Regulation on providers of on-demand audiovisual services268 Tax on revenues of providers of on-demand audiovisual media. Investments in the productions of audiovisual service distributors and on-demand audiovisual media service providers in Europe.

INTRODUCTION

- Number of on-demand audiovisual services in the Euro- pean Union as of the 31 st December 2015

- Tables “On-demand audiovisual services established in the EU” (T.1 & T.4)

- Number of on-demand audiovisual services by country of estab- lishment and by genre in the EU (December 2014)

- Number of on-demand audiovisual services by country of establishment and by genre in the EU (December 2014)

- Number of VoD services targeting primarily another country by country of establishment (December 2014)

- Number of legal VoD services available by country in the EU

- Number of legal VoD services available by country in Europe (December 2014)

- Other kind of on-demand audiovisual services available by coun- try in the European Union

- Other kind of on-demand audiovisual services available in Europe (December 2014)

- Number of on-demand audiovisual services available in the EU without double-counting 12

- Number of on-demand audiovisual services available in the EU without double-counting (December 2014)

- Number of legal VoD services available by country and by country of establishment

- Number of legal VoD services available by country and by country of establishment (except VoD adult) December 2014

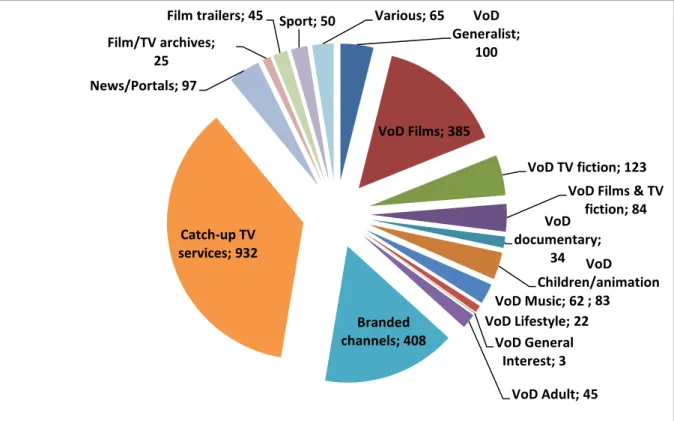

France (223 VoD services available), United Kingdom (225 VoD services available) and Germany (161 VoD services available) are the countries in the EU with the highest number of VoD services available. Number of on-demand audiovisual services available in the EU without double counting12 without double counting12.

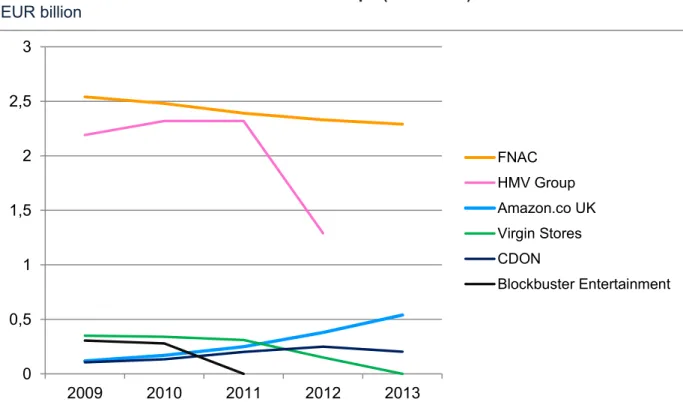

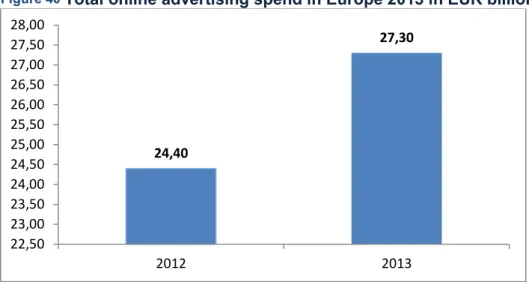

ONLINE ADVERTISING IN THE EU IN 2013

Executive summary

Main available figures on the European online advertising market

Therefore, when referring to "Europe", the figures are not representative of the European Union, but "Europe" of the 26 countries participating in the IAB survey. As there are large differences in the markets across the different countries in Europe and the EU (GDP, equipping households with connected devices, media consumption habits, broadband penetration), a general statement about the variations in the figures for online and TV advertising cannot be given. made here. It seems clear that as the second largest advertising medium behind TV in 2013, online ad spend is playing an increasingly central role in the advertising sector.

The figures given in the previous section are only totals for online advertising spend in Europe. The top three countries for online ad spend in the European Union in 2013 were the United Kingdom, with total online ad spend of €7.38 billion, Germany with. The "Top 10" countries by absolute online ad spend in the European Union are all in Western Europe, with the exception of Poland, which is the 6th most populous member of the European Union.

