ESCOLA DE P ´

OS-GRADUA ¸

C ˜

AO EM

ECONOMIA

Clara Costellini de Souza

Profit-share Bidding Auctions: A Theorectical

Approach

Profit-share Bidding Auctions: A Theorectical

Approach

Tese para obten¸c˜ao do grau de doutor apresentada `a Escola de P´os-Gradua¸c˜ao em Economia

´

Area de Concentra¸c˜ao: Teoria Econˆomica

Orientador: Alo´ısio Pessoa de Ara´ujo Co-orientador: Paulo Klinger Monteiro

Souza, Clara Costellini de

Profit-share bidding auctions: a theoretical approach / Clara Costellini de Souza. - 2015.

63f.

Tese (Doutorado) - Funda¸c˜ao Getulio Vargas, Escola de P´ os-Gradua¸c˜ao em Economia.

Orientador: Alo´ısio Pessoa de Ara´ujo. Coorientador: Paulo Klinger Monteiro. Inclui Bibliografia.

1. Leil˜oes. 2. Pr´e-sal 3. Petr´oleo em terras submersas. 4. Informa¸c˜ao assim´etrica. I. Ara´ujo, Alo´ısio Pessoa de, 1946-. II. Monteiro, Paulo Klinger. III. Funda¸c˜ao Getulio Vargas. Escola de P´os- Gradua¸c˜ao em Economia. IV. T´ıtulo.

Neste trabalho, estudamos o regime de partilha de produ¸c˜ao brasileiro, insti-tu´ıdo pela Lei No12.351, para explora¸c˜ao de petr´oleo atrav´es de uma abordagem

te´orica. Desenvolvemos um modelo de partilha de produ¸c˜ao a fim de capturar algumas caracter´ısticas do modelo de partilha brasileiro como, por exemplo, a participa¸c˜ao obrigat´oria da Petrobras, assimetria de informa¸c˜ao e a presen¸ca de participantes estrat´egicos. Atrav´es de solu¸c˜ao num´erica, fazemos uma an´alise das estrat´egias dos participantes e dos ganhos esperados. Al´em disso, desen-volvemos um modelo de custos heterogˆeneos para estudar as regras de conte´udo local.

In this paper, we study by means of a theoretical approach the Brazilian produc-tion sharing regime for oil exploraproduc-tion approved in Law No12.351. We develop a

model for production sharing to capture certain aspects of the Brazilian sharing model as compulsory participation of Petrobras, asymmetric information, and the presence of strategic participants. Using numerical solutions, we discuss the bidders’ strategies and their expected gains. Furthermore, we developed a model with heterogeneous costs to study the local content rules.

1 Fiscal regime and profit oil split - Nigeria . . . 17

2 Fiscal regime and profit oil split - Angola . . . 22

3 Expected payoff of participants - Almost common value model . . . . 40

4 Expected revenue of government - Almost common value model . . . 40

5 Expected revenue of government with asymmetric information . . . . 45

6 Expected payoff of participants with asymmetric information . . . 46

7 Expected revenue of government - Strategic x Informed participant . 48

8 Expected payoff of participants - Strategic x Informed participant . . 48

9 Expected payoff of firms - Heterogeneous costs . . . 59

1 Production bonus in Nigerian model . . . 17

2 Profit Oil Split under 2005 Nigerian PSC . . . 18

3 First Round Libyan EPSA IV 2005 . . . 20

4 Minimum signals for participation - Almost common value model . . 38

5 Bids for each signal - Almost common value model . . . 39

6 Bids for each asymmetry - Almost common value model . . . 39

7 Minimum signals for participation with asymmetric information . . . 44

8 Bids for each signal with asymmetric information . . . 44

9 Minimum signals for participation - Strategic x Informed participant. 47 10 Bids for each signal - Strategic x Informed participant . . . 47

11 Minimum signals for participation - Heterogeneous costs . . . 58

12 Bids for each signal - Heterogeneous costs . . . 58

1 Introduction 8

2 Production Sharing Agreements 11

2.1 Indonesia . . . 13

2.2 Nigeria . . . 15

2.3 Libya . . . 18

2.4 Angola . . . 21

2.5 Trinidad and Tobago . . . 23

2.6 Venezuela . . . 26

3 Rules for the Libra Oil Field Auction 28 3.1 Results from Libra Oil Field Auction . . . 28

4 Related Literature 31 5 Profit-Share Bidding Model 34 5.1 Profit-share Bidding Model with Almost Common Value . . . 34

5.1.1 Characterization of equilibrium . . . 35

5.1.2 First-order conditions . . . 36

5.2 Profit-share Bidding Model with Asymmetric Information . . . 41

5.2.1 Characterization of equilibrium . . . 42

5.2.2 First-order conditions . . . 43

5.2.3 Almost Common Value x Asymmetric Information . . . 46

5.3 Profit-share bidding model with Compulsory Participation . . . 49

5.3.1 Characterization of Equilibrium . . . 49

5.3.2 First-order conditions . . . 51

5.3.3 Alternative Formulation . . . 52

5.3.4 Nonexistence of Equilibrium in Pure Strategies . . . 53

6 Cost Heterogeneity and the Local Content Rule 55

7 Conclusions 61

1

Introduction

With the new discoveries of petroleum reservoirs of pre-salt layer, a new regime of exploration and production of oil, natural gas and other fluid hydrocarbons was adopted. The new rules include a production sharing agreement, not previously used in Brazil.

From the discovery, opponents of the concession model started a discussion about the regulatory framework, arguing that it did not fit the new reality revealed by the pre-salt. They argued that the areas have low exploratory risks and high profitability, so, it was necessary a model that guarantees higher participation over the results e more control over the potential wealth. Moreover, they said that the applicable law at the time was inadequate to the world scenario of high prices of the commodity. After a lot of discussion, in 2010, the Law No. 12.351 was approved and a model of production sharing was chosen.

In this new production sharing agreement, the area is auctioned through a profit-share bidding auction and the winning bidder is the one that offers to the Federal Union the largest percentage of profit oil (revenue from production less costs and royalties, converted to barrels of oil) and it is up to him to pay a signature bonus previously established on tender protocol, cost that is not included in calculating the profit oil and, therefore, is unrecoverable.

Despite the production sharing model, Petrobras has the exclusivity of oper-ations, since the winning consortium only executes investments and takes strategic decisions in the area to be explored. Apart from the exclusivity in operations, Petro-bras has the option to participate in the auctions and, in case of absence or loss, must adhere at 30% to the winning contract, including the payment of signature bonus required for beginning of operations.

The first point to note is that, as in most natural resource auctions, bidders only observe the true value of the object in question after the end of the process. Therefore, the offered bid is based on a previous estimate that participants have. So, it is possible that participants with similar characteristics make distinct offers, because they may have different estimates about the value of auctioned blocks. This type of auction, in which the value of the object is the same for all participants but is unknown, is called common value auction.

oil. As defined in contract, the winner is entitled to the amount of oil corresponding to spent costs and his share in profit.

Thereby, these agents are not interested only in the economic nature of the project. Even if there is no profit, they already benefit from oil property. These agents may be very aggressive in the auction. They are willing to give a large amount of the profit since they have the property of the oil as mentioned above. In this case, the object of the auction does not have the same value for all participants. The literature treats this case as an almost common value auction.

In common value auctions, the participants have only estimates about the unknown value of the object. In symmetric models, the estimates are drawn from a probability distribution that is common to all participants. The fact that Petrobras is the operator and better understands the areas to be exploited, mainly because it is located in Brazil, violates the hypothesis of equality in the distribution of estimates. Is reasonable to believe that Petrobras has access to more geological data and, on average, better estimates about the auctioned blocks than other participants. In our model, the distribution of the estimates from Petrobras has lower variance, therefore, they are more reliable.

The local content rules are also a concern for participants. For the exploration and development phases, the minimum local content required is 37% and 55%, re-spectively. The ability of internal market to meet demand and deadlines is very important to the efficiency of the projects and, consequently, to the cost involved.

