In relation to Item 7A of the agenda to approve the following recommendations from the Monitoring Officer's Report (Document “D”) to grant exemption to all members who have certain disclosed pecuniary interests listed in the Appendix. The CFO's report contains details of the Council's revenue estimates for 2021/22 (implementation document "DL").

Pecuniary Interests

Members with a spouse, partner or close relative in the employment of the Council

Members employed by or having a spouse, partner or close relative employed by a voluntary organisation/public body funded by the Council.

Members employed by or who have a spouse, partner or close relative employed by a voluntary organisation/public body funded by the Council

Members who occupied land or who had a spouse, partner or family member who did so or who were directors of companies or sat on the board.

Members who occupied land or who had a spouse, partner or relative who did or who were directors of companies or sat on the management

Members of other public authorities

Cllr Hinchcliffe (Lab) Cllr Ross-Shaw (Lab) Cllr Thirkill (Lab) Cllr Herd (Con) Cllr Heseltine (Con) Cllr Pennington (Con) Cllr D Smith (Con) Cllr Sullivan (Con) Cllr Whitaker (Con) Cllr Winnard (Kon).

Members who sit on the management committee/ trustee volunteer of a voluntary organisation in receipt of Council Funding

Members who are members of a Council funded organisation

Members appointed by the Council to a public body with an interest in the Council’s budget

Members who are school governors

Other Governors and Trustees Airedale General Hospital

Members entitled to receive an allowance paid by the Council All members of the Council in attendance

- PROPOSED COUNCIL TAX 2021/22

- PAYMENT DATES FOR COUNCIL TAX AND NATIONAL NON- DOMESTIC RATES

- DELEGATION TO OFFICERS

- PREPARATION OF ACCOUNTS

- COUNCIL TAX REQUIREMENT 2021/22

- That the total amount of £634.679m to be appropriated in respect of all schools covered by the Bradford Scheme for the Local Management of

- That Council had regard to the information contained within Executive Document “DG” in considering the Capital Investment Plan for 2021/22

- That commitments against reserve schemes and contingencies can only be made after a business case has been assessed by Project Appraisal

- That delegated authority be given to the Section 151 Officer to repay debt on an annuity basis, for chosen properties purchased during or

This is on top of the £38m we already fund annually to support Council Tax Reduction claimants. This is a budget to support resilience in the midst of an extremely challenging situation for the economy of the district, region and country.

- That the proposed 2021/22 MRP policy set out in Appendix 2 to Executive Document “DG" be approved

- That the Flexible Use of Capital Receipts Strategy be approved

- That specific approval be given for the following schemes previously approved by Executive to commence following a detailed review by

- That Members have regard to Executive Document “DI” and the

- That in accordance with Section 149 of the Equality Act 2010, Council has regard to the information contained in Executive Document “DE”,

The cost of the capital expenditure is £0.330m and it will be funded by corporate borrowing. The CFO's report to the board meeting on 16 February 2021 and the Council.

Report of the Director of Finance to the meeting of Executive to be held on 16 February 2021 and Council

Subject

Summary Statement

- PROPOSED REVENUE BUDGET 2021/22

- COUNCIL TAX IMPLICATIONS

- MATTERS RELATING TO 2020/21 FINANCIAL POSITION

- RISK MANAGEMENT AND GOVERNANCE ISSUES

- LEGAL APPRAISAL

- OTHER IMPLICATIONS 1 EQUALITY & DIVERSITY

- SUSTAINABILITY IMPLICATIONS

- GREENHOUSE GAS EMISSIONS IMPACTS

- COMMUNITY SAFETY IMPLICATIONS

- HUMAN RIGHTS ACT

- TRADE UNION

- WARD IMPLICATIONS

- IMPLICATIONS FOR CORPORATE PARENTING

- ISSUES ARISING FROM PRIVACY IMPACT ASSESMENT None

- RECOMMENDATIONS TO COUNCIL

- REVENUE ESTIMATES 2021/22

- PROPOSED COUNCIL TAX 2021/22

- PAYMENT DATES FOR COUNCIL TAX AND NATIONAL NON-DOMESTIC RATES

- DELEGATION TO OFFICERS

- PREPARATION OF ACCOUNTS

- COUNCIL TAX REQUIREMENT 2021/22

The Council will also want to take note of the directives of the parish and town councils. Band A Band B Band C Band D Band E Band F Band G Band H. All parts of the Council's area except those below.

