on the Brazilian ground-rent

appropriated by landowners

Renda fundiária brasileira apropriada

por proprietários de terras

nICoLAs gRInBeRg*

RESUMO: Este artigo apresenta uma medida da parcela de renda fundiária brasileira apropriada por proprietários de terras agrárias durante 1955-2005 e avalia sua importância em relação a outras formas de valor excedente apropriado na economia brasileira. O trabalho também apresenta estimativas originais de várias de séries temporais que são cruciais para o estudo do crescimento brasileiro de longo prazo e desenvolvimento. Finalmente, o papel combina as medidas obtidas com as de Grinberg (2008, 2013b) para apresentar uma aproximação para a evolução do total da renda fundiária brasileira durante 1955-2005. O apêndice apresenta as fontes e a metodologia utilizadas para as estimativas.

PALAVRAS-ChAVE: Brasil; desenvolvimento econômico; renda fundiária.

ABSTRACT: This paper presents a measurement of the portion of the Brazilian ground-rent appropriated by agrarian landowners during 1955-2005 and assesses its importance relative to other forms of surplus value appropriated in the Brazilian economy. In pursuing this task, the paper also puts forward original estimations of several time-series that are crucial for the study of Brazilian long-term growth and development. Finally, the paper combines the measurements obtained here with those advanced in Grinberg (2008, 2013b) to present an approximation to the evolution of the total Brazilian ground-rent during 1955-2005. The appendix presents the sources and methodology used for the estimations.

KEyWORDS: Brazil; economic development; ground-rent. JEL Classiication: N5; Q1; O1.

INTRODUCTION

The Brazilian economy has recently undergone a period of strong growth that put it back at the centre of the international stage. It is widely agreed that this

*Consejo Nacional de Investigaciones Científicas y Técnicas (CONICET) and Instituto de Altos Estudios Sociales (IDAES) de la Universidad Nacional de San Martin (UNSAM). E-mail: [email protected]. Submitted: 21/January/2014; Approved: 9/October/2014.

growth has been underpinned by the strong performance of primary-sector pro-duction. Indeed, Brazil has become a leading producer and exporter of a wide (and widening) range of agrarian and mining commodities. This, however, is hardly a new phenomenon. Despite the many differences that exist between this period and those that preceded it, a key characteristic of the Brazilian economy throughout its entire history has been its participation in the global economy as a producer of primary commodities. For neoclassical economists, this has no relevant implications. yet, raw materials production exhibits a speciic characteristic that distinguishes it

from industrial production. The prices of primary commodities are not regulated by normal but marginal conditions of production and thus include a rent for the use of the irreproducible means of production, land (Marx, 1981). In primary--commodity producing economies, like the Brazilian, a relatively large portion of

social wealth then takes the form of ground-rent.

The goal of the present paper is to complete the measurements of the historical evolution of the Brazilian ground-rent advanced in Grinberg (2008, 2013), presen-ting an estimation of the portion appropriated by landowners. In pursuing this goal, this paper will put forward the methodology and original estimation of a group of macroeconomic time-series that are also required for the analysis of the long-term performance of the Brazilian economy. For that purpose, the paper is organised as follows. The next section discuses the determination of the capitalist ground-rent and analyses its role in structuring the Brazilian process of capital accumulation. The third section presents an estimation of the ground-rent appro-priated by landowners in Brazil. Fourth section puts together the results of the previous section with the measurements presented in Grinberg (2008, 2013b) to produce an estimation of the total ground-rent available for appropriation in Bra-zil. Fifth section assesses the relative importance of ground-rent in the the produc-tion and appropriaproduc-tion of social wealth in the Brazilian economy. The last secproduc-tion closes the paper with some conclusions.

GROUND-RENT AND CAPITAL ACCUMULATION IN BRAZIL

1981, pp. 779-811; Iñigo Carrera, 2007, pp. 11-3).1 Likewise, if successive

applica-tions of capital of a given size, each yielding different output, need to be undertaken on plots of land of different quality already under production to satisfy solvent de-mand, infra-marginal portions of capital also yield surplus proit, even those applied to worst-quality lands (Ricardo 2001, pp. 43-4; Marx 1981, pp. 812-23).2

Competi-tion by individual capitals also transforms these surplus proits into ground-rent.3

Both the extensive and intensive types of differential rent spring from the monopoly by landowners over portions of the planet that yield a different output, and thus proits, for capitals of similar magnitude. Their existence is a concrete form of reali-sation of the equalireali-sation of the rate of proit among individual capitals.

This monopoly over differential conditions of production stands on an absolute monopoly over this irreproducible means of production which becomes apparent in the case of worst-quality lands. Indeed, since, contrary to Ricardo (2001), their ow-ners would not allow their productive use by capital without also receiving a payment in exchange, commercial prices of primary commodities must rise further above the price of production (i.e., the price that covers for normal production costs and ave-rage proits) corresponding to the output of worst-quality land (or, more precisely, lowest-yielding portions capital) in order to include a rent springing from the abso-lute monopoly by landowners of a means of production that cannot be produced by human labour. Unlike the differential ground-rent, the magnitude of the rent of ab-solute monopoly (both the absolute rent and rent of simple monopoly) varies not according to soil quality (or location) but to landowners’ bargaining power vis-à-vis productive capital (Marx, 1981, pp. 882-907; Iñigo Carrera, 2007, pp. 13-4).

In sum, their monopoly over natural conditions of production that increase labour productivity, or permit it altogether, allows landowners to appropriate a portion of social wealth without actively contributing to its creation in any sense whatsoever. In contrast to what occurs in the industrial sector, these conditions cannot be reproduced by capital and generalised; surplus proits appropriated by landowners thus become rent (Marx, 1981, pp. 783-4, 891-8).

In Brazil, the rent of agrarian and mining grounds have been substantial during most of the country’s history; not only due to the large availability of productive

1 The marginal land is, by definition, the one where, ceteris paribus, capital sets in action the lowest level

of labour productivity. This does not mean, however, that the last land brought into production to satisfy social demand is, by definition, the marginal one. yet, it means that, unless all lands are of the same quality, at any moment there would be a plot of land which is the marginal one.