Therefore, the production sharing model designed for the exploitation of pre-salt area has many characteristics that affect the behavior of agents. To better understand the dynamics of this process, this paper aims to get first answers in theoretical economic literature.

In the next section, we discuss the Brazilian regulatory framework for pre-salt layer and the production sharing agreements around the world. Following, in section

3, we detail the rules for the auction of Libra oil field, the largest oil reserve in Brazil, and analyze the results. It was the first round of pre-salt auction and a test of the new regime.

In section 4, we will briefly review the related literature of almost common value auctions and information asymmetry.

2

Production Sharing Agreements

Until the discovery of oil reservoirs in the pre-salt layer, the main oil exploration regime adopted by Brazil was the concession model. Due to the high expectations generated by the discovery of these new areas, the Brazilian government decided to develop a new regulatory framework for the oil industry of the country. Under these circumstances, by Law No. 12.351 of December 22, 2010, it was established that in the pre-salt area will be primarily adopted the production sharing regime for exploration and production of oil, natural gas and other fluid hydrocarbons.

In the production sharing contract, the State and the oil companies (OC) share among themselves the profits of oil and gas production, enabling the Federal Union to enjoy a share of the production generated. According to the government, the regime change is justified because the pre-salt layer has one of the largest oil provinces in the world and low exploratory risks.

Law No. 12.351 defines two fundamental concepts. The first is the cost oil, which is the portion of oil production corresponding to the costs and investments incurred by the contractor in the execution of the activities of exploration, eval-uation, development and production. The second is the profit oil, the portion of oil production to be split between contractor and Federal Union resulting from the difference between total production and the volume equivalent to the cost oil and the royalties.

Therefore, the OC contracted by the government shall be entitled to the amount of oil equivalent to the value of the costs of all activities carried out so far and the royalties paid in cash besides the value of their percentage in the profit oil. However, if it is not possible to declare the commerciality of the auctioned block, the OC should bear all the expense of the exploration phase.

The production sharing contracts may be awarded directly with Petrobras or through an auction. The Federal Union, through the Ministry of Mines and Energy, can directly award Petrobras for oil exploration and production in pre-salt area. In case of an auction, will be declared the winning bidder who offers the largest share of profit oil to the Government, above the floor fixed.

participation is ensured for Petrobras, as it has the exclusivity of the operation of all contracted blocks.

In the tender protocol is defined, among other things, the minimum percentage of the profit oil to the Federal Union, the minimum participation of Petrobras, which is above 30%, local content and the signature bonus value.

In addition to delivering a portion of production to the Federal Union, the winner must pay the signature bonus and royalties. The first is a value set in the production sharing contract and must be paid at the time of signature, while royalties represent the compensation to states and municipalities for the oil removed. The value of the signature bonus and the royalties are not part of the cost oil.

One of the major differences in the Brazilian production sharing model for the concession model, regime mostly used so far, is the property of the extracted oil. In the old model, from the time of extraction, the concessionary acquires the property right over the entire production. However, in the production sharing model, the Federal Union has the property of the production, and transfers to the contractor just the volume corresponding to the oil cost and to the royalties paid in cash and its share of the oil profit.

The production sharing model regulated by Law No. 12.351 was based on contracts used by other oil producing countries. The original model was created in Indonesia in the 1960’s and is currently adopted by many African and Asian countries.

In the first contracts, the division of profits between the government and con-tractors was previously fixed, not allowing adjustments in cases of technological advances, different sizes of the fields or drastic changes in oil prices. To correct these problems, subsequent contracts have predicted changes in the way of dividing the production using a sliding scale, usually based on the daily quantity produced or accumulated production. Currently, there are various ways to determine the share of profits of the agents involved in the exploration process. It can be fixed in the contract (fixed proportions or sliding scales) or subject to the bid of bidders (as established by the Law No. 12.351), although the last one is not very common.

Next, in order to better understand this regime, we will briefly discuss the cases of Indonesia, Nigeria, Libya, Angola, Trinidad and Tobago and Venezuela.

2.1

Indonesia

Indonesia is one of the pioneers in oil production in the world. The country has been producing oil on a commercial basis since 1890 and was an early member of the Organization of the Petroleum Exporting Countries (OPEC), participating from 1962 until 2008, when finally has accepted its condition of net importer of the commodity.

During the Dutch colonization period, foreign firms carried out the operations in the country under the concession regime. However, as from its independence in 1949, due to nationalistic feelings, the recently-established government tried to encourage legislation changes aiming at controlling and developing its natural re-sources.

The oil and gas sector nationalization process began with an intensification of operations performed by public companies and stricter negotiations with the oil enterprises and ended up with the creation of Pertamina in 1968 arising from the merging of Pertamin and Permina. Pertamina was a state company that, according to the new legislation, was empowered to act as a government agent when dealing with the OCs. Therefore, the production sharing agreement model was created becoming an innovation at that time and, later, reproduced by other countries.

Initially, the acceptance of the production sharing agreement was not good enough on the part of the OCs because there was a certain resistance to investments in undertakings that did not allow the total control of decisions and management. However, as time went on, the main OCs feared that they might lose ground for smaller enterprises and thus, they subdued to the regime.

effecting legislation changes.

The reforms undertaken in the early 2000 aimed at reducing the bureaucracy that was deeply rooted in the exploration and production procedures and, above all, increasing the transparency during the bidding procedures. Hence, the Pertam-ina potential was reduced because the government created a new independent body having regulatory and administrative functions called BP MIGAS. Despite the leg-islation permission for using other contractual forms, the country keeps utilizing the production sharing model in most cases (sometimes with minor alterations).

In November 2012, Indonesia’s Constitutional Court (the MK) declared BP MIGAS unconstitutional. In a decree, the MK declared that the articles of the Oil and Gas Law related to BP MIGAS were in conflict with the Constitution of the Republic of Indonesian. The responsibilities of BP MIGAS were temporarily trans-ferred to the Ministry of Energy and Mineral Rights. Subsequently, the MEMR delegated the management of upstream oil and gas business activities to SKK MI-GAS which assumes BP MIMI-GAS’ duties until the issuance of the new oil and gas law.

The hiring of an OC by the Indonesian government may occur in two ways: direct negotiation or competitive bidding. The bidding process starts with a data package disclosure about the block to be auctioned. Later on, the interested parties must present the commercial proposal and the documents proving the observance of the technical, legal, financial and administrative requirements demanded to par-ticipate in the bidding. The assigned committee, based on technical and financial criteria, chooses the best proposal and elects the winner who will, subsequently, be called to sign the contract. The invitations to bid usually establish the signature bonus, an amount that must be paid by the winning company to the government the moment the contract is signed. It is not cost recoverable and not tax deductible.

As from the conclusion of the bidding process, the winning OC starts the exploration phase. The OC bears all risks and costs of this phase. In case of the inexistence of commercial discoveries, it is not rewarded for these costs. In case of an economically feasible discovery, the OC will have its costs returned by means of the cost oil during the production phase. The proportion of the profit divided between the OC and the government is predetermined by the contract.

recovery. It is equal to 20% of the production and is split according to the shares of profit oil stipulated in the contract. This amount is a taxable income.

The second concept is the Domestic Market Obligation (DMO). The OC is required to supply a portion of the crude oil to the domestic market. Usually, DMO is 25% of the contractor’s share of the total quantity of oil produced from the contract area.

The entitlement is calculated as follows. From the total production is deducted the FTP (20% of production) and the cost oil. The production in excess, called equity oil, is split between the Government and the OC according to their shares previously stipulated. These shares also define the amount of the FTP each part is entitled. The contractor must transfer to the government the amount of oil related to the DMO.

Summing up, the amount of oil the Government is entitled is the sum of his share on FTP and on equity oil and the DMO. The OC receives its share on FTP and on equity, the cost oil and delivers the DMO.