Report of the Director of Finance to the meeting of Executive to be held on 16 February 2021

Summary statement

SUMMARY

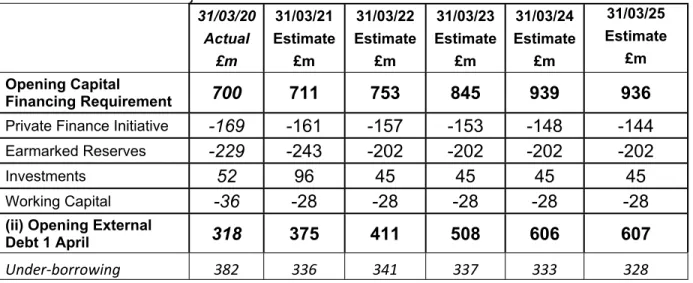

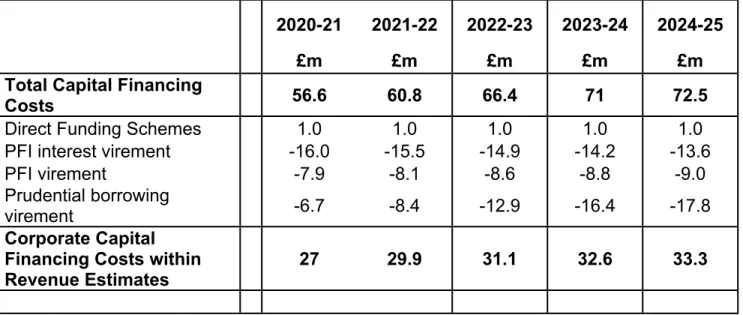

The impact of paying the loan principal and interest is professionally known as the cost of capital financing. Their purpose is to measure and consider the level of indebtedness of the Council and any impacts on revenue estimates for future generations.