2 In primary production, crucially in the agrarian sector, the different successive (discrete) applications

of capital do not change, as in industrial activities, the quality of the output. They simply change its quantity. Each portion of capital is thus associated with a different level of labour productivity. See Iñigo Carrera (2007, pp. 102-3).

3 Equally, if rural (or mining) wages are particularly lower than urban wages, for reasons other than

lands, and thus the extended production of rent-bearing (i.e., primary) commodities, but also due to the relatively favourable natural conditions for primary-commodi-ty production prevailing in vast areas of its territory, and thus the high average rent materialised in them. These conditions have determined Brazil’s role in the produc-tion of relative surplus-value on a global scale and thus its participaproduc-tion in the in-ternational division of labour as a producer of primary commodities. To the extent that rent-bearing commodities have been consumed outside the Brazilian economy, ground-rent has constituted an inlow of social wealth to there.

This characteristic of the Brazilian economy has not been simply a formal dif-ference with the industrially advanced ones. On the contrary, it has determined its speciic structure and long-term development. The process of capital accumulation in Brazil has, since its origins, revolved around the recovery of ground-rent by in-dustrial capital (Grinberg, 2013a), as has been the case in most countries incorpo-rated into the international division of labour as primary-commodity producers (Iñigo Carrera, 2008). Effectively, Brazil’s original subsumption into the global circuits of accumulation as a producer of primary commodities was ridden with a genetic contradiction that determined its long-term pattern of capitalist develop-ment. If, on the one hand, the total capital of world society enhanced its valorisa-tion capacity by reducing the value of means of consumpvalorisa-tion and hence labour--power, on the other, this was partly offset by the drain of surplus-value lowing into the pockets of landowners in the form of ground-rent. Industrial (i.e., produc-tive) capital became, then, driven to overcome this barrier to its accumulation ca-pacity by establishing an antagonistic association with local landowners in order to recover part of that surplus-value. hence, from being simply a source of relati-vely cheap primary commodities, Brazil, as most other raw-material producing colonies/nations, became determined, also, as a source of ground-rent for global industrial capital (Grinberg and Starosta, 2014).

From the Colonial period to approximately the 1930s, the alliance between capital and landowners over the appropriation of the ground-rent revolved around the production, transport and international trade of various primary commodities. During that period, capitals invested in these and related sectors, as well as foreign creditors, became landowners’ main partners in the appropriation of the Brazilian ground-rent. however, incipiently since the 1930s, and crucially the end of WWII, this position was taken over by industrial capital invested in manufacturing in whose cycle of valorisation most of the ground-rent originated.

state policies have intervened in the turnover cycle of primary-sector capital, sepa-rating a portion of ground-rent and thus interrupting its low towards landowners’ pockets. These have included exchange-rate overvaluation, taxes on primary-com-modity exports and state control over their domestic and international trade.4 All

of these policies have transferred a portion of ground-rent to privately-owned in-dustrial capitals, by setting domestic prices of raw materials and means of con-sumption (and thus labour-power) below their international levels5 and, in the

case of the overvaluation of the currency, by reducing the local price of foreign exchange for speciic imports and proits repatriation.6 These policies have also

transferred a portion of ground-rent to the state not only directly (through the monopoly/control of foreign-exchange markets and primary-commodity trade or the taxation of raw-material exports), but also indirectly (through the payment of relatively high import taxes and other import-related duties with an overvalued currency). Simultaneously, other policies have allowed the appropriation of the separated portion of ground-rent by industrial capital either through ‘market me-chanisms’ or direct state actions. These have included: the calibrated protection (higher for inal goods than for inputs and machinery) of the domestic markets where internationally-small industrial capitals realise the appropriation/recovery of ground-rent; the provision of services, industrial inputs and credit at subsidised rates by state-owned companies and banks; the regulated expansion of domestic markets through their activities (i.e., the purchase of locally produced goods and services at inlated prices and an oversized workforce); and, direct subsidies or tax credits. In other words, policies associated with ISI – both in their extended, ‘classic’, and in their limited, ‘neoliberal’, forms – and the political processes through which these have come about, have been the speciic politico-economic forms of realisa-tion of processes of accumularealisa-tion based on the appropriarealisa-tion/recovery of ground--rent by global industrial capital (see Grinberg, 2013a; Grinberg and Starosta, 2014). This speciic modality of accumulation has allowed industrial capital to recover part of the Brazilian ground-rent. however, it has rested on inherently contradictory foundations. In order to accomplish the appropriation of ground-rent, industrial (manufacturing) capital has had to open and close its valorisation cycle in the Bra-zilian domestic market. Otherwise, competition to sell (buy) there above (below) world-market prices would have left the rent in the hands of landowners. As a consequence, the domestic market has had to remain protected to a degree condi-tioned by the amount of ground-rent available to sustain local industrial

produc-4 See Bresser-Pereira (2008, 2013) for an alternative account that also relates causally exchange-rate

overvaluation to the existence of ‘natural resource’ rents. This author finds in the Ricardian rents the cause of the market failure known as Dutch disease – i.e., the tendency of the Brazilian currency to become overvalued.

5 National accounts thus underestimate the real weight of primary production in the Brazilian economy.

6 Profit-rate-equalising competitive pressures have passed the ‘discount’ from exporters to agrarian

tion. Indeed, unable to produce for world markets, and thus compete with those industrial capitals that had engendered the Brazilian process of accumulation, the scale of production of industrial capital operating there became since its origins limited to the size of the domestic market. With a scale of accumulation below world-market norms, the use of frontier technology has remained restricted, let alone its development. In addition, policies maximising the appropriation of ground-rent by industrial capital, crucially exchange-rate overvaluation and market protection, have reinforced this restriction further, as noted elsewhere (see, e.g., Bresser Pereira, 2008, 2013) among others.7 hence, though, on one hand,

foreign--owned industrial capital has managed in this way to valorise normally while recycling obsolete equipment and avoiding competition in world markets with parent houses, on the other, its accumulation capacity has depended, as that of locally-owned capital, on the evolution of the magnitude of the ground-rent avai-lable for appropriation. Not only because to reproduce on an expanded scale in-dustrial capital has required, ceteris paribus, a growing amount of ground-rent, but also to compensate for the ever-growing difference between local and world-market production costs, in turn resulting from the difference between local and world--market scales of production and their impact upon technological proiles and, thus,

levels of labour productivity.8 Moreover, by lowering primary-commodity domestic

prices, the forms of appropriation of ground-rent by social subjects other than landowners have restricted the intensive and extensive application of capital to primary production and, thus, the growth of primary-commodity production and the available ground-rent. In other words, these policies have pushed out of pro-duction portions of capital that, without them in place, would have yielded normal proits and some rent (Iñigo Carrera, 2007b, pp. 101-22).