2.2

Nigeria

Nigeria has the second largest amount of proven crude oil reserves in Africa. In addition, is the largest holder of natural gas proven reserves in the continent. Worldwide, Nigeria holds the 10th position in oil reserves and the 9th in natural gas.1

Nigeria’s first oil discoveries happened during the British rule in the 1950’s. Very soon, in 1960, the country conquered its independence but not the political sta-bility. Military coups and even a civil war prevented the Nigerians from savoring the abundance of their natural resources and reaching more comfortable levels econom-ically. Even after reconquering democracy in 1999, the country still faces political, economic and social problems. Corruption, ethnic conflicts and rising security prob-lems related to oil theft, pipeline sabotage and piracy hinder foreign investments in the oil sector impairing the productive process.

In 1971 Nigeria became a member of the OPEC. The Nigerian government, influenced by other countries of the group, starts the oil industry nationalization process. In 1977 the Nigerian National Petroleum Company (NNPC) was created, a state company responsible for the regulation and participation in the country’s oil

1

industry.

Despite the most frequent utilization of the joint ventures model, lately the country has been using the production sharing regime more often due to the offshore oil and natural gas upsurge. The difficulty of operating in offshore areas and the country’s scarce resources and other factors motivated the government to rely on this kind of contract. The production sharing model allows the government to increase the country’s oil production without resorting to its scanty available resources thus enabling the use of such resources in other sectors of the economy.

The bid submission consists of four elements:

• Signature Bonus: it has to be equal or greater than a prescribed minimum. The assigned weight to this item is 40%, achieved by bids of twice or more than the minimum.

• Work Programme Commitment: it is expressed as a quantity and value of seismic and drilling activity and must be equal or greater than a prescribed minimum. A 20% weighting is ascribed to this item.

• Cost Oil Recovery Ceiling: it is evaluated for bids of 80% or less, the maximum being scored by bids of 70% or less. A 20% weighting is ascribed to this item.

• Local Content: Bidders should reserve 10% of work commitment activity to Local Content Vehicles for deep offshore blocks and 30% for Niger Delta and Inland Basins areas. Bids are ranked according to the percentages of work commitment pro-rated below the prescribed minimum.

Similarly to what happens in other countries, the sharing production system is basically divided in two phases: exploration and production. In the exploration phase, the OCs must develop geological and geophysical researches, collect seismic data and perform additional prospection activities indispensable to a feasible oil finding. The production phase starts after an economically viable oil discovery.

Table 1: Production Bonus

Onshore Offshore Deepwater

10.000 b/d US$ 1 million US$ 2 million -50.000 b/d US$ 2 million US$ 4 million US$ 5 million

100.000 b/d - - US$ 5 million

It is wise to point out that the values of the signature and production bonuses are not recoverable, that is, they cannot be deducted from the oil profit calculus.

The fiscal regime and the profit oil split is summarized in the figure below.

Figure 1: Fiscal regime and profit oil split

increases in the R factor model.

Table 2: Profit Oil Split under 2005 PSC

R Factor Contractor Share

R <1.2 70%

1.2 < R <2.5 25% + [(2.5−R)(2.5−1.2)](70%−25%)

R >2.5 25%

R-Factor is the ratio of cumulative after tax receipts to cumulative expen-ditures - capital expenditure and operating costs.

An overhaul of the existing petroleum laws including the fiscal system was initially proposed in 2008 through the Petroleum Industry Bill (PIB). The objective is to improve the regulation and management of petroleum resources. Since then, the PIB has undergone several revisions. As might be expected, the delay in the approval of the Bill has led to a significant decline in the rate of investment in the oil and gas industry as a result of the uncertainties and its impact on the industry.

2.3

Libya

In April 1955, the Petroleum Law Enactment No 25 started the oil exploration in the Libyan territory. The first fields were discovered in 1959 and two years later the country was already exporting oil. Until the coup d’´etat in 1969, more than a hundred concession contracts had already been signed.

Since then, Muammar Gaddafi, Head of State as from 1970, adopted a series of measures aiming at nationalizing the country’s oil reserves. The National Oil Company (NOC) created in November 1970 was designed to assume the control of the oil sector. Participation agreements were established through the NOC with the purpose of replacing the concession contracts that had already been established with the OCs.

bonus called B-Factor. The exploration license is granted to the OC that offered the highest M-Factor to the government being the B-Factor used as a tie-breaking criterion.

The terms of EPSA IV are as follows: the government receives a fraction M of the gross revenue and is responsible for the payment of 50% of capital costs and a fraction M of operating costs. The other portion of revenue (1−M), is the revenue available to the contractor for recover costs: 100% of exploration costs, 50% of capital costs and a fraction (1− M) of operating costs.

After recover costs, the remaining is the profit oil that shall be splitted between OC and government according to a predetermined rule based on R-factor, which is calculated by dividing the contractor’s accumulated receipts by its accumulated expenditures.

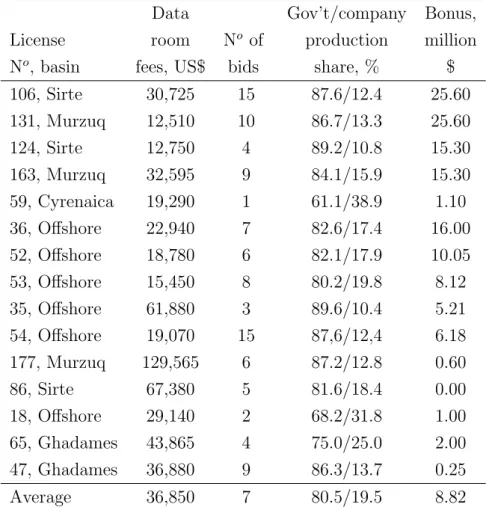

The competition of the first round biddings under the EPSA IV in 2005 was enormous with average of seven bids per licensed block and 15 blocks offered. The winning bids were between 61.1% and 89.6% reaching an average of 80.5%. The success of the bidding round was driven mainly by high oil prices. The results are summarized in the table below2.

2

Table 3: First Round EPSA IV 2005

Data Gov’t/company Bonus,

License room No of production million

No, basin fees, US$ bids share, % $

106, Sirte 30,725 15 87.6/12.4 25.60

131, Murzuq 12,510 10 86.7/13.3 25.60

124, Sirte 12,750 4 89.2/10.8 15.30

163, Murzuq 32,595 9 84.1/15.9 15.30

59, Cyrenaica 19,290 1 61.1/38.9 1.10

36, Offshore 22,940 7 82.6/17.4 16.00

52, Offshore 18,780 6 82.1/17.9 10.05

53, Offshore 15,450 8 80.2/19.8 8.12

35, Offshore 61,880 3 89.6/10.4 5.21

54, Offshore 19,070 15 87,6/12,4 6.18

177, Murzuq 129,565 6 87.2/12.8 0.60

86, Sirte 67,380 5 81.6/18.4 0.00

18, Offshore 29,140 2 68.2/31.8 1.00

65, Ghadames 43,865 4 75.0/25.0 2.00

47, Ghadames 36,880 9 86.3/13.7 0.25

Average 36,850 7 80.5/19.5 8.82

The EPSA IV also calls for some rules about the utilization of the local con-tent. The operator, for instance, must spend at least 50% of the budget on local equipment, services and inputs. The workforce must be totally national with ex-ception of the strategic management positions and the specialized labor in case it is not available in the country. Moreover, training programs must be developed by the operator so that the Libyans may hold top positions and replace the foreigners in most skilled segments where the local manpower is not plentifully prepared.

2.4

Angola

Although its first outstanding oil reserves had been discovered in the 1950’s, it was with the end of the civil war in 2002 that Angola, encouraged by the increase of its oil reserves and production, reached a significant economic growth. At present, the oil not only corresponds to half of Angola’s GDP but it also grants various loans to the government that uses the oil future volume as collateral.

Right after its independence, in 1976 the government created the Sonangol (Angola’s National Fuel Society) a state company that controls the oil exploration and production sector. Due to the civil war, Angola proved difficulties in the onshore exploration and was compelled to encourage the offshore exploration in search of the investment of oil companies that in partnership with the state company only played the role as operators.

