffectsarecalculated,itis

recommendedtostandardizetheindependentvariables(Jaccard

&Turrisi,2003;Osborne,2014).

Forthisreason,thetransformationofindependentvariables wereperformedonZ-scores.Moreover,wecheckedthepremises ofmultipleregressionanalysis.Withregardtonormaldataon theremainingsampleof150cases(aftereliminatingthemissing valuesanduni-andmultivariateoutliers),wetestedtheassumed univariatenormality(fromthedataskewnessandkurtosis).The univariatenormalityconditionwasmetinallmodelvariables, inwhichthedataasymmetrywasbetween−2.117and1.625,

with an mean value of −0.326. In relation of the amplitude

of kurtosis,itliesat−1.318and7.837,withameanvalueof −0.194.

Thehomoscedasticityconditionwasanalyzedbasedonthe Box’sMtestandtheLevene’stest(Hairetal.,2009).Theresults ofLevene’stestindicatethenon-metricvariables(markettime, numberofemployeesandrevenues)whichshowedsomevisible heteroscedasticityproblem.Theresultsindicatethatthevariable 11(totalcostoftheproduct)andvariable40(numberofactive customers)showheteroscedasticity patterns,whichshouldbe observedwithcaution.However,byhavingatheoreticalsupport

(Urdan,2005)wedecided toretainthesetwovariablesinthe

regressionanalysis.

Thelinearityconditionwasevaluatedbasedona standard-izedresidualsplot(Hairetal., 2009).Through verificationof scatter plots,itwas foundthat the variablesfromthe studied model showlinearrelationships.Finally, themulticollinearity wasanalyzedbythetolerancetest, havingidentifiedthatthey allshowedacceptablelevelswhilesituatingthetolerance lev-elsbetween0.46and0.85withavarianceinflationfactor(VIF) between1.05and2.17,whichindicatesthatthe multicollinear-ityisnotaprobleminrelationtothe selectedvariables(Hair

etal.,2009).

Operationalizationofconstructsandrespectivevariables

The researchquestionnairewas composedof40variables, groupedindimensions,accordingtothetheoreticalmodel pro-posed.ItusedaLikertscaleofsevenpoints,wheretheendswere represented from 1 (totally disregarded/strongly disagree/low performance)to7(fullyconsidered/stronglyagree/high perfor-mance).

Pricingstrategies

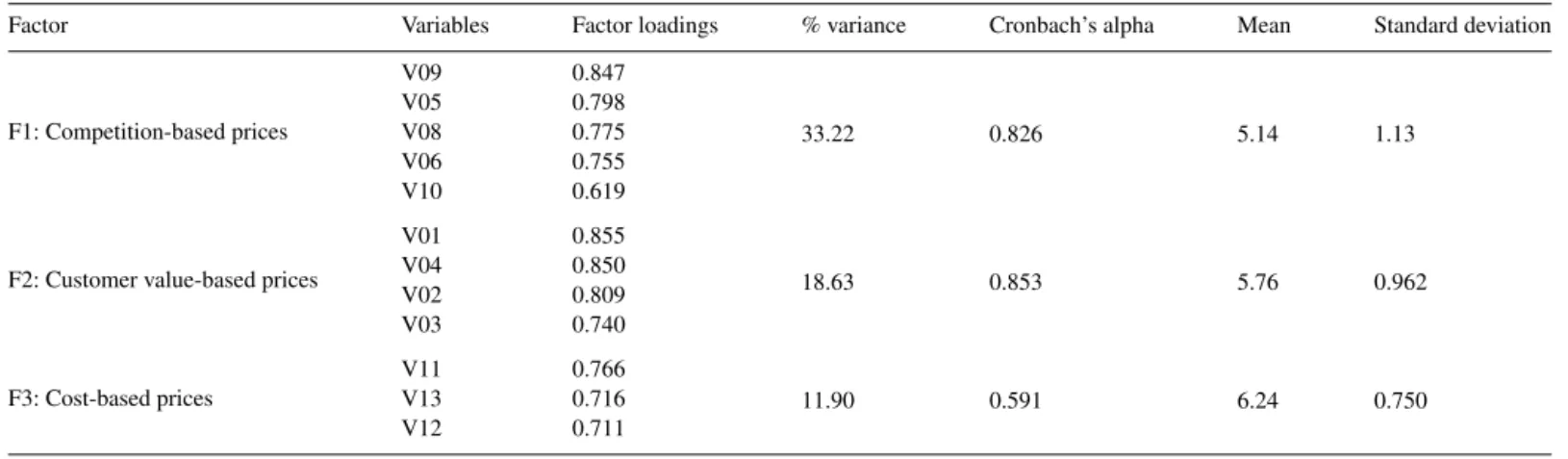

Table1 Pricedefinition.

Factor Variables Factorloadings %variance Cronbach’salpha Mean Standarddeviation

F1:Competition-basedprices

V09 0.847

33.22 0.826 5.14 1.13

V05 0.798 V08 0.775 V06 0.755 V10 0.619

F2:Customervalue-basedprices

V01 0.855

18.63 0.853 5.76 0.962

V04 0.850 V02 0.809 V03 0.740

F3:Cost-basedprices

V11 0.766

11.90 0.591 6.24 0.750

V13 0.716 V12 0.711

Source:Surveydata(2015).

For each factor formed, a newvariable was created from themeanofeachvariablethatintegratesthisfactor.Thus, Fac-tor1 was namedF1:Competition-based Prices,whichwas formedfromthevariablesV9:“Reactionofourcompetitorsto our company’sprices”, V5: “Price of our competitor’s prod-ucts”, V8:“Current pricing strategyof ourcompetitors”,V6: “Degree of competition in the market”, and V10: “Compet-itive advantages of competitors in the market”. The second factorwasnamed F2:CustomerValue-based Prices,which wasformedfromthevariablesV1:“Advantagesthatthe prod-uctofferstothecustomer”,V4:“Perceivedvalueoftheproduct bythecustomers(benefitsversuscosts)”,V2:“Balancebetween theadvantagesoftheproductanditspossibleprice”,andV3: “Advantagesthattheproductoffersincomparisontothe com-petitors’ products”. Finally, the third factor was named F3: Cost-based Prices, composed by the variables V11: “Total cost of the product”, V13: “Profit margin percentage set by thecompanyinrelationtothepriceoftheproduct”,andV12: “Variablecostsoftheproduct”.Table1summarizestheresults obtained.