Between the end of the WWII and the mid-to-late-1970s, the amount of ground-rent available for appropriation in Brazil increased strongly and remained, in general, suficient to sustain the expanded reproduction of capital accumulation, especially during the ‘commodity booms’ associated with the Korean War (1950-53) and the First Oil Shock (1973-74) which created the bases for the so-called ‘state--led’ ISI process and marked its peak, respectively. The strong growth of the global economy was then sustaining the demand for raw materials, especially those of agrarian origin. Moreover, since 1968, the expansion of global credit markets, cru-cially that of Eurodollars, gave place to a large inlow of loanable capital which complemented, as junior partner, the ground-rent in sustaining the process of

ca-7 Exchange-rate overvaluation maximises the appropriation of ground-rent by industrial capital for two

reasons. First, because it somehow hides the underlying content of the policy and its extent. Secondly, because it channels ground-rent directly into the profits of industrial capital, without further mediation of the state.

8 Between the end of WWII and the present, the productivity of Brazilian industrial labour has fluctuated

pital accumulation through ISI. Under these favourable conditions, the Brazilian economy and industrial value-added grew strongly, at 7.5 per cent and 10 per cent annual average, respectively. In the mainstream section of the industrial sector, employment expanded 4.7 per cent per year average while real wages grew at around 3.5 per cent to reach 54 per cent of US purchasing power levels in 1980 (Grinberg, 2011).

Throughout the mid-to-late-1970s, however, the prices of raw materials ente-red, after the short-lived 1973-75 boom, into a prolonged period of contraction, which affected negatively the evolution of the Brazilian ground-rent (Radetzki, 2006). The slow-growing, or even stagnating, ground-rent became, then, increasin-gly complemented by rapidly expanding inlows of foreign loanable capital. yet, though global credit supply has been expanding worldwide ever since (as a form of postponing the general crisis of overproduction), the process has not been cons-tant (Brenner, 2006; Iñigo Carrera, 2008, pp. 181-233). It has taken the form of an alternation of periods in which ictitious capital and, consequently, global credit supply expand rapidly and sustain world consumption, including that of raw ma-terials, and eventually credit lows to ‘developing’ countries, with periods in which the opposite occurs. Still, even if sporadically enlarged and complemented with large inlows of loanable capital, the Brazilian ground-rent has proved altogether incapable of sustaining the previous scale of accumulation, especially in the indus-trial sector. The ever-widening productivity gap and the emergence of new sources of cheap labour around the developing world have increased substantially capital’s requirement of these resources to valorise normally.

The slow growth of the ground-rent relative to industrial capital’s requirements has not only resulted in substantially weaker growth than during the pre-1980 period and in the partial reversion of the previous process of state-promoted indus-trial ‘deepening’. Indeed, measured in domestic currency of constant purchasing power, GDP grew at only 0.6 per cent annual average between the early 1980s and the early 2000s, before the recent ‘commodity-price boom’ and the concomitant expansion of the Brazilian ground-rent partly reversed the trends, while industrial value-added shrank by 44 per cent.9 As a consequence of this development, capital

has increasingly relied on even weaker sources of extraordinary social wealth to complement normal surplus-value: the payment of labour-power below its value and, crucially during the 1990s, the resources raised through the sale of state-owned assets at ire prices. hence, the ‘developmentalist’ policies of the rent, high--growth pre-1980 period gave way to a broadly, and increasingly, neoliberal state.

The latter has mediated politically these transformations in the economic content of the Brazilian process of capital accumulation. Though the policy shift slowly began in the early 1980s under the military, neoliberal policies peaked during the democratic governments of the 1990s. By then, the existence of an increasingly

9 See the methodological appendix below on the merits of different consumer price indices alternatively

large industrial reserve army dispensed capital to rely on politically expensive so-lutions to push down wages (Grinberg, 2013a).

Grinberg (2008, 2013b) presented an estimation of the magnitude of Brazilian (agrarian and mining) ground-rent appropriated by capital, crucially in the indus-trial sector, between 1955 and 2005. Figure 1 reproduces the results of those mea-surements.

Figure 1: Ground-rent appropriated by others than landowners – in million 2004 R$

-50000 0 50000 100000 150000 200000

1955 1957 1959 1961 1963 1965 1967 1969 1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

Source: Grinberg (2011).

As can be seen in Figure 1, the amount of ground-rent appropriated by others than landowners has been substantial during most of the 1955-2005 period, cru-cially during the ‘commodities boom’ of the 1970s. It can also be seen there that during 1984-86 and 2001-03 a peculiar situation emerged: landowners became able not only to appropriate the entire, albeit signiicantly reduced, rent but also managed to appropriate a portion of surpluses other than ground-rent – that is, of normal or ordinary surplus-value. This is relected in the negative sign of the values of the time-series during those years.

The magnitude of the ground-rent appropriated by others than landowners has depended, ceteris paribus, on the total size of the Brazilian ground-rent. In other words, the larger the total available ground-rent, the larger the size of the portion potentially appropriated by social subjects other than landowners. The remainder of the paper complements the measurements advanced in Grinberg (2008, 2013b), presenting an estimation of the portion of the Brazilian ground-rent effectively appropriated by agrarian landowners, and assessing its relative importance.10

10 The computation presented here will not include the portion of the ground-rent appropriated by

MEASURING ThE GROUND-RENT

APPROPRIATED By LANDOWNERS IN BRAZIL

The magnitude of the ground-rent effectively appropriated by agrarian lando-wners is calculated as a residual equal to the sector’s value added minus the con-sumption of ixed capital, the cost of the labour-force used for productive purposes and the proits normally corresponding to agrarian capital.11 The latter are

calcu-lated using the rate of proit of industrial capital as a proxy and the amount of capital (ixed and circulating) advanced in the agrarian sector. On average, compe-tition should make both proit rates (agrarian and industrial) approximately equal for individual capitals of a given size. A caveat should be made here, however. For reasons associated to the material characteristics of agrarian productions, small capitals tend to be more common in the agrarian than in the industrial sector. The normal rate of proit of agrarian capital thus tends to be, ceteris paribus, lower than that in the industrial sector. Using the average rates of proits in the latter as a proxy for the former thus slightly underestimates the magnitude of the ground-rent effectively appropriated by landowners. The following formula thus measures the annual ground-rent appropriated by landowners (LR).12