This shows the large differences in the online advertising market and the heterogeneous market situation in the field of the digital economy.

Focus on Display advertising

The acquisition33 in 2014 of YouTube's leading MCN, Maker Studios, by The Walt Disney Company for USD 950 million and the acquisition of 60% of the MCN Studio Bagel34 by the. and Gabszewicz J., "The media and advertising: a tale of two-sided markets" in Ginsburgh V. eds.), Handbook of Cultural Economics, Elsevier Science, August. 33 Dredge S., “Disney's YouTube deal is a real game changer”, The Guardian, 30 March 2014, available at: www.theguardian.com/technology/2014/mar/30/disney-youtube-deal-game- changer 34 Keslassy E., "Canal Plus Acquires Leading YouTube Channels Network Studio Bagel", Variety, 3. 47The original image of the American online display advertising ecosystem was created by LUMA partners, an investment firm and has since been adapted to the European online -advertising - ket, available at: www.lumapartners.com/lumascapes/display-ad-tech-lumascape.

In return, this makes it possible to target users based on their profile (preferences, interests, age, income, etc.). The use of personal information by private companies is gaining increasing attention from the general public because it is not always clearly stated what data is collected, retained and used to track individuals as they travel on the Internet. Getting the right ad is just one of the objectives of online display advertising. 60 Efrati A., “Google's Revenue Reignites Mobile Worries,” The Wall Street Journal, July 18, 2013, available at: http://blogs.wsj.com/digits googles-revenue-reignites-mobile-worries/.

Online display advertising companies are also taking advantage of the recent technological innovations and integrating them into their ad technology business.