AccordingtoTable1,whichincludesdatafromFactor Anal-ysis, it is possible to observe that the surveyed companies tend toconsider the costsas the main approachduring their product’sprice settlement process,since the mean registered for F3: Cost-based Prices was of 6.24. The factor F2: Cus-tomerValue-basedPricesremainedasthesecond optionwith amean of 5.76, andthe factorF3: Competition-basedPrices wasconsideredas thethirdoptionwithanmeanof5.14.Itis importanttopointoutthat thethreestrategicapproaches pre-sentedmeanshigherthan5ina7-pointscale,suggestingthat companies tend to consider the three approaches during the price definition process of their products. It is observed that theCronbach’sAlphafor factorF3(Cost-based Prices)stood at0.591,neartheborderzoneof0.60.Evenwithalow confi-denceindexwedecidedtoleavethisconstructinouranalysis, firstly,becauseithasatheoreticalbasethatsupportsit(Nagle

&Holden,2003)and,secondly,becausethevaluesfrom0.60to

0.70areconsideredthelowerlimitofacceptabilitybyHairetal.

(2009).

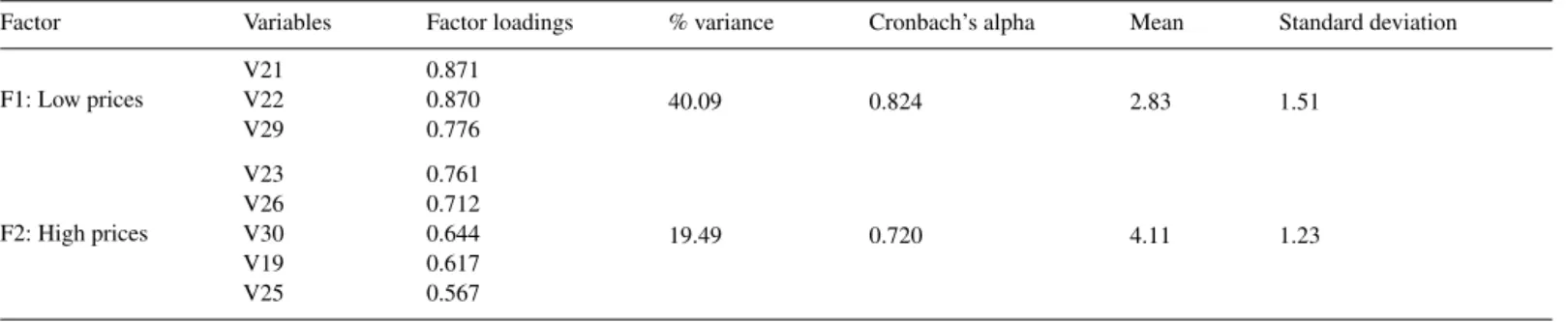

Pricelevels:definingfactorsandvariables

ForHamiltonandChernev(2010),pricelevelperceptionis

generallyexpressedinmonetarylevelsandscales,as,for exam-ple,highpricesversuslowprices.Nevertheless,therearealso manyotherfactorsthatmaynotbedirectlylinkedtotheprices suchas,location,credibility,company’sreputation,comparison withitscompetitorsandothers.Thus,usinganadaptedscaleof

UrdanandOsaku(2005),aFactorAnalysiswasperformedin

whichtwofactorsweredefined:

a) F1:Lowprices,grouping variablesV21: “Wedefinelow pricetoleveragesalesvolumeandtoreducecoststhrough accumulatedexperience”, V22:“We always try tohavea pricelowerthanourcompetitors’pricesinthemarket”,and V29:“Ourpricesarelowinthemarketduetotheinferior qualityofourproductsinrelationtocompetitors”;

b) F2:Highprices,composedbythevariablesV23:“Weoffer ourproductsatahigherpriceonthemostimportantsectors ofthe market andalowerpricebymeans of discountsin lessimportantsectors”,V26:“Forproductsthathave com-plementaryoroptionalitems(suchasaccessories,parts,and services),weput alowerprofit marginonthe basic prod-uct(central)andahigherprofitmarginoncomplementary items(premiumprice)”,V30:“Weofferproductsets(aset of variousproducts) atatotalprice thatallowscustomers tosavemoney,insteadofpurchasingtheproducts individu-ally(separately)”,V19:“Wedefineahighpriceinitiallyand thenwereduceitsystematicallyovertime”,andV25:“Our customerssee thepricesof ourproductsas ahighquality indicator”.

Table2 Pricelevels.

Factor Variables Factorloadings %variance Cronbach’salpha Mean Standarddeviation

F1:Lowprices

V21 0.871

40.09 0.824 2.83 1.51

V22 0.870 V29 0.776

F2:Highprices

V23 0.761

19.49 0.720 4.11 1.23

V26 0.712 V30 0.644 V19 0.617 V25 0.567

Source:Surveydata(2015).

variablesweregenerated fromthe mean of the variablesthat formedeachfactor,soitispossibletonoticethatthesurveyed companiestend toagree more(mean=4.11) on ahighprice strategyandtodisagreeonalowpricestrategy(mean=2.83).

Table2belowsummarizestheseresults.

The fact that companies agree more on the higher price practiceandagreelessonthelowerpricepracticemaybelinked tothemarketcharacteristicsinwhichthesecompaniesoperate. Thus,fortherespondents,definingahigherpricepracticemay signalabetterqualityand,consequently,itleadstobetterprofit marginsfor thecompany. Thismaybe seenwhenanalyzing, singly,V29variable:“Ourpricesarelowinthemarketduetothe inferiorqualityofourproducts...”,sincetheirmeanwas2.08, and132oftheanalyzedcompanies,bymeansoftheinterviewed managers,disagreewiththisaffirmation.Thisnumberof com-paniescorrespondsto86.3%ofthesampleand,amongthem,80 totallydisagree,whichrepresents52%oftheanalyzedsample.