LRi = VAi – Wi – CFKi – ∏agri ∏agri = πindi* Kagri

Where,

VAi is the value added in the agrarian sector during year i; Wi is the cost of the rural labour-force during year i;

CFKi is the consumption of ixed capital during year i; ∏agri is the mass of agrarian capital proits during year i;

πindiis the rate of proit of industrial capital during year i;

Kagri is the amount of capital advanced in the agrarian sector during year i.

The remainder of this section will present the results of the measurement of each of these variables and comment upon them. Some of the time-series needed for the measurements in question are readily available. Others need to be estimated. The methodology and sources used to compute all time-series used in the measure-ments are presented in an appendix at the end of the paper.

Value of agrarian and industrial product and their constituent parts (wages, surplus-value and ixed capital consumption)

11 The portion of ground-rent appropriated by others than landowners is already deducted from the

sector’s value added account in the form of policy-induced lower prices of primary sector output or higher prices of its inputs.

12 See Iñigo Carrera (2007) for the original development for the Argentinian case of the methodology

In order to measure the rate of proit, the mass of surplus-value appropriated by capital needs to be compared with the capital advanced to obtain it. The annu-al mass of surpluses appropriated by capitannu-al in each branch of production is equannu-al to the value added in that sector minus the consumption of ixed capital and the cost of labour-power (i.e., total wages plus total employer contributions to social security) used in the production process, as shown in the following formula.13

∏yi = VAyi – CFKyi – Wyi

Where,

∏yi are total surplus-value appropriated in the sector y the year i; VAyiis the value added in the sector y the year i;

CFKyiis the ixed capital consumed in the sector y the year i; Wyiis the cost of labour-power in the sector y the year i;

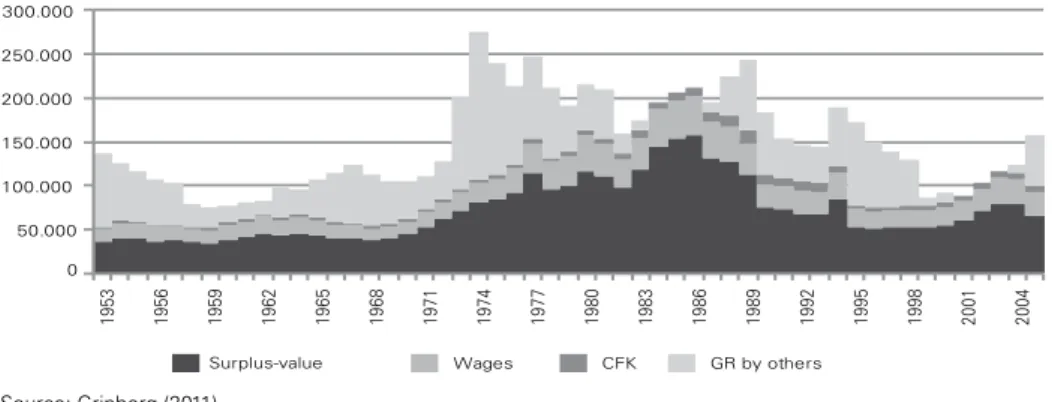

Figures 2 and 3 plot the evolution of the different components of the value of agrarian and industrial product, respectively. The portion of ground-rent (GR) appropriated by others than landowners – mostly outside that the primary sector – is added to the value of agrarian product appropriated in the sector. In the absen-ce of state policies transferring ground-rent to social subjects other than landow-ners, this portion would appear in the national accounts as part of the value of primary-sector product. As mentioned, the evolution of this portion of social we-alth was estimated in Grinberg (2008, 2013b). Two caveats, however, should be introduced here. First, as noted above, in the measurements presented here that portion includes mining ground-rent appropriated by others than mining landow-ners. Second, it also includes ground-rent appropriated by agrarian capital through low-priced equipment and inputs. Though both variables are relatively small, their inclusion somehow overestimates the measure of the value of agrarian product offered in Figure 2.

Several comments can be made on the Figures 2 and 3. First, it can be gathered that both the value of agrarian product appropriated in the sector and of industrial output expanded strongly during most the period up to the mid-1980s and collap-sed thereafter. The mass of wealth produced in the agrarian sector, however, peaked during the ‘commodities boom’ of mid-1970s rather than during the mid-1980s. Secondly, it can also be seen that the mass of surplus-value (net surpluses) appro-priated in the agrarian and industrial sectors roughly followed the evolution of the value of output. yet, in the industrial sector, it expanded more strongly than the value of output during the post late-1990s recovery as the wage mass remained practically stagnant. Though employment expanded, wages fell well below those prevailing in the 1980s.

Capital yearly advanced for valorisation in the industrial and agrarian sectors

As noted, the estimation of agrarian capital’s proits is needed to measure the portion of ground-rent appropriated by landowners. For that purpose, it is irst neces-sary to measure the amount of agrarian capital advanced for valorisation (K) and the rate of proit of industrial capital, which in turn requires comparing the surplus-value appropriated in the industrial sector with the amount of capital advanced for that purpose. Regardless of the sector of investment, the latter is composed of two parts: ixed (FK) and circulating (‘working’) portions (CK). From the point of view of macro-economic accounting, FK includes all means of production with a turnover period greater than one year – i.e., those whose use-value is consumed, and thus its value transferred to the product, throughout periods longer than one year. This includes buildings, machinery, equipment, and transport material. The circulating portion of capital includes all means of production with a turnover period shorter than one year (i.e., raw and auxiliary materials) and labour-power. Turnover period refers here to the time that takes a speciic portion of capital to fully return to the money-form in which

0 50.000 100.000 150.000 200.000 250.000 300.000

1953 1956 1959 1962 1965 1968 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004

Surplus-value Wages CFK GR by others

0 100.000 200.000 300.000 400.000 500.000 600.000 700.000

1953 1956 1959 1962 1965 1968 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004

Surplus-value Wages CFK

Figure 3: Value of industrial product – in million 2004 R$ Figure 2: Value of agrarian product – in million 2004 R$

Source: Grinberg (2011).

was originally advanced.14 The following formula synthetises the composition of

capi-tal according to the turn-over period of its different material elements:

Ki = FKi + CKi

The magnitude of ixed capital yearly advanced for valorisation is equal to the addition of the net value of the different instruments of production (fk), as deined in the following formula.