At that time, the elaboration of the General Law of the Oil Activities was a great step forward in reserves and production. Although the law foresees other forms of association between Sonangol and the oil companies, the predominant model is the sharing production contract where Sonangol sometimes represents the State in decision-making and at times it acts as an operator jointly with the associated companies. In 2004, due to the alterations in the sector, the Law was revised in order to protect the national interests and to corroborate the main points from the former text.

The procedures concerning the choice of the partner companies happen through a bidding process and, in special cases, through a direct negotiation. The law also admits special bidding processes in which only small enterprises or those controlled by the Angolan citizens are involved. Thus, the proposals of the interested companies that fulfill the predetermined requirements are appraised by objective criteria and the winning company is determined.

The contractor’s remuneration is calculated as follow. From the gross revenue, is discounted the cost recovery that ranges from 50% to 65%. The costs are recovered in a particular order. First, development costs (uplift 50%), then, operating costs and, finally, exploration costs. The excess is the profit oil.

The share related to each rate of return is stipulated by the contract. The RoR is determined based on the accumulated net cash flow of each development area. Although there is no payment of royalties, from the contractor’s share is discounted the income tax of 50%.

Figure 2: Fiscal regime and profit oil split

The fiscal regime and oil profit split are summarized in the figure above.

The other peculiar difference is that the Law makes mandatory the sale of a production portion to the internal market so that the consumption in the market is guaranteed in case of a demand increase.

2.5

Trinidad and Tobago

The hydrocarbon resources and particularly its natural gas allowed Trinidad and Tobago to become the most industrialized Caribbean country. The foreign investment in the energy sector represents more than 90% of the country’s export revenues.

The first oil discoveries occurred in 1866 and the first relevant drilling happened in 1907. The oil production started out in 1908 and the first oil refinery was created in 1912. The offshore oil exploration set about in 1954.

The oil production had a peak hike totaling 230 thousand barrels a day in 1978 and was on a downturn until recently. In 2002, the production rose from an average of 113 thousand to a mean of 130 thousand barrels daily. Due to well discoveries in the latest years, production went up to 140 thousand barrels in a day in 2005 and in 2007 it leaped up to 145 thousand barrels.

The exploration and production licenses had been the principal legislative in-struments till 1970. Owing to the swiftest oil evolution, better management of contractual arrangements was necessary. In 1974, the first two production sharing contracts on Trinidad’s east coast were signed. These initial contracts did not fore-see a production portion to cover the recovery costs what allowed the government a production portion based on the production levels. Moreover, the costs recovery was ring-fenced, that is, each contract area is treated as a center to recover costs and for the taxes calculus.

In 1995, the World Bank production sharing contracts model was adopted. The new model incorporated the costs recovery and the government share was based on price and production level. The contracts also foresaw disavowal, relinquishment, minimum work programs, minimum obligations during the research period, incentive to the natural gas market development besides financial obligations as signature bonus, research and development and technical equipment bonus.

Similarly to the previous model, the contracts continue ring-fenced and assure a constant revenues flow to the government.

In 2005, an oil tax revision encouraged the creation of a new model called taxable production sharing contract .This contract has two principal characteristics that differ from the previous ones.

share of the oil profit when the oil price increases and, secondly, the consolidation of new contracts classified as deep water or onshore and shallow zone. Hence the consortium type investment became easier and the growing risks diminished.

Moreover, they introduced a special incentive that foresees a 40% increase on the exploration expenses in deep water.

In 2010, a new tax regime was approved aiming at improving competitiveness and attracting new potential investors locally and abroad. To fulfill such a goal they laid emphasis on the bidding process, on the terms and on the contractual conditions of the future competitive bidding rounds.

Such contracts encourage the investment in deep water zones. The petroleum profits tax rate was decreased from 50 % to 35%. An important feature of the model is that it provides tax stability to the companies.

The matrices for the government participation in profit oil are open for bids by the companies and the prices and production to these matrices ranges reflect the expected price and the costs atmosphere.

In recent contracts, the main terms are:

• Participants intending to bid shall pay a pre-bid application fee (US$ 50.000,00 in the 2013 bidding round);

• In addition to the pre-bid application fee, a bid application fee shall be payable (US$ 60.000,00 in the 2013 bidding round);

• In case of a tie, each bidder shall be required to bid a signature bonus;

• A bid shall contain proposals in respect of

– a technical and commercial evaluation of the block;

– a Minimum Work Programme;

– a Minimum Expenditure Obligation;

– proposals for the sharing of petroleum produced.

Production Tier Oil Price Class

A B C D

Production up to 75000 B/D x x x x

In excess of 75000 B/D and

x x x x

up to 100000 B/D

In excess of 100000 B/D and

x x x x

up to 150000 B/D

In excess of 150000 B/D and

x x x x

up to 200000 B/D

Greater than 200000 B/D x x x x

Price Class A refers to Government’s share for a crude cil price less than or equal to US$50.00 per barrel.

Price Class B refers to Government’s share for a Crude Oil price greater than US$50.00 per barrel but less than or equal to US$75.00 per barrel.

Price Class C refers to Government’s share for a Crude Oil price greater than US$75.00 per barrel but less than or equal to US$100.00 per barrel.

Price Class D, Crude Oil price greater than US$100.00 per barrel, the Govern-ment’s share of Profit Crude Oil is equal toBR+ 70%[(P−U S$100)/P](1−

BR) where BR refers to the Base Rates set out in Price Class D, and P is the Crude Oil price.

• Contractor shall recover costs to the extent of and out of 80% of all Available Crude Oil (crude oil produced and saved from the contract area and not used in Petroleum Operations).

In the last deep water competitive bidding round, six blocks were offered. Only three bids were received for two blocks:

• TTDAA 3

– BHP Billiton/BG International

– Repsol

• TTDAA 7

The consortium BHP Billiton/BG International won in both areas. Total investment for both blocks is planned at approximately US$250 million. Now, there are nine deep water blocks operating under production sharing contracts.

2.6

Venezuela

Venezuela is the world’s tenth biggest oil producer and the country possesses one of the most wide-ranging planet’s oil reserves. The country has been OPEC’s member since its foundation and is only backed up by Ecuador as a South America representative at the Organization. Its economy is totally dependent on oil and extremely controlled by state companies in various sectors.

In mid-20th century, Venezuela began its oil industry nationalization process as other Latin America countries. However, it was in 1958 that this process gained strength. The suspension of the ongoing concession renewals and the signatures of new contracts led to the progressive oil nationalization in the country.

In 1975, Petr´oleos de Venezuela S.A (PDVSA) was created, a state company responsible for the coordination and supervision of the oil activities. In 1976, the government formally announced the nationalization closing the doors to private in-vestments. PDVSA assumes the activities and takes in charge a national and inter-national expansion process.

However, in the late 1980’s with the low oil price and Venezuela’s growing debt, PDVSA had no resources to accomplish the necessary investments to guarantee the production growth and even to avoid its collapse because at that time many wells had already reached the top limit.

The openness process starts slowly in 1992 with the signature of services con-tracts to recover marginal fields and to reactivate the inactive ones. By and large, Venezuela adopts the Joint Ventures regime, but in June 1995 an alteration in the Nationalization Law allowed new covenants to explore ten new oil production geo-graphic areas adopting the production sharing model.

This mixed enterprise has the scope of directing, coordinating and supervising the activities in exploration, production, transportation and trading.

The investors themselves, under the agreed terms and conditions, assume the risk of the exploration activities based on the established Exploration Plan. Once the plan is fulfilled, the continuation of the blocks or areas exploration must be approved by a committee. The ones who are not approved leave the covenant and return to the management of CVP.

If the investors find hydrocarbon deposits they must define their traits and the marketability of the discoveries based on an Evaluation Plan. Once the plan is executed, the investors must define the commercial exploration feasibility and present a Development Plan.

