The first week they will struggle to make ends meet, scraping the barrel of what they have. They play an important role in the welfare system, but evidence suggests that in their current form they are not working as intended and may be having a counterproductive effect. I want to move my life in the right direction, but without money it feels impossible.

With all this piled up on their plate, they are not in the right frame of mind to look for work. However, there are important areas of work that bureaus undertake which are not reflected in the advice statistics – most notably in the financial literacy/skills group. Only a relatively small proportion of financial skills advice with individual clients is recorded in advice statistics.

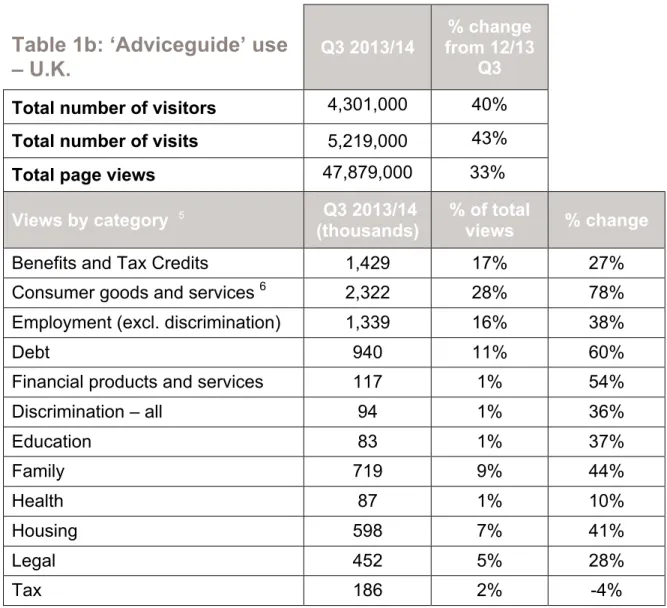

The newsletter also includes statistics for our Adviceguide self-help website and, from April 2012, for Customer Service covering England, Wales and Scotland. This web-based helpline and service (covering general consumer issues, Energy and Post) was taken over by Citizens Advice (England and Wales) and Citizens Advice Scotland in April 2012. If you have any questions or are interested in discussing further access to the data please email Peter Watson in the Corporate Management Information Team.

7 New service in April 2012 when Citizens Advice acquired Consumer Direct in England, Wales and Scotland.

Overview of Quarter 3

Combined bureau and consumer service issues

Education Taxes Immigration and asylum Healthcare and community care Financial products/services Legal Other Consumers (non-financial) Relationships and family Employment Housing Debt Benefits and tax credits.

Adviceguide

Advice delivered by bureaux

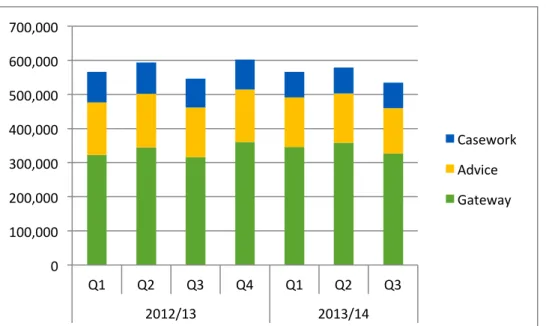

Bureau activity levels and services

LSC legal aid funding to agencies to support specialist caseworkers largely ceased by the end of March 2013. Agencies have worked hard to find new ways to fund and deliver specialist support, and some relieved local authorities have provided replacement funds to cope with the expected demands that have arisen. of welfare reform. These changes in service delivery mean that the average number of contacts with the customer per inquiry has fallen, because a greater percentage of inquiries are single contact Gateways.

Similarly, the average number of 'problems' (also called 'advice problems') per question has decreased, as fewer client problems are now recorded in the Gateway phase. This trend in problems has been further reinforced by the rollout of our new customer base.13 The total number of registered problems ('advice problems') therefore fell by 19% in the third quarter and the number of customer contacts by 10%. 13 From Quarter bureaux has started the transition to a new customer base in which Gateways and associated customer problems are recorded in a different way.