Businessperformance

Regardingthe businessperformance, ananalysis basedon theprofitmarginreportedbythecompanieswasimplemented. Thisvariablewasalso used inthestudy developedby Milan

etal.(2013),whichwasbuiltbasedonthescalesproposedby

Ingenbleeketal.(2003).Theresultsindicatethatthesurveyed

companies’ average net profit is between 5% and 10%, and that25companies(16.4%ofthesample)showedaprofitability above15%.

Finally,weusedtwocontrolvariables.Oneofthemwasthe numberofnewly releasedproducts inthe past2 years(these variablesweretransformedintoalogarithmicscaleduetotheir largedispersion),andtheotherwasifthecompanyimportedor not,measuredfromabinaryvariable(0=itdoesnotimport,and 1=itimports).

Results

Inthissection,wepresentthemainresearchresultsinrelation tothesamplecharacterizationandtotheanalysiscomingfrom thedatacollected.

Sampledescriptionandvarianceanalysis

Ofthe150surveyedcompaniesonthemetal-mechanic indus-try of Serra Gaúcha region, situated in the northeast of Rio

Grande do Sul State, 54.9% of them belong to the metal-mechanic sector, 23.5% belongto the automotive sectorand theremaining21.6%belongtotheelectronicssector.Theyhave ameanof21yearsofexperienceinthemarketand,according toourfindings,39.6%ofthecompanieshave20yearsof expe-riencewhile40% ofthem areonthe rangewith10–20years of experience. The remaining 22.2%have up to 10 yearsof experienceinthemarket.

Whentalkingaboutthenumberofemployees,35.3%ofthe companies haveupto19employees,37.9%havefrom 20to 100employees,andtheremaining26.9%havemorethan100 employees.Abouttheirrevenue,accordingtotheBNDES guide-lines(BrazilianDevelopmentBank),24.2%of thecompanies haveanannualgrossrevenueof2.4million(forthatreasonthey areconsideredmicroenterprises),34.0%haveanannualrevenue ofupto16million(consideredsmallenterprises),25.5%have anannualrevenueof upto90million(beingcharacterizedas medium-sizedenterprises),and,lastly,16.4%ofthecompanies haveanannualrevenueabove90million(beingcharacterized asmedium-largeorlargeenterprises).

Inthequestionnaire,weaskedifthecompanycarried com-mercialactivityonforeignmarketandwefoundoutthat39.9% ofcompaniesexport,andtheseexportsaccountforupto10%of theirannualrevenuein38outof60exportingcompanies.For the remaining 22companies, theseexports account for more than10% of their annual revenue. Wealsoasked abouttheir imports. Overall, 52.3%ofthe companiesmade purchasesin theforeignmarket(imports),andtheremaining47.7%didnot makepurchasesintheforeignmarket.

Regardingthelaunchofnewproducts,34.6%ofcompanies declaredthattheyhadreleaseduptothreenewproductsinthe past2years,28.8%launchedbetweenthreeandtenproducts,and 36.6%declaredhavinglaunchedmorethantenproductswithin thisperiod.Regardingtheprofitmarginofthecompanies,2.7% statedthattheirprofitmarginwasnegative,while55.3%reported havinguptoa10%profitmargin.Theremaining42%declared having a profit margin above 10%. The results are shownin

Table3.

Table3

Profitmarginsofthecompanies.

Netprofitmargin Frequency %

Negativenetprofitmargin 4 2.7

From0%to5% 29 19.3

From5.1%to10% 54 36.0

From10.1to15% 40 26.7

From15.1%to20% 14 9.3

Above20% 9 6.0

Total 150 100

Source:Surveydata(2015).

tothefieldofactivities,revenuesandthefactofimportingor not.

Itisevidentthat companiesonthe electricaland electron-ics industry have a higher profit margin (mean=4.00) than thoseonthemetal-mechanicindustry(mean=3.14;p=0.000) andthoseontheautomotiveindustry(mean=3.14;p=0.042). Two assumptions may emerge from this result, firstly due to the fact that companies in the electrical and electronics industry tend to definetheir prices based on customer value (mean=6.14)morethanthecompaniesinthemetal-mechanic industry(mean=5.54;p=0.005),and,secondly,becauseofthe volumeofnewproductslaunched,consideringthattheelectrical andelectronicsindustrylaunchesmorenewproducts(morethan tenproducts every2 years)thanthe metal-mechanic industry (lessthantennewproductsevery2years,p=0.001).Therefore, thefactsthatthesecompaniesaremoreproactiveinthe devel-opmentofnewproductsandaddmorevaluetotheirproducts, maybejustifywhytheirprofitmarginsarehigher.

Withregardstorevenues,thecompanieswithrevenuesabove R$2,400,000.00haveaprofitmarginhigherthan10%,whilethe companieswithrevenuesbelowthisrangedisplayaprofit mar-ginbelow10%(p=0.007).Thiscanalsobejustifiedbythefact thatthesecompaniesadopted amoreintense customer value-basedpricingstrategy(mean=6.03versus5.50;p=0.000)and that theylaunchedmorenewproductsintheir markets(more thantenproductsevery2years,p=0.000).

Regarding the release of new products, it was found that companiesthatlaunchedmorethantenproductsevery2years displayedahigherprofitmargin(morethan10%)in compari-sontothosethatlaunchedlessthantenproductsevery2years (p=0.002).AccordingtoBoeheetal.(2009),product innova-tionstrategy,competitiveintensityinthemarket,andfunctional integrationamongthevariousareasofthecompanyinfluence significantlythedevelopmentofnewproducts(DNP)andthe performance.Thus,market competitivenessandthe organiza-tionalstrategiesgearedtonewproductsdrivethecompaniesto developmoreproducts,improvingtheprofitmargin.