Once the Development Plan is approved, the subsidiary and the investors es-tablish a consortium in which the CVP will have a 35% participation to finance the project. However, if the branch deems necessary, it may reduce its participation up to 1%. The resulting production will be traded in the international market by the investors and the branch according to its participation in the consortium at export prices and on the best possible conditions.

The operational costs, depreciation and taxes will be deducted from the gross income. From the remaining, before the income tax deduction, will be paid to the subsidiary to be transferred to the State after its costs deduction, the Participation of the State in the profits (PEG). The lower PEG limit is determined by the investors at the moment of the bidding and it may not be more than 50%. The investor who offers the highest percentage to the State is the bidding winner. In case of a draw, the signature bonus value breaks the tie.

The bidding procedure produced, initially, to PDVSA a profit of US$260 mil-lion from which 245 milmil-lion were collected with the signature bonuses and 15 milmil-lion arising from the sale of packages supplying geological information about the areas to be auctioned.

3

Rules for the Libra Oil Field Auction

The auction of the Libra oil field, the largest oil reserve in Brazil, was the first test of the new regime for exploration and production, which has suffered much criti-cism and was the target of pessimistic forecasts. Some of them have been confirmed, others minimized with the first round.

In addition to the general rules imposed by Law No. 12.351, the tender protocol defined the parameters for the first round. It was confirmed that Petrobras must join the winning contract with a minimum participation of 30%. Any company interested in participating in the bidding process must pay a participation fee of R$ 2,067,400.00. The signature bonus was set at R$ 15 billion.

The minimum bid was set as 41.65%. The amount of oil to be given to the Union depends, besides the bid, on the Brent oil price and the average daily produc-tion. More specifically, the offered bid defines the share of government in a scenario where Brent oil price ranges between US$ 100.01 and US$ 120.00 and average daily production ranges between 10,000.01 barrels/day and 12,000 barrels/day.

If Brent oil price or average daily production decrease, a percentage is deducted from the offered bid. The opposite occurs if the price or the production increase. Therefore, in the worst scenario, where Brent oil price is less than 60 US$/bbl and the average production is less than 4,000 bbl/day, the share of the Union is the offered bid minus 31.72%. In the best scenario, where Brent price is higher than 160 US$/bbl and daily production is higher than 24,000 bbl, the share of the Union is the offered bid plus 3.91%.

The amount of cost oil recovered cannot exceed 50% of gross revenue from production during the first two years and 30% of gross revenue in the subsequent years. Royalties are paid monthly and are equivalent to 15% of production of oil and natural gas during the month.

The minimum local content required in the exploration phase is 37%. In the development phase, the minimum percentage will be 55% for modules starting until 2021 and 59% for modules starting after 2022.

3.1

Results from Libra Oil Field Auction

The consortium is formed by Petrobras (40%), the French oil company To-tal (20%), the Anglo-Dutch Shell (20%) and two Chinese state-owned companies, CNOOC (10%) and CNPC (10%). The winning bid was the minimum stated by the tender protocol, 41.65%.

It was expected a more aggressive participation of Chinese state-owned enter-prises that, in order to meet their demand for oil, would be willing to give higher bids, putting Petrobras in a tricky financial situation. The prediction was not confirmed since the consortium emerged victorious with the minimum bid.

The winning bid has generated divergent opinions. From the point of view of government, it was not a success. On the other hand, it is a relief to Petrobras. Getting a larger share of the profits, may have softened its cash problems as well as increase its investment capacity, as it needs to be able to operate the fields, an activity that take place exclusively.

The exclusivity of operations, the possibility of a strong state intervention through Pre-Sal Petroleo SA (PPSA), created to monitor the exploratory process, and local content rules, that can generate inefficiency if the local market does not meet demand and deadlines, may be cited as the main reasons for the absence of the largest companies of the sector. These factors limit the choices of firms during the exploratory process and make the project less attractive.

Moreover, the unprecedented and complex model also discourages the partici-pation of industry’s giants and attracts mainly state companies from countries with high energy demand, looking primarily for oil reserves and not maximum profit.

Still, the winning consortium has two major European private companies, as well as two Chinese state-owned. Thus, the concern with undesirable partners for Petrobras was put in the background.

The government must solve important questions in relation to the rules that will define the next rounds of the pre-salt layer. It is quite obvious the need to attract the major oil companies that have decided not to run in the Libra field auction on the eve of the deadline for the payment of the participation fee. On the other hand, changing the rules for the next pre-salt auctions can weaken the regulatory framework and generate distrust by investors.

4

Related Literature

It is known that, in practice, some asymmetry between the participants is very common. It is reasonable to believe that some of them have greater interest in the object being auctioned. This is the case, for example, of incumbent companies in the sector where the auction takes place, since they already have the infrastructure and expertise in the field. Or, as previously mentioned, the case of countries like China that have high energy demand. The literature that discusses this case is called almost common value auctions. In these auctions, bidders receive an unbiased signal about the value of the object, which is unknown. All participants have the same ex post utility over the object, except one of them, whose valuation in case of victory is greater than the others.

Although it is not obvious that a small asymmetry in the valuation of the object has great impact on the outcome of auctions, we find in the literature several papers showing that, under certain conditions, it is crucial in determining the price and the winning bidder.

Underlying this effect is what the literature calls winner’s curse. The partic-ipant who naively bases his bid on unconditional expectation of the value of the object, that is, in his own estimation, ignores the fact that he will only be the win-ner if his estimate is one of the largest. In other words, conditional on the event of winning, the participant will be overestimating the value of the item. Unless the bidding strategy considers this inherent adverse effect of winning the auction of an object of unknown value, the winning bid will produce smaller or even negative profit.

This feature is more problematic in second price auctions. In this model, the winner is the participant that gives the higher bid, but the price paid is the second highest bid.

Given his benefit, the advantaged participant’s bids3are more aggressive, so the

risk to suffer from the winner’s curse is higher for the other competitors. Then, the other participants become more conservative, giving lower bids and thus decreasing the likelihood of the winner’s curse happen to the advantaged participant, who gives even more aggressive bids, and so on.

Several articles show that in this case, the advantaged participant always wins

3

and the revenue of the auctioneer reduces drastically, since the price paid is the second highest, that is small because of the effect explained above. Among them are Bikhchandani (1988), Avery & Kagel (1997) andKlemperer (1998).

However, this explosive effect does not occur if there are more than two par-ticipants. Levin & Kagel (2005) shows that in this case the advantaged participant does not always win and changes in strategies are proportional to the size of the asymmetry. Therefore, there is a proportional reduction in the revenue.

Intuitively, with more than a regular participant, to prevent the winner’s curse due to the aggressiveness of the advantaged participant there is no need to lower the bid so much because there is the possibility of winning the auction with a draw with another regular participant, increasing his expected revenue.

In first price auctions, which is the Brazilian case, the effect of this asymmetry is more uncertain. As we shall see, the advantaged participant is more likely to win in this type of auction, but he cannot adopt the strategy of giving very aggressive bids, since your bid determines the price.

Thus, the less aggressive bids from the advantaged participant reduces the winner’s curse faced by regular one, which encourages him to make higher offers increasing his probability of winning the auction.

In other words, when the advantaged participant gives a more aggressive bid, the regular player wants to give lower bids, since in case of victory, his marginal profit is lower. On the other hand, since his probability of winning is smaller, the cost of increasing the bids is lower. Therefore, the argument used previously does not apply to the case of first price auctions.

Avery & Kagel (1997) shows that, for small asymmetries, there is an equilib-rium in which the bids of participants are very close to the bids in the symmetric case. Hence, the expected revenue of the auctioneer is very close to the revenue of the common value model.

De Frutos & Jarque (2007) give us some interesting results too. They found that for small asymmetries

• The advantaged participant is more likely to win;

• The probability of winning is sensitive to the size of comparative advantage;

• The profit of advantaged participant is strictly increasing in the asymmetry. The opposite occurs with the regular participant.

In their model, for large asymmetries, they found that the advantaged partic-ipant always wins.