This results in a drop in recorded issues ("Issues") for technical reasons, due to a different structure.

What problems did bureaux advise about this quarter?

Online, the number of people viewing ESAs on our Adviceguide website has almost doubled in the last year. Changes to the sanctioning system for Jobseeker's Allowance (JSA) and Employment and Support Allowance (ESA) recipients have led to an increase in demand for advice on both issues. We saw over 40% growth in JSA sanctions advice this quarter compared to the same period last year.

1,150 customers (2.4% of all HB customers advised) registered to be advised about rent restrictions affecting their benefit in the social rented sector, following the introduction of HB size restrictions for the social rented sector in April – the so-called 'Bedroom Tax'. 61% of customers advised of HB size restrictions in the social rented sector last quarter were disabled or had long-term health problems. In the last quarter we advised over 3,200 clients to claim discrete housing payments, an increase of 50%.

Discretionary housing payments provide the only financial recourse in the benefits system for clients who have lost benefits due to any limitations on amount or eligibility (e.g., benefit caps, size limits). Agencies are still reporting problems making a claim over the telephone, delays in sending forms and delays in arranging face-to-face assessments by Capita and Atos. There have also been significant delays in the processing of special rules claims submitted by people with terminal illnesses.

Over 5,700 customers sought help to recover too much tax credit last quarter. The drivers behind this increase include; changes in the way in which overpayments of tax deductions have been prosecuted, changes in how the annual income is calculated and an initiative within. We continue to see a steady increase in the number of customers in need of emergency food supplies.

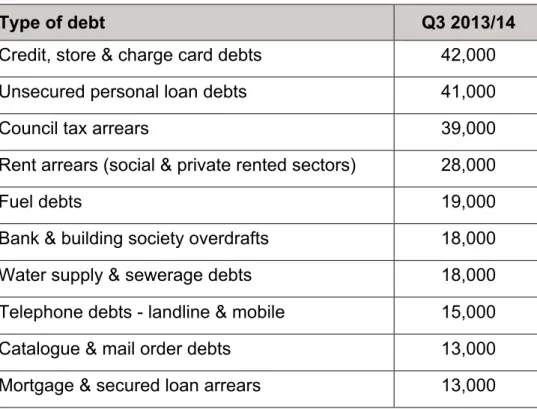

Debt advice fell by 17% in the last quarter, reflecting trends across many individual types of debt. National statistics from the Council of Mortgage Lenders show a further reduction in the number of mortgages in arrears as well as foreclosures this quarter.16 The government has just announced the end of its mortgage rescue plan in England next March. In the last six months there has been a sharp increase in inquiries about eligibility for council tax reliefs and reductions, with general advice on council tax increasing by 24%.

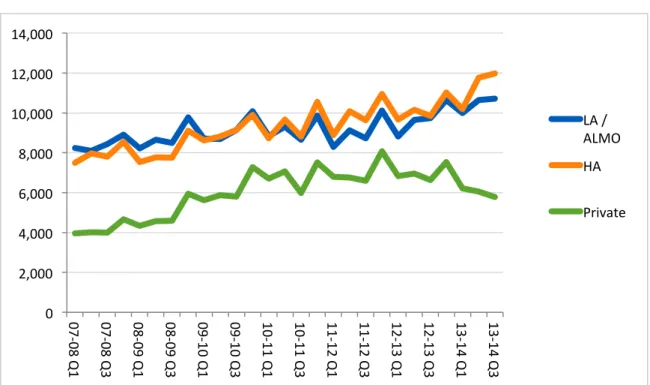

Rent arrears to social landlords has risen from 4% to 6% of all debt advice since 2015. The rise in the number of advice to social landlord rent arrears advising them about possession or eviction action has risen even more alarmingly - up 31% in the last quarter from a year ago - to 5,177.