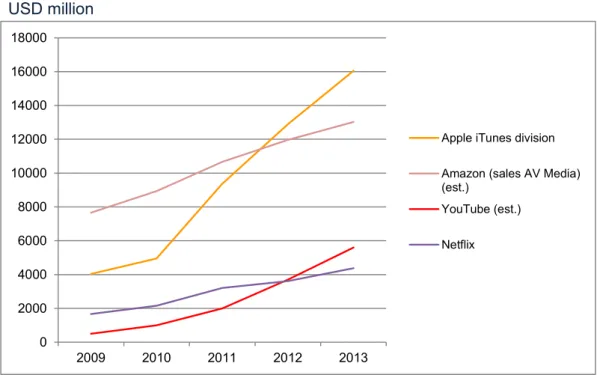

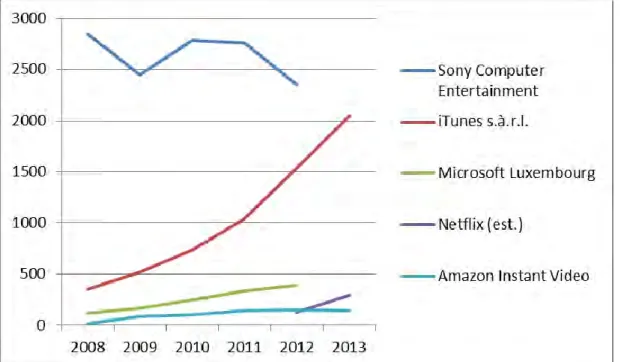

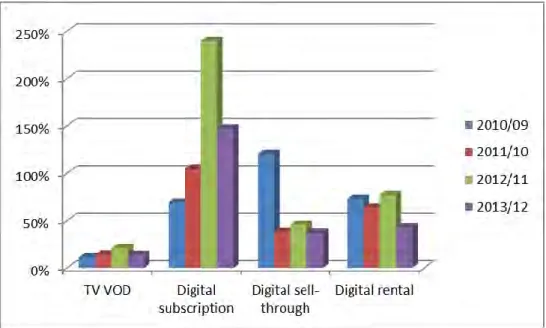

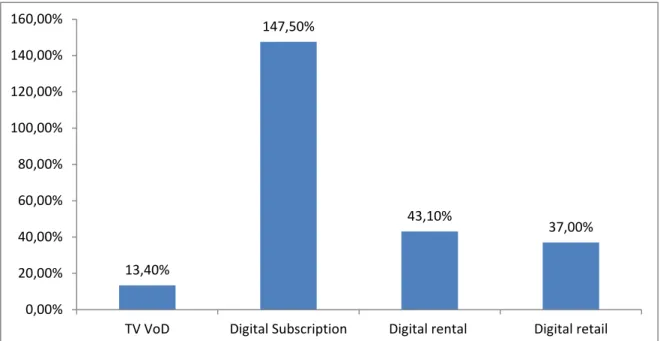

RECENT DEVELOPMENTS OF THE SVOD MARKET IN EUROPE IN 2014

European market figures

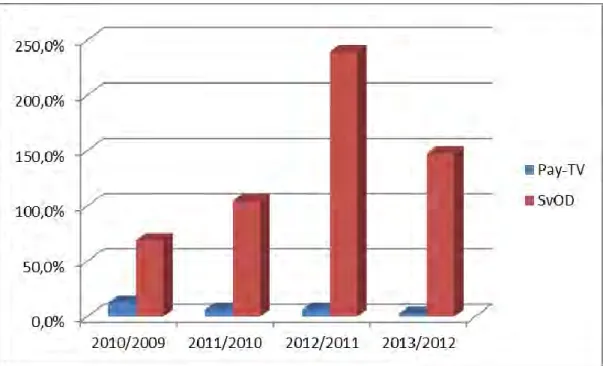

Netflix's entry into six new European markets, including Germany and France, has also highlighted the emergence of SVoD services as a source of content for European customers. This short note will provide the key figures available for the European SVoD market, discuss the key issues relating to SVoD services and provide a detailed profile of the state of the SVoD markets in France, Germany and the UK. An important fact to highlight is that the European markets are very uneven in terms of adoption and consumer consumption of SVoD services.

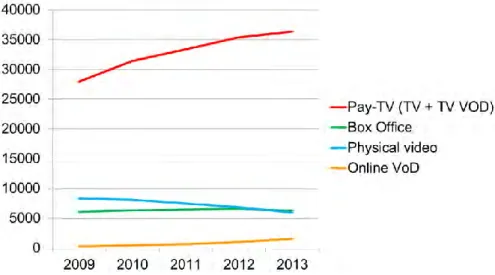

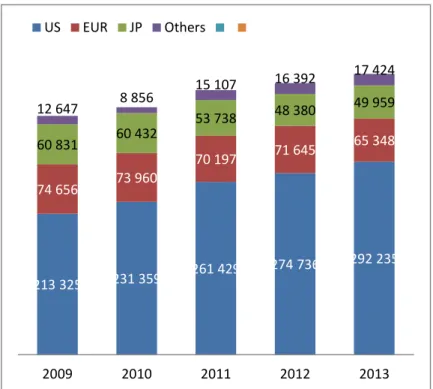

According to IVF and IHS alone, the UK accounted for €233 million in 2013 or almost 45% of total European consumer spending on SVoD. The Scandinavian markets (Sweden, Denmark, Finland and Norway), with consumer spending on SVoD, SVoD (with a total amount of €148 million compared to 2012) accounted for 28.4% of total European consumer spending on SVoD services. That is why the Scandinavian countries and the United Kingdom alone account for almost three-quarters of total European consumer spending on digital subscription services.

Digital TV Research74 projects that 59 million European households (20% of the European pay TV market) will subscribe to SVoD services by 2020.

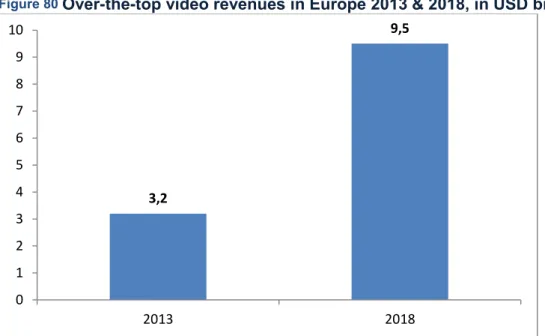

OTT video, a general trend reinforcing the adoption of SVoD services in Europe

Multi-device and multi-screen availability – the need to adapt to “ATAWAD” media consumption (Any Time, Any Where, Any Device) and the importance of access In a world where mobile connected devices and mobile and fixed broadband connections are becoming the standard, it is crucial to provide access to subscribers on any connected devices. Technical players, who do not come from the traditional audiovisual ecosystem, have this mindset – the importance of technology, continuous improvement and innovation, adaptation to the evolution of technology trends – in their DNA, while incumbents in the audiovisual sector must adapt to this new market situation . The digital economy as a whole relies heavily on the mining and analysis of data collected about users to improve services and increase customer satisfaction (this is generally true, not just for SVoD services. The advertising industry and other sectors of the digital economy uses data about their customers to establish precise user profiles).

The importance of analyzing the metadata collected about subscribers (and users, customers in general) will only increase in the short term. The proper use and exploitation of "big data" therefore seems to play a role in the rapid spread of SVoD services in Europe, as subscribers are satisfied with the service offered to them on services such as Netflix. The fact that the three main SVoD services are bidding against each other on individual "big ticket shows". the analysis cites Gotham and Blacklist as examples) has offset the impact of the reduced acquisition of bulk library rights.