THE CAPITAL SCHEMES

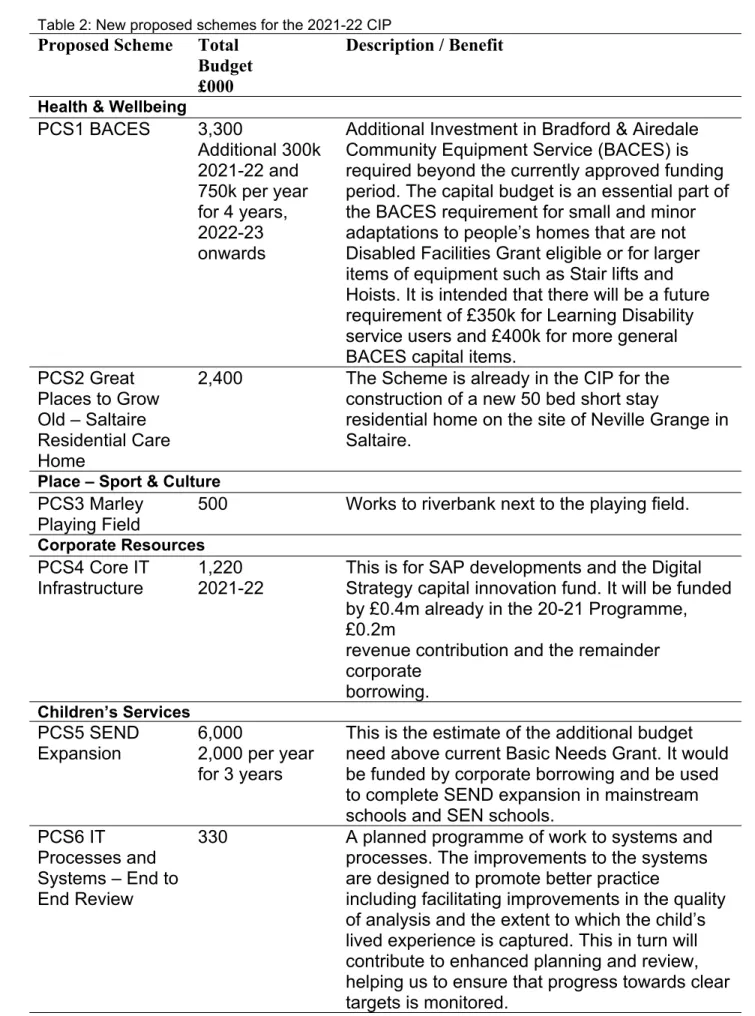

A potential increase of £0.5m for the Saltaire Residential Care Home Scheme 4.7 The proposed new schemes in Table 2 are at various stages in relation to the. The total cost of the proposed Program is £2.5m and this will be funded by the £2m included in Reserves and the movement of £0.5m from the Argus Chambers Property Scheme. The new schemes are held in a Reserves & Contingencies section of the CIP and as such cannot be released to budget managers.

Compared to previous years, the only change to the policy is an update to the Council's new Housing Revenue Account.

PRUDENTIAL INDICATORS

- SUSTAINABILITY IMPLICATIONS

- GREENHOUSE GAS EMISSIONS IMPACTS There are no direct impacts arising from this report

- TRADE UNION None

- WARD IMPLICATIONS None

- AREA COMMITTEE ACTION PLAN IMPLICATIONS (for reports to Area Committees only)

- IMPLICATIONS FOR CORPORATE PARENTING None

- ISSUES ARISING FROM PRIVACY IMPACT ASSESMENT None

- NOT FOR PUBLICATION DOCUMENTS None

- OPTIONS None

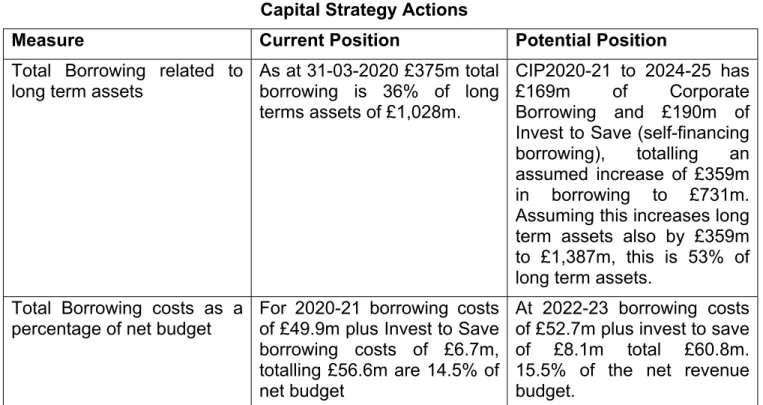

This figure also appears in the Council's accounts and is externally audited. This impact measures the annual costs against the net expenditure requirement shown in the 2021-22 revenue estimates (Document DE). The majority of the increase in the ratio is driven by borrowing for Invest to Save schemes.

9 RISK MANAGEMENT AND MANAGEMENT 9.1 The risk consequences are described in the main part of this report.

Capital Strategy 2021-22

PRUDENCE, AFFORDABILITY, SUSTAINABILITY

Each scheme's contribution to the council's service delivery and its resource needs is assessed individually. This is because the cost of borrowing is higher than the interest the council received on its investments. The council currently employs Link Asset Services as treasury management advisers and PWC as VAT advisers.

This approach ensures that the Council has access to specialist expertise when required to support its staff, in line with its risk appetite.