FKi =

∑

n

y fkyi

The magnitude of circulating capital advanced for valorisation every year is equal to the addition of the mass of capital in the form of direct wages and other indirect forms of compensation of the labour-force (W), raw and auxiliary materials (M) divided by the number of times (v) their value turns, on average, over during one year.

KCi = (Wi + Mi) ÷ vi

Figure 4 plots the evolution of the amount of capital advanced for valorisation in the agrarian and industrial sectors of the Brazilian economy.

Figure 4: Capital advanced for valorisation – in million 2004 R$

0 200000 400000 600000 800000 1000000 1200000 1400000 1600000 1800000 2000000

1955 1957 1959 1961 1963 1965 1967 1969 1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

Industrial Agrarian

Source: Grinberg (2011).

From Figure 4, it can be seen that the amount of capital advanced for valo-risation in the industrial sector grew strongly until around 1980, crucially during the ‘big push’ into heavy industry of the 1970s, and entered a downward trend between then and the mid-2000s. A relatively similar evolution is observed in the agrarian sector, though the stock of capital did not fall after the mid-1980s but stop growing.

14 See Marx (1992, pp. 236-61) for the analysis of the process of turn-over of industrial (productive)

Rate of proit of industrial capital

The rate of proit, that is the rate of valorisation of capital, is obtained by di-viding the total surplus-value appropriated in the economy, or a speciic branch, in a given period of time by the total amount of capital (i.e., ixed plus circulating) advanced to obtain them. Thus the formulas to measure sectoral rates of proit are the following.

πyi = ∏yi = ÷ Kyi

Where,

πyi is the average rate of proit in the sector y the year i.

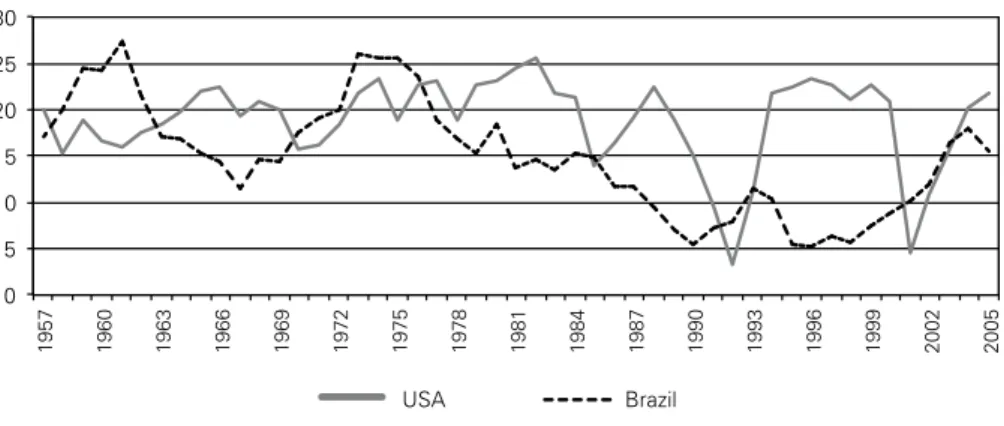

Figure 5 compares the evolution during 1957-2005 of the rate of proit of industrial capital in Brazil and in the USA.

Figure 5: Pre-tax rate of profit of industrial capital

0 5 10 15 20 25 30

1957 1960 1963 1966 1969 1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005

USA Brazil

Source: Grinberg (2011).

ac-cumulation began come about through increasingly ‘neoliberal’ policies. It only recovered after the late 1990s as industrial-sector wages had fallen below 40% of those prevailing in the mid-1980s (Grinberg, 2013a).

ground-rent appropriated by landowners

Armed with the measurements presented in the previous sections, it is now possible to plot the estimation of the magnitude of the portion of Brazilian ground--rent effectively appropriated by landowners. In Figure 6 below, this is compared with the portion appropriated by other social subjects estimated in Grinberg (2008, 2013b). The latter, it should be noted, also includes the portion of the mining ground-rent appropriated by others than landowners.

Figure 6: Ground-rent appropriation

in million 2004 R$

-50000 0 50000 100000 150000 200000

1955 1957 1959 1961 1963 1965 1967 1969 1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

By landowners By others

Source: Grinberg (2013a:195)).

TOTAL GROUND-RENT

The magnitude of the total ground-rent (TR) available for appropriation in Brazil is then measured by adding up the portions appropriated by landowners and by other social subjects as in the following equation.

TRi = A0Ri + LRi

Where,

AORi is the ground-rent appropriated by others than landowners during year i; LRi is the ground-rent appropriated by landowners during year i.

Figure 7 plots the evolution of total ground-rent appropriated by different social subjects in the Brazilian economy between 1955 and 2005.

Figure 7: Total Ground-rent

in million 2004 R$

0 20000 40000 60000 80000 100000 120000 140000 160000 180000 200000

1955 1957 1959 1961 1963 1965 1967 1969 1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

Source: Grinberg (2011).

RELATIVE IMPORTANCE OF GROUND-RENT IN ThE BRAZILIAN ECONOMy

Finally, this section assesses the relative importance of ground-rent in the Bra-zilian economy. Figure 8 below plots the evolution of the total ground-rent (GR) and of the portion of the rent effectively appropriated by landowners (LR) relative to total surplus-value (SV) or net surpluses. Figure 8 also shows the evolution of the ground-rent appropriated by landowners against Gross domestic product (GDP).

Figure 8: Relative importance of ground-rent in the Brazilian economy

0 0,1 0,2 0,3 0,4 0,5 0,6

1956 1959 1962 1965 1968 1971 1974 1977 1980 1983 1986 1989 1992 1995 1998 2001 2004

GR/SV LR/SV LR/GDP

Source: Grinberg (2011).