Asignificantdifferenceintheprofit marginsof companies that import was also noticed.Companies that import show a superiorprofit margin(mean=3.68)when comparedtothose thatdonotimport(mean=3.08,p=0.001).Thefactthatthese companiesimportindicatesthattheyaretryingtoreducetheir costsaswellastheymaybereleasingmorenewproductsin rela-tiontothosethatdonotimport(p=0.001),maybebecausethey

searchfor innovationsintheforeignmarketandtrytolaunch theminthenationalmarket.Inaddition,thegainsassociatedto thestrategyofusingimportedrawmaterialsandsuppliesmay resultinhigherprofitmarginsdependingontheexchangerate appreciation.Similarly,theexchangerateappreciationincreases the exposuretoforeigncompetitors. Therefore,aninnovation strategy allows important distinctions,leading tocompetitive advantages, canadd morecustomer valueand, consequently, thecompanycanachievebetterprofits(Boeheetal.,2009;De

Tonietal.,2011).

Pricingpoliciesandtheirrelationshipwithbusiness performance

BasedontheconstructsofPricingStrategies(customer value-based,competition-based andcost-based) andPriceLevelsin relationtothe competition(higherorlower),it wasidentified thatcost-basedandcompetition-basedpricingstrategiesdidnot showsignificantdifferencesbetweentheirmeanswithregardto the profit margins. On the otherhand, customer value-based pricing strategies showed a significant difference (p=0.000) betweenthemeans.

Forexample, 30companieswithaprofit margin from0% to5%displayeda5.13meanintheusageofcustomer value-basedpricingstrategies,while65companieswithaprofitmargin above10%havea6.15meanwhenusingthisstrategy.This indi-catesthatthegreatertheusageofavalue-basedpricingstrategy, thegreateraretheopportunitiesforthecompaniestoincrease their profit margin. Suchevidenceconfirms the proposal that theusageofacustomervalue-basedpricingstrategyenablesa betterprofitabilityforthecompanies(Nagle&Holden,2003). Similarly, itsuggeststhatcompanieswithahighperformance withregardtonewproductdevelopment(DNP)(morethanten productsevery2years)usemoreacustomervalue-basedpricing strategy(meanHighDNP=6.03versusmeanLowDNP=5.30,

p=0.000)thananyotherpricingstrategies.

Thisfactcouldberelatedtothesearchforabetter understand-ingofthemarket,thusbetterunderstandingthespecificneedsof thecustomers,whodemandamorediversifiedlineofproducts andahigherlevelofquality.Suchresultsaresimilartothoseof

Boeheetal.(2009),whoidentifiedthatcompanieswhichadopt

innovationstrategiesorlaunchalargenumberofproductsinto themarkettendtohavebetterperformance.Theseresultsalso complement the idea suggested by Cooper (2000) that com-panieswithadifferentiationstrategy,withuniquebenefitsand superiorcustomervaluetendtohaveabetterperformanceinthe market.

Table4

Correlationsamongtheconstructs.

Constructs 1 2 3 4 5 6

1Businessperformance(netprofitmargin) 1

2Highprices 0.471** 1

3Lowprices −0.453** −0.362** 1

4Customervalue-basedprices 0.481** 0.401**

−0.425** 1

5Competition-basedprices 0.075 0.205* 0.163* 0.287** 1

6Cost-basedprices 0.116 0.153 −0.219** 0.294** 0.169* 1 Source:Surveydata(2015).

Note:*Significantlevelof10%;**Significantlevelof5%.

Obs.:allvariableswerestandardized(mean=0;standarddeviation=1).

Thesecondfindingisconsistentwiththefirstone,asthereisan increasingandsignificantrelationshipbetweenusinghighprice practiceandhavingabetterprofitmargin.Thegreaterthe utiliza-tionofthispractice,thegreatertheprofitmargin(p=0.000).For example,65companiesthatpracticehighpricesshowaprofit marginabove10%,while85companiesthatusesuchpractice toasmallerextentshowprofitmarginsbelow10%(meanHigh Price=4.75versusmeanLowPrice=3.64,p=0.000).

Likewise, concerning the development of new products (DNP),theresultsindicatethatcompaniesthatusehighprice levels develop more new products (mean High Price=4.11 versusmeanLowPrice=2.83,p=0.000).Forexample,the56 companies whichdeveloped more than ten products every 2 yearsuse,withgreaterintensity,highpricinglevels.Theresults revealsimilaritiestothestudiesbySimonetal.(2008)andMilan

etal.(2013),whichfoundthatcompaniesthatusehighprices

tendtohaveabetterperformancethanthosethat employlow prices.

Whencomparingpricingstrategieswiththeperformanceand itsrelationshipwiththemarketshareofthecompanies,itwas observedthat thecompanies whichadopt highpricesdisplay a larger market share if compared to those which offer low prices(meanHighPrice=4.11versusmeanLowPrice=2.83,

p=0.000).Theseresultsindicatethatpracticinglowpricelevels notalwaysitispossibletoleveragelargermarketshareorlarger salesvolume, because lowpricesmayalso suggestasmaller perceivedlevelofquality(DeToni&Mazzon,2013a;Zeithaml,

1988).

Impactofpricingpoliciesonprofitmarginandits moderatingfactors

Thisstageofthestudyincludedanassessmentthrougha mul-tiplelinearregressionoftherelationshipsbetweenthesetof met-ricexplanatoryvariables,inthiscaserepresentedbythefactors linkedtothepricingstrategyandthechargedpricelevels,which mostinfluencetheprofitabilityoftheanalyzedcompanies.For theoperationalizationoftheanalysis,weusedastepwise multi-pleregression,whichhasasamaincharacteristictheindividual assessmentofeachvariablecontributionbeforedevelopingthe equation.Theindependentvariablewiththegreatest contribu-tion isadded first andthe independent variablesare selected forinclusionbasedontheirincrementalcontributionoverthe variablesalreadypresentintheequation(Hairetal.,2009).

Consideringthis,firstofall,Table4presentsthecorrelations among theconstructs. We pointout the correlationsbetween businessperformanceandhighprices(0.471),business perfor-mance andcustomervalue-based prices(0.481)andbusiness performanceandlowprices(−0.453).