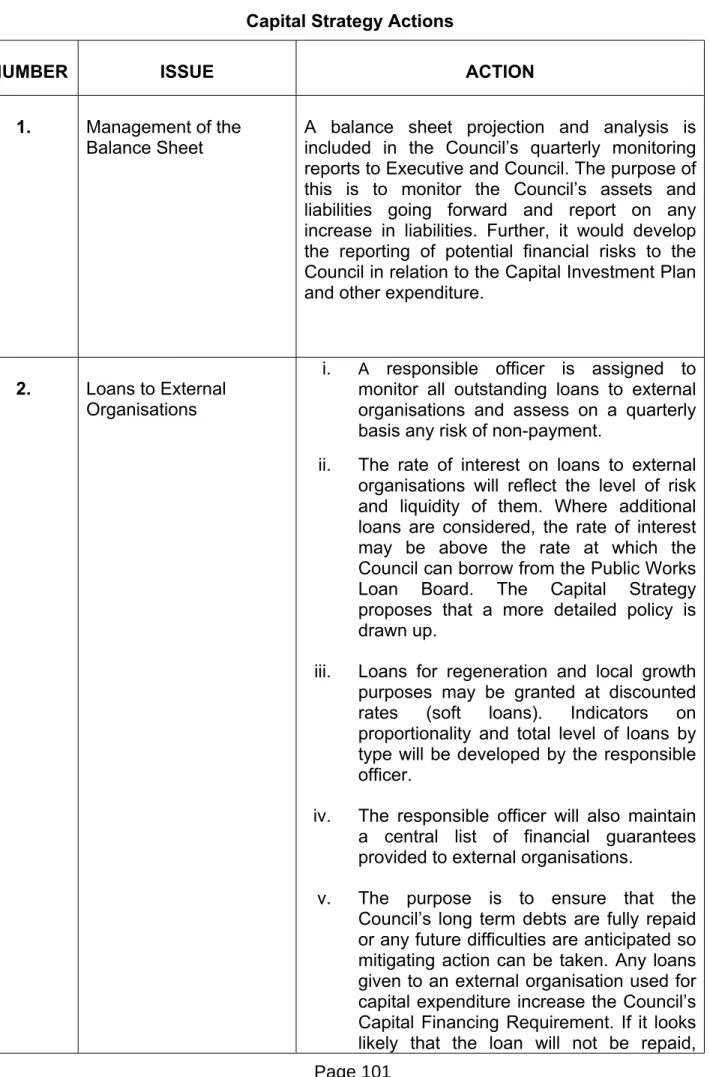

CAPITAL STRATEGY ACTIONS

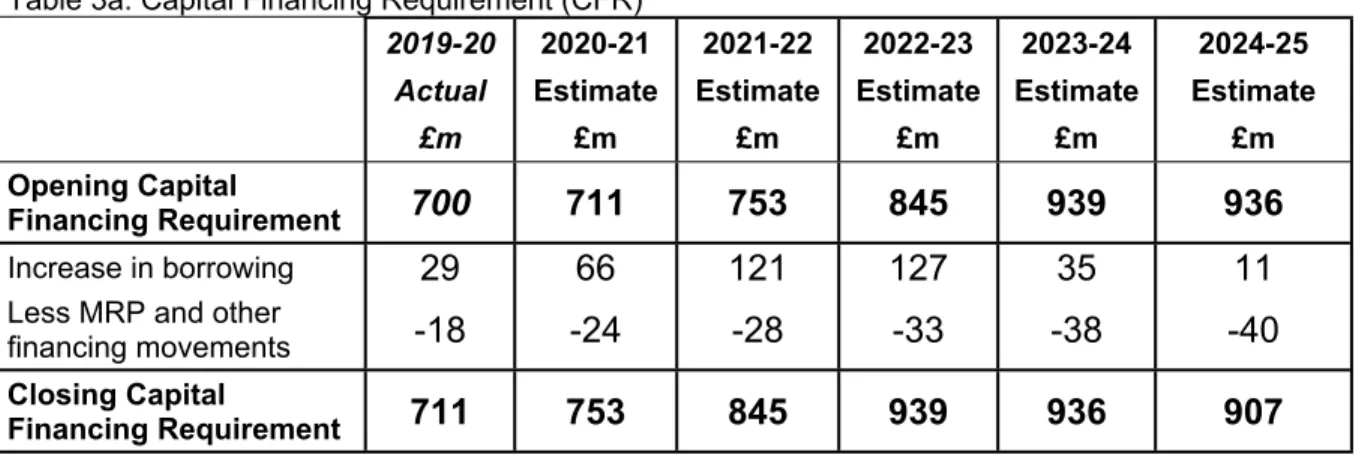

The increase in the capital financing cost ratio is mitigated within the medium-term financial strategy by: savings and income generation from the Invest to Save schemes; some technical accounting adjustments that impact the debt repayment profile for the Public Finance Initiative. The proposed CIP 2020-21 to 2024-25 requires substantial new borrowing, increasing the CFR and the amount of funding set aside for future revenue estimates. A further £161.7 million of loans relates to the private finance initiative with a private company and will be repaid from future contractual lease payments.

The Council assembles project teams from all professional disciplines across the Council when necessary.

Investment Strategy 2021-22

INVESTMENTS – DEFINITION

The guidance was issued in part as a response to local authorities' increasing investment in commercial property. As such, commercial property was specifically identified as declining within the terms of the guidance and this strategy. Most of the council's commercial property portfolio is historic with just two additional investments in recent times.

However, this strategy does not cover investments managed within the delegated cash management scheme.

KEY STRATEGIC PRINCIPLES

- Transparency and democratic accountability

- Contribution to Council’s overall purposes

- Investment indicators

- Security, Liquidity and Yield

- Investment Limit

The Global Housing Revenue Account (HRA), which aims to increase affordable housing in the District, meets criteria A. The Council proposes to adopt a system of quantitative indicators to guide and inform investment decisions in relation to other investments. The Council proposes to first adopt the indicators proposed in the Guidelines (see Annex to this Investment Strategy).

They will cover both the Council's current position and the expected position, assuming all planned investments for the following year are completed.