Homelessness

Discrimination

Within employment discrimination, disability, excluding mental health, race/nationality and pregnancy/maternity, are consistently the main grounds for discrimination and make up 63% of that category. While disability decreased by 3 percentage points, both race/nationality and pregnancy/maternity increased by 6 and 4 percentage points, respectively.

Domestic violence and victims of crime

Our clients in the last quarter Gender

The proportion of customers who are owner-occupiers continues to fall, while the proportion of social housing tenants and private renters has increased.

Consumer Service

Issues at level 3

Energy cases

Types of complaint

Appendices

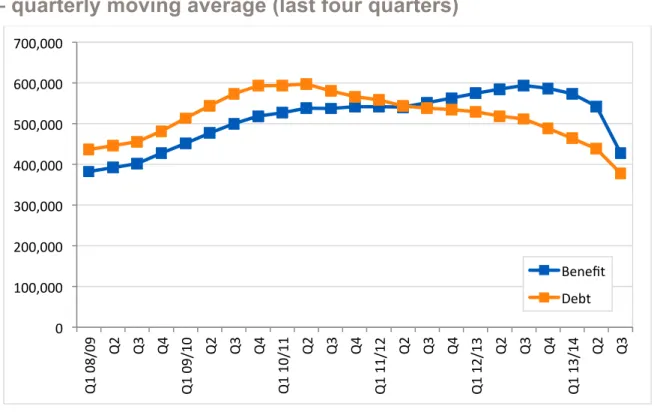

Client profile (rolling 4 quarter average)

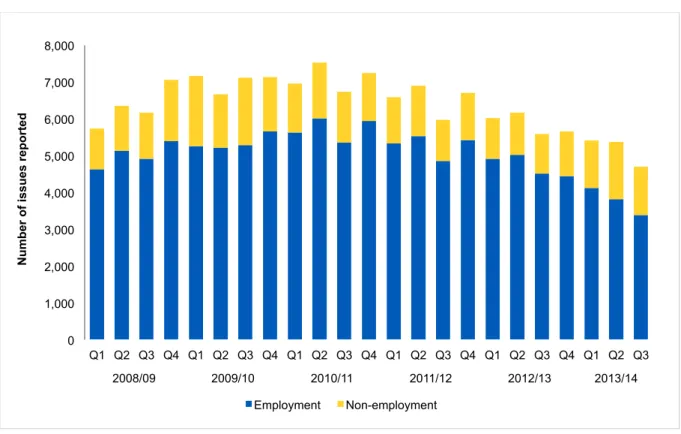

Advice Issue statistics – last eight quarters

Within an agency there is one client file for an individual client, no matter how often he/she returns to that agency. The client file contains profile information about age, gender, ethnicity and disability, and other characteristics, including local authority and district. Each time a client contacts the agency, an advisor will look up their information and either add a new inquiry, or continue working on an existing inquiry if the client has come back about an ongoing problem.

A new investigation will be opened if a customer submits a new problem or a set of related problems. Within the enquiry, codes for 'advice issues' are recorded reflecting all issues for which the client is advised within that enquiry. Level two (Part 2) – a more detailed breakdown, such as the type of debt or type of benefit being advised about.

Third level (Part 3) – describes the nature of the advice, such as negotiating repayments with the creditor for a particular debt, or advising on eligibility and entitlement to a particular benefit. Debts include all debt problems, including all utility debts, rent or mortgage arrears and benefit and tax credit debts. Financial products and services pose consumer problems, with the exception of problems with the repayment of consumer credit debts.

Consumer goods and services include all other consumer issues – with the exception of travel, transportation and vacations, which have their own category. If the customer returns for further assistance on the same query, a new contact will be added. However, consultants do not add a duplicate code to existing issue codes if work continues on the same issue (eg repayment negotiations).

Further problems are only added if the client presents a further related problem (such as a new debt) or requires a new type of advice. Cases can take months and problems can be added as cases develop. If you require a second-level breakdown for categories not included in Appendix 3, or if you are interested in third-level statistics, please contact us.