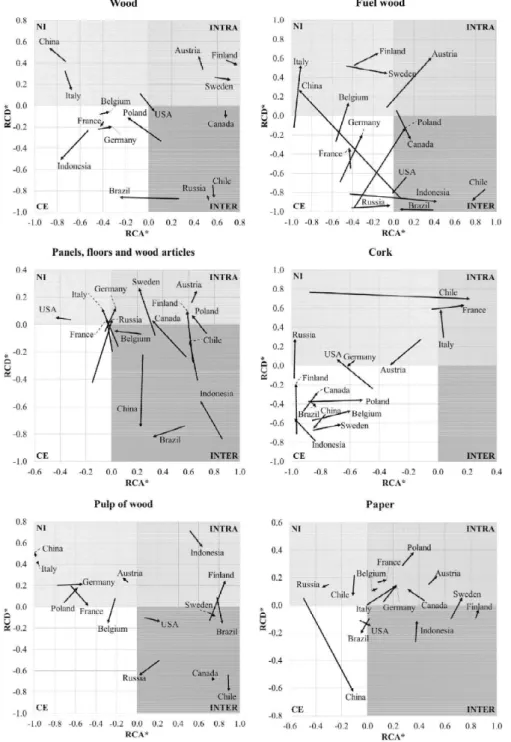

A INSERÇÃO DO BRASIL NO COMÉRCIO INTERNACIONAL DE PRODUTOS DA CADEIA FLORESTAL

Texto

Imagem

Documentos relacionados

Acabo de apresentar uma VOLIÇÂO NOBMAL E COMPLETA, um ato de vontade com as suas quatro fases... Examinarei agora a falta ou os defeitos de cada fase. Uni rapaz, exímio nadador,

O grupo “Enfermeiros Luminescentes” contempla e é norteado pelos seguintes pilares teóricos: a promoção de atividades que buscam a educação popular em saúde, tendo em vista a

Levando em consideração nosso objetivo central, que foi o de analisar o uso do diário de bordo como instrumento de coleta de dados e acompanhamento das atividades, podemos afirmar

gestroi foragers was not found in samples buried in Alcântara 1, Santa Cruz 2 and UFRRJ during the four exposure periods, nor by other termite species or by other

Para alguns professores a aposta foi no envolvimento dos pais nas actividades da sala de aula através de diferentes dinamizações (leitura de histórias,produção de materiais),

Procurámos, assim, identificar e organizar os conceitos de maior relevo sobre as expectativas e objectivos dos professores intervenientes no estudo, o grau de participação

1) The wood planks were cut into sticks measuring 700 mm x 15 mm x 15 mm and denominated long sticks (Figure 1). Eighteen long sticks were selected, three of each wood, and

The chemical constitution of the wood was influenced by the presence of reaction wood in the stem; tension and opposite wood showed lower levels of lignin and extractives and