GOVERNANCE ARRANGEMENTS

The Council will establish and review one or more investment restrictions from time to time. The contribution from other investments should more than cover the associated debt costs while providing a net return to support the Council's revenue budget. The council can set interest rates for the long term, eliminating the risk of interest rate volatility.

Provision of £40m is included in the capital programme, phased through the program and funded by prudential borrowing.

RISK ASSESSMENT

A small budget of £0.7 million has also been included, as part of the Leeds City Region Revolving Investment Fund.

CAPACITY, SKILLS AND CULTURE

The income generated from property investment will fund 0.6% of the Council's net service expenditure in the medium term. The achievement of targeted revenue streams will be managed as part of the Council's standard budget monitoring process. Operating costs relate to the cost of the Council's internal Asset Management function in relation to the administration of assets purchased under the property investment strategy.

Invalid periods will be included in the financial evaluations as part of the evaluation criteria where necessary, so this indicator can be reviewed after the investments have been made.

Minimum Revenue Policy (Proposed 2021-22)

Furthermore, an amount equal to the set-aside will be used to finance capital expenditure on the housing stock.

CAPITAL STRATEGY TABLES

As part of this, developing the council's common understanding of the capital schemes' critical paths. The purpose is also to prepare for a likely change in accounting rules, which may increase the council's capital financing costs as a result of leasing agreements. The arrangements in Capital Investment 2021-22 were previously linked to the Council's strategies for reporting purposes.

The aim is to minimize the Council's borrowing requirements and to simplify the Project Appraisal Group.

Report from the Director of Finance to the board meeting of February 16, 2021 and the Council.

