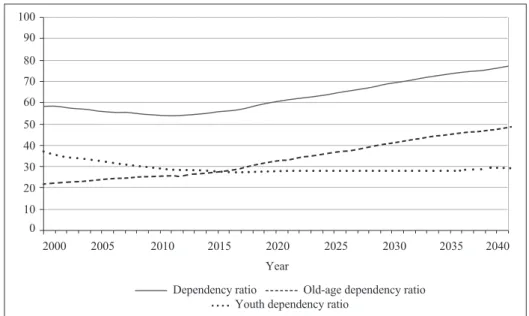

The Ageing Population and the Associated Challenges of the Slovenian Pension System

Texto

Imagem

Documentos relacionados

The fourth generation of sinkholes is connected with the older Đulin ponor-Medvedica cave system and collects the water which appears deeper in the cave as permanent

The irregular pisoids from Perlova cave have rough outer surface, no nuclei, subtle and irregular lamination and no corrosional surfaces in their internal structure (Figure

Extinction with social support is blocked by the protein synthesis inhibitors anisomycin and rapamycin and by the inhibitor of gene expression 5,6-dichloro-1- β-

Ao Dr Oliver Duenisch pelos contatos feitos e orientação de língua estrangeira Ao Dr Agenor Maccari pela ajuda na viabilização da área do experimento de campo Ao Dr Rudi Arno

Uma das explicações para a não utilização dos recursos do Fundo foi devido ao processo de reconstrução dos países europeus, e devido ao grande fluxo de capitais no

Neste trabalho o objetivo central foi a ampliação e adequação do procedimento e programa computacional baseado no programa comercial MSC.PATRAN, para a geração automática de modelos

Ousasse apontar algumas hipóteses para a solução desse problema público a partir do exposto dos autores usados como base para fundamentação teórica, da análise dos dados

Peça de mão de alta rotação pneumática com sistema Push Button (botão para remoção de broca), podendo apresentar passagem dupla de ar e acoplamento para engate rápido