CONCLUSIONS

This paper put forward an original measurement of the Brazilian ground-rent effectively appropriated by landowners. In pursuing this task, the paper also pre-sented original estimations of various time-series that are crucial for any analysis of the long-term performance of the Brazilian economy. This included the stock of capital in the agrarian and industrial sectors, the masses of surplus-value appro-priated by industrial and agrarian capital and the average rate of proit of industrial capital. These time-series cover the period 1955-2005.

The measurements presented here complement those advanced in Grinberg (2008, 2013b), making it possible to have an estimation of the total size of the mass of surpluses (surplus-value) determined in the unity of the world market as Brazi-lian ground-rent. This measurement is crucial for the understanding of a process of capital accumulation, as the Brazilian, that has revolved around the appropria-tion of the local ground-rent by different social subjects. It was seen in this paper that while the ground-rent appropriated by landowners remained a fairly stable portion of total surpluses and national income throughout much of the post-WWII period, that appropriated by others, and hence the total ground-rent, experienced notable changes.

REFERENCES

Abreu, M. de Paiva (2008), ‘The Brazilian economy, 1930-1980’, in L. Bethell (ed.), The Cambridge History of Latin America Volume IX, Brazil since 1930, Cambridge: Cambridge University Press. Alves, P. and A. Messa Silva (2008), ‘Estimativa do estoque de capital das empresas industriais

brasilei-ras’, Texto para Discussão No. 1325, Instituto de Pesquisa Econômica Aplicada. ANFAVEA (2008), Brazilian Automotive Industrial Yearbook, ANFAVEA, São Paulo.

Bacha, E., et al. (1972), ‘Encargos trabalhistas e absorção de mão de obra: Uma interpretação do problema e seu debate’, Relatorios de Pesquisa, Instituto de Planejamento Econômico e Social, 12, IPEA/INPES, Rio de Janeiro.

Brenner, R. (2006), The Economics of Global Turbulence, London: Verso Books.

Bresser-Pereira, L.C. (2008), ‘The Dutch disease and its neutralization: a Ricardian approach’, Brazilian Journal of Political Economy, 28 (1), pp. 47-71.

Bresser-Pereira, L.C. (2013), ‘The value of the exchange rate and the Dutch disease’, Brazilian Journal of Political Economy, 33 (3), pp. 371-387.

CEPAL/BNDE (1956), Análisis y Proyecciones del Desarrollo Económico: El desarrollo económico del Brasil, Naciones Unidas, Departamento de Asuntos Económicos y Sociales, México.

Chacel J.M. (1967), ‘O setor agricola, a renda nacional e a taxa de investimento’, Revista Brasileira de Economia, 4, pp. 50-60.

Franco, G. (2000), ‘The Real plan and the exchange rate’, Essays in International Finance, No. 217, Princeton University, New Jersey.

Ghilardi, A. (2005), ‘Custo operacional básico e receita líquida de laranja para indústria na região norte do estado de São Paulo, safra agrícola 2003/4’, Informações Econômicas, 35 (3).

Fonseca, R. and T.C. Mendes (2002), ‘Produtividade do capital na indústria brasileira’, Texto para Discussão No. 2, Confederação Nacional da Indústria, Brasília.

Fundação Getulio Vargas, Conjuntura Econômica, IBRE, various issues.

Grinberg, N. (2008), ‘From the ‘miracle’ to the ‘lost decade’: Intersectoral transfers and external credit in the Brazilian economy’, Brazilian Journal of Political Economy, 28 (2). p. 291-311.

Grinberg, N. (2011), ‘Transformations in the Brazilian and Korean processes of capitalist development: the political economy of late-industrialisation’, PhD thesis, London School of Economics and Political Science.

Grinberg, N. (2013a), ‘The political economy of Brazilian (Latin American) and Korean (East Asian) long-term development: moving beyond nation-centred approaches’, New Political Economy, 18 (2), pp. 171-197.

Grinberg, N. (2013b), ‘Capital accumulation and ground-rent in Brazil: 1953-2008’, International Review of Applied Economics, 27 (4), pp. 449-471.

Grinberg, N. and G. Starosta (2014), ‘From global capital accumulation to varieties of centre-leftism in South America: The Cases of Brazil and Argentina’, in J. Webber and S. Spronk (eds.), Crisis and Contradiction: Marxist Perspectives on Latin America in the Global Economy, Leiden: Brill Aca-demic Publishers, historical Materialism Book Series.

IBGE, Agrarian Census, various issues. IBGE, Demographic Census, various issues.

IBGE, National Household Sample Survey, various issues. IBGE, Statistics on Foreign Trade, various issues.

Instituto do Café (1976), Boletim Estatístico, various issues.

Iñigo Carrera, J. (2007), La formación Económica de la Sociedad Argentina, Buenos Aires: Imago Mundi.

Iñigo Carrera, J. (2008), El Capital: razón histórica, sujeto revolucionario y conciencia, Buenos Aires: Ediciones Cooperativas.

Langoni, C. (1974), As Causas do Crescimento Economico do Brasil, Rio de Janeiro: APEC Editora. Marx, K. (1992), Capital Volume II, London: Penguin Books.

Marx, K. (1981), Capital Vol. III, harmondsworth: Penguin Books.

Morandi, L. and E. Reis (2004), ‘Estoque de capital ixo no Brasil – 1950-2002’, XXXII Encontro Nacional de Economia, ANPEC.

Paiva Badiz Furlaneto, F. et al. (2005), ‘Custo de produção e rentabilidade da cultura da banana ‘Maçã’ na região do médio Paranapenema’, Informações Econômicas, 35 (12), pp. 19-25.

Radetzki, M. (2006), ‘The anatomy of three commodity booms’. Resources Policy, 31, pp. 56–64. Ricardo, D. (2001), On The Priniples of Political Economy and Taxation, Ontario: Batoche Books. Rodrigues Vegro, C. (2004), ‘Lucro na cafeicultura: miragem ou concreta possibilidade?’, Instituto de

Economia Agrícola, São Paulo, mimeo.