Allocation of the Schools Budget 2021/22 Financial Year

BACKGROUND

Therefore, one of the main functions of the Schools Forum is to recommend to the Authority how the funding made available by the Government to schools and individual students (known as the Dedicated Schools Grant (DSG)) is managed. As a result, it is not proposed to transfer money from the School Block for 2021/2022 to support the high need pressure. A key part of the Government's National Funding Formula for mainstream primary and secondary schools/academies in 2021/2022 is the requirement that all primary schools/academies receive a minimum of £4,180, and all secondary schools/academies a minimum of £5,415 per year. pupil.

In the context of meeting the cost-paying award, including an increase in the National Living Wage (+2.2%), the total aggregate settlement for early years providers is less than +1.5%.

SCHOOLS FORUM DECISIONS & RECOMMENDATIONS ON THE ALLOCATION OF THE SCHOOLS BUDGET 2021/22

- Pupil Referral Units (PRUs) & Alternative Providers £3,985 Two key strategic provision changes that have adjusted the 2021/22 High Needs

- Authority-Led SEND Resourced Provisions (Primary & Secondary) £5,090 Authority-Led SEND Resourced Provisions are provisions attached to mainstream

- Placements in Out of Authority & Independent Settings £10,745 The cost of placements of pupils with EHCPs in out of authority and in independent

- Provision for the Creation of Additional SEND Places £3,000 The planned budget includes £3.000m full year provision to support the creation of

- Additional Provision for the Banded Model £1,000 The 2021/22 planned budget retains a reduced earmarked contingency provision

- Former Teacher Pay and Pensions Grants £1,422 We are required to add into our formula funding arrangements for specialist settings

Providers will be funded to deliver the 2-year entitlement at a single flat rate per hour of £5.36, which fully passes on the £0.08 per hour increase awarded by the Government to our Early Years Block. The transfer to the DSG of the full cost of Post 16 High Need provision was completed by April 2017. 0.917 million main phase of the primary phase from the 2020/21 and 2021/22 settlements earmarked to be spent in support of the primary phase funding formula (provisionally the one-off application of the receipt increase factor) in 2022/23.

2.125 million retained to be used in support of the cost, including any unexpected or higher than expected costs, of the Early Years Funding Formula (EYSFF) in 2021/22 and beyond.

FINANCIAL & RESOURCE APPRAISAL

RISK MANAGEMENT AND GOVERNANCE ISSUES

LEGAL APPRAISAL

The Local Authority currently maintains some flexibility in how it distributes the funding it receives through the NFF locally in consultation with schools. The School and Early Years Finance (England) Regulations require the Local Authority to calculate budgets for all maintained schools, and amounts to be allocated in respect of early years provision, using a funding formula and to decide which formula it the funding period will use . Under new provisions set out in the Schools and Early Years Finance (England) Regulations 2020, and in the DSG grant conditions for 2021-22, local authorities will have to carry forward any cumulative shortfall in their Schools Budget to offset against DSG in the next funding period (Y+ 1); whether all or part of the deficit is carried over to the funding period thereafter (Y+2) to determine how much resource is available to be spent during the funding period (Y+1).

OTHER IMPLICATIONS

- SUSTAINABILITY IMPLICATIONS

- GREENHOUSE GAS EMISSIONS IMPACTS

- COMMUNITY SAFETY IMPLICATIONS

- HUMAN RIGHTS ACT

- TRADE UNION

- WARD IMPLICATIONS

- IMPLICATIONS FOR CORPORATE PARENTING

- ISSUES ARISING FROM PRIVACY IMPACT ASSESMENT There are no issues resulting from this report

NOT FOR PUBLICATION DOCUMENTS None

OPTIONS

RECOMMENDATIONS

- It is recommended that the Executive asks Council to

APPENDICES

BACKGROUND DOCUMENTS

It is expected that the additional funding will reflect the costs of additional support that an agency incurs in relation to the individual needs of the child or young person. In 2020/2021, the annual increase in the cost of support from higher salaries must be covered exclusively by the additional element, otherwise there will be an annual erosion of funding in real terms. The Banded Model works together with a clarified/adapted approach to sharing the costs of specialist equipment.

The top-up funding is allocated and retained by the school or provider. mainstream primary.