In terms of expected revenue of auctioneer, the effect is, in principle, am-biguous. The expected payment of the advantaged participant increases with the asymmetry since both the probability of winning as the equilibrium bid increase. The expected payment of regular player is decreasing with the asymmetry for sig-nals sufficiently pessimistic. However, for the most optimistic regular participant, his bid increases with the asymmetry.

Solving the model, they found that a small asymmetry has just a small impact over the expected revenue. In addition, we have that a small asymmetry is actually a benefit to the auctioneer.

Although the literature does not consider this issue as a very relevant problem in the case of first price auctions, another characteristic of the Brazilian model may change this analysis. The compulsory participation of Petrobras in the auction and, even more, their participation in the contract even in case of defeat may aggravate the situation in which a participant is very aggressive.

Petrobras may be required to explore an area that does not judge interesting in a contract that does not seek profitability and delivery much of the profit oil to the government.

In the literature of asymmetric information, we have the article from Milgrom & Weber (1982), based on Wilson (1967), Weverbergh (1979) and Engelbrecht-Wiggans et al.(1983). They consider a sealed first-price common value auction with two participants, where agent A observes a private signal and agent B has access only to public information. The paper analyzes the incentives of participants in acquiring private information about the value of the good auctioned, considering the possibility of doing it secretly or not. They show that the expected revenue of the auctioneer increases when the asymmetry between participants decreases.

5

Profit-Share Bidding Model

To analyze more specifically the proposed new regulatory framework, we will develop a profit-share bidding model that will allow us to establish the consequences of the presence of strategic participants in this environment.

Consider two agents competing in a common value first price auction of an area whose operating profit v is unknown ex ante. Suppose that v is a realization of a random variable V with cumulative distribution function H(·) and probability density function h(·).

Each agent observes a private unbiased signalsabout the operating profit, that is, each signal is a realization of a random variableS|v, conditional to the true value of v, whose conditional probability density function g(·|v) is such that E[s|v] = v. Moreover, distribution of signals is common knowledge.

Each participant must bid a fraction of any positive profits received as a result of winning the auction. This fraction is a function of the observed signal and the winner will be the firm that offer the government the higher share. Moreover, the winner will have to pay an exogenous signature bonus B, which is known to all participants.

5.1

Profit-share Bidding Model with Almost Common Value

We consider that one agent is a strategic participant and has a private ad-vantage over the other, the regular one, in the sense that, for any realization of v, derives more utility in case of win the auction4.

More specifically, the bidder’s payoff are represented by the functions Pi : [0,1]×[0,1]→R,i=r, a:

Pr(br, ba) =

0 if br ≤ba

[min{(1−br)v, v} −B] ifbr > ba

(1)

4

Pa(ba, br) =

0 if bp < br

v/α1−B if ba≥br andv ≤0

α2(1−ba)v−B if ba≥br andv >0

(2)

where br e ba are bids from regular and advantaged participants, respectively, and

α1 e α2 are both greater than one. In the case whereα1 =α2 = 1, we have a model

with symmetric agents.

Note that the winner does not share negative profits with the auctioneer, that is, if the realization of V is less than 0, he assumes the loss. Moreover, in case of defeat, the payoff of both participants is zero.

5.1.1 Characterization of equilibrium

We want to find an equilibrium (br(·), ba(·),s˜r,s˜a) such that the agent i=r, a participates only, and if only, si ≥ ˜si and br(˜sr) = ba(˜sa) = 0, where (˜sr,s˜a) are the signs that make agents indifferent between not participate in the auction and participate with bid equal to zero.5 So, we have to solve

Z ˜sa

−∞

Z ∞

−∞

[v−B]k(˜sr, u, v)dvdu=0

Z ˜sr

−∞

Z 0

−∞

[v/α1−B]k(u,s˜a, v)dvdu+

Z sr˜

−∞

Z ∞

0

[α2v−B]k(u,s˜a, v)dvdu = 0 (3)

wherek(sr, sa, v) =gr(sr|v)ga(sa|v)h(v).

The objective of participants is to choose bids bi ∈ [0,1], i = {r, a} that maximize their expected payoff. Therefore, if ba(·) is the strategy of agent a, the problem faced by the regular participant is to choose, for every sr ∈ R, br ∈ [0,1]

5

We are supposing that equilibrium functions ba(·) e br(·) are differentiable and strictly

such that his expected payoff is maximized:

max br

(

Z b−a1(br)

−∞

Z ∞

−∞

[min{(1−br)v, v} −B]gr(sr|v)ga(u|v)h(v)dvdu

)

(4)

Analogously, if br(·) is the strategy of regular participant, the problem of the advantaged is to choose for every sa ∈R,ba∈[0,1] that maximizes:

max ba

(

Z b−r1(ba)

−∞

Z 0

−∞

[v/α1−B]gr(u|v)ga(sa|v)h(v)dvdu

+

Z b−r1(ba)

−∞

Z ∞

0

[α2(1−ba)v−B]gr(u|v)ga(sa|v)h(v)dvdu

)

(5)

5.1.2 First-order conditions

Differentiating in br the equation (4) and equating to zero we obtain

Z b−a1(br)

−∞

Z ∞

0

−v h(v)gr(sr|v)ga(u|v)dvdu+

+

Z ∞

−∞

[min{(1−br)v, v} −B]h(v)gr(sr|v)ga(b−a1(br)|v)dv×(b−a1)′(br) = 0

(6)

Since in equilibrium br =br(sr),

(b−a1)′(br(sr)) =

Rb−a1(br(sr))

−∞

R∞

0 vh(v)gr(sr|v)ga(u|v)dvdu

R∞

−∞[min{(1−br(sr))v, v} −B]h(v)gr(sr|v)ga(ba−1(br(sr))|v)dv (7)

Z b−11(ba)

−∞

Z ∞

0

−α2v h(v)ga(sa|v)gr(u|v)dvdu+

+

Z ∞

0

[α2(1−ba)v−B]h(v)ga(sa|v)gr(b−r1(ba)|v)dv×(b

−1

r )

′(ba)+

+

Z 0

−∞

[v/α1−B]h(v)ga(sa|v)gr(br−1(ba)|v)dv×(b−r1)′(ba) = 0 (8)

In equilibrium, we have ba=ba(sa) and we get the following system:

(b−1

a )′(br(sr)) =

Rb

−1

a (br(sr))

−∞

R∞

0 vh(v)gr(sr|v)ga(u|v)dvdu

R∞

−∞[min{(1−br(sr))v,v}−B]h(v)gr(sr|v)ga(b −1

a (br(sr))|v)dv

(b−1

r )′(ba(sa)) =

Rb

−1

r (ba(sa))

−∞

R∞

0 α2v gr(u|v)ga(sa|v)h(v)dvdu

R0

−∞

h

v α1−B

i

k(b−1

r (ba(sa)),sa,v)dv+

R∞

0 [(1−ba(sa)+α2)v−B]k(b −1

r (ba(sa)),sa,v)dv (9)

Since we have that, in equilibrium, range(br(·)) = range(ba(·)), we can rewrite the system makingx=br(sr) =ba(sa) and obtain the following system of differential equations:

(b−r1)′(x) =

Rb−r1(x)

−∞

R∞

0 α2v gr(u|v)ga(b −1

a (x)|v)h(v)dvdu

R0

−∞

h

v α1 −B

i

f(x, v)dv+R∞

0 [(1−x+α2)v−B]f(x, v)dv

(b−a1)′(x) =

Rb−a1(x)

−∞

R∞

0 v gr(b−r1(x)|v)ga(u|v)h(v)dvdu

R∞

−∞[min{(1−x)v, v} −B]f(x, v)dv

(10)

wheref(x, v) =gr(b−1

r (x)|v)ga(ba−1(x)|v)h(v).

An analytic solution to this problem seems to be impracticable. Therefore, we will present a numeric solution. To do this, we must assign values to the parameters and specific distributions for random variables.