Fortestingthehypotheses,thedatawereanalyzedby hier-archical regression,whichshowsthat byaddingoneor more predictive variablestothe existingregression equation it sig-nificantlyincreasestheexplanationofthevarianceofanalysis criteria(Jaccard&Turrisi,2003;Osborne,2014).Inaddition, theeffectsofinteractionormoderationarepresentedinorderto testH1bandH3bhypotheses,whichidentifythepresenceofa dependentvariable,independentvariable(s),andathirdvariable seenasthemoderator.Therefore,thereisamoderatingeffect whentheeffectoftheindependentvariableoverthedependent variablediffersasafunctionofthemoderatingvariable(Jaccard

&Turrisi,2003;Osborne,2014).

Inthemultipleregressionanalysis,weobservedthatallthe fourmodelstestedweresignificantatthelevelp<0.01,asshown

inTable5.Model1,whichincludesonlytwocontrolvariables

(numberofnewproductslaunchedandifthecompanyimportsor not),explains7.9%(adjustedR-squared)ofthetotalvariance, suggesting how much thetwo variablesinfluence profit mar-gin.Theresultsshowedthattheperformancewithnewproducts andthefactthatthecompanyimportsornothaveasmall par-ticipationonthecompany’sprofitmargin.Besides,morethan 92%ofotherfactorsmayalsoinfluencecompany’sprofitability. Eventhoughthoseitems’participationinprofitabilityislow,the resultsofthesurveyindicate,asseeninthevariancetests,that companieswhichdevelopandlaunchmoreproductsandwhich importhaveahigherprofitmargin.

Model 2 includesthe main effects betweenthe dependent variable,theprofitmargin.Itwasnotedthattheexplained vari-anceissignificantlygreater(R2=35.7%;F=11.96),meaning thattheindependentvariablesaddexplanatoryvaluetothe equa-tion.

Table5

Hierarchicalregressionmodels(dependentvariable:profitmargin).

Constructs Controlvariables Maineffect Interactioneffect Interactioneffect

Model1 Model2 Model3 Model4

Newproductsdevelopment(NPD) 0.170** 0.052

−0.009 −0.006

Imports 0.216** 0.095 0.112 0.110

Customervalue-basedpricestrategy 0.238* 0.475* 0.489*

Competition-basedpricestrategy −0.014 −0.003 0.003

Cost-basedpricestrategy −0.044 −0.076 −0.155

Highprices 0.259* 0.241* 0.236*

Lowprices −0.228* −0.240* −0.247

Customervalue-basedpricestrategyversusNPD −0.287*

−0.291*

Cost-basedpricestrategyversusimports 0.096

Constant 0.569* 0.606* 0.618* 0.618*

AdjustedR2 0.079 0.326 0.348 0.347

R2 0.092 0.357 0.382 0.386

F 11.96* 5.982** 0.834

Source:Surveydata(2015).

Note:*p<0.05;**p<0.01–standardcoefficients.

wasadded(H3b),theinteractionbetweentheindependent vari-able (cost-basedpricing strategy) andthe control variable(if thecompanyimportsornot),doesnotshowasignificanteffect concerningmodel3(R2=38.6%;F=0.834).

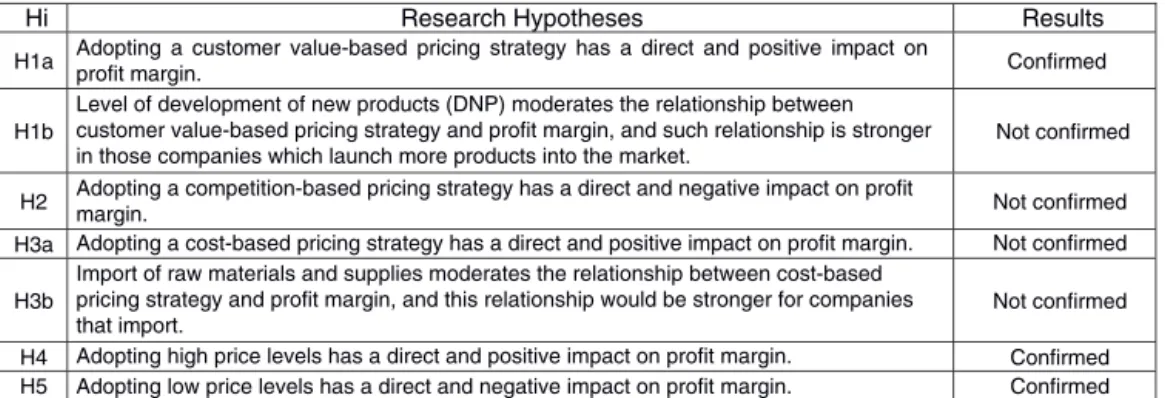

Basedonthehierarchicalregressionanalysis,itwaspossible toproceedtotestthehypothesesofwhichtheresultsareshown

inTable3.Thefirst hypothesis(H1a)proposes thatadopting

a value-based pricing strategy is directly proportional to the profitmarginofthecompany.Giventhatthepositivecoefficient (0.238inmodel2 and0.475inmodel 3)is significantatthe

p<0.01 level, H1a can be accepted. However, H1b was not confirmed,sincetheresultsoftheregressionanalysisshowed contradictory results, because the moderation of the level of release of new products in relation tousing the customer value-based pricing strategy significantly and negatively influencestheprofitmargin.Anyways,asshowninmodel1in

Table5,thedevelopmentofnewproductsimpactssignificantly

the companies’ profit margin, but such strategy needs to be related to other organizational actions that lead to a better performance. H2indicates that thecompetition-based pricing strategydidnotsignificantlyinfluencetheprofitmarginofthe companiesanalyzed(−0.014inmodel2and−0.003inmodel

3),thusrejectingH2.H3aindicatesthatthecost-basedpricing

strategypositivelyinfluencesprofitmargin.Theresultsdidnot confirm thishypothesiswithinthe surveyedsamples (−0.044

inmodel 2 and−0.076inmodel 3), thereforerejectingH3a.

