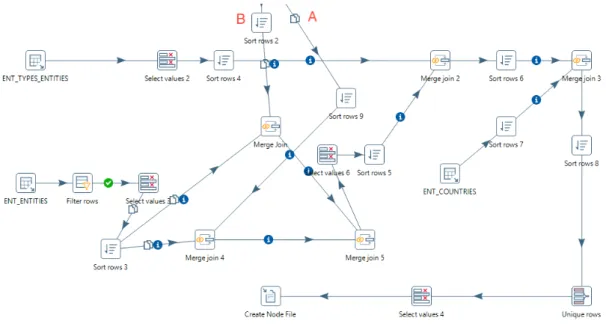

Insurance Fraud Detection - Using Complex Networks to Detect Suspicious Entity Relationships

153

0

0

Texto

(2)(3)

(4)(5)(6)(7)

(8)(9)

(10)(11)

(12)(13)

(14)(15)

(16)

(17)

(18)(19)

(20)

(21)

(22)(23)

(24)

(25)

(26)(27)

(28)(29)

(30)

(31)

(32)

(33)

(34)(35)

(36)

(37)

(38)

(39)

(40)

(41)

(42)

(43)

(44)

(45)

(46)

(47)

(48)

(49)

Imagem

![Figure 2.1: Survey performed upon Australian organizations identifying basic fraud control and prevention techniques by PricewaterhouseCoopers Economic Crime Survey 2007 [12]](https://thumb-eu.123doks.com/thumbv2/123dok_br/15194349.1017263/36.892.173.773.426.805/performed-australian-organizations-identifying-prevention-techniques-pricewaterhousecoopers-economic.webp)

+7

![Table 3.3: Some of the most relevant metrics regarding complex networks [52].](https://thumb-eu.123doks.com/thumbv2/123dok_br/15194349.1017263/71.892.108.757.576.1019/table-relevant-metrics-regarding-complex-networks.webp)

Documentos relacionados

Eles podem não escrever ali o que é, mas ouvir alguém falar, o pai falou isso, a mãe falou aquilo, daí você também não pode dizer a mãe não sabe, o pai não sabe, você já

A regulação do crescimento é complexa e multifatorial, sendo os fatores genéticos fundamentais para determinação do potencial do crescimento, porém com uma interface múltipla

Disse que não conversa muito com o pai, só com a mãe Perguntei o motivo de ele conversar pouco com o pai, ele disse: “meu pai é muito sério, quase não fica em casa

F ullerman está à espera… «Não só foste eleito para o conselho escolar, como também alcançaste a MAIOR PONTUAÇÃO DE SEMPRE no teste da semana passada.. Agora, o Marcus

O Partido Republicano Riograndense (PRR) esteve no poder do Estado do Rio Grande do Sul por quase 40 anos, tendo como principais líderes Júlio Prates de Castilhos e

A mãe devemos eterna alegria e gratidão Não importa seu sexo, se é “pai-mãe”.. Sentimentos de ser mãe, não importa em

・ Lar de pai ou mãe solteiro(a) ou mora no lar pessoa com deficiência(a própria criança, pai, mãe, irmãos), lar que se enquadra para pagar imposto municipal (pai e mãe

FAMÍLIA SECRETA DE ORAÇÃO 2 | A relação com o cardápio do almoço para o encerramento da Família Secreta de Oração já está com Anne (Cerimonial da SAF). Todas