Report of the Director of Finance to the meeting of Executive to be held on 16 February 2021 and Council

- OPTIONS

- FINANCIAL & RESOURCE APPRAISAL

- RISK MANAGEMENT AND GOVERNANCE ISSUES

- OTHER IMPLICATIONS 1 EQUALITY & DIVERSITY

- GREENHOUSE GAS EMISSIONS IMPACTS

- WARD IMPLICATIONS

- NOT FOR PUBLICATION DOCUMENTS None

- RECOMMENDATIONS

- APPENDICES

- Appendix 1: Risk-Based Assessment

- BACKGROUND DOCUMENTS

- Risk-Based Assessment of Potential Events Affecting the Proposed 2020/21 Budget and Beyond

This report assesses the strength of the proposed 2021/22 budget, the adequacy of forecast reserve levels and the associated risks within the Council's medium-term financial outlook. The assessment is based on extensive review, supervision and personal participation in the development of the proposed budget. The 2021/22 budget proposals include a number of key proposals to mitigate the worst effects of COVID-19.

The Executive and individual Portfolio Holders have been involved in the development of the proposals at a very detailed level.

Addendum to DOC “DI”

- OTHER CONSIDERATIONS

- FINANCIAL & RESOURCE APPRAISAL

- RISK MANAGEMENT AND GOVERNANCE ISSUES

- LEGAL APPRAISAL

- OTHER IMPLICATIONS

- SUSTAINABILITY IMPLICATIONS None specific from this report

- GREENHOUSE GAS EMISSIONS IMPACTS None specific from this report

- COMMUNITY SAFETY IMPLICATIONS None specific from this report

- HUMAN RIGHTS ACT

- TRADE UNION

- WARD IMPLICATIONS

- AREA COMMITTEE ACTION PLAN IMPLICATIONS (for reports to Area Committees only)

- IMPLICATIONS FOR CORPORATE PARENTING None specific from this report

- ISSUES ARISING FROM PRIVACY IMPACT ASSESMENT None specific from this report

- NOT FOR PUBLICATION DOCUMENTS N/A

- OPTIONS

- RECOMMENDATIONS

- APPENDICES N/A

- BACKGROUND DOCUMENTS

This report provides commentary on the impact on my s151 assessment arising from the proposed Labor Group budget amendments. This report does not seek to repeat the details of my s151 assessment but should be regarded as an addendum to that report. My s151 assessment is the additional budget impact is not material against the overall council budget, and Council has proven ability to meet challenging budget targets in previous years through efficiencies, savings and revenue growth.

Report of the Director of Finance to the Executive Meeting to be held on 2 February 2021.

Report of the Director of Finance to the meeting of Executive to be held on 2nd February 2021

- MAIN MESSAGES

- OTHER ANNOUNCEMENTS

- LOCAL FUNDING ISSUES

- LEGAL APPRAISAL

- OTHER IMPLICATIONS 1 EQUALITY & DIVERSITY

- SUSTAINABILITY IMPLICATIONS

- GREENHOUSE GAS EMISSIONS IMPACTS

- COMMUNITY SAFETY IMPLICATIONS

- WARD IMPLICATIONS

- IMPLICATIONS FOR CORPORATE PARENTING None identified

- ISSUES ARISING FROM PRIVACY IMPACT ASSESMENT None identified

- NOT FOR PUBLICATION DOCUMENTS None

- RECOMMENDATIONS 1 Executive are asked to note

- BACKGROUND DOCUMENTS

There is some flexibility in the application of the Adult Social Care prescription so that it can be applied over 2 years. The weight given to the objectives of the duty is not necessarily less if the number of people affected is small. That in accordance with Section 149 of the Equality Act 2010, the Executive shall take into account the information contained in Appendix B and the Appendix to Appendix B together with the equality assessments when considering the recommendations to make to Council on budget proposals for 2021-22 make. .

Officers and elected members consider the effects of equality as part of the development of budget proposals, whereby.