Likewise,H3bwasnotconfirmed,becauseofthefactthatthe company imports did not show any moderation between the cost-basedpricingstrategyandtheprofitmarginofthesurveyed companies(0.096inmodel4).Not beingabletoconfirmthis hypothesiscouldalsoberelatedtothefactthatin2013–2014 therewasa15%declineintheimportsectorinCaxiasdoSul, accordingtothe BrazilianMinistry of Development,Industry and Foreign Trade (MDIC).The imports of raw material for thissectorwereapproximately3%(inR$)ofthegrossrevenue

in 2014 (Brasil, 2016). Basedon thesedata, we believe that

importscouldhavebarelyinterferedonthecostandtheincrease of the profit margins of the surveyed companies during this period.

H4identifiesthatthecompanieswhichsethighprices dis-played asignificant andpositiveimpactonthe profitmargin, thus being confirmed (0.259in model 2 and 0.241in model 3).Likewise,H5wasconfirmedbecausecompanieswhichset lowpricesdisplayedasignificantnegativeimpactontheirprofit margins (−0.228inmodel 2 and−0.240inmodel 3). Fig.2

summarizestheinherentresultsofthetestedhypotheses.

Results Research Hypotheses

Hi

H1a Adopting a customervalue-based pricing strategy has a directand positive impact on

profit margin. Confirmed

H1b

Level of development of new products (DNP) moderates the relationship between customer value-based pricing strategy and profit margin, and such relationship is stronger in those companies which launch more products into the market.

H2 margin. Adopting a competition-based pricing strategy has a direct and negative impact on profit Not confirmed

Not confirmed

Not confirmed Adopting a cost-based pricing strategy has a direct and positive impact on profit margin.

H3a

H3b

Import of raw materials and supplies moderates the relationship between cost-based pricing strategy and profit margin, and this relationship would be stronger for companies that import.

Confirmed Adopting high price levels has a direct and positive impact on profit margin.

H4

Confirmed Adopting low price levels has a direct and negative impact on profit margin.

H5

Not confirmed

Fig.2.Researchhypothesestestresults.

Concludingremarks

Inordertohaveabetterperformancethantheircompetitors, companiesshouldestablishasetofsuperiorresources,suchas, abilities, skillsand knowledge, because the role of the price fixingcapacityasawayofeffectivelyimprovingthecompany’s performanceisvital(Dutta,Zbaracki,&Bergen,2003;Liozu

&Hinterhuber,2013).Therefore,amorestrategicapproachto

thecompanies’pricingprocessexcelsasarelevantelementfor thecompanies’betterperformanceandfortheconstructionofa possiblesourceofcompetitiveadvantage(Hinterhuber&Liozu,

2014).

Theprofitabilityandcosteffectivenessofthecompaniesare highlyattachedtoapricingstrategythatvisualizestheirinternal capacities,skillsandcorporate advantagesagainst their com-petitorswhilealsoconsideringtheircustomer’sneedsor how muchtheyarewillingtopay.Settinglowerpricescould sacri-ficeprofitsbecauseagreatersalesvolumemaynotcompensate foralowerprofitmargin.Higherpricescouldalsosacrifice pro-fitsbecausegreatermarginsperunitmaynotcompensatefora smallersalesvolume(Simonetal.,2008).

Therefore,the resultsofourstudy indicatethatcompanies whichsearch foracustomervalue-basedpricingstrategy and whichsethigh prices, logically within the market context in whichtheyoperate,tendtoyieldagreaterprofitmarginthantheir competitorswhomayadoptacompetition-basedpricingstrategy andsetlowerprices. Another important fact isthat the most innovativecompanies,or thosewholaunch ahigherquantity ofnewproducts,andoperatewithimportedrawmaterialsand suppliesalsoshowahigherprofitmargin.Thisindicatesthatthe highertheusageofvalue-basedpricingstrategies(inwhichthe companyadds moreinnovation launchingnewproducts), the greaterarethepossibilitiesofincreasing thecompany’sprofit margin.

Suchresultsmaybeidentifiedonthehierarchicaltestfrom thehierarchicalregression(seemodel3inTable5),inwhichit isconfirmedthatacustomervalue-basedpricingstrategy,when addedto the interaction effectof newproducts, significantly increasestheexplanationoftheproposedmodel(Fig.1),since theindependentvariablesandthemoderatingvariablesexplain the34.8%variance.

Amongthisstudy’scontributions,wecanlistmainlytwo.The firstreferstotheproposalofthetheoreticalmodelitself,inwhich itisidentifiedthatthestrategiesandpricelevelspracticedhave asignificantimpactonprofitmargin.Suchtheoreticalproposal identifiesthatthepriceexertsapreponderantroleoncompanies’ profitabilityandthattheinteractioneffectscontributetoabetter explanationofthismodel.Thesecondcontributionisrelatedto theresultsofthesurvey,whichshowthatthecustomer value-basedpricing strategyandthe settingofhighpricesenable a betterprofitability.Thiscanbe seenfromtheconfirmation of hypothesesH1a,H4andH5,whichreinforcesthe powerthat avalue-basedpricing strategyandthe highpriceshaveinthe profitabilityoforganizations.

However,hypothesesH2andH3awerenotconfirmed,which meansthatcompetition-basedandcost-basedpricingstrategies did not significantly influence companies’ profitability. It is

observedthatthe cost-basedpricingstrategyisthemostused bythesurveyedcompanies(meanvalue=5.75,mean competi-tion=5.14,andmeancosts=6.24),whichisalsoconfirmedby otherstudies(Liozuetal.,2011).Thesmallcorrelationbetween bothstrategieswiththeprofitmarginmaybeamongthefactors thatmayhavecontributedtothefailuretoconfirmhypotheses

H2 andH3a (Table 1).Likewise, the two proposed

modera-tionswerenotconfirmedtoH1b,sincethedevelopmentofnew products (DNP) moderates the relationship between the cus-tomervaluestrategyandthe profitmarginsofthecompanies, butinanegativeway,andtoH3b,astheimportofraw mate-rial andsupplies does not moderatethe relationshipbetween thecost-basedpricingstrategyandprofitmargin.Nonetheless, thisalsoneedstobeseenasacaveat,sincewedidnotaskin thesurveythecompanies’percentageofimportandhowmuch importeditemsrepresentintheircosts.Futurestudiescanrepeat thesetestsusingthisinformationtotestagainthismoderation, because,accordingtoBoeheetal.(2009),rawmaterialand sup-pliesimportsmaycontributetocostreductionandimprovements oftheorganization’sprofitmargins.