Suppose that V ∼ N(µ, σ2

profit estimated by agent i before participating in the auction. The values of the distributions’ parameters are based on the work of Reece (1979). The average of v

is adjusted so that the probability of positive profits (excluding signature bonus) is 15%, ie, P(V ≥0) = 0.15. Thus, µ=−1.466.

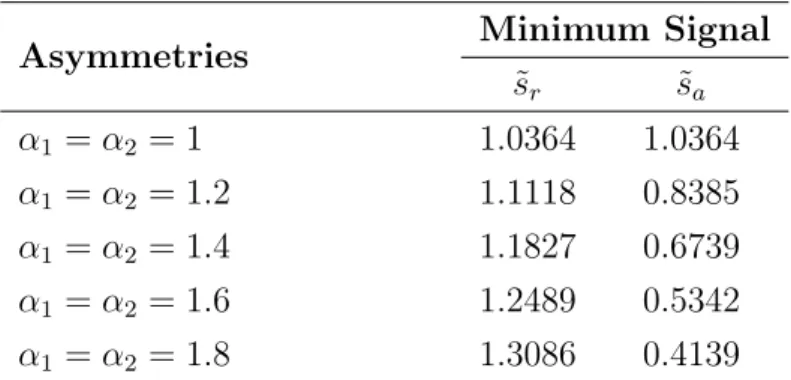

Table 4: Minimum signals for participation with positive bids

Asymmetries Minimum Signal

˜

sr s˜a

α1 =α2 = 1 1.0364 1.0364

α1 =α2 = 1.2 1.1118 0.8385

α1 =α2 = 1.4 1.1827 0.6739

α1 =α2 = 1.6 1.2489 0.5342

α1 =α2 = 1.8 1.3086 0.4139

Variance of signals is 0.8 and signature bonus equal to 0.1.

Table4provides, for each value ofα1 and α2, the minimum signal above which

agents are willing to participate with positive bids. Note that, when α1 = α2 = 1,

that is, when participants are identical, minimum signal is the same for both. As the asymmetry is accentuated, that is, α1 e α2 increase, minimum signal for the

advantaged participant decreases, while the signal for the regular one increases. In other words, the advantage in utility makes the advantaged participant more aggressive, making him willing to participate in the auction even if his signal is not so optimistic. The regular participant, on the other hand, becomes increasingly prudent, demanding higher signals to participate in the auction.

Furthermore, the advantaged participant is more aggressive in the sense that, for the same value of the signal, his bid is higher than the regular’s bid. The table below illustrates this fact:

6

Table 5: Bids for each signal

Signal Bid

Regular Advantaged

sr =sa= 1.0746 0 0.0897

sr =sa= 1.25 0.0972 0.1865

sr =sa= 1.5 0.2097 0.3005

sr =sa= 1.75 0.2967 0.3928

sr =sa= 2 0.3639 0.4706

Variance of signals is 0.8, signature bonus equal to 0.1 and

α1=α2= 1.1

Another effect we can observe is that, given a signal, bids from the advantaged firm increase with the private benefit, that is, the greater are the values ofα1 and

α2. The regular participant, on the other hand, gives lower bids as the advantage of

the other participant increases.

As we saw in section4, because it is a first-price auction, we have that responses of the bids to variations on private benefit are proportional to it. To show this, we will fix a signal to each participant and will analyze the value of bids. The table below shows the results.

Table 6: Bids for each asymmetry

Asymmetries Bid

Regular Advantaged

α1 =α2 = 1 0.2363 0.0386

α1 =α2 = 1.1 0.2097 0.1047

α1 =α2 = 1.3 0.1640 0.2290

α1 =α2 = 1.4 0.1441 0.2893

α1 =α2 = 1.5 0.1258 0.3310

Variance of signals is 0.8, signature bonus equal to 0.1 and

sr= 1.5 esa = 1.1.

It remains to consider what these changes in strategies entail in terms of ex-pected payoff, both for participants and for the government.

advantaged participant, the higher is his expected payoff. The opposite occurs with regular participant.

Figure 3: Expected payoff of participants

With respect to government revenue, we see in the graphic above that for small asymmetries, the revenue increases compared to the case without private advantage. Although it is somewhat counterintuitive, we found similar results in the literature, for example inDe Frutos & Jarque(2007). As the asymmetry increases, the expected revenue of government decreases. This result is in line with what we saw in the table (6). In fact, when the private benefit increases, one participant gives higher bids than in the symmetric case and the other gives lower bids. Weighting by the probability of each participant win, it is possible that, with small asymmetries, the aggressiveness of advantaged participant offset the lower bids from regular participant.

We concluded in our model that all theoretical predictions for models of con-cession auctions are confirmed when we analyze the profit-share bidding auction, i.e., the advantaged participant is more aggressive the greater his private benefit, regular participant is more cautious and the movement of the expected revenues are proportional to size of asymmetry.

5.2

Profit-share Bidding Model with Asymmetric

Informa-tion

In this section, we will continue to study cases where participants are treated asymmetrically. Here, an agent has access to more information than the other competitors.

The main reason for this approach is the situation of Petrobras in the auction of pre-salt blocks. Besides acting for over five decades in Brazil and being considered a world leader in oil production in deep water technology, Petrobras was the main responsible for the discovery of potential oil reserves in the crust of salt in Brazil. Therefore, it is reasonable to consider that the Brazilian company has a much more detailed knowledge of the pre-salt areas than any other oil company in the world.

To consider this property in the model described in section above, we will make the assumption that one agent receives a more precise estimative about the value of the auctioned area. This notion of precision will be defined as lower variance in distribution of signal, although there is in literature many other ways to do this. This asymmetry should cause changes in the strategies of participants, changing the equilibrium and, consequently, the expected payoffs.

behavior of the expected gains of participants and the expected revenue of the auc-tioneer when the difference in precision of signal increases. We will consider the presence of a advantaged participant in this framework ahead.

Again, we have an object being disputed by two agents through a share-bidding auction whose value v comes from a random variable V with density h(v). Each participant offers a sealed bid bi ∈ [0,1], i = {1,2} and the author of the higher bid wins the auction. The bid is based on a signal si observed by the agent i. This unbiased signal is a realization of the random variable Si|v with conditional probability density functiongi(·|v).

As previously assumed, V ∼N(µ, σ2v) and Si|v ∼N(v, σi2) and we interpret v and si|v as described above.

We have that, the smaller the variance of the unbiased signal, the greater the precision of the estimation of the realized value ofV.

The payoffs of agents 1 and 2 are described by functionsPi : [0,1]×[0,1]→R:

Pi(bi, bj) =

0 if bi ≤bj

[min{(1−bi)v, v} −B] ifbi > bj

wherei, j ∈ {1,2}, i6=j.

5.2.1 Characterization of equilibrium

We want to find an equilibrium (bi(·),s˜i), i= 1,2, such that agentiparticipates only, and if only,si ≥˜si and bi(˜si) = 0. We have that ˜si is defined by equations

Z sj˜

−∞

Z ∞

−∞

[v−B]gi(˜si|v)gj(u|v)h(v)dvdu = 0 i, j ∈ {1,2}, i6=j (11)

When observes si, participant i must chooses bi that maximizes his expected payoff given by the expression below:

Z b−j1(bi)

−∞

Z ∞

−∞

5.2.2 First-order conditions

We will solve the problem of agent 1. The problem of agent 2 is analogous.

Differentiating in b1 the expected revenue and equating to zero we get

Z b−21(b1)

−∞

Z ∞

0

−v h(v)g1(s1|v)g2(u|v)dvdu+

+

Z ∞

−∞

[min{(1−b1)v, v} −B]h(v)g1(s1|v)g2(b−21(b1)|v)dv×(b−21)′(b1) = 0

(13)

Since in equilibrium b1 =b1(s1),

(b−21)′(b1(s1)) =

Rb−21(b1(s1))

−∞

R∞

0 vh(v)g1(s1|v)g2(u|v)dvdu

R∞

−∞[min{(1−b1(s1))v, v} −B]h(v)g1(s1|v)g2(b −1

2 (b1(s1))|v)dv

(14)

An analogous equation is obtained from the problem of agent 2.

