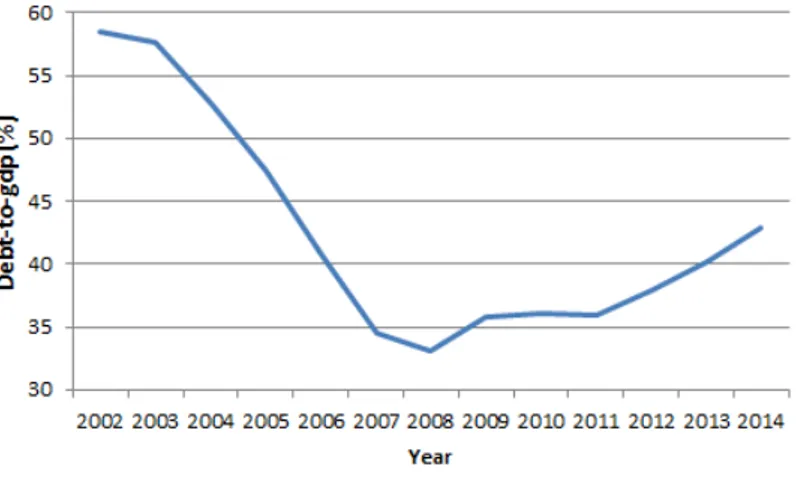

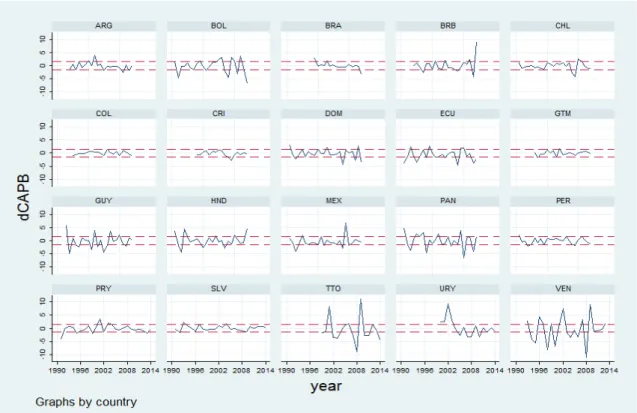

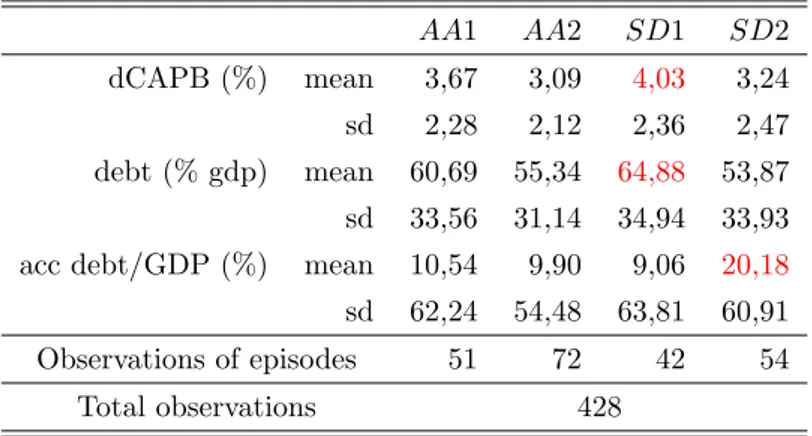

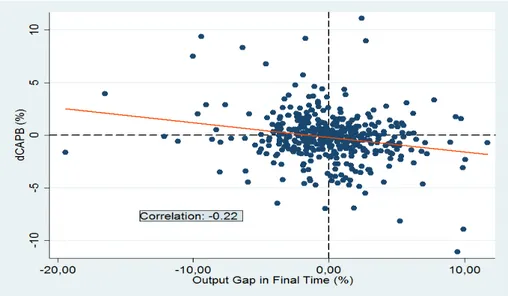

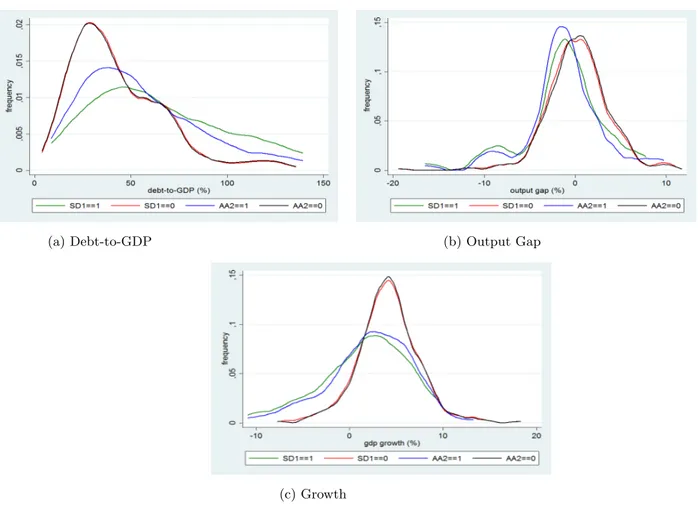

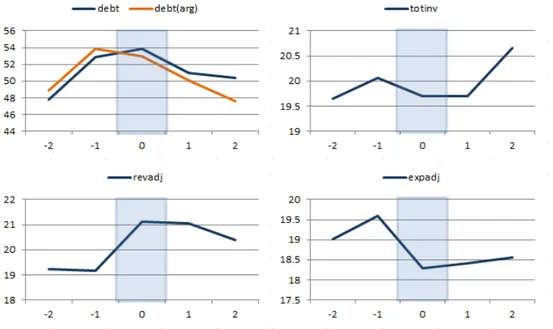

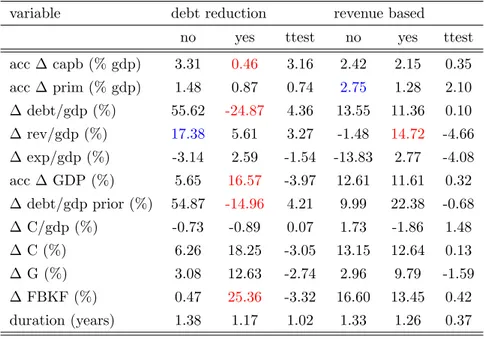

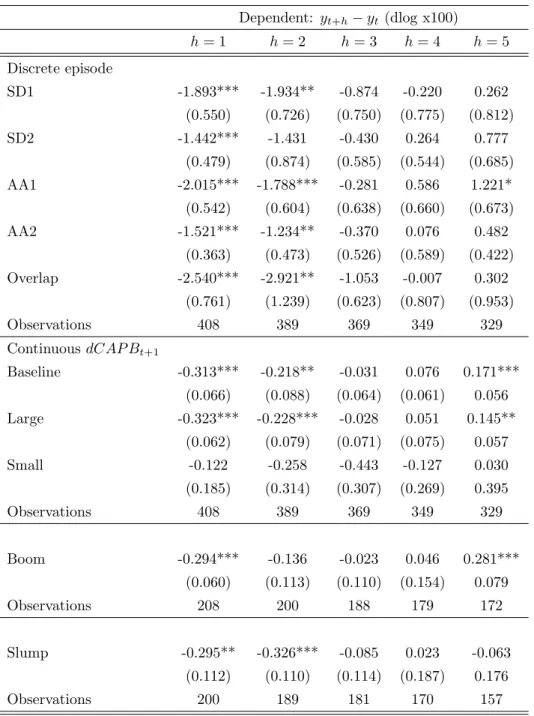

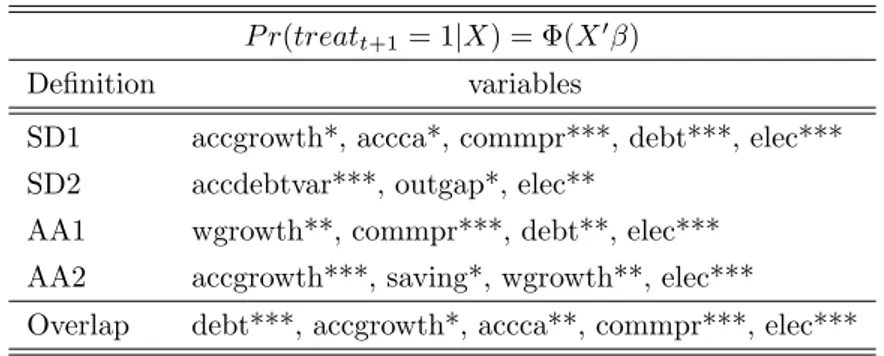

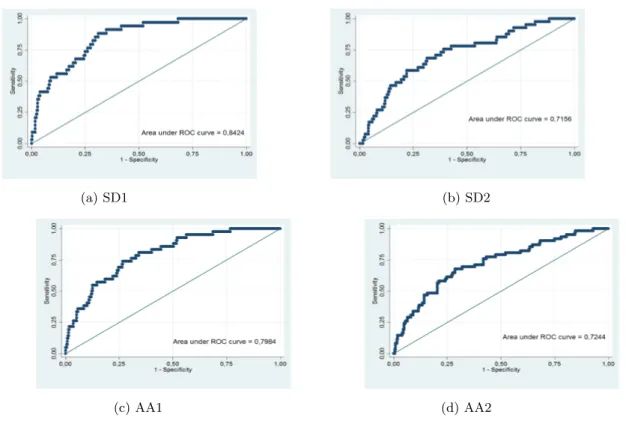

Effects of fiscal consolidations in Latin America

Texto

Imagem

Documentos relacionados

Mo- lecular epidemiology of clinical and environmental isolates of the Cryptococcus neoformans species complex reveals a high genetic diversity and the presence of the molecular

Assim, no que respeita ao grau de evolução do solo pode observar-se o seguinte: o Os minerais primários mais abundantes nos solos são o quartzo e os feldspatos –.. são os

In regard to mortality levels in children in the first years of life, Latin America and the Caribbean is in an intermediate position between the developed

O WIG-2004 deve poder voar em cruzeiro sem a acção do piloto, deve possuir um piloto automático, apresentar uma transição suave da água para o ar e ser capaz de operar em ventos de

Extinction with social support is blocked by the protein synthesis inhibitors anisomycin and rapamycin and by the inhibitor of gene expression 5,6-dichloro-1- β-

Using the data entered, the materials characteristics built in the database system, and the knowledge base on changes in prop- erties due to additional treatment, the

social assistance. The protection of jobs within some enterprises, cooperatives, forms of economical associations, constitute an efficient social policy, totally different from

This quick review of recent trends leads to the conclusion, that at least in the next few years, the attainment of HFA / 2000 in Latin America and the Caribbean will continue, as