ThefailuretoconfirmtheDNPandimportsmoderating vari-ablesindicatethatacompanies’profitabilityisacomplexand multidimensionalphenomenonandthattherearenumerous vari-ableswhichcanaffectprofitability.Inaddition,thecompanies workingwithlowpricesdonotnecessarilyworkwithlowcosts, interferingnegativelyintheirprofitability.

Itisworthmentioningthat thismayberelatedtoa poten-tiallimitationinourstudy,sincetheprofitmarginofsurveyed companieswasmeasuredbytherespondent’sperception (sub-jectivemetrics)andnotbyinformationdirectlycollectedfrom incomestatements(objectivemetrics).Inaddition,thefactthat Braziliancompaniesobtainfinancialprofitsascompensationfor weakoperationalresults,sincedebtsandtaxesmayalsodistort theresults.Werecommend,forfuturestudies,usingEBITDA insteadofaprofitmargin.

Anotheraspectthatundergoes thesameeffectisrelatedto thepricelevelspracticedbythecompanies(highandlowprices) sinceit isknown thatbusinessesalso operateinintermediate levelsorthattheyaccompanythecompetitors’prices.Therefore, infuturestudies,the usageor notofintermediatepricelevels couldbemeasuredandtheimpactoftheseonthecompanies’ performancecouldbeverified.

Inthisstudy’scase,wemeasuredtheperformancebyonly onevariable,theprofitmargin.Nevertheless,itisknownthatthe performanceofanorganizationcanbemeasuredbymanyother variables,suchasfixedassets,customersatisfaction,cost effec-tivenessandothers(Ingenbleeketal., 2003;Urdan&Osaku, 2005).In thismanner,future studiescould usedifferent per-formancevariablesandchecktheirdifferentimpactsassociated topricingstrategiesandpricelevelspracticed(Hinterhuber&

Liozu,2014;Ingenbleek&VanDerLans,2013).

on performance betweencompanies. Moreover, further stud-ies regardingthe pricing processes of smaller businessesare appropriatebecausetheremaybeaninfluencebylarger com-panieswithgreaterbargainingpower,influencingthemethods, thestrategiesandthepricinglevelspracticedbythem.

Pricing strategies may be seen as a complex activity that requiresagood understandingofthe internalstructure ofthe company,agoodknowledgeofthemarket,andagood knowl-edgeofthediversevariablesthatcompriseitandtheirinterfaces

(Milanetal., 2013).Theprice isconsideredoneof the most

impacting elements in companies’ performance. The results foundindicatetheimportanceofmaintaining thefocusofthe pricing on the current and potential customers and not only oncompetitors.Thereby,thedifferentiationwhetherfromnew productsand/or servicesandthevaluedeliveredtocustomers provides amoreeffective waytopractice bestpricing strate-gies,whichwillhaveapositiveimpactoncompanies’profitand competitiveness(Davcik&Sharma,2015).

Conflictsofinterest

Theauthorsdeclarenoconflictsofinterest.

References

Avlonitis,G.,Indounas,K.A.,&Gounaris,S.P.(2005).Pricingobjectives overtheservicelifecycle:Someempiricalevidence.EuropeanJournalof Marketing,39(5/6),696–714.

Avlonitis,G.,&Indounas,K.A.(2006).Pricingpracticesofservice organiza-tions.JournalofServiceMarketing,20(5),346–356.

Besanko,D.,Dranove,D.,Shanley,M.,&Schaefer,S.(2012).Aeconomiada estratégia(5thed.).PortoAlegre:Bookman.

Brasil.(2016).MinistériodoDesenvolvimento,IndústriaeComércio Exte-rior.Secretariade ComércioExterior.In Balan¸caComercialBrasileira porMunicípio.. RetrievedMay 31,2016.http://www.mdic.gov.br//sitio/ sistema/balanca/

Boehe,D.M.,Milan,G.S.,&DeToni,D.(2009).Desempenhodoprocesso dedesenvolvimentodenovosprodutos:opesorelativodefatores organiza-cionais,mercadológicoseoperacionais.RAUSP–RevistadeAdministra¸cão,

44(3),250–264.

Cooper,R.G.(2000).Winningwithnewproducts:Doitright.IveyBusiness Journal,64(6),54–60.

Cooper,R.G.,&Kleinschmdt,E.J.(1987).Newproducts:Whatseparates winnersfromlosers?TheJournalofProductInnovationManagement,4(3), 169–184.

Cressman,G.E.,Jr.(2012).Value-basedpricing:Astate-of-the-artreview.In G.Lilien,&R.Grewal(Eds.),Handbookonbusinesstobusinessmarketing. Massachusetts:EdwardElgarPublishing.

Davcik,N.S.,&Sharma,P.(2015).Impactofproductdifferentiation, mar-ketinginvestmentsandbrandequityonpricingstrategies:Abrandlevel investigation.EuropeanJournalofMarketing,49(5/6),760–781.

DeToni,D.,Milan,G.S.,&Reginato,C.E.R.(2011).Fatorescríticospara osucessonodesempenhodenovosprodutos:umestudoaplicadoaosetor moveleirodaSerraGaúcha.Gestão&Produ¸cão,18(3),587–602.

DeToni,D.,&Mazzon,J.A.(2013a).Imagemdeprec¸odeproduto:proposic¸ão deummodeloconceitual.RAUSP–RevistadeAdministra¸cãodaUSP,48(3), 454.

DeToni,D.,&Mazzon,J.A.(2013b).TestedeumModeloTeóricoSobreoValor PercebidodoPrec¸odeumProduto.RAUSP–RevistadeAdministracãoda USP,49(3),549–565.

Diamantopoulos, A.(2005).Determinac¸ão de prec¸os. In: M.Baker (org.), Administrac¸ãodemarketing,RiodeJaneiro:Elsevier.

