Business as Usual 36

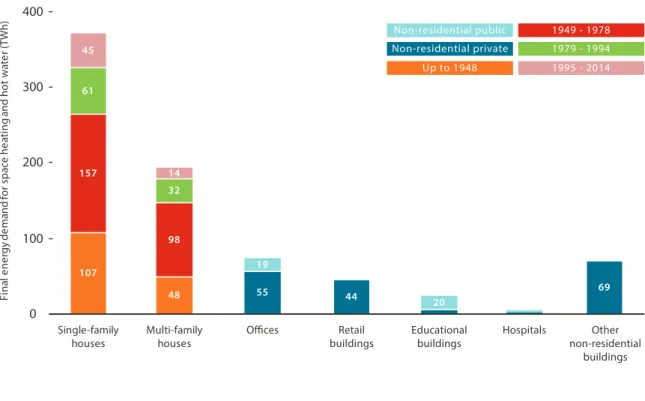

In a typical scenario, half of the building categories are located above the line and are therefore not cost-effective (disregarding additional benefit). Non-residential building categories have the most cost-effective potential for renovation, particularly hospitals, educational institutions, retail and private offices. It is worth noting that in the residential sector, only older dwellings built before 1948 show cost-effective renovation potential – these are the ones with the highest specific energy consumption, as shown in Figure 13.

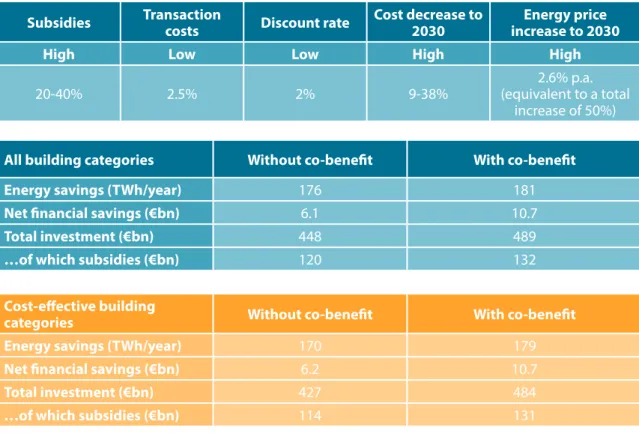

There will undoubtedly be some measures or partial renovations for newer buildings that provide cost-effective benefits, even if they achieve lower savings. Inclusion of co-benefits leads to a doubling of the energy savings of cost-efficient building categories, while net financial savings for the total of all building sectors become positive (€2.8 billion, compared to a net cost of €0.8 billion). Assuming that investors undertake only cost-effective renovations, the total investment required amounts to €97 billion, of which €19 billion is public subsidy.

For each scenario, we present a series of additional graphs that illustrate a more detailed breakdown of the results. The case of cost-efficient building categories, without fringe benefit (bottom left in Table 7), recognizes that investors will only invest in renovations where there is a net financial saving, and also that they rarely factor in the amenity benefit. The comparison of the two cases shows the great impact of including the side benefit in the economic assessment.

Cost-effective investment is only triggered for eight out of the 16 building categories without the co-payment, but increases to 12 when the co-payment is included. Over half of the renovation activity will only affect the two housing categories single-family houses and multi-family houses, in both cases related to the oldest stock, built up to 1948. Our analysis shows that there is a wide range of cost-effectiveness in the renovation of different building categories.

However, policymakers should seek to encourage investment across all building categories (except the latest stock, built since 1995). The resulting return will be calculated based on the weighted average return of the components of the investment package. To increase economic viability, the government could decide to apply subsidies to certain building categories.