Using the fact that, in equilibrium, range(b1(·)) = range(b2(·)), we can rewrite

the equations makingx=b1(s1) =b2(s2) and obtain the following system of

differ-ential equations:

(b−j1)′(x) =

Rb−j1(x)

−∞

R∞

0 v gi(b −1

i (x)|v)gj(u|v)h(v)dvdu

R∞

−∞[min{(1−x)v, v} −B]gi(b −1

i (x)|v)gj(b

−1

j (x)|v)h(v)dv

(15)

wherei, j ∈ {1,2}, i6=j.

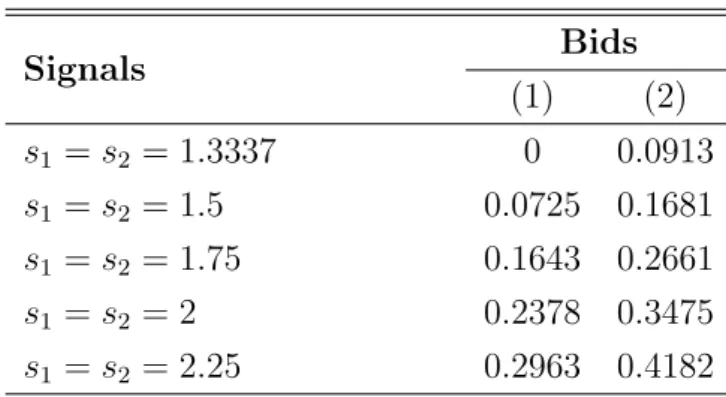

Again, an analytical solution do not seems possible. We will solve numerically using the same values used previously for the parameters, except for the variance of the signals which is the object of study in this section.

more informed, he requires a less optimistic signal to participate. The other one, in turn, need increasingly optimistic signals.

Table 7: Minimum signals for participation with positive bids

Variances Minimum signals

˜

s1 s˜2

σ2

1 = 1.1, σ22 = 1.1 1.2858 1.2858

σ2

1 = 1.1, σ22 = 1.0 1.3338 1.1606

σ2

1 = 1.1, σ22 = 0.9 1.3913 1.0366

σ2

1 = 1.1, σ22 = 0.7 1.5467 0.7939

σ2

1 = 1.1, σ22 = 0.5 1.8054 0.5624

Defineα1=α2= 1 and signature bonus equal to 0.1.

The more informed participant appears more aggressive giving higher bids than the less informed participant when they receive the same signal. Intuitively, we know that the smaller the variance of the distribution, the more reliable the estimate. Knowing that the probability of the profit being much lower than the signal received is small, the informed player is willing to bid higher. We see this fact in the table below.

Table 8: Bids for each signal

Signals Bids

(1) (2)

s1 =s2 = 1.3337 0 0.0913

s1 =s2 = 1.5 0.0725 0.1681

s1 =s2 = 1.75 0.1643 0.2661

s1 =s2 = 2 0.2378 0.3475

s1 =s2 = 2.25 0.2963 0.4182

Define σ2

1 = 1.1, σ 2

2 = 1.0, signature bonus equal to 0.1 andα1=α2= 1

Figure 5: Expected revenue of government

Figure 6: Expected payoff of participants

5.2.3 Almost Common Value x Asymmetric Information

Now, we will develop a model in which the two asymmetries described above interact. In a model where one agent is strategic in the sense described in section

5.1 and the other is regular but more informed, we have that an effect can excel in relation to the other.

Table 9: Minimum signals for participation with positive bids

Asymmetries Minimum Signal

˜

sr s˜a

α1 =α2 = 1 0.7593 1.1778

α1 =α2 = 1.1 0.7865 1.0677

α1 =α2 = 1.3 0.8394 0.8784

α1 =α2 = 1.4 0.8652 0.7947

α1 =α2 = 1.7 0.9382 0.5803

Define σ2

r= 0.6, σ 2

a= 0.8 and signature bonus equal to 0.1.

Table 10: Bids for each signal

Signals Bids

Regular Advantaged

s1 =s2 = 0.8784 0.0311 0

s1 =s2 = 1 0.1203 0.0728

s1 =s2 = 1.25 0.2700 0.1999

s1 =s2 = 1.5 0.3844 0.2993

s1 =s2 = 1.75 0.4752 0.3763

Define σ2

r = 0.6, σ 2

a = 0.8, signature bonus equal to 0.1 and

α1=α2= 1.3

As previously said, the regular participant, more informed than the strate-gic one, requires lower signal to bid positively, provided that the advantage of his opponent is small. When this advantage increases, as in the example above, the information asymmetry is not capable to compensate. The same occurs with the bids.

In the table (10), we have an example where the information asymmetry is large enough to make the regular participant more aggressive. Increasing the advantage of the strategic participant, we have the opposite. The regular participant becomes more cautious about the bids.

the participants are qualitatively equal to the case without information asymmetry, except that for certain values, regular agent’s expected payoff is higher than the expected payoff of advantaged participant.

Figure 7: Expected revenue of government

We can conclude that Petrobras’ position as a world leader and active in Brazil gives to her information about the areas to be explored that may be sufficient to counteract the aggressiveness of a strategic participant, which aims not only profit, but also the reserves of oil as previously discussed. As Petrobras is able to participate in the auctions as it meets all the requirements, this might be a way of government to protect themselves from possible losses.

In addition, the other companies may choose to invest more in research that will make them more competitive in the process.

5.3

Profit-share bidding model with Compulsory

Participa-tion

According to the new law governing the exploration and production of oil, in case of absence in the auction or in case of loss, Petrobras must adhere at 30% to the winning contract. Therefore, its participation is compulsory.

We consider the model described in section 5 with two agents called regular and Petrobras and denoted byr and p, respectively.

Now, we consider that agentpgets a fractionλ∈(0,1) of the agent r’s contract in case of defeat in the auction. Therefore, the bidder’s payoff are represented by the functionsPi : [0,1]×[0,1]→R,i=r, p:

Pr(br, bp) =

0 if br ≤bp

(1−λ) [min{(1−br)v, v} −B] if br > bp

(16)

Pp(bp, br) =

λ[min{(1−br)v, v} −B] if bp < br

min{(1−bp)v, v} −B if bp ≥br

(17)

5.3.1 Characterization of Equilibrium

participate with bid equal to zero. So, we have to solve

(1−λ)E(V −B)ISp<sp˜ |Sr = ˜sr

= 0

E[(V −B)ISr<˜sr +λ(min{(1−br(Sr)V, V} −B)ISr≥˜sr|Sp = ˜sp] =

λE[(min{(1−br(Sr))V, V} −B)ISr≥sr˜ |Sp = ˜sp]

(18)

Rearranging, the system simplify to

E

(V −B)ISp<˜sp|Sr = ˜sr

= 0

E[(V −B)ISr<˜sr|Sp = ˜sp] = 0

(19)

Suppose bi differentiable and strictly increasing when the agent i participates (i.e. when si ≥s˜i). If bp(·) is the strategy of agent p, the problem of agent r is to choose, for everysr ∈R, z ∈[0,1] such that his expected payoff is maximized:

E(min{(1−z)v, v} −B)Iz>bp(Sp)|Sr =sr

=

=

Z b−p1(z)

−∞

Z ∞

−∞

[min{(1−z)v, v} −B]h(v)gr(sr|v)gp(u|v)dvdu.

(20)

Analogously, if br(·) is the strategy of agent r, the problem of agent p is to choose, for everysp ∈R, y∈[0,1] that maximizes the following expression:

E(min{(1−y)v, v} −B)Iy>br(Sr)|Sp =sp

+

+λE(min{(1−br(sr))v, v} −B)Iy<br(Sr)|Sp =sp

=

=

Z b−r1(y)

−∞

Z ∞

−∞

[min{(1−y)v, v} −B]h(v)gr(u|v)gp(sp|v)dvdu+

+λ

Z ∞

b−1

r (y)

Z ∞

−∞