Santana Ferreira (1992), ‘Cacao standard production cost monitoring in Bahia, Brazil’, Agrotopica, 4 (3), Centro de Pesquisas do Cacau, Ilhéus, Bahia.

Serra, J. (1982), ‘Ciclos e mudanças estruturais na economia brasileira de pós-guerra’, in Gonzaga M. Belluzzo, L. and R. Coutinho (eds.), Desenvolvimento Capitalista no Brasil, São Paulo: Editora Brasiliense.

US Bureau of Census (1975), Historical Statistics of the United States, Colonial Times to 1970. US Bureau of Census, ‘Quarterly inancial report for manufacturing, mining and trade corporations’,

various issues.

APPENDIX: METhODOLOGICAL BASES AND SOURCES15

CONSUMER PRICE INDEX

Methodology and sources

The Consumer Price Index (CPI) produced by the Getulio Vargas Foundation (FGV) is used here instead of the Augmented Consumer Price Index (IPCA) pub-lished by the Brazilian Institute of Geography and Statistics (IBGE). Two reasons assist this choice. First, the CPI-FGV is the irst of such indices produced in Brazil and, for that reason, the only one that covers the entire period under study keeping methodological consistency. Its origins date back to the early 1940s, when it was calculated for the city of Rio de Janeiro. A correction, using the re-estimation avail-able in Correa do Lago (1989, p. 248) and Abreu (2008a, p. 373), was made on the original time-series for 1973. That year, the inlation rate measured by the FGV was grossly underestimated, under pressure from the military attempting to keep readings low for political and policy purposes. The original reading of 13.7% was changed for the subsequent re-estimation of 26.6%. Secondly, the IPCA, produced by the IBGE since 1980, suffered several, often spurious, manipulations and meth-odological changes with the purpose of reducing the oficial inlation readings, crucially in 1990-92, when the Collor Plan was implemented, and during July--August 1994, when the Plan Real was launched and the so-called ‘residual’ inlation

was removed from the index.16

GROSS FIXED CAPITAL FORMATION DEFLATOR

Methodology and sources

They are computed dividing the time-series of gross ixed capital formation in

15 All base and derived time-series used in this paper are available in Grinberg (2011, pp. 443-521).

16 See the theoretically weak defence of this manipulation put forward by Gustavo Franco (2000, p. 8),

current prices for those in constant prices. They are computed for total Gross ixed capital formation, ‘Constructions’ and ‘Machinery and equipment’.

a) 1950-2005: The time-series of Gross ixed capital formation are estimated by the IBGE and are available in Ipeadata.

AGRARIAN AND INDUSTRIAL GDP AT FACTOR COSTS

sources

a) 1955-2005: The time-series of sectoral GDP are estimated by the IBGE (available in Ipeadata).

TOTAL LABOUR COSTS IN ThE INDUSTRIAL SECTOR

Methodology and sources

The time-series of the total cost of industrial labour-power was constructed by adding-up the annual cost of the labour-force in formal employment contracts and the annual cost of those employed without formal employment contracts. The former was obtained by multiplying the average wage in the sector plus employer contributions to social security by the total amount of the formally employed la-bour-force. The latter was calculated multiplying the average wage by the quantity of informal workers, obtained by ducting the amount of formally employed indus-trial labour from the total indusindus-trial labour-force. Indusindus-trial wages were computed by dividing the wage mass with the number of workers employed during the rele-vant year. Indirect wages were calculated by multiplying direct wages with the rate of employer contribution to social security.

Wages

a) 1955-1975: Base time-series were obtained from the Annual Industrial Sur-vey (PIA) undertaken by the IBGE.

b) 1976-2008: Values were estimated using an index of nominal wages for industrial workers in the metropolitan area of São Paulo, Brazil’s largest industrial district, produced by the Federation of São Paulo Industrial Companies (FIESP).

Rate of employer contributions to social security

a) 1954-1969: It was obtained from Bacha et al. (1972, p. 165). b) 1975: It was obtained from Conjuntura Econômica, June, 1975. c) 1980: It was obtained from Conjuntura Econômica, April, 1980.

d) 1976-1979: It was estimated taking the weighted average of 1975 and 1980 values. e) 1988-1990, 1992-1993 and 1997-2007: It was computed by dividing the value of total contributions by the value of total wages published in the PIA.

g) 1994-1995: It was estimated taking the average of 1993 and 1996 values.

total industrial labour force

a) 1955-2005: The time-series was taken obtained from the ‘10-sector’ data-base produced by the Groningen Growth and Development Centre (GGDC). This information is compatible with that compiled in the Demographic Censuses and the National household Sample Survey (PNAD).

Industrial workers with formal employment contracts

a) 1989-2005: It was taken from the Ministry of Labour RAIS database. b) 1981-1988: Generated using rates of growth of an index of industrial em-ployment on São Paulo produced by FIESP (available in Ipeadata).

c) 1955-1987: Generated using rates of growth of the values presented in the PIA.

TOTAL LABOUR COSTS IN ThE AGRARIAN SECTOR

Methodology and sources

The total cost of the rural labour-force (employees, self-employed and family workers) was computed using available estimations of ‘labour’s share’ in agrarian valued-added, and multiplying these values by the valued-added in the sector. Mul-tiplying rural wages by rural workforce overestimates total labour costs; this meth-od does not account for large underemployment in the sector.

total labour costs

a) 1962-1963: It was taken from Chacel (1967) based on a FGV study. b) 1970, 1975, 1980, 1985, and 1995/6: It was obtained from Prado Lima (2007) who estimated the values using Rural Census data.

c) The rest of the time-series was estimated taking weighted averages of values available.

STOCK OF FIXED CAPITAL IN ThE INDUSTRIAL SECTOR

Methodology and sources

indirectly producing consumer goods.17 An annual average depreciation rate of

3.7% of the net value of the capital stock estimated in Morandi and Reis (2002) for economy-wide ixed capital stock was used to calculate the consumption of ixed capital.

a) 1955-2003: The time-series was generated using the rate of growth of the following estimations of the stock of ixed capital in the industrial sector:

a.1) Serra (1982) for the period 1955-1980.

a.2) Fonseca and Mendes (2002) for the period 1981-1995. a.3) Alves and Mesa Silva (2008) for the period 1996-2003.

b) 2004-2005: It was estimated using the rate of growth of total (economy-wide) ixed capital stock available in Ipeadata.