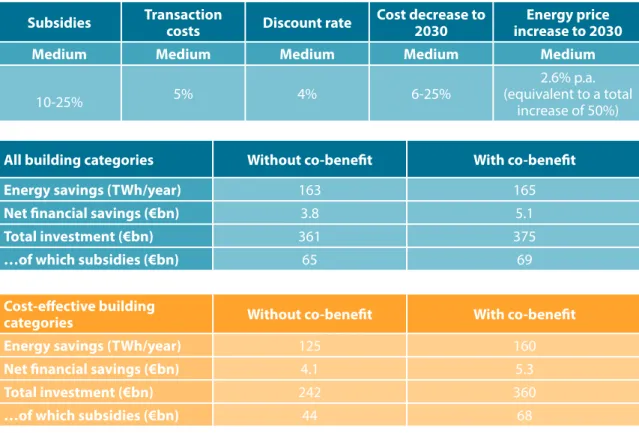

High Subsidy 41

All building categories Without co-benefit With co-benefit. categories Without co-benefit With co-benefit. Both residential and business sectors show a higher share of the ambitious renovation depth, corresponding to 80%. of the total if it is commercial construction.

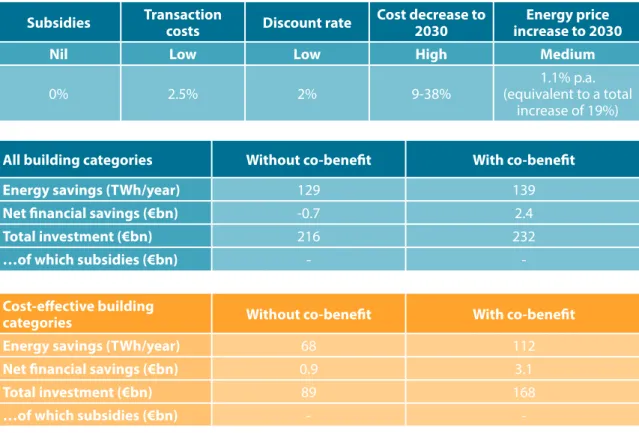

High Energy Price 45

When co-benefits are included, two important categories of buildings become cost-effective: multi-family homes and "other non-residential" categories.

Soft Measures 49

Eight of the 16 building categories are cost-effective, although the only residential building category where cost-effective investment is encouraged is single-family homes built before 1978. Only about 5% of residential buildings and 30% of non-residential buildings , attract the most ambitious depth of renewal (R3). This shows that soft measures are an important tool to encourage renewal activities, even in the absence of the direct fiscal stimulus of a subsidy.

Best Case 53

The impact of including the common comfort benefit can be seen immediately in the bottom graph, with all curves shifting down and to the right. In the following tables, a summary of the most significant results is presented to enable comparison between the scenarios and also to see the impact of the inclusion of the co-benefit. The co-benefit impact can be seen most easily in the Business as Usual and Soft Measures scenarios, where, for all building categories, the overall financial impact shifts from negative to positive.

The effect of including co-benefit is even more pronounced for the cost-effective results (in orange) with, in the Business As Usual case, a more than doubling of the investment and consequent energy savings. This figure also shows the lost opportunity in terms of savings if the prevailing economic conditions, as modeled in the Business As Usual scenario, continue. In the business sector, offices (both private and public) and shop buildings hold the greatest potential.

At worst, more than half of all renovations can be shallow, and at best, more than 70% are deep. Incorporating the co-benefit value of comfort has a major impact on all construction sectors and in all scenarios. We would not expect these new buildings to be renovated in significant numbers in the period up to 2030.

The analysis in this report shows that additional policy measures are needed if the full potential for energy savings in the German building stock is to be achieved. For these reasons, the focus of national policy should shift towards maximizing the energy savings achieved in the building stock by stimulating comprehensive and deep renovation. In the framework of the development of the national building renovation strategy, a comprehensive, comprehensive analysis of how to stimulate the market should be undertaken.

Another way to address the varying cost-effectiveness of different building categories could be in the form of an investment fund, which pools projects with different economic performances to reduce average investment risks. For building owners and investors, encouraging the inclusion of additional benefits such as increased comfort and property values in the economic assessment can have a major impact on the cost-effectiveness of deep renovations. Advice centers and one-stop-shops could offer free software that incorporates additional benefits into the economic assessment.

Costs of energy efficiency measures in building renovation: a summary report on target countries, a report within the framework of the IEE project ENTRANZE. Challenges, dynamics and activities in the construction sector and its energy needs in Germany.