Even if these films were released direct to video (no French distributor acquired the rights99), this is another important development in the increasing investment of SVoD services in content.

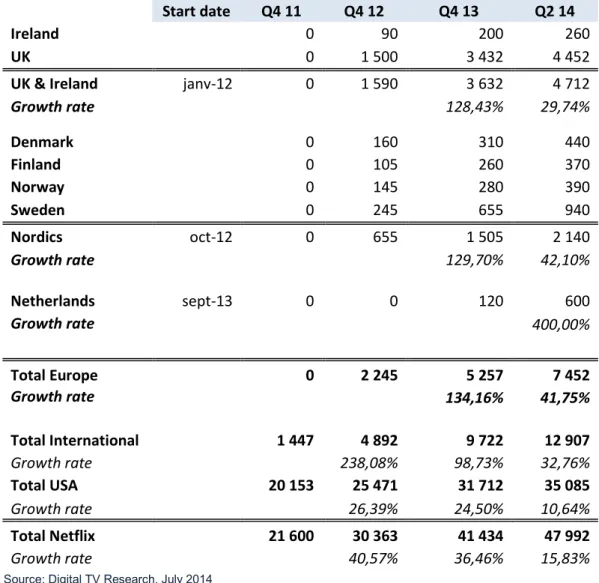

Profile of Netflix and its 2014 European expansion into six countries

At this time (October 2014) it is too early to evaluate the impact of the launch on subscriber numbers. The Diffusion Group has published the report "Netflix 2014 – Domestic Dominance, International Escalation125" (a report on which Netflix declined to comment; the last announcement about streaming hours by Netflix was in May 2014, when the company claimed its subscribers have worldwide a volume of 6.5 billion hours streamed in the first quarter of 2014, or 44.8 hours per month), including hours streamed by Netflix subscribers. In light of the paucity of data on Netflix's activity, it's quite difficult to give an overall picture of how its service is used.

In France, the entry of the SVoD giant was widely commented in the press and raised fears among established players. A revision of the release window legislation will raise questions about the future of the French system. The UK is the only European market for which actual market shares and financial data are available (IHS and Kantar Worldpanel estimates) and published in the 2014156 British Video Association Annual.

This situation has not changed since 2012, when the two SVoD services already controlled more than 90% of the UK SVoD market.

THE PROPORTION AND THE PROMINENCE OF EUROPEAN WORKS IN VOD CATA-

LOGUES

Reach of the share of European works in VoD catalogues, in number and % Reach - Share of European works Number of services in. Special offers (44.5%) and recommendations via an algorithm (40.5%) were used by less than half of the VoD services surveyed. Seven172 catalogs of VoD services were deeply analyzed in mid-October 2014 by ROVI, a company that manages the metadata of the works in catalogs of its customers.

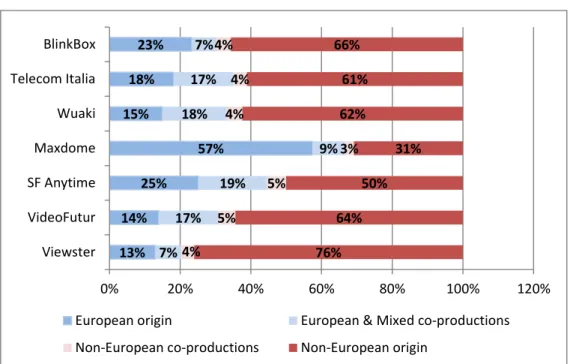

The genres of European works least present in VoD catalogs are feature films and animation. TV series and TV movies are the genres with the highest proportion of works of European origin in the catalogs of the seven VoD services. Feature films and animation are the genres with the smallest share of European works (36% and 45% of the catalogues, respectively), while TV series (58%) and TV movies (59%) are the genres where the share of European productions are the highest.

Significant differences in VoD services in terms of composition and proportion of European works in the catalogues.

Introduction - The proportion and

Another problem is the status of a segment (which exists in France, Germany and the UK, as well as the US) called "Networked Studies". The document does not provide a systematic analysis of how the implementation of the provisions on the share of European works in the catalogs is monitored. In 2013, the number of active VoD titles (programs downloaded at least once during the period) on the panel's services increased significantly.

Movies (theatrical films and films released directly to video) made up the majority of the supply. Other methods seem necessary to obtain interesting details about the presence of European works in catalogues. The letter sent with the questionnaire stated the purpose of the survey (survey on the presence of European works in VoD catalogs) and the scope (preparation of a note by the Observatory for the European Commission's DG Connect).

Regarding the share of European works in the catalogues, respondents were asked to indicate the percentage of the total number of titles of European origin (No.

Questionnaire survey