STOCK OF FIXED CAPITAL IN ThE AGRARIAN SECTOR

Methodology and sources

There is no oficial publication of the time-series of gross capital formation in the agrarian sector. Data speciic to the agrarian sector is included in the aggre-gated ‘private sector’ gross capital formation account. Nor is there a unoficial estimation of the stock of agrarian capital. For this reason, the estimation of the annual stock of ixed capital in the sector (i.e., machinery, buildings, plantations and livestock) had to be done following a different methodology than that used for the industrial sector.

The stocks of ixed capital in the form of machinery were estimated through the perpetual inventory method.18 The apparent consumption of the different types

of machinery (tractors, cultivators and harvesters) was used as a measure of invest-ment lows. In the case of milking machines, due to the lack of information, only imports were computed as investments in this type of ixed capital. Data from ANFAVEA (2008) was used for domestic production of tractors, cultivators and harvesters. Data from FAOSTAT was used for the number of tractors imported between 1950 and 2005. Information from UN Comtrade database was used for imports in domestic currency of other types of agricultural machinery. Prices of agricultural machinery published by the São Paulo Institute of Agrarian Economics (IEA) for 2005 and an index of prices of rural tractors (see below) were used to

17 This study, conducted by the United Nations Economic Commission for Latin America and the

Caribbean, known as ECLAC (originally ECLA) and the recently established Brazilian National Development Bank (Banco Nacional do Desenvolvimento, BNDE), was part of region-wide project coordinated by the UN ECLA. This project developed for the first time a uniform methodology to undertake a wide and exhaustive study of the state of Latin American economies and their growth potentialities. In some sense, this project informed the subsequent wave of developmentalist policies across the region.

18 This method consists of generating the first value of the time-series by adding the flow of investments

generate the time-series of prices for 1955-2005. For imports before 1960, data published in the Statistics on Foreign Trade by the IBGE was used. A 5% deprecia-tion rate (i.e., 20 years of useful life) was used to calculate the annual consumpdeprecia-tion of this type of ixed capital.

The estimation of the stocks of ixed capital in the form of rural buildings was done adding the low of investments and deducting the consumption (depre-ciation) of ixed capital to an original stock. Langoni’s estimation of the total stocks of rural constructions for 1953 was used for the irst value of the time-series. The estimation of annual investments in rural constructions for 1950-1969 was done by the IBGE (unpublished material) and reproduced in Langoni (1974). For 1970-2005, information on investments in rural commercial buildings is only available for the census years of 1970, 1975, 1980, 1985, and 1995-6. The rest of the time-series was estimated using the weighted averages of the sector’s investments-to-value-added ratios. Only 63% of the original stock and invest-ments in rural buildings were considered as part of the stock of ixed capital advanced for valorisations in the form of commercial buildings in the agrarian sector. The other 37% was considered to be residential buildings. The relationship between residential and non-residential constructions was taken from the Agrar-ian Censuses. The 63% mentioned above is an average of the values of the differ-ent census years.

The annual value of the stock of animals was computed by multiplying the number of animals by their prices. As livestock reproduces itself indeinitely, a turnover speed equal to ininity was used to represent the annual consumption of this type of ixed capital. In other words, livestock is always considered to be worth its full face value.

stock of animals

a) 1955-2005: The number of animals for livestock production was gathered from FAOSTAT.

Prices of livestock

a) 1955-1990: Prices for the different types of animals were obtained from various issues of the Statistical yearbook produced by the IBGE.

b) 1991-2005: They were estimated using price indices constructed for each type of animal. This information was obtained from the database of the São Paulo IEA. When no speciic information was available (i.e., birds and sheep) a compos-ite index of animals prices was used instead.

CIRCULATING CAPITAL IN ThE AGRARIAN SECTOR (EXCLUDING LIVESTOCK)

Methodology and sources

The value of circulating capital advanced for valorisation was calculated by dividing the annual value of wages and of non-wage expenditures (i.e., intermediate consumption) by the number of times that this type of capital turns over per year.

turnover speed

The average turnover of 2 times per year estimated in Iñigo Carrera (2007) for agrarian productions in Argentina is used here as a proxy for the rate of turnover of circulating capital in the Brazilian agrarian sector. This average calculated through various studies cited in that source, includes almost all the most important agrarian productions undertaken in Brazil under relatively similar productive and commercial conditions. Moreover, this value seems a good approximation consid-ering that most agrarian production processes take place once a year with the corresponding labour-processes extending through several months. The circulating capital required for these processes (e.g., seeds, fertilizers, and labour-power) tends to be disbursed across the year with disbursements on inputs concentrating during the sowing period and on labour-power during harvesting time.19 In any case,

en that circulating capital has constituted a relatively small fraction of total agrar-ian capital (22.5% average during 1955-2005 under the unrealistic assumption that its components turn over only once per year), measurement errors associated with the treatment given here are negligible.

non-wage production costs

a) 1955-2005: Values were estimated using the relationship between interme-diate consumption and value-added in the sector published in the input-output tables of 1959, 1970, 1985, 1995 and 1996. The rest of the information was gener-ated using weighted averages of that relationship and the time-series of agrarian value-added.

CIRCULATING CAPITAL IN ThE INDUSTRIAL SECTOR

Methodology and sources

The same methodology used for agrarian circulating capital.

turnover speed

The turnover speed of inventory stocks was used as a proxy for the turnover speed of circulating capital in the industrial sector. The data of the former for a sample of 665 medium and large size industrial companies during 1981-1987 was published in Conjuntura Econômica (1988). The average of those years, 6.18 times a year, was used for the entire period 1955-2005.

non-wage production costs

a) 1955-2005: Values were estimated using the relationship between intermedi-ate consumption and value-added published in the input-output tables of 1959, 1970, 1985, 1995 and 1996. The rest of the information was generated using weighted

averages of that relationship and the time-series of the sector’s value-added.

RATE OF PROFIT OF US INDUSTRIAL CAPITAL

Methodology and sources

In the absence of a time-series of the rate of proit of industrial capital for the period analysed here, either by mainstream or critical economists, the rate of return

of ‘manufacturing corporations’ calculated by the US Bureau of Census was used as an approximation.