Dutta,S.,Zbaracki,M.J.,&Bergen,M.(2003).Pricingprocessasacapability:A resource-basedperspective.StrategicManagementJournal,24(7),615–630.

Field,A.(2013).DiscoveringstatisticsusingIBMSPSSstatistics(4thed.). ThousandOaks:SagePublications.

Füreder,R.,Maier,Y.,&Yaramova,A.(2014).Value-basedpricinginAustrian médium-sizedcompanies.StrategicManagement,19(10),13–19.

Guilding,C.,Drury,C.,&Tayles,M.(2005).Anempiricalinvestigationof theimportanceofcost-pluspricing.ManagerialAuditingJournal,20(2), 125–137.

Hair,J.F.,Jr.,Black,W.C.,Babin,B.J.,Anderson,R.E.,&Tatham,R.L. (2009).Análisemultivariadadedados(6thed.).PortoAlegre:Bookman.

Hamilton,R.,&Chernev,A.(2010).Theimpactofproductlineextensions andconsumergoalsontheformationofpriceimage.JournalofMarketing Research,47(1),51–62.

Heil,O.P.,&Helsen,K.(2001).Towardanunderstandingofpricewars:Their natureandhowtheyerupt.InternationalJournalofResearchinMarketing,

18(1),83–98.

Hinterhuber,A.(2004).Towardsvalue-basedpricing–anintegrativeframework fordecisionmaking.IndustrialMarketingManagement,33(8),765–778.

Hinterhuber,A.(2008).Customervalue-basedpricingstrategies:Why compa-niesresist.JournalofBusinessStrategy,29(4),41–50.

Hinterhuber,A.,&Liozu.(2013).Innovationinpricing:Contemporarytheories andbestpractices.NewYork:Routledge.

Hinterhuber,A.,&Liozu.(2014).Isinnovationinpricingyournestsourceof competitiveadvantage?BusinessHorizons,57(3),413–423.

Ingenbleek,P.,Debruyne,M.,Frambach,R.T.,&Verhallen,T.M.(2003). Suc-cessfulnewproductpricingstrategies:Acontingencyapproach.Marketing Letters,14(4),289–305.

Ingenbleek,P.,Frambach,R.T.,&Verhallen,T.M.(2010).Theroleofvalue informedpricinginmarketorientedproductinnovationmanagement. Jour-nalofProductInnovationManagement,27(7),1032–1046.

Ingenbleek, P., & Van Der Lans, I. A. (2013). Relating price strategies and price-setting practices. European Journal of Marketing, 47(1/2), 27–48.

Jaccard,J.,&Turrisi,R.(2003).Interactioneffectsinmultipleregression(2nd ed.).ThousandOaks:SagePublications.

Juran,J.M.,&DeFeo,J.(2010).Juran’squalityhandbook:Thecompleteguide toperformanceexcellence(6thed.).NewYork:McGraw-Hill.

Kohlia,C.,&Surib,R.(2011).Thepriceisright?Guidelinesforpricingto enhanceprofitability.BusinessHorizons,54(6),563–573.

Lancioni, R.(2005).Astrategicapproachtoindustrialproductpricing:The pricingplan.IndustrialMarketingManagement,34(2),177–183.

Liozu, S. M. (2013). Pricing capabilities and firm performance: A socio-technical framework for the adoption of pricing as a transfor-mationalinnovation.(ElectronicThesisorDissertation).Retrievedfrom

https://etd.ohiolink.edu/

Liozu,S.,Boland,R.,Hinterhuber,A.,&Perelli,S.(2011).Industrialpricing orientation:Theorganizationaltransformationtovalue-basedpricing.Paper presentedatFirstInternationalConferenceonEngagedManagement Schol-arship,June2,2011.AvailableatSSRN:http://ssrn.com/abstract=1839838

Liozu,S.M.,&Hinterhuber,A.(2012).Industrialproductpricing:Avalue-based approach.JournalofBusinessStrategy,33(4),28–39.

Liozu,S.M.,&Hinterhuber,A.(2013).Pricingorientation,pricingcapabilities, andfirmperformance.ManagementDecision,51(3),594–614.

Malhotra,N.K.,Birks,D.,&Wills,P.(2012).Marketingresearch:Applied approach(4thed.).NewYork:Pearson.

Milan,G.S.,DeToni,D.,Larentis,F.,&Gava,A.M.(2013).Relac¸ãoentre estratégiasdeprec¸osedecusteio.RevistadeCiênciadaAdministra¸cão,

15(36),229–244.

Monroe,K.B.(2003).Princingmakingprofitabledecisions(3rded.).NewYork: McGraw-Hill/Irwin(internationaledition).

Nagle,T.,&Holden,R.K.(2003).Estratégiasetáticasdepre¸cos:umguiapara asdecisõeslucrativas.SãoPaulo:PrenticeHall.

Nagle,T.T.,&Hogan,J.E.(2007).EstratégiaeTáticasdePre¸co–UmGuia paraCrescercomLucratividade.SãoPaulo:PearsonEducationdoBrasil, 2007.

Payne,A.,&Frow,P.(2014).Developingsuperiorvaluepropositions:Astrategic marketingimperative.JournalofServiceManagement,25(2),213–227.

Porter,M.(1986).Estratégiacompetitiva:técnicasparaanálisedeindústriase daconcorrência(17theed.).RiodeJaneiro:Campus.

Simon,H.(1992).Pricingopportunities–andhowtoexploitthem.Sloan Man-agementReview,33(2),55.

Simon,H.,Bilstein,F.R.,&Luby,Frank.(2008).Gerenciarparaolucro,não paraaparticipa¸cãodemercado.PortoAlegre:Bookman.

Urdan, A.T. (2005). Práticase resultados de apre¸camento nasempresas brasileiras(RelatóriodePesquisa/2005).SãoPaulo:FGV/EASP.

Urdan,A.T.,&Osaku,W.A.A.(2005).Determinantesdosucessodenovos pro-dutos:umestudodeempresasestrangeirasnoBrasil.AnaisdoEncontroda Associa¸cãoNacionaldoProgramasdePós-Gradua¸cãoemAdministra¸cão. pp.29.Brasil:Brasília,DF.